Global Kyphoplasty Market

Market Size in USD Billion

CAGR :

%

USD

1.68 Billion

USD

4.52 Billion

2024

2032

USD

1.68 Billion

USD

4.52 Billion

2024

2032

| 2025 –2032 | |

| USD 1.68 Billion | |

| USD 4.52 Billion | |

| % | |

|

Kyphoplasty Market Size

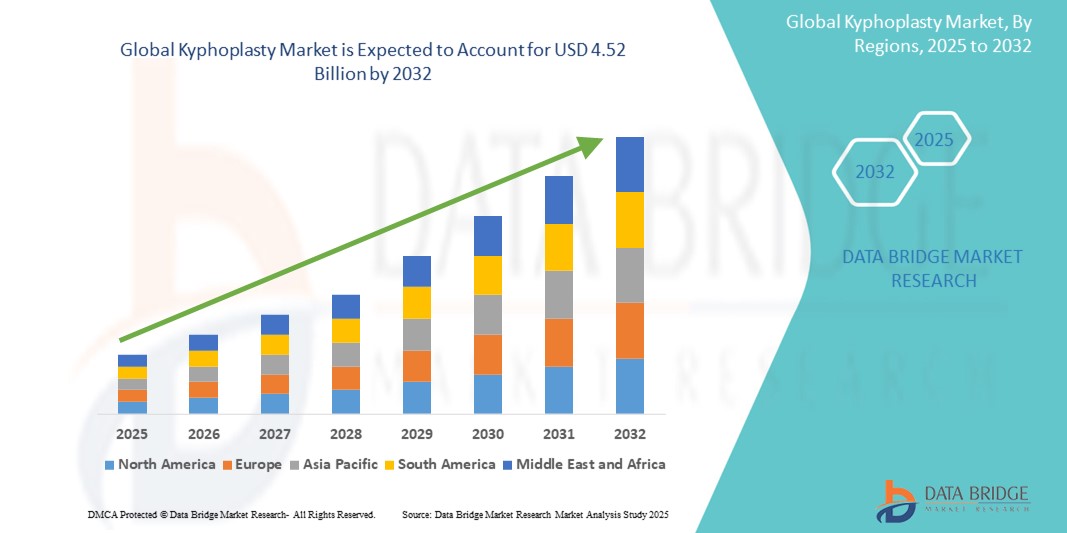

- The global kyphoplasty market size was valued at USD 1.68 billion in 2024 and is expected to reach USD 4.52 billion by 2032, at a CAGR of 13.20% during the forecast period

- This growth is driven by factors such as more spinal fractures, demand for minimally invasive surgery, tech advancements, and better healthcare access

Kyphoplasty Market Analysis

- Kyphoplasty is a minimally invasive surgical procedure used to restore the height and stability of fractured vertebrae, primarily caused by osteoporosis or spinal injuries. It plays a crucial role in relieving pain, correcting spinal deformities, and improving patient mobility across healthcare settings

- The market is experiencing steady growth, driven by the rising incidence of osteoporosis and vertebral compression fractures, increasing preference for minimally invasive treatments, continuous technological innovations, and the global expansion of healthcare services

- North America is expected to dominate the kyphoplasty market with a share of 51.6%, due to the increasing incidence of osteoporosis, rising adoption of kyphoplasty procedures, and the presence of advanced healthcare infrastructure in the region

- Asia-Pacific is expected to be the fastest growing region in the kyphoplasty market during the forecast period due to

- Balloon kyphoplasty systems segment is expected to dominate the market with a market share of 40.3% due to their proven effectiveness in restoring vertebral body height, reducing spinal deformity, and providing rapid pain relief compared to traditional methods. In addition, the minimally invasive nature of the procedure, shorter recovery times, and rising prevalence of osteoporosis-related vertebral compression fractures globally are key factors driving the preference for balloon kyphoplasty over other systems

Report Scope and Kyphoplasty Market Segmentation

|

Attributes |

Kyphoplasty Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Kyphoplasty Market Trends

“Growing Prevalence of Osteoporosis and Vertebral Compression Fractures”

- One prominent trend in the global kyphoplasty market is the growing prevalence of osteoporosis and vertebral compression fractures

