Coronary Stents Market

Market Size in USD Billion

CAGR :

%

USD

2.28 Billion

USD

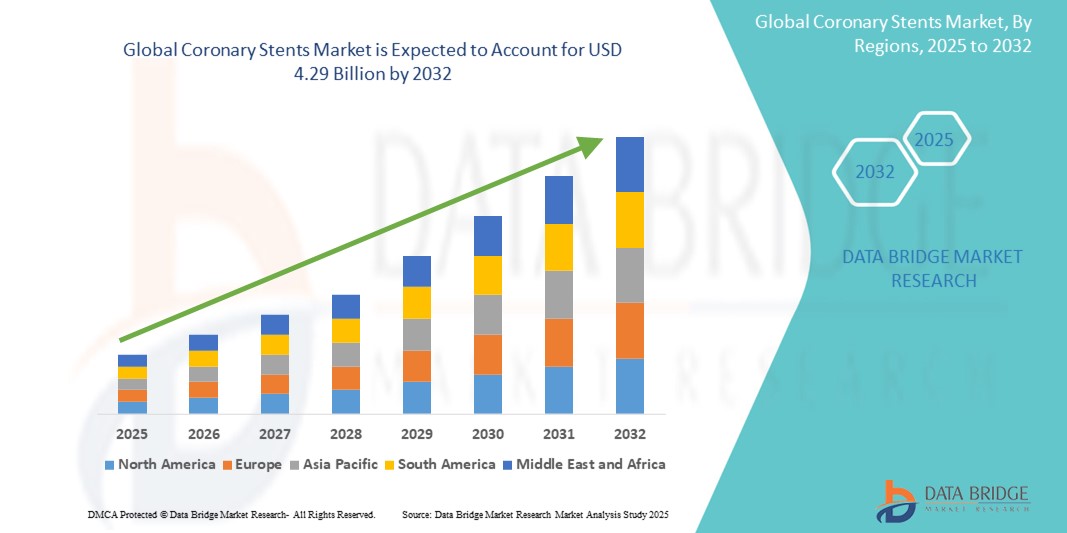

4.29 Billion

2024

2032

USD

2.28 Billion

USD

4.29 Billion

2024

2032

| 2025 –2032 | |

| USD 2.28 Billion | |

| USD 4.29 Billion | |

| % | |

|

Coronary Stents Market Size

- The global Coronary Stents Treatment market was valued at USD 2.28 billion in 2024 and is expected to reach USD 4.29 billion by 2032, at a CAGR of 7.3%, during the forecast period

- The rising prevalence of coronary artery disease and the growing preference for minimally invasive cardiovascular procedures are driving demand for coronary stents globally. Additionally, increasing awareness about the benefits of early intervention with stent implantation, along with advancements in stent technology—such as drug-eluting and bioresorbable stents—is further propelling market growth.

Coronary Stents Market Analysis

- Coronary stents are small, expandable mesh tubes inserted into narrowed or blocked coronary arteries to restore and maintain blood flow to the heart. These stents are vital in the treatment of coronary artery disease (CAD), which results from the buildup of plaque in the arterial walls. By physically supporting the artery and releasing medications in the case of drug-eluting stents, they help prevent restenosis, improve heart function, and reduce the risk of heart attacks, thereby enhancing patient outcomes and quality of life.

- North America emerges as a leading region in the Global Coronary Stents Market, supported by a highly developed healthcare infrastructure, widespread awareness of cardiovascular diseases, and strong reimbursement frameworks for interventional cardiology procedures.

- The region’s ongoing investments in advanced stent technologies, such as bioresorbable scaffolds and next-generation drug-eluting stents, coupled with an aging population and high prevalence of CAD, continue to fuel market growth and innovation in coronary stent therapies.

