Global Food Coating Market

Market Size in USD Billion

CAGR :

%

USD

5.04 Billion

USD

8.34 Billion

2025

2033

USD

5.04 Billion

USD

8.34 Billion

2025

2033

| 2026 –2033 | |

| USD 5.04 Billion | |

| USD 8.34 Billion | |

| % | |

|

Food Coating Market Size

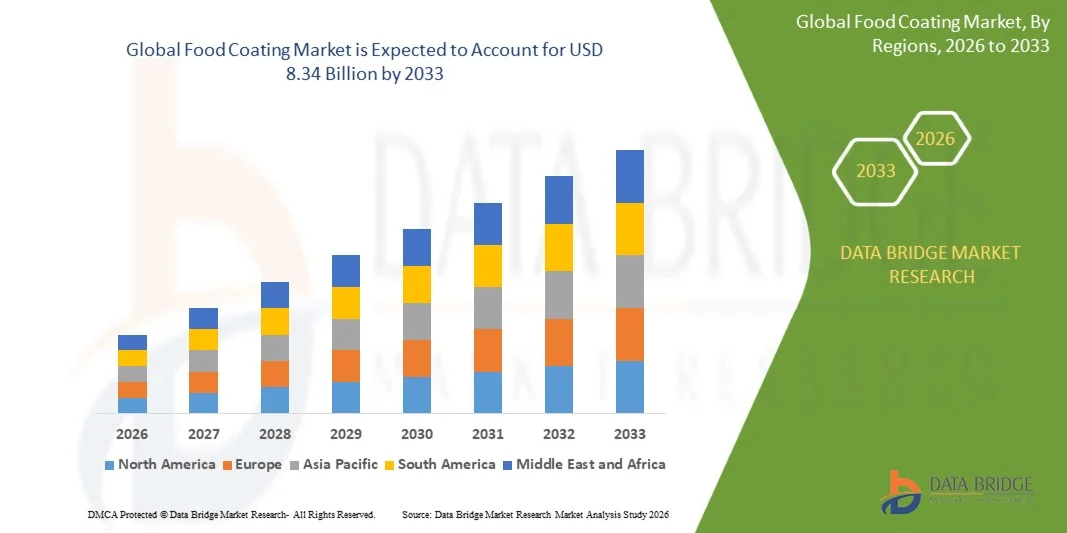

- The global food coating market size was valued at USD 5.04 billion in 2025 and is expected to reach USD 8.34 billion by 2033, at a CAGR of 6.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for processed and convenience foods across urban populations

- Rising consumer preference for enhanced taste, texture, and appearance in food products is supporting the adoption of advanced coating solutions

Food Coating Market Analysis

- The food coating market is experiencing steady growth driven by evolving consumer eating habits and the expansion of the global processed food industry, where coatings play a critical role in improving product appeal and shelf life

- In addition, technological advancements in coating ingredients and processes such as clean-label coatings and functional coatings are enhancing product innovation and enabling manufacturers to meet changing consumer preferences for healthier and premium food options

- North America dominated the food coating market with the largest revenue share in 2025, driven by the high consumption of processed and convenience foods, along with strong demand for ready-to-eat and frozen products

- Asia-Pacific region is expected to witness the highest growth rate in the global food coating market, driven by expanding food processing industries, changing dietary habits, and increasing consumption of ready-to-eat and snack products

- The batter segment held the largest market revenue share in 2025 driven by its extensive use in coating meat, seafood, and snack products to enhance texture, adhesion, and crispiness. Batter coatings provide a uniform layer and improve product appearance and taste, making them widely preferred in processed food applications. In addition, advancements in batter formulations such as gluten-free and low-oil variants are further supporting their adoption across health-conscious consumer segments. The versatility of batter in both fried and baked applications continues to strengthen its demand across global food processing industries

Report Scope and Food Coating Market Segmentation

|

Attributes |

Food Coating Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Bowman Ingredients (U.K.) • JBT Corporation (U.S.) |

|

Market Opportunities |

• Expansion Of Plant-Based And Vegan Food Products |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Food Coating Market Trends