- This trend is driven by the aging global population, increasing sedentary lifestyles, and a rise in bone health-related disorders, leading to higher demand for vertebral fracture treatments

- For instance, organizations such as the International Osteoporosis Foundation report that millions suffer osteoporotic fractures annually, significantly raising the need for effective interventions such as kyphoplasty

- The surge in fracture cases is also encouraging innovation in kyphoplasty techniques and devices aimed at faster recovery, better vertebral height restoration, and pain reduction

- As healthcare providers focus on minimizing disability and improving quality of life for elderly and at-risk populations, the rising burden of osteoporosis and vertebral fractures is expected to strongly drive kyphoplasty market growth

Kyphoplasty Market Dynamics

Driver

“Rising Number of Geriatric Population”

- The rising number of the geriatric population is a significant driver for growth in the kyphoplasty market, as older adults are more prone to osteoporosis and vertebral compression fractures

- This shift is particularly prominent in healthcare sectors focused on spine health, where advanced kyphoplasty procedures are essential for restoring vertebral height, reducing pain, and improving mobility

- With the increasing number of elderly individuals globally, there is a growing demand for minimally invasive treatments such as kyphoplasty to address age-related spinal issues

- Manufacturers are advancing kyphoplasty technologies to offer better procedural outcomes, shorter recovery times, and enhanced patient satisfaction to meet the evolving needs of the aging population

- The push for improved care for elderly individuals, along with the rising incidence of bone fractures, is intensifying the demand for kyphoplasty procedures in hospitals, clinics, and outpatient surgical centers

For instance,

- Medtronic and Stryker have developed innovative kyphoplasty devices designed for optimal performance in geriatric patients, ensuring better fracture stabilization and quicker recovery

- KARL STORZ has focused on enhancing the imaging guidance and procedural tools in its kyphoplasty devices to support optimal treatment for older patients with complex spinal conditions

- The kyphoplasty market is set for strong growth, driven by the increasing geriatric population, technological advancements in kyphoplasty systems, and the growing focus on improving quality of life for elderly individuals

Opportunity

“Growing Number of R&D Activities”

- The growing number of R&D activities presents a significant opportunity for the kyphoplasty market, driven by the increasing need for improved treatments and devices for spinal fractures and deformities

- Healthcare sectors are focusing on advanced technologies that enhance the precision, efficiency, and outcomes of kyphoplasty procedures, creating a demand for innovative devices and systems

- This opportunity aligns with the broader trend toward minimally invasive spine surgeries, where continuous research and development are improving treatment options and patient recovery

For instance,

- Zimmer Biomet has introduced advanced robotic-assisted systems aimed at enhancing precision and reducing recovery times for patients undergoing kyphoplasty

- Johnson & Johnson is conducting research on new biomaterials for kyphoplasty that enhance bone healing and prevent future fractures

- As R&D activities continue to advance, the kyphoplasty market is expected to experience significant growth, fueled by the development of more effective, less invasive, and safer treatment options for spinal conditions

Restraint/Challenge

“High Cost of Minimally Invasive Ablation Procedures”

- The high cost of minimally invasive ablation procedures presents a significant challenge for the kyphoplasty market, particularly with the increasing demand for advanced spinal treatments

- The expense of specialized equipment, surgical tools, and post-operative care can limit the accessibility of kyphoplasty procedures for healthcare providers, especially in cost-sensitive markets

- This challenge is especially prominent in regions with budget constraints and healthcare systems that prioritize cost-effective treatments, where the high cost of kyphoplasty may hinder its widespread adoption

For instance,

- Manufacturers of kyphoplasty devices face increased production costs due to the need for advanced materials, research, and development, as well as regulatory approvals to ensure safety and efficacy

- The financial burden associated with these procedures may slow the adoption of kyphoplasty in both developing and developed healthcare systems, potentially limiting overall market growth

Kyphoplasty Market Scope

The market is segmented on the basis of product type, application, and end user.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Application |

|

|

By End User |

|

In 2025, the balloon kyphoplasty systems is projected to dominate the market with a largest share in product type segment

The balloon kyphoplasty systems segment is expected to dominate the kyphoplasty market with the largest share of 40.3% in 2025 due to their proven effectiveness in restoring vertebral body height, reducing spinal deformity, and providing rapid pain relief compared to traditional methods. In addition, the minimally invasive nature of the procedure, shorter recovery times, and rising prevalence of osteoporosis-related vertebral compression fractures globally are key factors driving the preference for balloon kyphoplasty over other systems.