Report Scope and Coronary Stents Segmentation

|

Attributes |

Coronary Stents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Coronary Stents Market Trends

“Growing Preference for Minimally Invasive and Targeted Therapies”

- A key trend in the global coronary stents market is the increasing preference for minimally invasive, targeted cardiovascular interventions, particularly percutaneous coronary intervention (PCI) using stents.

- Drug-eluting stents (DES) and bioresorbable vascular scaffolds (BVS) are gaining popularity due to their ability to reduce restenosis, enhance arterial healing, and provide targeted drug delivery directly at the lesion site.

- For instance, next-generation stents with biodegradable polymer coatings and tailored drug release profiles are offering greater flexibility and improved long-term outcomes, aligning with the growing demand for personalized treatment strategies

- The trend is further supported by advancements in stent delivery systems, enabling precise placement, reduced procedural time, and improved patient safety.

- Additionally, the integration of intravascular imaging technologies such as OCT (optical coherence tomography) and IVUS (intravascular ultrasound) enhances procedural accuracy, stent positioning, and clinical decision-making.

- This shift toward patient-centric, non-surgical cardiovascular solutions is reshaping interventional cardiology and driving innovation in the global coronary stents market.

Coronary Stents Market Dynamics

Driver

“Increasing Prevalence of Coronary Artery Disease (CAD)”

- As the global population continues to age and lifestyle-related risk factors such as obesity, sedentary behavior, diabetes, and smoking become more prevalent, the incidence of coronary artery disease (CAD)—a condition characterized by narrowing or blockage of the coronary arteries due to plaque buildup—is rising significantly. CAD remains the leading cause of death worldwide, contributing to a growing demand for effective, life-saving interventions like coronary stents.

- Coronary stents, particularly drug-eluting stents (DES), offer a minimally invasive solution to restore blood flow in blocked arteries, relieve chest pain (angina), and reduce the risk of heart attacks. These devices are increasingly favored over traditional open-heart surgeries due to shorter recovery times, lower complication rates, and improved long-term outcomes.

For instance,

- In November 2023, the World Health Organization (WHO) reported that cardiovascular diseases are responsible for approximately 17.9 million deaths annually, with coronary heart disease accounting for a majority

- According to data published by the American Heart Association (2024), around 18.2 million adults in the United States are living with CAD, and this number is projected to rise with increasing age and risk factor prevalence

- The growing global burden of CAD is driving the need for scalable, effective interventional solutions. At the same time, heightened awareness among clinicians and patients about the benefits of early stenting is accelerating adoption rates.

- As clinical outcomes continue to improve due to innovations in stent design, coating technologies, and delivery systems, healthcare professionals are more frequently recommending PCI (Percutaneous Coronary Intervention) with stenting as a frontline treatment. This convergence of clinical need, awareness, and technological progress is creating a robust environment for the continued growth of the global coronary stents market.

Opportunity

“Advancements in Stent Technologies and Delivery Systems”

- Significant innovations in coronary stent design—such as next-generation drug-eluting stents (DES), bioresorbable vascular scaffolds (BVS), and dual therapy stents—are transforming the treatment landscape for coronary artery disease. These advancements provide longer-lasting arterial support, reduced restenosis rates, and enhanced biocompatibility, appealing to both clinicians and patients seeking safer and more effective cardiovascular solutions.

- Cutting-edge delivery systems and catheter technologies are improving stent placement precision, reducing procedure time, and minimizing complications, particularly in complex or multi-vessel interventions. These improvements directly align with the global shift toward minimally invasive cardiac procedures and contribute to better clinical outcomes and faster patient recovery.

For instance,

- Abbott Laboratories, Boston Scientific, and Medtronic have introduced stents with polymer-free coatings, ultra-thin strut designs, and optimized drug elution profiles to improve long-term patency and reduce inflammatory response.

- In early 2024, peer-reviewed studies published in journals such as JACC: Cardiovascular Interventions and EuroIntervention highlighted the superiority of new-generation DES in complex lesions and high-risk patient groups, including those with diabetes and chronic total occlusions

- These technological advances meet the increasing demand for durable, patient-centric cardiovascular care in both mature and emerging markets.

