Global Liver Cirrhosis Drugs Market

Market Size in USD Billion

CAGR :

%

USD

1.49 Billion

USD

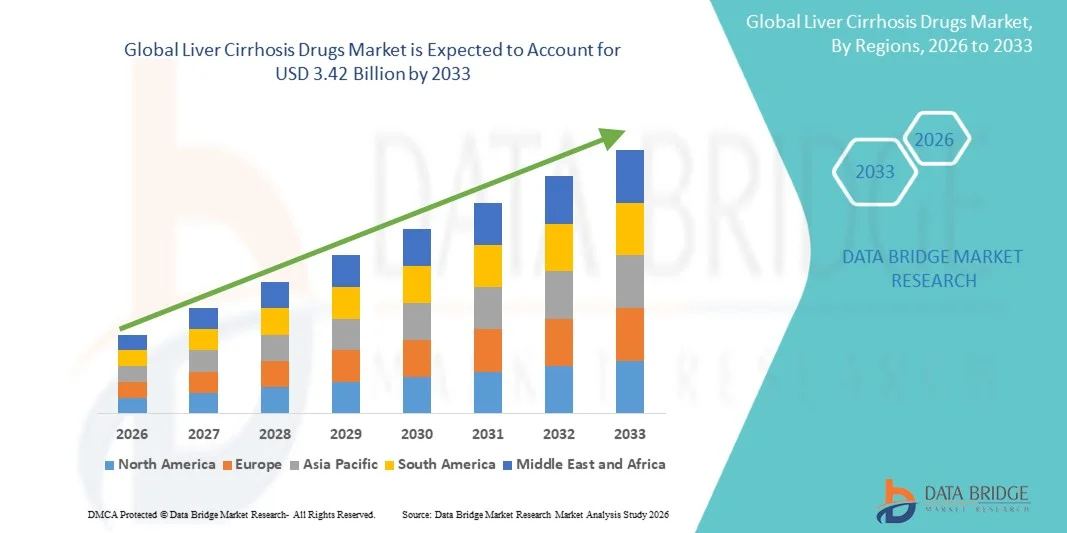

3.42 Billion

2025

2033

USD

1.49 Billion

USD

3.42 Billion

2025

2033

| 2026 –2033 | |

| USD 1.49 Billion | |

| USD 3.42 Billion | |

| % | |

|

Liver Cirrhosis Drugs Market Size

- The global liver cirrhosis drugs market size was valued at USD 1.49 billion in 2025 and is expected to reach USD 3.42 billion by 2033, at a CAGR of 10.95% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic liver diseases, rising cases of alcohol-related liver damage, and growing incidence of hepatitis infections, leading to a higher demand for effective treatment options and improved disease management

- Furthermore, the rising demand for advanced, targeted, and long-term therapeutic solutions is establishing liver cirrhosis drugs as a critical component in hepatology care. These converging factors are accelerating the uptake of liver cirrhosis drugs, thereby significantly boosting the market growth

Liver Cirrhosis Drugs Market Analysis

- Liver cirrhosis drugs, used for managing complications and slowing disease progression in chronic liver conditions, are becoming increasingly important in modern healthcare due to the rising global burden of liver diseases and the need for long-term therapeutic management

- The escalating demand for liver cirrhosis drugs is primarily driven by the increasing prevalence of alcohol-related liver disease, hepatitis infections, and non-alcoholic fatty liver disease (NAFLD), along with growing awareness regarding early diagnosis and treatment

- North America dominated the liver cirrhosis drugs market with a revenue share of approximately 39.6% in 2025, supported by advanced healthcare infrastructure, high treatment adoption rates, and strong presence of key pharmaceutical companies. The U.S. leads the region due to a high patient population and continuous advancements in drug therapies

- Asia-Pacific is expected to be the fastest-growing region in the liver cirrhosis drugs market during the forecast period, driven by increasing healthcare expenditure, rising awareness, and a growing prevalence of liver disorders in countries such as China and India