The restoring lost vertebral body is expected to account for the largest share during the forecast period in application market

In 2025, the restoring lost vertebral body segment is expected to dominate the market due to increasing incidence of osteoporotic vertebral compression fractures and the growing demand for treatments that quickly stabilize the spine, restore height, and relieve pain. Advances in minimally invasive kyphoplasty techniques and heightened awareness among both patients and healthcare providers about the benefits of early intervention are further boosting this segment's growth.

Kyphoplasty Market Regional Analysis

“North America Holds the Largest Share in the Kyphoplasty Market”

- North America dominates the kyphoplasty market with a share of 51.6%, driven by the increasing incidence of osteoporosis, rising adoption of kyphoplasty procedures, and the presence of advanced healthcare infrastructure in the region

- U.S. holds a significant share due to its strong medical device industry, extensive healthcare network, and the growing prevalence of age-related conditions such as osteoporosis and vertebral compression fractures

- The region’s sophisticated healthcare infrastructure, combined with innovations in kyphoplasty technologies such as improved balloon designs and imaging guidance systems, enhances the accuracy and effectiveness of these procedures. This has led to higher patient satisfaction and adoption rates across hospitals, clinics, and ambulatory surgical centers

- As the demand for effective spinal fracture treatments increases, North America is expected to maintain its dominant position through 2032, supported by continuous technological advancements, a high level of healthcare expenditure, and favorable reimbursement policies

“Asia-Pacific is Projected to Register the Highest CAGR in the Kyphoplasty Market”

- Asia-Pacific is expected to witness the highest growth rate in the kyphoplasty market, driven by rapid urbanization, increasing healthcare investments, and a growing geriatric population

- China holds a significant share due to expansion of healthcare infrastructure, rising awareness of osteoporosis, and the increasing number of spinal fractures among elderly individuals

- The growing demand for minimally invasive surgical procedures in countries such as Japan, South Korea, and India is also contributing to the expansion of the kyphoplasty market. Local manufacturers are playing a key role in market growth by offering cost-effective solutions tailored to the needs of the region

- With continued investments in healthcare infrastructure, stronger public-private partnerships, and greater access to medical funding, Asia-Pacific is set to emerge as the fastest-growing region in the kyphoplasty market through 2032

Kyphoplasty Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Medtronic (Ireland)

- B.D. (U.S.)

- Abbott (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Stryker (U.S.)

- Osseon LLC. (U.S.)

- Alphatec Spine, Inc. (U.S.)

- G21 S.r.l. (Italy)

- Globus Medical (U.S.)

- SOMATEX Medical Technologies GmbH (Germany)

- Parallax health Sciences, Inc. (U.S.)

- Merit Medical Systems (USA)

- RONTIS (Switzerland)

- ZAVATION (U.S.)

- IZI Medical Products (U.S.)

- Teknimed (France)

- BPB medica (Italy)

- Cook (US)

- Zimmer Biomet (U.S.)

Latest Developments in Global Kyphoplasty Market

- In April 2022, Nanox received approval from the U.S. FDA for its HealthOST device, an AI-powered software designed to monitor vertebral compression fractures and detect osteoporosis by assessing poor bone density. This advancement in diagnostic technology positions Nanox to strengthen its competitive edge in the market, offering innovative solutions for early osteoporosis detection and expanding its portfolio of medical devices

- In August 2021, IZI Medical Products launched the Vertefix HV cement, an advanced device for kyphoplasty and vertebroplasty surgeries that enables real-time flow visualization during cement injection. This innovation enhances the precision and effectiveness of kyphoplasty procedures, allowing IZI Medical Products to broaden its product offerings and capture a larger share of the growing kyphoplasty market

- In May 2021, Medtronic plc had announced the U.S. launch of New Directional Cannula for Balloon Kyphoplasty. According to a study, hospitals in the United States reported a 35 percent drop in operating room volume from March to July 2020. During the COVID period, however, the market for robotic spinal surgery increased. Furthermore, the demand for spinal surgery medical instruments and equipment has decreased dramatically

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.