- Companies that invest in innovative stent platforms, customized treatment solutions, and precision-guided PCI tools are better positioned to capitalize on the expanding global burden of coronary artery disease. This makes the coronary stents sector an attractive and strategic area for long-term investment and competitive growth within the interventional cardiology space.

Restraint/Challenge

“High Cost and Accessibility Barriers in Coronary Stent Procedures”

- The high cost of coronary stent implantation, especially when coupled with advanced stent technologies and hospital-based interventional procedures, presents a major challenge to widespread accessibility—particularly in low- and middle-income countries (LMICs) and underserved populations. Even in high-income nations, patients may face substantial out-of-pocket expenses due to insurance limitations or tiered reimbursement structures, which can discourage timely intervention and compromise long-term cardiovascular health outcomes.

- While drug-eluting stents (DES) have improved clinical efficacy, they are often significantly more expensive than bare-metal stents (BMS), leading some healthcare systems and patients to opt for less effective but more affordable alternatives.

- Additionally, the cost of post-procedural care, including dual antiplatelet therapy (DAPT), regular monitoring, and follow-up angiography, further increases the financial burden on patients and healthcare systems. This cumulative cost structure may limit the reach of life-saving stenting procedures in areas with constrained healthcare budgets.

For instance,

- A 2023 report by the American College of Cardiology (ACC) noted that percutaneous coronary intervention (PCI) with drug-eluting stents can range between USD 10,000 to USD 35,000, depending on geographic region, hospital, and stent type.

- In January 2024, a Lancet Global Health study emphasized that in LMICs, many hospitals struggle to afford newer-generation stents, resulting in limited adoption of the most effective technologies and increased reliance on outdated or less durable options

- According to Medtronic and Boston Scientific, pricing disparities between high-end DES and generic alternatives, along with limited government subsidies in certain regions, restrict patient access to the latest coronary stent innovations.

- These financial and infrastructural barriers hinder equitable access to advanced interventional cardiology. Addressing them through pricing reform, broader insurance coverage, tiered product offerings, and government-supported subsidy programs will be essential to ensure global market expansion and improved patient outcomes.

Coronary Stents Market Scope

The market is segmented on the type, absorption rate, material, rate, application, mode of delivery and end users.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Absorption Rate |

|

|

By Material |

|

|

By Rate |

|

|

By Application |

|

|

By Mode Of Delivery |

|

|

By End Users |

|

In 2025, the Drug-Eluting Stents (DES) Segmentis Projected to Dominate the Market with the Largest Share in the type Segment

The Drug-Eluting Stents (DES) segment is expected to dominate the Global Coronary Stents Market in 2025, accounting for the largest market share of approximately 68.7%. This leadership is primarily driven by the superior clinical outcomes associated with DES, including significantly reduced rates of restenosis and revascularization compared to bare-metal stents (BMS). DES are coated with pharmacological agents that inhibit cell proliferation, effectively preventing arterial re-narrowing post angioplasty—a major breakthrough in interventional cardiology.

cardiac centers are Expected to Account for the Largest Share During the Forecast Period in end user segment

In 2025, hospitals and cardiac centers are projected to dominate the Global Coronary Stents Market, accounting for the largest market share of approximately 64.9%. This segment's dominance is fueled by the rising global burden of cardiovascular diseases, particularly coronary artery disease (CAD), which necessitates timely and sophisticated interventional procedures such as percutaneous coronary interventions (PCI). Hospitals and specialized cardiac centers remain the primary treatment hubs for patients requiring angioplasty and stent implantation, owing to their access to state-of-the-art catheterization laboratories, skilled interventional cardiologists, and comprehensive post-operative care infrastructure. Advanced healthcare facilities in countries such as the U.S., Germany, Japan, and China are heavily investing in next-generation stenting technologies, including drug-eluting stents (DES), bioresorbable scaffolds, and image-guided intervention systems, to enhance procedural accuracy and long-term clinical outcomes.