- The Oral segment held the largest market revenue share of 58.7% in 2025, driven by its convenience, ease of administration, and high patient compliance

Report Scope and Liver Cirrhosis Drugs Market Segmentation

|

Attributes |

Liver Cirrhosis Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• F. Hoffmann-La Roche Ltd (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Liver Cirrhosis Drugs Market Trends

“Advancements in Targeted Therapies and Regenerative Medicine Approaches”

- A significant and accelerating trend in the global liver cirrhosis drugs market is the growing focus on targeted therapies and regenerative medicine aimed at slowing disease progression and improving liver function

- Increasing research into antifibrotic drugs and biologics is enabling the development of therapies that directly address liver fibrosis, a key underlying cause of cirrhosis

- For instance, ongoing clinical studies are exploring novel drug candidates that target inflammatory and fibrotic pathways to prevent further liver damage

- In addition, advancements in regenerative medicine, including stem cell therapy, are gaining attention as potential treatment options for repairing damaged liver tissue

- The adoption of combination therapies, involving antivirals, immunomodulators, and supportive treatments, is also improving patient outcomes

- Furthermore, increasing emphasis on early diagnosis and disease monitoring is supporting timely therapeutic intervention

- This trend is driving innovation and expanding treatment possibilities in the Liver Cirrhosis Drugs market

Liver Cirrhosis Drugs Market Dynamics

Driver

“Rising Prevalence of Liver Diseases and Increasing Alcohol Consumption”

- The increasing prevalence of chronic liver diseases is a major driver for the Liver Cirrhosis Drugs market

- Factors such as excessive alcohol consumption, viral hepatitis infections, and the growing incidence of non-alcoholic fatty liver disease (NAFLD) are significantly contributing to the rising burden of liver cirrhosis globally

- For instance, the increasing number of patients diagnosed with hepatitis B and C is leading to higher demand for effective therapeutic solutions to manage and prevent cirrhosis progression

- In addition, sedentary lifestyles, obesity, and metabolic disorders are further accelerating the incidence of liver-related complications

- Growing awareness regarding liver health and improved access to diagnostic services are encouraging early detection and treatment

- Moreover, advancements in pharmaceutical research and increasing availability of treatment options are supporting better disease management

- These factors collectively are significantly contributing to the growth of the Liver Cirrhosis Drugs market

Restraint/Challenge

“High Treatment Costs and Limited Curative Options”

- One of the major challenges in the Liver Cirrhosis Drugs market is the high cost associated with long-term treatment and disease management

- Advanced therapies, prolonged medication use, and frequent monitoring increase the overall financial burden on patients and healthcare systems

- For instance, treatments involving antiviral therapies and hospitalization for complications such as ascites or hepatic encephalopathy can be expensive, particularly in low- and middle-income regions

- In addition, the lack of a definitive cure for advanced liver cirrhosis limits treatment effectiveness, with liver transplantation often being the only option in severe cases

- Limited availability of donor organs and high transplantation costs further restrict access to curative treatment

- Furthermore, late diagnosis and asymptomatic disease progression in early stages can delay timely intervention and worsen patient outcomes

- Addressing these challenges through affordable treatment options, improved early diagnosis, and continued research into curative therapies will be essential for sustained market growth

Liver Cirrhosis Drugs Market Scope

The market is segmented on the basis of type, stage type, therapy type, mechanism of action type, drug type, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the Liver Cirrhosis Drugs market is segmented into Hepatitis C-related Cirrhosis, Alcoholic Cirrhosis, Primary Sclerosing Cholangitis, Primary Biliary Cirrhosis, and others. The Hepatitis C-related Cirrhosis segment dominated the largest market revenue share of 41.8% in 2025, driven by the high global prevalence of chronic hepatitis C infections leading to liver damage and cirrhosis. Increasing screening programs and early diagnosis initiatives have significantly improved detection rates, supporting treatment demand. The segment benefits from the availability of advanced antiviral therapies that help slow disease progression. In addition, rising awareness about viral hepatitis and government-led elimination programs are contributing to market growth. Patients with hepatitis C-related cirrhosis often require long-term medication and monitoring, increasing healthcare utilization. The expansion of healthcare access in emerging markets further supports segment dominance. Pharmaceutical companies are investing heavily in developing effective therapies targeting viral causes. Favorable reimbursement policies in developed regions also contribute to adoption. Continuous research in antiviral drug development enhances treatment outcomes. Overall, the high disease burden and strong treatment pipeline maintain this segment’s leading position.