“Rising Demand for Convenience and Ready-to-Eat Food Products”

• The increasing consumption of convenience and ready-to-eat food products is significantly shaping the global food coating market, as consumers seek quick, easy-to-prepare meal options without compromising on taste and quality. Food coatings play a vital role in enhancing flavor, texture, and visual appeal, making them essential in processed foods such as snacks, frozen products, and bakery items. This trend is strengthening demand for innovative coating solutions across food manufacturing industries

• Rapid urbanization, changing lifestyles, and busy work schedules are accelerating the demand for coated food products in both developed and emerging markets. Consumers are increasingly inclined toward products that offer extended shelf life and consistent quality, encouraging manufacturers to invest in advanced coating technologies and formulations that improve product durability and sensory attributes

• The demand for crispy, flavorful, and visually appealing food products is influencing product development, with manufacturers focusing on coatings that enhance crunchiness, moisture retention, and overall eating experience. This has led to the introduction of customized coatings tailored to specific applications such as meat, seafood, bakery, and snack products, supporting product differentiation and brand positioning

• For instance, in 2024, companies such as McCain Foods in Canada and Tyson Foods in the U.S. expanded their portfolios of coated frozen snacks and ready-to-cook products to meet rising consumer demand for convenience foods. These products were distributed through retail and foodservice channels and marketed based on taste, texture, and ease of preparation, contributing to increased consumer engagement and repeat purchases

• While demand for convenience foods continues to grow, sustained market expansion depends on continuous innovation, cost optimization, and maintaining product quality across large-scale production. Manufacturers are focusing on developing coatings that balance taste, texture, and nutritional value while ensuring scalability and efficiency in production processes

Food Coating Market Dynamics

Driver

“Growing Demand for Enhanced Texture and Flavor in Processed Foods”

• Increasing consumer preference for high-quality, flavorful, and textured food products is a key driver for the food coating market. Coatings are widely used to improve crispiness, mouthfeel, and overall sensory appeal, making them essential in a wide range of processed food applications. This trend is encouraging manufacturers to develop innovative coating solutions that cater to diverse consumer tastes and preferences

• Expanding applications across bakery, confectionery, meat, seafood, and snack segments are further supporting market growth. Food coatings help improve product stability, appearance, and shelf life while enhancing eating experience, enabling manufacturers to deliver consistent quality products to consumers

• Food manufacturers are actively investing in product innovation, marketing strategies, and partnerships to promote coated food products. These efforts are supported by increasing consumer demand for premium and indulgent food options, as well as the need to differentiate products in a competitive market landscape

• For instance, in 2023, companies such as Nestlé in Switzerland and General Mills in the U.S. increased the use of advanced coating technologies in snack and bakery products to enhance texture and flavor profiles. These initiatives were driven by rising demand for indulgent and high-quality food products, leading to improved brand positioning and customer retention

• Although demand for enhanced texture and flavor supports market growth, wider adoption depends on maintaining cost efficiency, ensuring ingredient availability, and meeting regulatory standards. Continuous innovation and investment in coating technologies will be crucial for sustaining long-term market growth

Restraint/Challenge

“Health Concerns Related to High Fat and Calorie Content in Coated Foods”

• Health concerns associated with high fat, calorie, and sodium content in coated food products present a significant challenge for the market. Consumers are becoming more health-conscious and are increasingly scrutinizing product labels, which may limit the consumption of heavily coated or fried foods. This trend is prompting manufacturers to reformulate products with healthier coating alternatives

• Regulatory pressures and nutritional guidelines are also influencing product development, as governments and health organizations emphasize reducing unhealthy ingredients in processed foods. Compliance with these standards can increase production costs and require continuous reformulation efforts, impacting profitability and product timelines

• Supply chain and ingredient sourcing challenges further affect market growth, as manufacturers need to ensure consistent quality and availability of coating ingredients. Fluctuations in raw material prices and the need for specialized ingredients can increase operational complexity and cost structures

• For instance, in 2024, food manufacturers in regions such as Europe and North America reported slower growth in certain coated food categories due to rising consumer preference for baked or minimally processed alternatives. Brands responded by introducing low-fat and air-fried coated products, but higher production costs and pricing challenges impacted overall adoption rates

• Addressing these challenges will require innovation in healthier coating solutions, improved ingredient sourcing strategies, and effective marketing to highlight nutritional benefits. Manufacturers must balance taste, texture, and health considerations while ensuring cost efficiency and scalability to sustain long-term growth in the global food coating market

Food Coating Market Scope

The market is segmented on the basis of ingredient type, ingredient form, equipment type, mode of operation, and application.

