North America Q Pcr Reagents Market

Market Size in USD Million

CAGR :

%

USD

510.35 Million

USD

890.07 Million

2025

2033

USD

510.35 Million

USD

890.07 Million

2025

2033

| 2026 –2033 | |

| USD 510.35 Million | |

| USD 890.07 Million | |

| % | |

|

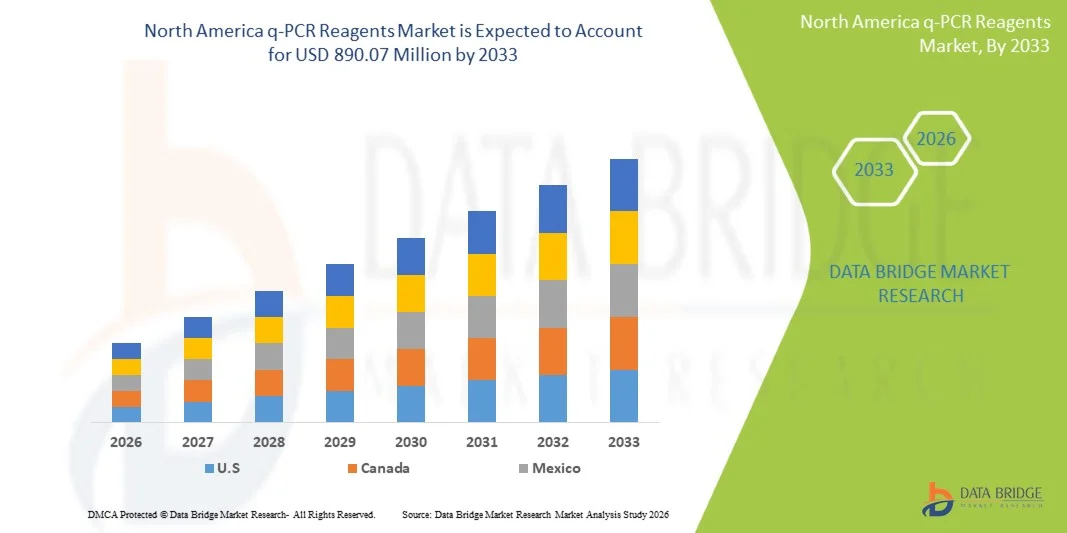

North America q-PCR Reagents Market Size

- The North America q-PCR reagents market size was valued at USD 510.35 million in 2025and is expected to reach USD 890.07 million by 2033, at a CAGR of 7.2% during the forecast period

- The market growth is largely fueled by the expanding adoption of quantitative polymerase chain reaction (q-PCR) technologies in clinical diagnostics, research laboratories, and biotechnology applications, supported by continuous advancements in molecular biology tools and precision medicine approaches

- Furthermore, increasing demand for rapid, accurate, and high-sensitivity molecular diagnostic solutions for infectious diseases, oncology, and genetic testing is establishing q-PCR reagents as a critical component of modern laboratory workflows. These converging factors are accelerating the uptake of q-PCR reagent solutions, thereby significantly boosting the industry's growth

North America q-PCR Reagents Market Analysis

- q-PCR reagents, including enzymes, master mixes, primers, and fluorescent probes, are essential consumables used in quantitative polymerase chain reaction workflows, enabling highly sensitive, accurate, and real-time detection of nucleic acids across clinical diagnostics, research, and biotechnology applications

- The escalating demand for q-PCR reagents is primarily fueled by the rising prevalence of infectious diseases, growing adoption of molecular diagnostics, expanding applications in oncology and genetic testing, and continuous advancements in precision medicine and life science research

- The United States dominated the q-PCR reagents market with the largest revenue share of 78.6% in 2025, characterized by a strong biotechnology ecosystem, advanced diagnostic infrastructure, high R&D spending, and the presence of major life sciences companies, with widespread adoption across clinical laboratories, academic institutes, and pharmaceutical research organizations

- Canada is expected to be the fastest growing country in the q-PCR reagents market during the forecast period driven by increasing government investments in healthcare research, expanding molecular diagnostic capacity, and rising demand for early and accurate disease detection technologies

- The master mixes segment dominated the q-PCR reagents market with a market share of 56.8% in 2025, driven by their high efficiency, improved accuracy, reduced contamination risk, and widespread use in standardized diagnostic and research workflows

Report Scope and North America q-PCR Reagents Market Segmentation

|

Attributes |

North America q-PCR Reagents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico |

|

Key Market Players |

|

|

Market Opportunities |

· Increasing adoption of multiplex q-PCR assays is creating strong opportunities for reagent manufacturers · Expanding use of q-PCR reagents in companion diagnostics for personalized medicine |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