The Alcoholic Cirrhosis segment is anticipated to witness the fastest growth rate of 21.4% from 2026 to 2033, fueled by increasing alcohol consumption globally and rising cases of alcohol-related liver diseases. Changing lifestyles and growing stress levels are contributing to higher alcohol intake, thereby increasing disease incidence. The segment is also supported by rising awareness regarding alcohol-induced liver damage and the need for early intervention. Increasing hospital admissions for alcohol-related complications are driving demand for treatment. Governments and healthcare organizations are focusing on awareness campaigns and treatment programs, further supporting growth. In addition, advancements in supportive therapies and rehabilitation programs are improving patient outcomes. The growing burden of liver diseases in developing regions is also contributing to segment expansion. Pharmaceutical companies are exploring new treatment options targeting inflammation and fibrosis. Increasing healthcare expenditure and improved access to treatment further accelerate growth. As lifestyle-related disorders continue to rise, the segment is expected to grow rapidly over the forecast period.

• By Stage Type

On the basis of stage type, the Liver Cirrhosis Drugs market is segmented into Compensated Cirrhosis and Decompensated Cirrhosis. The Compensated Cirrhosis segment held the largest market revenue share of 55.2% in 2025, driven by higher diagnosis rates at earlier stages due to improved screening and monitoring practices. Patients in this stage often show mild or no symptoms, allowing timely intervention and long-term disease management. The segment benefits from the availability of various pharmacological and lifestyle-based treatment approaches aimed at delaying disease progression. Increasing awareness and routine health check-ups are contributing to early diagnosis. In addition, advancements in diagnostic technologies are enabling better detection of liver conditions. Patients in the compensated stage require prolonged treatment, contributing to sustained revenue generation. Healthcare providers emphasize preventive care and disease monitoring in this stage. Rising prevalence of chronic liver diseases further supports segment growth. Favorable reimbursement scenarios also enhance treatment accessibility. Overall, early-stage management drives strong dominance of this segment.

The Decompensated Cirrhosis segment is expected to witness the fastest CAGR of 20.6% from 2026 to 2033, driven by the increasing number of advanced liver disease cases requiring intensive treatment. This stage is characterized by severe complications such as ascites, hepatic encephalopathy, and variceal bleeding, leading to higher healthcare demand. Growing hospital admissions for advanced liver conditions are supporting segment growth. The need for specialized treatments, including hospitalization and surgical interventions, further drives demand. Increasing availability of advanced therapies and liver transplantation options also contributes to expansion. Healthcare systems are investing in critical care infrastructure to manage such cases. Rising awareness about complications and improved diagnosis rates are also supporting growth. In addition, research efforts are focused on developing therapies for late-stage disease management. The high unmet medical need in this segment further accelerates innovation. As disease progression rates increase globally, this segment is expected to grow significantly.

• By Therapy Type

On the basis of therapy type, the Liver Cirrhosis Drugs market is segmented into Medication, Healthy Diet, Surgery, Weight Loss, Liver Transplantation, and others. The Medication segment dominated the largest market revenue share of 49.6% in 2025, driven by its role as the primary treatment approach for managing symptoms and slowing disease progression. Medications such as diuretics, beta-blockers, and antivirals are widely prescribed across all stages of cirrhosis. The segment benefits from continuous advancements in drug development and increasing availability of effective therapies. Patients often require long-term pharmacological management, supporting sustained demand. In addition, medications are more accessible and cost-effective compared to surgical options. Growing awareness about early treatment and disease management further drives adoption. The expansion of generic drug markets also enhances affordability. Healthcare providers rely heavily on medications for initial and ongoing treatment. Rising prevalence of liver diseases globally continues to support growth. Overall, widespread use and accessibility maintain segment dominance.

