Global Rigid Paper Containers Market

Market Size in USD Billion

CAGR :

%

USD

80.76 Billion

USD

128.54 Billion

2024

2032

USD

80.76 Billion

USD

128.54 Billion

2024

2032

| 2025 –2032 | |

| USD 80.76 Billion | |

| USD 128.54 Billion | |

| % | |

|

Rigid Paper Containers Market Size

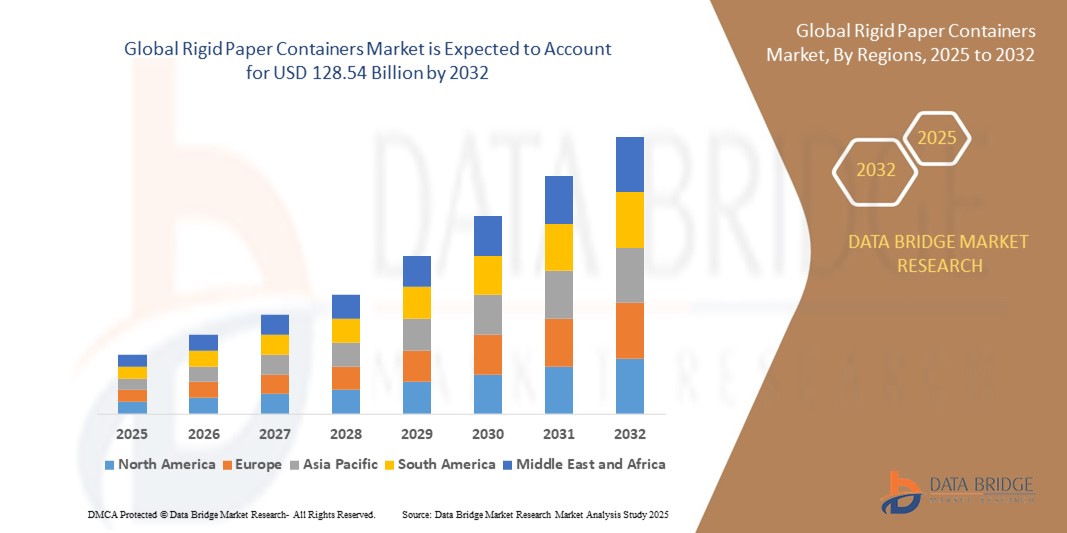

- The Global Rigid Paper Containers Market size was valued at USD 80.76 Billion in 2024 and is expected to reach USD 128.54 Billion by 2032, at a CAGR of 5.3% during the forecast period

- The market growth is largely fueled by rising demand for eco-friendly packaging solutions

- Furthermore, the Rising production of paper is indirectly fostering the growth of rigid paper container market and rising consumer awareness, rising demand for packaged food and beverages because of rising population and rising personal disposable income, are further anticipated to propel the growth of the Rigid Paper Containers Market

Rigid Paper Containers Market Analysis

- Rigid paper container is paper based packaging solutions manufactured using either paperboard or container board.

- They are widely used by verticals such as food and beverages, pharmaceuticals, cosmetics and personal care, automotive and allied industries, electronics and electricals and other consumer goods, rigid paper containers are designed to store solid products which are generally made of cellulosic materials

- North America dominates the Rigid Paper Containers Market with the largest revenue share of 35.1% in 2024, characterized by strong demand from end-use sectors such as food and beverages, healthcare, and personal care.

- Asia-Pacific is expected to be the fastest growing region in the Rigid Paper Containers Market during the forecast period due to rapid urbanization, industrialization, and the rise of middle-class consumers

- The paperboard segment is expected to dominate the Rigid Paper Containers Market with a market share of 43.2% in 2024, driven by its lightweight nature, ease of printing, and superior folding properties

Report Scope and Rigid Paper Containers Market Segmentation

|

Attributes |

Glass Fiber Reinforced Plastics Composites Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Rigid Paper Containers Market Trends

“Sustainable Barrier Coatings Replacing Plastic Liners”

- A growing trend in the Global Rigid Paper Containers Market is the adoption of bio-based and recyclable barrier coatings as alternatives to plastic liners, driven by sustainability goals and regulatory pressure.

- For example, in 2024, Stora Enso expanded its production of dispersion-coated paperboard, eliminating the need for polyethylene (PE) films in food-grade packaging.

- Similarly, Mondi launched paper-based containers with water-based coatings offering grease and moisture resistance, aligning with EU directives on single-use plastics.