North America q-PCR Reagents Market Trends

“Rising Adoption of Automation and Digital PCR Integration”

- A significant and accelerating trend in the North America q-PCR reagents market is the increasing integration of automated liquid handling systems and digital PCR platforms, improving workflow efficiency and result accuracy in molecular diagnostics and research laboratories

- For instance, Thermo Fisher Scientific qPCR reagent systems are widely used with QuantStudio platforms enabling high-throughput automated gene expression and pathogen detection workflows across clinical and research settings

- Automation in q-PCR workflows enables reduced manual errors, higher reproducibility, and faster turnaround times, while digital PCR compatibility is improving absolute quantification of nucleic acids in oncology and infectious disease testing applications

- Furthermore, integration of q-PCR reagents with laboratory information management systems (LIMS) and cloud-based data analytics is enabling centralized data tracking, improved reproducibility, and enhanced laboratory productivity across diagnostic networks

- This trend towards highly automated, data-driven, and digitally integrated q-PCR workflows is reshaping laboratory expectations for speed and accuracy in molecular testing processes

- The demand for advanced q-PCR reagent kits compatible with automated and digital platforms is growing rapidly across clinical diagnostics and research institutions as laboratories increasingly prioritize scalability and precision

- Furthermore, rising collaborations between reagent manufacturers and diagnostic instrument companies are accelerating the development of fully integrated q-PCR workflow solutions for clinical laboratories

North America q-PCR Reagents Market Dynamics

Driver

“Rising Demand Driven by Expanding Molecular Diagnostics and Infectious Disease Testing”

- The increasing prevalence of infectious diseases and growing reliance on molecular diagnostic techniques is a major driver for the rising demand for q-PCR reagents across clinical laboratories and research institutes

- For instance, in April 2025, Bio-Rad Laboratories expanded its q-PCR reagent portfolio to support high-sensitivity pathogen detection workflows, strengthening its position in clinical diagnostic applications

- As healthcare systems increasingly shift toward early and accurate disease detection, q-PCR reagents provide high specificity and sensitivity for applications in oncology, genetic disorders, and infectious disease screening

- Furthermore, the growing adoption of personalized medicine and biomarker-based testing is making q-PCR reagents a critical component in advanced diagnostic workflows across hospitals and biotech companies

- The increasing use of q-PCR in pharmaceutical research, vaccine development, and clinical trials is further propelling demand in both public and private healthcare sectors

- The trend toward rapid, scalable, and cost-effective molecular testing solutions continues to strengthen the adoption of q-PCR reagents across North America

- Additionally, increasing government funding for genomic research and public health surveillance programs is significantly boosting demand for high-quality q-PCR reagents

- Furthermore, the expansion of hospital-based molecular diagnostic laboratories is accelerating routine use of q-PCR technologies for disease monitoring and screening programs

Restraint/Challenge

“High Cost of Advanced Reagents and Risk of Technical Variability”

- Concerns surrounding the high cost of premium q-PCR reagents and variability in assay performance across different platforms pose a significant challenge to broader market penetration in cost-sensitive laboratory settings

- For instance, variability in amplification efficiency between reagent brands has been reported in comparative studies, leading to inconsistent results in some diagnostic and research applications

- Addressing cost barriers through optimized reagent formulations and bulk supply agreements is essential for improving accessibility among small and mid-sized laboratories

- Additionally, strict regulatory compliance requirements for clinical-grade q-PCR reagents increase development complexity and slow product approval timelines in North America

- While leading companies such as Roche and Thermo Fisher Scientific offer highly validated reagent systems, their premium pricing can limit adoption among budget-constrained institutions

- Overcoming these challenges through cost optimization, improved standardization, and enhanced quality control measures will be vital for sustained market growth

- Additionally, supply chain dependencies for critical raw materials such as enzymes and fluorescent dyes can create periodic shortages impacting reagent availability

- Furthermore, the need for highly skilled technical expertise to operate and interpret q-PCR workflows remains a barrier in smaller laboratories and emerging diagnostic facilities

North America q-PCR Reagents Market Scope

The market is segmented on the basis of detection type, assay type, plexity, packaging type, technology, application, end user, and distribution channel.