• By Ingredient Type

On the basis of ingredient type, the food coating market is segmented into Cocoa and Chocolate, Fats and Oils, Flours, Breaders, Batter, Sugars and Syrups, Salts, Spices, and Seasonings, and Others. The batter segment held the largest market revenue share in 2025 driven by its extensive use in coating meat, seafood, and snack products to enhance texture, adhesion, and crispiness. Batter coatings provide a uniform layer and improve product appearance and taste, making them widely preferred in processed food applications. In addition, advancements in batter formulations such as gluten-free and low-oil variants are further supporting their adoption across health-conscious consumer segments. The versatility of batter in both fried and baked applications continues to strengthen its demand across global food processing industries.

The spices and seasonings segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumer demand for diverse flavors and customized taste profiles. The growing popularity of ethnic cuisines and flavored snack products is encouraging manufacturers to incorporate innovative seasoning blends, enhancing product differentiation and consumer appeal. In addition, clean-label seasoning formulations and natural flavor enhancers are gaining traction among health-conscious consumers. Manufacturers are also focusing on regional flavor innovations to cater to localized taste preferences, further boosting segment growth.

• By Ingredient Form

On the basis of ingredient form, the food coating market is segmented into Dry and Liquid. The dry segment held the largest market revenue share in 2025 driven by its ease of storage, longer shelf life, and widespread use in breading and seasoning applications. Dry coatings are preferred for their cost-effectiveness and ability to provide consistent texture and crispiness across various food products. In addition, dry mixes are easy to handle and transport, making them suitable for large-scale food processing operations. Their compatibility with automated systems further enhances operational efficiency and production scalability.

The liquid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior adhesion properties and ability to form uniform coatings in industrial processing. Liquid coatings are increasingly used in batter applications and advanced processing techniques, supporting product consistency and scalability. In addition, innovations in liquid coating formulations such as reduced oil absorption and improved binding capabilities are enhancing their functional performance. The rising demand for premium and uniform-coated products is also contributing to the segment’s rapid expansion.

• By Equipment Type

On the basis of equipment type, the food coating market is segmented into Coaters and Applicators, Breader Applicators, Flour Applicators, Batter Applicators, Seasoning Applicators, Other Coaters and Applicators, and Enrobers. The coaters and applicators segment held the largest market revenue share in 2025 driven by their versatility and extensive use across multiple coating processes in large-scale food production. These systems enable efficient and uniform coating application, supporting high production volumes. In addition, advancements in automation and precision control technologies are improving coating consistency and reducing material wastage. Their integration with modern processing lines is further enhancing productivity and operational efficiency.

The enrobers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand in confectionery and bakery applications for chocolate and compound coatings. Enrobing technology allows precise coating control and enhances product aesthetics, making it suitable for premium and value-added products. In addition, manufacturers are investing in advanced enrobing systems to achieve higher efficiency and better product customization. The growing demand for premium confectionery and visually appealing bakery products is further supporting segment growth.

• By Mode Of Operation

On the basis of mode of operation, the food coating market is segmented into Automatic and Semi-Automatic. The automatic segment held the largest market revenue share in 2025 driven by increasing automation in food processing industries and the need for high efficiency and consistency. Automatic systems reduce labor costs and improve production speed, making them ideal for large-scale manufacturers. In addition, these systems ensure uniform coating quality and minimize human error, supporting large-volume production requirements. The adoption of Industry 4.0 technologies is further enhancing the performance of automatic coating systems.