- These innovations support recyclability and compostability, making rigid paper containers more appealing for food, personal care, and pharmaceutical applications

Rigid Paper Containers Market Dynamics

Driver

“Rising Demand from E-commerce and Automated Warehousing”

- The exponential growth of e-commerce and the shift towards automated warehousing systems are major drivers for the Global Rigid Paper Containers Market.

- Online retailers and third-party logistics providers are investing in durable and cost-effective packaging solutions to optimize packaging and transportation.

- The need for efficient handling and storage solutions in automated warehouses has led to increased demand for standardized, nestable, and stackable rigid paper containers.

- This trend is further supported by the growing emphasis on sustainability, leading to a higher demand for recyclable and biodegradable packaging options.

Restraint/Challenge

“High Initial Investment and Integration Costs for Smart Packaging”

- The high initial investment required for smart packaging equipped with IoT and RFID technologies poses a significant challenge for the market.

- These costs include hardware integration, software for tracking and data analytics, and infrastructure upgrades to ensure compatibility with existing supply chain systems.

- For small and medium enterprises (SMEs), these expenses can be prohibitive, limiting adoption despite long-term benefits such as enhanced durability, reduced maintenance, and supply chain transparency.

- Additionally, the integration of electronic components into packaging materials can complicate recycling processes, leading to environmental concerns and potential regulatory challenges.

Rigid Paper Containers Market Scope

The market is segmented on the basis of board type, product type, end use, and industry verticals.

- By Board Type

On the basis of board type, the Rigid Paper Containers Market is segmented into Paperboard and Containerboard. The Paperboard segment dominates the largest market revenue share of 43.2% in 2025, driven by its lightweight nature, ease of printing, and superior folding properties. Widely used in folding cartons and display packaging, paperboard enables high-quality branding and is preferred in food, personal care, and electronics packaging. Its recyclability and alignment with eco-conscious consumer behavior continue to drive demand.

The Containerboard segment is anticipated to witness the fastest growth rate of 8.7% from 2025 to 2032, fueled by increasing adoption in e-commerce packaging and shipping logistics. Containerboard offers high stacking strength and durability, making it suitable for corrugated boxes and trays. Rising global trade volumes and sustainability initiatives are accelerating containerboard consumption in industrial packaging.

- By Product Type

On the basis of product type, the Rigid Paper Containers Market is segmented into Boxes, Tubes, Trays, Liquid Cartons, and Clamshells. The Boxes segment held the largest market revenue share in 2025, driven by their extensive use in shipping, retail packaging, and storage applications. Boxes offer structural strength and versatility, making them indispensable across industries such as food, electronics, and apparel.

The Liquid Cartons segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising demand for shelf-stable beverage packaging. Liquid cartons are designed for both aseptic and non-aseptic filling and offer excellent barrier properties, recyclability, and branding surfaces. Growing health-conscious consumption of dairy, juices, and plant-based drinks is a key growth driver.

- By End Use

On the basis of end use, the Rigid Paper Containers Market is segmented into Bags and Pouches, Sacks, Envelopes, Corrugated Sheets, Composite Cans, and Cartons. The Cartons segment dominates the largest market revenue share of 39.4% in 2025, driven by their extensive application in consumer goods packaging. Cartons offer high printability, tamper resistance, and user-friendly handling, which makes them ideal for premium and everyday items alike.

The Composite Cans segment is anticipated to witness the fastest growth rate of 9.3% from 2025 to 2032, fueled by increasing use in snacks, powdered beverages, and luxury packaging. These cans combine strength with product differentiation capabilities and offer eco-friendlier alternatives to metal or plastic formats, enhancing appeal among environmentally conscious brands.

- By Industry Verticals

On the basis of industry verticals, the Rigid Paper Containers Market is segmented into Food and Beverages, Pharmaceuticals, Cosmetics and Personal Care, Automotive and Allied Industries, Electronics and Electricals, and Other Consumer Goods. The Food and Beverages segment held the largest market revenue share in 2025, driven by high consumption of packaged snacks, cereals, frozen foods, and ready-to-drink beverages. Paper-based rigid packaging provides product safety, convenience, and eco-appeal, supporting mass-market and premium positioning.

The Pharmaceuticals segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising global health expenditure and regulatory emphasis on sustainable pharmaceutical packaging. Rigid paper containers are gaining traction in over-the-counter (OTC) and prescription drug packaging due to their compliance readiness, barrier performance, and lower environmental impact compared to plastic.