- By Detection Type

On the basis of detection type, the q-PCR reagents market is segmented into dye-based reagents and probe-based reagents. The probe-based reagents segment dominated the market with the largest market revenue share of 58.4% in 2025, driven by their high specificity, superior sensitivity, and strong ability to detect multiple genetic targets with minimal background interference. These reagents are widely preferred in clinical diagnostics, especially in infectious disease and oncology testing where accuracy is critical for decision-making. Their compatibility with regulatory-approved assays further strengthens adoption in hospital laboratories. Growing use in multiplex diagnostic panels is also reinforcing demand across advanced testing workflows. Additionally, strong integration with automated q-PCR platforms is supporting large-scale clinical deployment.

The dye-based reagents segment is anticipated to witness the fastest growth rate of 17.9% from 2026 to 2033, fueled by their cost-effectiveness, simplicity, and broad applicability in research laboratories. SYBR Green-based systems are widely used in academic research for gene expression studies due to their flexible assay design and lower development complexity. Increasing adoption in emerging biotech startups and teaching laboratories is further boosting demand. Continuous improvements in dye chemistry are enhancing amplification specificity and reducing non-specific binding issues. Their affordability makes them highly attractive for routine experimental workflows. Expanding applications in exploratory genetic research are also supporting segment growth.

- By Assay Type

On the basis of assay type, the market is segmented into q-PCR singleplex test/assay and q-PCR multiplex test/assay. The singleplex segment dominated the market with a revenue share of 52.7% in 2025, driven by its high reliability, straightforward optimization, and strong usage in routine diagnostic testing. It is widely used for detecting single pathogens or gene targets in clinical laboratories where precision is prioritized. Singleplex assays are easier to validate and standardize, making them highly suitable for regulatory-approved diagnostic workflows. Their compatibility with most q-PCR instruments further enhances adoption. Hospitals and diagnostic centers continue to rely on single-target testing for infectious disease confirmation. Established protocols and consistent performance contribute significantly to market dominance.

The multiplex segment is expected to witness the fastest growth rate of 19.3% from 2026 to 2033, driven by its ability to detect multiple targets in a single reaction, improving efficiency and reducing testing time. It is increasingly used in respiratory panels, cancer diagnostics, and genetic screening applications. Multiplexing significantly reduces reagent consumption and overall testing cost per sample. Rising demand for high-throughput diagnostics in hospitals and reference laboratories is further accelerating adoption. Advances in fluorescent probe technology are enabling higher levels of multiplexing with improved accuracy. Growing demand for comprehensive disease profiling is strongly supporting segment expansion.

- By Plexity

On the basis of plexity, the market is segmented into singleplex and multiplex systems. The singleplex segment dominated the market with a revenue share of 54.1% in 2025, driven by its wide acceptance in clinical diagnostics and standardized testing environments. It offers high accuracy with minimal risk of cross-reactivity, making it ideal for single-target detection applications. Laboratories prefer singleplex systems for their ease of use and reproducibility across routine workflows. Regulatory approvals for diagnostic assays further strengthen its dominance. It is extensively used in infectious disease confirmation and genetic mutation testing. Established clinical protocols continue to support steady demand.

The multiplex segment is expected to witness the fastest growth rate of 20.5% from 2026 to 2033, driven by rising demand for simultaneous detection of multiple biomarkers. It is widely used in oncology and infectious disease panels where multiple pathogen identification is required. Multiplex systems improve laboratory efficiency by reducing turnaround time and sample volume requirements. Increasing adoption in hospital networks and reference laboratories is boosting growth. Technological improvements in probe chemistry are enabling more complex multiplex designs. Expanding applications in precision medicine are further strengthening market expansion.

- By Packaging Type

On the basis of packaging type, the market is segmented into kits and master mixes. The master mixes segment dominated the market with a revenue share of 56.8% in 2025, driven by ease of use, reduced pipetting steps, and improved consistency in q-PCR reactions. Master mixes are widely preferred in clinical and high-throughput laboratories due to their standardized formulation. They minimize contamination risks and enhance reproducibility across experiments. Compatibility with automated systems further increases adoption in advanced diagnostic labs. Hospitals and diagnostic centers favor master mixes for routine testing workflows. Their efficiency and reliability make them the dominant packaging format.

The kits segment is expected to witness the fastest growth rate of 18.6% from 2026 to 2033, driven by increasing demand for customized and application-specific assays. Kits provide flexibility in experimental design, making them suitable for academic and research applications. Growing use in biotechnology startups and molecular biology studies is supporting demand. They are widely adopted in gene expression and mutation analysis workflows. Continuous innovation in kit formulations is improving sensitivity and performance. Expanding research activities in genomics are further accelerating segment growth.