The Liver Transplantation segment is anticipated to witness the fastest growth rate of 22.0% from 2026 to 2033, driven by increasing cases of end-stage liver disease and advancements in transplant procedures. Liver transplantation is considered the most effective treatment for severe cirrhosis, offering improved survival rates. The growing availability of specialized transplant centers is supporting segment expansion. In addition, advancements in surgical techniques and post-operative care are improving patient outcomes. Increasing awareness about organ donation is also contributing to growth. Governments and healthcare organizations are investing in transplant infrastructure and programs. The rising burden of chronic liver diseases further increases demand for transplantation. Technological innovations and better immunosuppressive therapies enhance success rates. In addition, international collaborations and medical tourism are supporting access to transplantation services. As demand for advanced treatment rises, this segment is expected to grow rapidly.

• By Distribution Channel

On the basis of distribution channel, the Liver Cirrhosis Drugs market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment accounted for the largest market revenue share of 46.8% in 2025, driven by the high number of hospital-based treatments and prescriptions for liver cirrhosis patients. Hospitals serve as primary care centers for diagnosis, treatment, and management of severe liver conditions. The segment benefits from the availability of specialized medications and professional supervision. Increasing hospital admissions for liver diseases further support growth. In addition, hospital pharmacies ensure the availability of critical and emergency drugs. Strong distribution networks and partnerships with pharmaceutical companies enhance supply efficiency. The segment also benefits from reimbursement support in many regions. Growing healthcare infrastructure further strengthens its position. Continuous advancements in hospital care contribute to improved patient outcomes. Overall, hospital pharmacies remain the leading distribution channel.

The Online Pharmacy segment is expected to witness the fastest CAGR of 21.7% from 2026 to 2033, driven by the rapid growth of digital healthcare platforms and increasing consumer preference for convenient purchasing options. Online pharmacies offer home delivery, competitive pricing, and easy access to medications, attracting a large patient base. Increasing internet penetration and smartphone usage are supporting segment growth. Patients with chronic conditions prefer online platforms for repeat purchases. The expansion of e-commerce in healthcare is also contributing to adoption. Technological advancements and secure payment systems enhance user experience. Growing partnerships between pharmaceutical companies and online platforms further support expansion. Regulatory developments are also encouraging the growth of digital pharmacies. Rising awareness about online healthcare services is boosting demand. As digital transformation continues, this segment is expected to grow rapidly

• By Mechanism of Action Type

On the basis of mechanism of action type, the Liver Cirrhosis Drugs market is segmented into Diuretic, Ammonia Reducer, Beta Blocker, Antibiotics, and Antiviral Drug. The Diuretic segment dominated the largest market revenue share of 36.9% in 2025, driven by its widespread use in managing ascites and fluid retention, which are common complications of liver cirrhosis. Diuretics such as spironolactone and furosemide are routinely prescribed as first-line treatments, making them highly utilized across healthcare settings. The segment benefits from strong clinical guidelines supporting their use in symptom management. In addition, increasing cases of decompensated cirrhosis are driving demand for effective fluid control therapies. Diuretics are cost-effective and easily accessible, further supporting their dominance. Physicians rely heavily on these drugs for improving patient comfort and reducing hospitalization rates. The growing prevalence of liver diseases globally continues to support demand. Furthermore, ongoing monitoring and long-term use contribute to sustained revenue generation. The availability of generic formulations enhances affordability and accessibility. Overall, their essential role in symptom management maintains strong market leadership.

