Global Core Materials Market

Market Size in USD Billion

CAGR :

%

USD

4.19 Billion

USD

6.84 Billion

2024

2032

USD

4.19 Billion

USD

6.84 Billion

2024

2032

| 2025 –2032 | |

| USD 4.19 Billion | |

| USD 6.84 Billion | |

| % | |

|

Core Materials Market Size

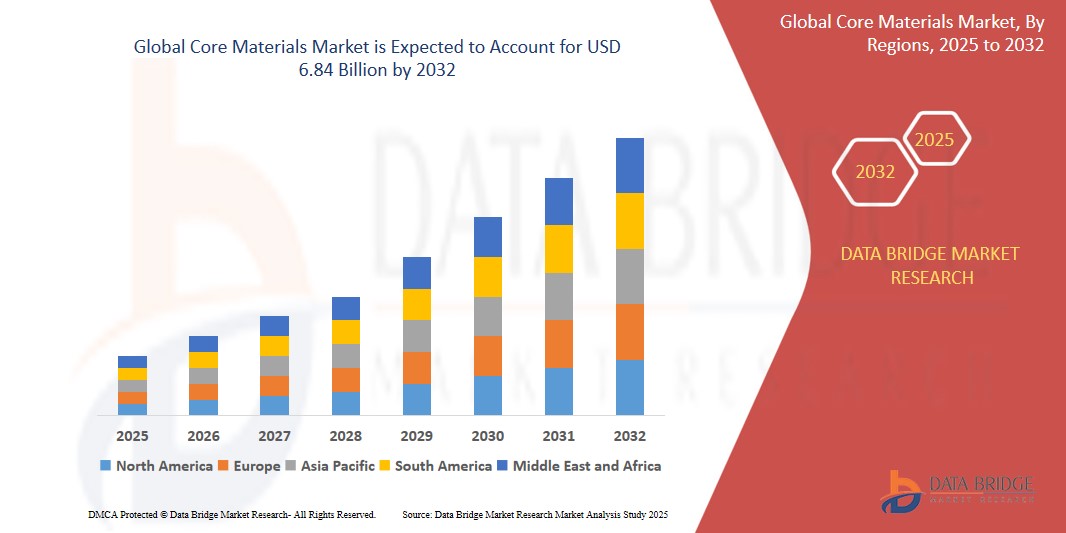

- The global core materials market was valued at USD 4.19 billion in 2024 and is expected to reach USD 6.84 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 6.34%, primarily driven by rising renewable energy demand, aerospace advancements, lightweight composites, infrastructure growth, and automotive sector expansion are key growth drivers globally

- This growth is driven by factors such as increasing wind energy installations, booming aerospace industry, demand for fuel-efficient vehicles, infrastructure development, and rising use of composite materials worldwide

Core Materials Market Analysis

- Core Materials are utilized in advanced applications across wind energy, aerospace, marine, and automotive industries to enhance structural integrity, weight reduction, fuel efficiency, and durability. These materials enable superior performance and foster collaborations among resin producers, composite manufacturers, and OEMs to drive innovation and meet evolving sustainability and performance standards

- The demand for Core Materials is significantly driven by the rising need for lightweight composites, energy efficiency, and high-strength applications. Increased focus on renewable energy, especially wind power, aerospace safety, and marine durability propels adoption. Additionally, advancements in foam, balsa, and honeycomb cores improve mechanical properties and cost-efficiency. Government initiatives promoting renewable energy, carbon reduction, and sustainable construction further stimulate market growth, alongside rising investments in eco-friendly technologies

- The Asia-Pacific region stands out as one of the dominant regions for core materials, driven by its booming wind energy projects, expanding aerospace sector, and growing infrastructure development with lightweight composite adoption

- For instance, China leads in Core Materials adoption. Major energy and aerospace companies leverage advanced core materials, supported by government renewable energy targets, infrastructure expansion policies, and incentives to enhance structural performance, sustainability, and project efficiency