The semi-automatic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its affordability and flexibility for small and medium-sized enterprises. These systems offer a balance between manual control and automation, making them suitable for diverse production requirements. In addition, semi-automatic equipment allows customization and easier handling for niche or low-volume production. Growing investments in small-scale food processing units are further contributing to segment expansion.

• By Application

On the basis of application, the food coating market is segmented into Meat and Seafood Products, Confectionery Products, Bakery Products, Bakery Cereals, and Snacks. The meat and seafood products segment held the largest market revenue share in 2025 driven by high consumption of coated fried and ready-to-cook products globally. Coatings enhance texture, flavor, and shelf life, making them essential in this segment. In addition, increasing demand for frozen and convenience meat products is further supporting segment growth. Manufacturers are also focusing on innovative coatings that improve product crispiness while reducing oil absorption.

The snacks segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for convenient and flavored snack products. Increasing consumption of chips, extruded snacks, and coated nuts is encouraging manufacturers to innovate with new coating technologies and flavor profiles, supporting market growth. In addition, the introduction of healthier snack alternatives with baked coatings and reduced fat content is gaining traction among consumers. The expansion of retail and e-commerce channels is further boosting the availability and demand for coated snack products.

Food Coating Market Regional Analysis

• North America dominated the food coating market with the largest revenue share in 2025, driven by the high consumption of processed and convenience foods, along with strong demand for ready-to-eat and frozen products

• Consumers in the region highly value product quality, texture, and taste enhancement, with food coatings playing a key role in delivering crispiness, flavor, and visual appeal across a wide range of food categories

• This widespread adoption is further supported by advanced food processing infrastructure, high disposable incomes, and continuous product innovation, establishing food coatings as a critical component in both retail and foodservice industries

U.S. Food Coating Market Insight

The U.S. food coating market captured the largest revenue share in 2025 within North America, fueled by the strong presence of leading food manufacturers and the growing demand for convenience and packaged foods. Consumers are increasingly prioritizing taste, texture, and premium-quality products, driving the use of advanced coating technologies. The expansion of quick-service restaurants and frozen food categories, along with continuous innovation in coating formulations, further supports market growth in the country.

Europe Food Coating Market Insight

The Europe food coating market is expected to witness steady growth from 2026 to 2033, primarily driven by increasing demand for high-quality bakery, confectionery, and processed food products. The rise in health-conscious consumers is encouraging manufacturers to develop clean-label and low-fat coating solutions. In addition, strict food safety regulations and a strong focus on product quality are fostering innovation and adoption of advanced coating technologies across the region.

U.K. Food Coating Market Insight

The U.K. food coating market is expected to witness notable growth from 2026 to 2033, driven by the rising demand for convenience foods and ready-to-cook meal options. In addition, increasing consumer preference for premium and innovative food products is encouraging manufacturers to invest in advanced coating techniques. The expansion of retail and online food distribution channels is further supporting market growth in the country.

Germany Food Coating Market Insight

The Germany food coating market is expected to witness significant growth from 2026 to 2033, fueled by strong demand for bakery and processed food products, along with increasing focus on product quality and innovation. Germany’s well-established food processing industry and emphasis on technological advancements are promoting the adoption of efficient coating equipment and ingredients. The growing trend of clean-label and sustainable food products is also influencing market expansion.

Asia-Pacific Food Coating Market Insight

The Asia-Pacific food coating market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, increasing disposable incomes, and changing dietary habits across countries such as China, India, and Japan. The growing demand for processed, ready-to-eat, and snack products is significantly boosting the adoption of food coatings. Furthermore, expanding food processing industries and rising investments in manufacturing capabilities are supporting market growth in the region.

Japan Food Coating Market Insight

The Japan food coating market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced food processing technologies and high demand for premium-quality food products. Consumers in Japan place significant emphasis on texture, presentation, and taste, driving the use of innovative coating solutions. The increasing popularity of ready-to-eat meals and convenience foods is further contributing to market expansion.

China Food Coating Market Insight

The China food coating market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid urbanization, a growing middle-class population, and increasing consumption of processed and convenience foods. China stands as one of the largest food processing markets, with strong demand for coated meat, seafood, and snack products. The availability of cost-effective manufacturing and continuous product innovation are key factors propelling the market in China.