Rigid Paper Containers Market Regional Analysis

- North America dominates the Rigid Paper Containers Market with the largest revenue share of 35.1% in 2024, driven strong demand from end-use sectors such as food and beverages, healthcare, and personal care.

- Stringent regulations on packaging materials and a strong focus on sustainability have further propelled the adoption of recyclable and reusable rigid packaging formats.

U.S. Rigid Paper Containers Market Insight

The U.S. Rigid Paper Containers Market captured the largest revenue share of 82.03% in 2025 within North America, fueled by strong domestic manufacturing capabilities and technological advancement. The U.S. market is primarily driven by the expanding e-commerce sector, with companies like Amazon implementing sustainable packaging initiatives.

Europe Rigid Paper Containers Market Insight

The European Rigid Paper Containers Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by high consumer awareness about sustainability and eco-friendly practices, coupled with stringent regulations promoting recyclable and biodegradable packaging. Countries like Germany, France, and the United Kingdom lead the market with well-established industrial bases and innovation-driven production capabilities.

U.K. Rigid Paper Containers Market Insight

The U.K. Rigid Paper Containers Market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing consumer demand for sustainable packaging solutions and government initiatives promoting environmental responsibility. The country's strong retail sector and emphasis on reducing plastic usage contribute to the adoption of paper-based packaging alternatives.

Germany Rigid Paper Containers Market Insight

The German Rigid Paper Containers Market is expected to expand at a considerable CAGR during the forecast period, fueled by its strong manufacturing base, technological advancement, and robust recycling infrastructure. German manufacturers are at the forefront of developing innovative and sustainable packaging solutions, supported by significant investments in research and development.

Asia-Pacific Rigid Paper Containers Market Insight

The Asia-Pacific Rigid Paper Containers Market is poised to grow at the fastest CAGR of over 8.5% during the forecast period of 2025 to 2032, driven by rapid urbanization, industrialization, and the rise of middle-class consumers in countries like China, India, and Southeast Asian economies.

Japan Rigid Paper Containers Market Insight

The Japan Rigid Paper Containers Market is gaining momentum due to technological innovation and a strong culture of environmental responsibility. The country's machinery and precision tools industries are turning to high-performance bio-lubricants for efficiency and lower toxicity.

China Rigid Paper Containers Market Insight

China Rigid Paper Containers Market accounted for the largest market revenue share in Asia Pacific in 2025, driven by its vast manufacturing capabilities, large consumer base, and growing adoption of sustainable packaging solutions. Chinese manufacturers continue to invest in advanced technologies and production capabilities to meet increasing domestic and international demand.

Rigid Paper Containers Market Share

The Glass Fiber Reinforced Plastics Composites Industry is primarily led by well-established companies, including:

- Amcor plc (Switzerland)

- DS Smith (U.K.)

- Huhtamäki Oyj (Finland)

- Omniform (South Africa)

- Berry Global Inc. (U.S.)

- Evergreen Packaging LLC (U.S.)

- Holmen (Sweden)

- International Paper (U.S.)

- Mayr-Melnhof Karton AG (Austria)

- WestRock Company (U.S.)

- Smurfit Kappa (Ireland)

- Graphic Packaging International, LLC (U.S.)

- Stora Enso (Finland)

- Cascades Inc. (Canada)

- Sappi (South Africa)

- Svenska Cellulosa Aktiebolaget SCA (publ) (Sweden)

- Sonoco Products (U.S.)

Latest Developments in Global Rigid Paper Containers Market

- In March 2024, 3M introduced an innovative solution aimed at revolutionizing the shipping and packaging industry. This new product is engineered to boost sustainability and efficiency in logistics, responding to the increasing demand for eco-conscious alternatives. By utilizing advanced materials and cutting-edge technology, 3M’s development aims to minimize waste and streamline the shipping process. This launch underscores the company's dedication to environmental responsibility while equipping businesses with effective, modern packaging solutions.

- In May 2022, Lecta expanded its Adestor range of self-adhesive materials by launching the Adestor Standard Films series. This new line includes polypropylene and polyethylene films tailored for labeling across various sectors, including food, industrial, and hygiene. The films offer excellent transparency and flexibility, meeting a wide array of packaging requirements. Additionally, Lecta enhanced its service portfolio with the Exact Cut program, providing customized roll formats—all produced under strict environmental and quality regulations.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Rigid Paper Containers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Rigid Paper Containers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Rigid Paper Containers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.