Coronary Stents Market Regional Analysis

“North America is the Dominant Region in the Global Coronary Stents Market”

- North America leads the global coronary stents market, driven by its advanced healthcare infrastructure, high procedural volumes of percutaneous coronary interventions (PCI), and widespread availability of cutting-edge stent technologies such as drug-eluting stents (DES) and bioresorbable scaffolds.

- The United States holds the largest market share, owing to the rising prevalence of coronary artery disease (CAD), growing aging population, and increasing lifestyle-related risk factors such as obesity, hypertension, and diabetes.

- Favorable reimbursement policies, extensive healthcare coverage, and strong government support for cardiovascular health programs contribute significantly to the region’s market dominance.

- Additionally, the presence of key players such as Abbott, Boston Scientific, and Medtronic, along with continuous R&D investments and clinical trial activity, fuels technological innovation and product adoption across North America

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- The Asia-Pacific region is anticipated to experience the fastest growth in the coronary stents market, driven by the rising burden of cardiovascular diseases, improving healthcare access, and increasing adoption of interventional cardiology procedures.

- Countries like China, India, and Japan are emerging as key markets due to large patient populations, higher demand for minimally invasive procedures, and government-led initiatives to address the growing cardiovascular health crisis.

- Japan, with its well-developed medical infrastructure and aging population, is a leader in adopting advanced DES and imaging-guided PCI techniques.

- In China and India, growing investments in healthcare infrastructure, an expanding network of cardiac care centers, and increasing awareness of CAD management are fueling market expansion.

- Moreover, the rise of domestic stent manufacturers and cost-effective product offerings, combined with supportive regulatory reforms, are positioning the region as a key growth engine for the global coronary stents market.region

Coronary Stents Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Abbott Laboratories (U.S.)

- Medtronic plc (Ireland)

- Boston Scientific Corporation (U.S.

- BIOTRONIK SE & Co. KG (Germany)

- Terumo Corporation (Japan)

- B. Braun Melsungen AG (Germany)

- Cook Medical (U.S.)

- MicroPort Scientific Corporation (China)

- Biosensors International Group, Ltd. (Singapore)

- Alvimedica (Turkey

- Cardinal Health, Inc. (U.S.)

- Meril Life Sciences Pvt. Ltd. (India)

- JW Medical Systems Ltd. (China)

- Hexacath (France)

- Relisys Medical Devices Ltd. (India)

Latest Developments in Global Coronary Stents

- In March 2025, Boston Scientific Corporation announced the commercial launch of its latest generation Synergy XD drug-eluting stent in major global markets. The stent features a redesigned delivery system aimed at enhancing placement accuracy and procedural efficiency, especially in complex lesions.

- In January 2025, Medtronic plc received CE Mark approval for its NextGen Resolute Onyx DES, incorporating a new polymer technology designed to improve endothelial healing and reduce long-term thrombosis risks. The product is expected to drive growth in European and Asia-Pacific markets.

- In November 2024, Abbott Laboratories announced positive long-term results from its XIENCE 90 post-market study, showing superior safety and efficacy of the XIENCE drug-eluting stent with a shorter dual antiplatelet therapy (DAPT) duration, enhancing patient compliance and reducing bleeding risks.

- In August 2024, Biotronik SE & Co. KG launched its Orsiro Mission DES in Latin America, strengthening its regional footprint. The stent is known for its ultrathin struts and bioabsorbable polymer coating, tailored for improving outcomes in patients with complex coronary artery disease.

- In June 2024, Terumo Corporation announced the expansion of its Ultimaster Tansei DES platform in Southeast Asia. The move aligns with the company's strategy to capture the growing demand for advanced interventional cardiology solutions in emerging markets.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.