- By Technology

On the basis of technology, the market is segmented into gene expression, gene typing, miRNA analysis, pre-amplification, and virus detection. The virus detection segment dominated the market with a revenue share of 46.9% in 2025, driven by strong demand for infectious disease testing and outbreak preparedness. q-PCR reagents are extensively used for rapid and accurate detection of viral pathogens in clinical laboratories. High sensitivity and fast turnaround time make them essential for hospital diagnostics. Government-led disease surveillance programs further strengthen adoption. Hospital labs heavily rely on virus detection workflows for routine screening. Continuous demand for respiratory virus testing supports market dominance.

The miRNA analysis segment is expected to witness the fastest growth rate of 21.2% from 2026 to 2033, driven by rising research in cancer diagnostics and gene regulation studies. miRNA biomarkers are increasingly used in precision medicine and therapeutic research. Expanding applications in oncology and translational research are fueling adoption. Growing focus on early disease detection is further supporting demand. Technological advancements are improving detection accuracy for low-abundance miRNA targets. Increasing academic and pharmaceutical research investments are accelerating segment expansion.

- By Application

On the basis of application, the market is segmented into diagnostics, research, and forensic. The diagnostics segment dominated the market with a revenue share of 63.5% in 2025, driven by widespread use in infectious disease detection, genetic disorder screening, and oncology diagnostics. q-PCR reagents are critical in hospital laboratories for accurate and early disease identification. Increasing patient testing volumes further support dominance. Strong clinical validation and regulatory approvals enhance adoption in diagnostic workflows. Rising prevalence of chronic and infectious diseases also contributes significantly. Hospitals remain the largest end-use environment for q-PCR applications.

The research segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, driven by increasing investment in genomics and molecular biology research. Academic and biotech institutions are expanding use of q-PCR for gene expression and functional studies. Pharmaceutical companies rely on these reagents for drug development and biomarker discovery. Growing focus on personalized medicine is further driving adoption. Rising government funding for life sciences research is supporting expansion. Collaboration between industry and academia is accelerating innovation.

- By End User

On the basis of end user, the market is segmented into hospital & diagnostic centers, forensic laboratories, research & academic institutes, clinical research organizations, and others. The hospital & diagnostic centers segment dominated the market with a revenue share of 57.3% in 2025, driven by high diagnostic testing volumes and widespread adoption of molecular diagnostics. These facilities rely heavily on q-PCR reagents for infectious disease and genetic testing. Strong infrastructure and skilled workforce further support dominance. Increasing hospital-based molecular laboratories is boosting demand. Integration with automated systems enhances efficiency in clinical workflows. Continuous patient inflow ensures sustained reagent consumption.

The research & academic institutes segment is expected to witness the fastest growth rate of 19.7% from 2026 to 2033, driven by expanding genomics research and molecular biology studies. Universities and research centers are increasingly using q-PCR for advanced genetic analysis. Rising funding for life sciences research is supporting adoption. Collaboration with biotech companies is enhancing innovation. Growing focus on biomarker discovery is further accelerating demand. Expanding educational and experimental applications are strengthening segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and others. The direct tender segment dominated the market with a revenue share of 62.4% in 2025, driven by bulk procurement from hospitals, government laboratories, and large research institutions. Direct procurement ensures cost efficiency and reliable long-term supply agreements. It also guarantees product authenticity and standardized quality. Large-scale buyers prefer direct sourcing for better pricing advantages. Strong manufacturer-institution relationships support dominance. This channel is widely used in high-volume diagnostic environments.

The third-party distributors segment is expected to witness the fastest growth rate of 17.6% from 2026 to 2033, driven by expanding reach to smaller laboratories and regional diagnostic centers. Distributors improve accessibility of specialized q-PCR reagents across fragmented markets. They play a key role in supply chain efficiency and inventory management. Increasing number of diagnostic labs is boosting demand through indirect channels. Growing penetration in emerging healthcare facilities is further supporting growth. Their logistical advantages are strengthening market expansion.

North America q-PCR Reagents Market Regional Analysis

- The United States dominated the q-PCR reagents market with the largest revenue share of 78.6% in 2025, characterized by a strong biotechnology ecosystem, advanced diagnostic infrastructure, high R&D spending, and the presence of major life sciences companies, with widespread adoption across clinical laboratories, academic institutes, and pharmaceutical research organizations

- Laboratories and healthcare providers in the region highly value the high sensitivity, accuracy, and reliability offered by q-PCR reagents for applications such as infectious disease detection, oncology testing, and genetic analysis workflows

- This widespread adoption is further supported by a well-established biotechnology ecosystem, high healthcare expenditure, and strong presence of leading life sciences companies and diagnostic laboratories across the United States and Canada

U.S. North America q-PCR Reagents Market Insight

The U.S. q-PCR reagents market captured the largest revenue share of 79% in 2025 within North America, fueled by the rapid expansion of molecular diagnostics, strong biotechnology infrastructure, and increasing adoption of precision medicine across healthcare systems. Laboratories and research institutions in the country are increasingly prioritizing high-sensitivity and accurate nucleic acid detection for infectious disease, oncology, and genetic testing applications. The growing preference for automated high-throughput q-PCR workflows, combined with strong demand for clinical-grade diagnostic solutions, further propels market growth. Moreover, the extensive integration of advanced q-PCR platforms from leading players such as Thermo Fisher Scientific and Bio-Rad is significantly contributing to market expansion.