The Antiviral Drug segment is expected to witness the fastest CAGR of 22.5% from 2026 to 2033, driven by increasing focus on treating underlying viral causes such as hepatitis B and C. Antiviral therapies help slow disease progression and prevent further liver damage, making them highly valuable in cirrhosis management. The growing global burden of viral hepatitis is a major factor supporting segment growth. In addition, advancements in antiviral drug development are improving treatment outcomes and patient compliance. Governments and healthcare organizations are implementing hepatitis elimination programs, boosting demand. Increasing awareness and early diagnosis further contribute to higher adoption. Pharmaceutical companies are investing heavily in innovative antiviral therapies. Favorable reimbursement policies in developed regions also support growth. Rising healthcare expenditure in emerging markets is improving access to treatment. As focus shifts toward disease-modifying therapies, this segment is expected to expand rapidly.

• By Drug Type

On the basis of drug type, the Liver Cirrhosis Drugs market is segmented into Ursodeoxycholic Acid, Obeticholic Acid, Azathioprine, Colchicine, and others. The Ursodeoxycholic Acid segment dominated the largest market revenue share of 39.4% in 2025, driven by its extensive use in treating cholestatic liver diseases and improving bile flow. This drug is widely prescribed due to its proven efficacy in slowing disease progression and improving liver function. The segment benefits from strong clinical acceptance and long-term usage in patients. In addition, its favorable safety profile supports widespread adoption. Increasing diagnosis of liver disorders is contributing to higher demand. The availability of generic versions enhances affordability and accessibility. Physicians prefer this drug due to its established therapeutic benefits. Growing awareness about liver health also supports segment growth. Continuous research and development activities further strengthen its market presence. Overall, its effectiveness and accessibility maintain its leading position.

The Obeticholic Acid segment is anticipated to witness the fastest growth rate of 21.8% from 2026 to 2033, fueled by its innovative mechanism of action targeting bile acid pathways. This drug is gaining traction in treating advanced liver diseases and conditions such as primary biliary cholangitis. Increasing clinical evidence supporting its efficacy is driving adoption. In addition, growing focus on targeted therapies is boosting demand. Pharmaceutical companies are investing in expanding its indications. Rising awareness among healthcare providers further supports growth. The drug offers improved outcomes for patients with limited treatment options. Increasing research in liver disease therapeutics is also contributing to segment expansion. Favorable regulatory approvals in key markets enhance adoption. As demand for advanced therapies rises, this segment is expected to grow significantly.

• By Route of Administration

On the basis of route of administration, the Liver Cirrhosis Drugs market is segmented into Oral, Intravenous, and others. The Oral segment held the largest market revenue share of 58.7% in 2025, driven by its convenience, ease of administration, and high patient compliance. Most liver cirrhosis medications are available in oral formulations, making them suitable for long-term treatment. Patients prefer oral drugs as they can be taken at home without medical supervision. The segment benefits from widespread availability and cost-effectiveness. In addition, oral medications reduce the need for hospital visits, enhancing patient convenience. Increasing prevalence of chronic liver diseases further supports demand. Pharmaceutical companies are focusing on developing advanced oral formulations. The availability of generic drugs also enhances affordability. Strong distribution networks ensure easy access across regions. Overall, convenience and accessibility maintain the dominance of this segment.

The Intravenous segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, driven by the increasing need for immediate and effective treatment in severe cases. Intravenous administration is commonly used in hospital settings for patients with advanced cirrhosis and complications. The segment benefits from rapid drug delivery and higher bioavailability. Growing hospital admissions for liver-related conditions support demand. In addition, advancements in infusion therapies are improving treatment outcomes. Healthcare providers prefer IV administration for critically ill patients. Increasing healthcare infrastructure and critical care facilities further drive growth. Rising awareness about advanced treatment options also contributes to adoption. As severe cases of cirrhosis increase, this segment is expected to grow steadily.