- Globally, the Core Materials market ranks as a critical segment within the composites and advanced materials space, playing a pivotal role in enhancing product strength, reducing weight, improving energy efficiency, and supporting sustainability across industries such as energy, aerospace, marine, and automotive

Report Scope and Core Materials Market Segmentation

|

Attributes |

Core Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Core Materials Market Trends

“Increasing demand from the wind energy industry”

- One prominent trend in the advancement of Core Materials is the rapid expansion of the wind energy sector, which is significantly boosting demand for lightweight, durable core materials in turbine blade manufacturing

- Core Materials provide essential benefits such as weight reduction, enhanced structural strength, and fatigue resistance, making them critical for improving turbine efficiency, lifespan, and performance under demanding environmental conditions

- For instance, with the surge in global wind energy installations, manufacturers are increasingly adopting foam, balsa, and honeycomb cores to construct larger, more efficient blades, meeting both renewable energy targets and cost-optimization goals

- The widespread integration of advanced core materials in wind turbines contributes to higher energy output, reduced maintenance costs, and greater reliability, reinforcing the viability of wind as a major renewable energy source

Core Materials Market Dynamics

Driver

“Growing need for composites in the aerospace industry”

- The rising demand for lightweight, fuel-efficient aircraft is significantly driving the growth of the Core Materials market within the aerospace industry

- As the aerospace sector pushes for enhanced performance, fuel savings, and reduced emissions, manufacturers are increasingly focused on developing advanced composite materials that leverage high-strength, lightweight core materials for critical structural components

- Core Materials are extensively used in aircraft fuselage panels, wings, interior structures, and engine nacelles due to their ability to reduce overall aircraft weight, enhance structural integrity, and improve aerodynamic efficiency

- These materials not only enhance aircraft fuel economy and performance but also contribute to lower maintenance costs and extended service life, aligning with stringent safety and environmental standards in the aerospace industry

- As global air travel demand rises and aerospace companies aim to meet both economic and sustainability goals, the adoption of innovative Core Materials is poised to expand, supporting the evolution of next-generation aircraft designs

For instance,

- In 2015, Airbus introduced the A350 XWB, an advanced long-range aircraft that incorporates over 50% composites by weight. The design integrates honeycomb and foam core materials within fuselage panels and wing structures, significantly reducing aircraft weight while enhancing fuel efficiency and overall performance

- In December 2014, NASA launched the Orion spacecraft, engineered with advanced composite structures utilizing honeycomb and foam core materials. These cores are integrated into structural panels and heat shields, delivering exceptional strength-to-weight performance essential for atmospheric re-entry and deep-space exploration missions

Opportunity

“Significant need for core materials in the 3D printing and medical industry”

- The growing demand for advanced core materials in the 3D printing and medical industries is driven by their ability to provide lightweight, customizable, and high-strength structures for intricate applications

- These core materials enable the production of complex geometries in medical implants, prosthetics, and personalized devices, enhancing both performance and patient comfort. In 3D printing, they contribute to improved material efficiency and quicker production times

- Additionally, the adoption of core materials in these industries aligns with trends toward precision manufacturing, faster medical interventions, and patient-specific solutions, supporting the medical and 3D printing sectors’ shift toward more efficient, customizable, and innovative technologies

For instance,

- In 2022, advancements in 3D printing technology led to the increased use of core materials such as polymer foams and lightweight honeycomb structures in orthopedic implants. These materials reduce implant weight, promote bone growth, and enhance overall implant performance, paving the way for personalized, patient-specific healthcare solutions

Restraint/Challenge

“Stringent regulatory standards regarding emissions and environmental impact”

- While there is increasing adoption of core materials in various industries, stringent regulatory standards regarding emissions and environmental impact remain a significant challenge for wider market acceptance