Canada q-PCR Reagents Market Insight

The Canada q-PCR reagents market accounted for a significant revenue share in North America in 2025, driven by increasing adoption of molecular diagnostics, expanding clinical research infrastructure, and rising focus on early disease detection across healthcare facilities. The country is witnessing growing utilization of q-PCR technologies in infectious disease testing, oncology diagnostics, and genetic screening applications. Strong government support for genomics research and public health initiatives is further accelerating reagent demand. Additionally, collaborations between academic institutions, biotechnology firms, and healthcare organizations are enhancing innovation and expanding the use of advanced q-PCR workflows across research and clinical laboratories.

Mexico q-PCR Reagents Market Insight

The Mexico q-PCR reagents market is experiencing steady growth, supported by improving healthcare infrastructure, rising awareness of molecular diagnostics, and increasing demand for affordable and rapid disease testing solutions. The country is gradually expanding the use of q-PCR technologies in infectious disease detection and clinical research applications. Growing investment in laboratory modernization and diagnostic capabilities is further supporting market adoption. Additionally, increasing collaborations with international biotechnology companies and expanding access to cost-effective reagent solutions are driving wider adoption of q-PCR-based testing across hospitals and diagnostic centers.

North America q-PCR Reagents Market Share

The North America q-PCR Reagents industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc., (U.S.)

- F. Hoffmann-La Roche Ltd, (Switzerland)

- Bio-Rad Laboratories, Inc., (U.S.)

- QIAGEN (Germany)

- Merck KGaA, (Germany)

- Takara Bio Inc., (Japan)

- Promega Corporation, (U.S.)

- Agilent Technologies, Inc., (U.S.)

- Danaher (U.S.)

- Biosearch Technologies, Inc., (U.S.)

- Enzo Life Sciences, Inc., (U.S.)

- LGC Biosearch Technologies, (U.K.)

- Analytik Jena AG, (Germany)

- Bioneer Corporation, (South Korea)

- Norgen Biotek Corp., (Canada)

- Jena Bioscience GmbH, (Germany)

- Biotium, Inc., (U.S.)

- PCR Biosystems Ltd., (U.K.)

- GeneCopoeia, Inc., (U.S.)

What are the Recent Developments in North America q-PCR Reagents Market?

- In July 2025, Bio-Rad Laboratories expanded its digital PCR and q-PCR ecosystem by launching the QX Continuum system and related workflow enhancements, strengthening its high-precision molecular diagnostics and reagent integration capabilities. The expansion improves compatibility between q-PCR reagents and advanced digital PCR platforms. It enhances multiplexing performance for oncology and infectious disease applications

- In January 2024, Thermo Fisher Scientific introduced an advanced high-throughput q-PCR platform designed to improve speed, sensitivity, and multiplexing efficiency for clinical and research applications across North America. The system enhances performance of q-PCR reagent kits in diagnostic workflows. It enables faster turnaround times for infectious disease and genetic testing

- In November 2023, QIAGEN developed lyophilized q-PCR reagents to improve reagent stability, storage flexibility, and usability in decentralized laboratory environments across North America. The innovation reduces dependency on cold-chain logistics for reagent distribution. It enhances testing reliability in remote and resource-limited settings. It supports broader adoption of q-PCR diagnostics in field applications

- In July 2022, Roche Diagnostics expanded its North American molecular diagnostics operations by strengthening its q-PCR reagent production and supply capabilities to support rising clinical testing demand. The expansion improved availability of q-PCR reagents in hospital laboratories. It enhanced supply chain resilience for high-volume diagnostic testing. It supported infectious disease and oncology testing workflows

- In March 2021, multiple North American diagnostic companies expanded q-PCR reagent production and distribution networks in response to increased demand for molecular testing during and after the COVID-19 pandemic. The expansion ensured continuous supply of critical diagnostic reagents. It supported large-scale PCR testing infrastructure across hospitals and labs

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.