• By End-Users

On the basis of end-users, the Liver Cirrhosis Drugs market is segmented into Hospitals, Homecare, Specialty Clinics, and others. The Hospitals segment dominated the largest market revenue share of 52.1% in 2025, driven by the availability of advanced diagnostic and treatment facilities. Hospitals serve as primary care centers for managing moderate to severe liver cirrhosis cases. The presence of skilled healthcare professionals and multidisciplinary teams supports effective treatment. Increasing hospital admissions for liver-related complications further drive demand. In addition, hospitals provide access to surgical procedures and transplantation services. Strong reimbursement frameworks in developed regions support growth. The segment benefits from continuous advancements in hospital infrastructure. Rising prevalence of liver diseases globally contributes to higher patient inflow. Hospitals also play a key role in emergency care and long-term management. Overall, comprehensive care capabilities maintain segment dominance.

The Homecare segment is anticipated to witness the fastest growth rate of 21.3% from 2026 to 2033, fueled by increasing preference for home-based treatment and chronic disease management. Patients with stable conditions prefer homecare due to convenience and cost-effectiveness. The availability of oral medications and telehealth services supports this trend. Increasing awareness about self-care and lifestyle management also contributes to growth. Digital health technologies enable remote monitoring and consultation. In addition, homecare reduces the burden on hospitals and healthcare systems. Pharmaceutical companies are focusing on patient-friendly treatment options. Rising demand for personalized healthcare further supports segment expansion. As healthcare shifts toward patient-centric models, this segment is expected to grow rapidly.

Liver Cirrhosis Drugs Market Regional Analysis

- North America dominated the liver cirrhosis drugs market with the largest revenue share of approximately 39.6% in 2025, supported by advanced healthcare infrastructure, high treatment adoption rates, and a strong presence of key pharmaceutical companies

- The region benefits from widespread availability of advanced therapeutic options, early diagnosis, and well-established healthcare systems for managing chronic liver diseases

- This dominance is further reinforced by increasing prevalence of liver disorders, favorable reimbursement frameworks, and continuous advancements in drug development, establishing North America as a key contributor to the Liver Cirrhosis Drugs market

U.S. Liver Cirrhosis Drugs Market Insight

The U.S. liver cirrhosis drugs market captured the largest revenue share in 2025 within North America, driven by a high patient population and continuous advancements in drug therapies. The country benefits from strong research and development activities, early adoption of innovative treatments, and high healthcare expenditure. In addition, the presence of leading pharmaceutical companies and increasing awareness regarding liver diseases are significantly contributing to market growth in the United States.

Europe Liver Cirrhosis Drugs Market Insight

The Europe liver cirrhosis drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of liver diseases and strong healthcare infrastructure. The region is witnessing rising awareness regarding early diagnosis and effective disease management. Furthermore, growing adoption of advanced therapeutic approaches and supportive government healthcare policies are contributing to improved patient outcomes across Europe.

U.K. Liver Cirrhosis Drugs Market Insight

The U.K. liver cirrhosis drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing incidence of liver disorders and growing focus on early diagnosis and treatment. Government healthcare initiatives and access to public healthcare services are supporting disease management. In addition, rising awareness regarding alcohol-related liver diseases and lifestyle modifications is expected to contribute to market growth in the U.K.

Germany Liver Cirrhosis Drugs Market Insight

The Germany liver cirrhosis drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure and strong emphasis on research and innovation. The country supports the adoption of advanced treatment options and efficient disease management strategies. Increasing awareness regarding liver health and availability of specialized care are key factors driving market growth in Germany.

Asia-Pacific Liver Cirrhosis Drugs Market Insight

The Asia-Pacific liver cirrhosis drugs market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing healthcare expenditure, rising awareness, and a growing prevalence of liver disorders in countries such as China and India. The region is witnessing significant improvements in healthcare infrastructure and access to treatment, enabling better diagnosis and management of liver cirrhosis. In addition, rising incidence of hepatitis infections, alcohol consumption, and lifestyle-related disorders are contributing to the increasing disease burden. Government initiatives aimed at improving healthcare systems and expanding access to treatment are further accelerating market growth across the region

Japan Liver Cirrhosis Drugs Market Insight

The Japan liver cirrhosis drugs market is gaining momentum due to the country’s aging population and increasing prevalence of chronic liver diseases. The presence of advanced healthcare technologies and strong emphasis on early diagnosis and preventive care are supporting market growth. In addition, increasing adoption of innovative drug therapies and efficient disease management practices is contributing to improved patient outcomes in Japan.