- These regulations, while essential for sustainability, impose additional compliance costs and complexity on manufacturers, requiring them to adopt eco-friendly materials and production processes that meet emission reduction targets and minimize environmental harm

- The higher costs of adhering to these regulatory standards can deter smaller manufacturers and emerging market players, limiting the broader implementation of advanced core materials and slowing down overall market growth in some regions

Core Materials Market Scope

The market is segmented on the basis of type, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By End User |

|

Core Materials Market Regional Analysis

“Asia-Pacific is the Dominant Region in the Core Materials Market”

-

The Asia-Pacific region is a key growth driver in the Core Materials market, propelled by rapid industrialization, increased automotive production, and the growing demand for renewable energy solutions

- China holds a dominant position in the market due to its booming automotive and wind energy sectors, with manufacturers increasingly adopting lightweight core materials to enhance performance and meet sustainability goals

- The region's strong manufacturing base, coupled with advancements in aerospace, automotive, and construction industries, creates a favorable environment for the growth of the Core Materials market in Asia-Pacific

- Furthermore, the rising consumer demand for energy-efficient solutions, coupled with government initiatives promoting clean energy technologies, continues to drive the adoption of core materials across key industries in the Asia-Pacific region

“North America is Projected to Register the Highest Growth Rate”

-

The North American region is expected to witness steady growth in the Core Materials market, driven by the increasing demand for advanced manufacturing solutions and the automotive industry's focus on lightweight, high-performance materials

- The U.S. stands out as a key market, propelled by its robust automotive and aerospace industries, where core materials such as honeycomb structures and composite cores are increasingly used for fuel-efficient and sustainable applications

- Canada, with its growing renewable energy sector, particularly in wind power, also presents significant opportunities for core material adoption in turbine blade manufacturing and other infrastructure projects

- The increasing focus on sustainability, coupled with regulatory pressures to reduce emissions, is driving the demand for eco-friendly and high-performance core materials in North America, further accelerating market growth

Core Materials Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Stahl Holdings BV (Netherlands)

- Lear Corporation (U.S.)

- Toyota Boshoku Corporation (Japan)

- Technical Textile Services Ltd. (U.K)

- ZF Friedrichshafen AG (Germany)

- Faurecia S.A. (France)

- Delphi Technologies (U.K)

- Grammer AG (Germany)

- Johnson Controls (Ireland)

- Grupo Antolin (Spain)

Latest Developments in Global Core Materials Market

- In January 2024, Gurit introduced two new products. The first, Gurit Kerdyn FR+, is a PET recycled structural foam that holds Class C - EN13501 certification. It offers excellent compressive strength and stiffness. The second, Balsaflex Lite, is a next-generation balsa and PET core material featuring an innovative coating system that minimizes resin uptake during infusion processes. Additionally, in October 2023, Gurit secured significant long-term supply agreements with two major OEMs, which are expected to drive substantial net sales over the duration of the contracts

- In June 2022, Korean Aerospace Industries (KAI) entered into a new long-term agreement with The Gill Corporation. Under this contract, The Gill Corporation will provide non-metallic honeycomb products from its El Monte division and metallic honeycomb products from its Maryland division. In May 2022, 3A Composites Core Materials acquired SOLVAY's TegraCore PPSU resin-based foam, incorporating it into the AIREX TegraCore portfolio. Both companies agreed to continue their collaboration to further advance the development of AIREX TegraCore

- In February 2021, Armacell International S.A. introduced its new flexible PET foams to the global market, aiming to enhance revenue generation

- In February 2021, Euro-Composites S.A. introduced its poly-shaped core material, designed for use in boats, helicopters, aircraft, and various other applications. The launch of this core material is intended to strengthen its presence across different end-use industries

- In November 2019, Evonik Industries announced an increase in its production capacity for lightweight construction materials by expanding its ROHACELL closed foam cell production in North America. This expansion aims to boost revenue generation

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Core Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Core Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Core Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.