Food Coating Market Share

The Food Coating industry is primarily led by well-established companies, including:

• Bowman Ingredients (U.K.)

• Cargill Incorporated (U.S.)

• Dohler GmbH (Germany)

• Kerry Inc. (Ireland)

• Ingredion Inc. (U.S.)

• JBT Corporation (U.S.)

• Lavva (U.S.)

• Amy's Kitchen (U.S.)

• Barry Callebaut (Switzerland)

• Cargill (U.S.)

• Chr. Hansen (Denmark)

• Crowley Foods (U.S.)

• Daiya Foods (Canada)

• Doves Farm Foods (U.K.)

• Edlong Dairy Technologies (U.S.)

• Newly Weds Foods (U.S.)

• PGP International Inc. (U.S.)

• SensoryEffects (U.S.)

• Tate & Lyle PLC (U.K.)

• Archer Daniels Midland Company (U.S.)

• Marel (Iceland)

• GEA Group (Germany)

• Bühler AG (Switzerland)

Latest Developments in Global Food Coating Market

- In September 2026, DuPont, capacity expansion, announced the expansion of its manufacturing facilities in Asia to strengthen its production capabilities for food coating ingredients, aiming to meet rising regional demand and improve supply chain efficiency. This move is expected to enhance production capacity and reduce lead times for customers across key markets. In addition, the expansion supports DuPont’s long-term growth strategy in emerging economies where processed food consumption is increasing. The improved regional presence is also likely to boost customer relationships and operational flexibility. Overall, this development strengthens DuPont’s competitive positioning in the global food coating market

- In November 2025, Kerry Group, strategic partnership, entered into a collaboration with a food technology firm to develop advanced coating solutions that improve flavor and texture in processed foods. This initiative focuses on enhancing sensory performance and meeting evolving consumer expectations for premium food experiences. The partnership enables Kerry to leverage technological expertise and accelerate innovation in coating formulations. In addition, it supports the company’s strategy to expand its value-added ingredient portfolio. This development is expected to strengthen Kerry’s market presence and drive differentiation in a competitive landscape

- In October 2024, BASF, product launch, introduced a new range of sustainable food coating ingredients derived from renewable resources, focusing on reducing environmental impact while meeting regulatory requirements. This launch aligns with the growing demand for eco-friendly and clean-label food ingredients across global markets. The introduction of sustainable solutions is expected to attract environmentally conscious consumers and food manufacturers. In addition, BASF is likely to enhance its brand image and leadership in sustainable ingredient innovation. This move also supports long-term growth by aligning with global sustainability trends

- In June 2024, Ingredion Incorporated, product innovation, launched clean-label coating solutions designed to improve texture and shelf life in processed foods. These solutions are aimed at helping manufacturers meet consumer demand for natural and minimally processed ingredients. The innovation enhances product functionality while maintaining label transparency, which is increasingly important in purchasing decisions. In addition, Ingredion is strengthening its position in the premium ingredient segment through continuous R&D investments. This development is expected to drive adoption among food manufacturers seeking healthier and high-performance coating solutions

- In August 2023, Cargill Incorporated, investment, announced increased investment in research and development for specialty food coating ingredients to enhance functionality and nutritional value. This initiative focuses on improving product performance while addressing changing consumer preferences for healthier food options. The investment is expected to accelerate innovation and enable the development of customized coating solutions. In addition, it supports Cargill’s strategy to expand its footprint in value-added ingredient markets. This move is likely to enhance competitiveness and drive long-term growth opportunities

- In May 2022, Archer Daniels Midland Company, expansion, expanded its ingredient solutions portfolio with a focus on food coatings to improve product performance and application versatility. This expansion aims to cater to a wide range of food applications, including snacks, bakery, and processed foods. The initiative supports ADM’s strategy to diversify its product offerings and strengthen its global presence. In addition, it enables the company to better serve evolving customer requirements with innovative solutions. This development is expected to enhance market share and reinforce ADM’s position in the food ingredients industry

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Food Coating Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Food Coating Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Food Coating Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.