China Liver Cirrhosis Drugs Market Insight

The China liver cirrhosis drugs market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to a large patient population, increasing prevalence of liver diseases, and improving healthcare infrastructure. Rising healthcare expenditure, growing awareness regarding liver health, and expanding access to advanced treatment options are key factors driving market growth. Furthermore, government initiatives focused on controlling chronic diseases and improving healthcare delivery are expected to further propel the market in China.

Liver Cirrhosis Drugs Market Share

The Liver Cirrhosis Drugs industry is primarily led by well-established companies, including:

• F. Hoffmann-La Roche Ltd (Switzerland)

• Gilead Sciences, Inc. (U.S.)

• AbbVie Inc. (U.S.)

• Bristol-Myers Squibb Company (U.S.)

• Novartis AG (Switzerland)

• Pfizer Inc. (U.S.)

• Johnson & Johnson (U.S.)

• Sanofi S.A. (France)

• Merck & Co., Inc. (U.S.)

• Bayer AG (Germany)

• AstraZeneca plc (U.K.)

• Eli Lilly and Company (U.S.)

• Intercept Pharmaceuticals, Inc. (U.S.)

• Madrigal Pharmaceuticals, Inc. (U.S.)

• Galectin Therapeutics Inc. (U.S.)

• Durect Corporation (U.S.)

• Viking Therapeutics, Inc. (U.S.)

• Conatus Pharmaceuticals Inc. (U.S.)

• Zydus Lifesciences Limited (India)

• Sun Pharmaceutical Industries Ltd. (India)

Latest Developments in Global Liver Cirrhosis Drugs Market

- In July 2021, Albireo Pharma announced that the U.S. Food and Drug Administration approved Bylvay (odevixibat), a first-in-class ileal bile acid transporter inhibitor, for the treatment of rare pediatric cholestatic liver diseases, representing a significant advancement in managing liver conditions that can progressively lead to fibrosis and cirrhosis if left untreated

- In March 2024, Madrigal Pharmaceuticals announced that the U.S. Food and Drug Administration approved Rezdiffra (resmetirom), marking the first-ever approved therapy for metabolic dysfunction-associated steatohepatitis (MASH), a major underlying cause of liver fibrosis and cirrhosis, thereby transforming the treatment landscape for chronic liver disease

- In April 2024, Madrigal Pharmaceuticals officially launched Rezdiffra (resmetirom) in the United States, enabling physicians to directly target liver fat accumulation and inflammation, which are key drivers in the progression from early liver disease to advanced fibrosis and cirrhosis

- In June 2025, European Medicines Agency issued a positive opinion recommending conditional approval of resmetirom for patients with MASH and significant fibrosis, highlighting growing regulatory support in Europe for innovative therapies aimed at preventing cirrhosis progression

- In August 2025, European Commission granted marketing authorization for Rezdiffra (resmetirom) across the European Union, significantly expanding patient access to a disease-modifying therapy that addresses key metabolic drivers of liver cirrhosis

- In May 2025, Galectin Therapeutics announced positive clinical trial outcomes for belapectin, a galectin-3 inhibitor, demonstrating its potential to reduce portal hypertension and associated complications in cirrhosis patients, thereby addressing critical unmet needs in advanced-stage disease management

- In September 2025, Roche announced its agreement to acquire 89bio, a clinical-stage biotechnology company specializing in liver disease therapies, for up to USD 3.5 billion, aiming to strengthen its pipeline of treatments targeting metabolic liver diseases that can progress to cirrhosis

- In October 2025, GlaxoSmithKline announced the acquisition of efimosfermin from Boston Pharmaceuticals, a late-stage investigational therapy targeting liver fibrosis, reinforcing its strategic focus on expanding its portfolio in chronic liver diseases including cirrhosis

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.