Global Agriculture Drones Market

Marktgröße in Milliarden USD

CAGR :

%

USD

3.88 Billion

USD

16.79 Billion

2025

2033

USD

3.88 Billion

USD

16.79 Billion

2025

2033

| 2026 –2033 | |

| USD 3.88 Billion | |

| USD 16.79 Billion | |

| % | |

|

Global Agriculture Drone Market Segmentation, By Type (Fixed-Wing Drones, Multi-Rotor Drones, and Hybrid Drones), Product (Software and Hardware), Battery Life ( 100 Minutes), Components (Flight Controllers, Propulsion Systems, Camera System, Batteries, and Global Positioning System), Mode of Operation (Fully-Autonomous, Semi-Autonomous, and Remotely Operated), Range (Extended Visual Line of Sight, Beyond Line of Sight, and Visual Line of Sight), Technology (GNSS, Obstacle Detection and Collision Avoidance Technology, Drone Analytics, and Others), Application (Spraying, Field Mapping, Scouting, Soil and Field Analysis, Crop Monitoring, Health Assessment, Irrigation, Crop Spraying, Aerial Planting, Precision Agriculture, Livestock Monitoring, Agricultural Photography, Precision Fish Farming, and Others) - Industry Trends and Forecast to 2033

Agriculture Drone Market Size

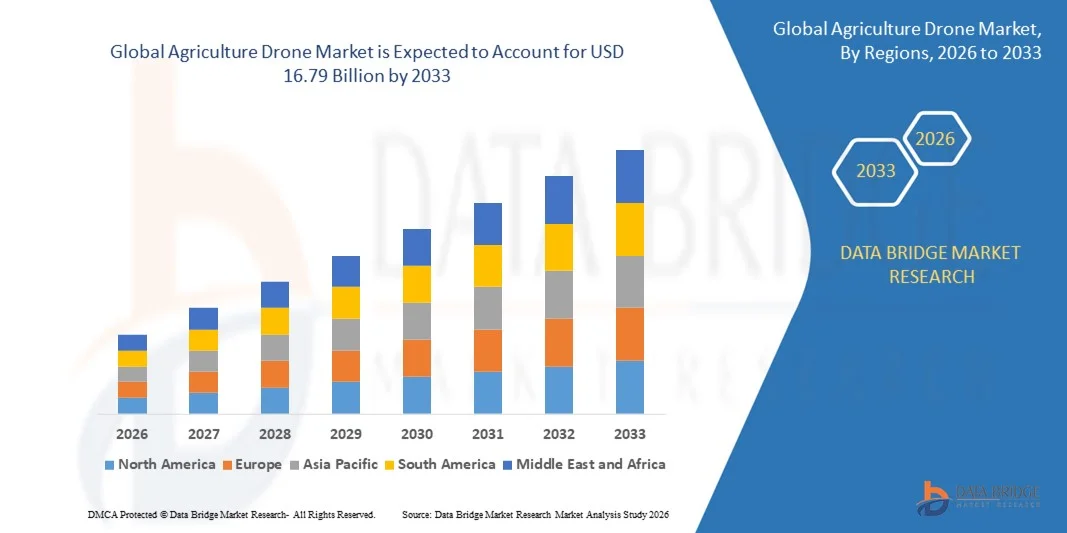

- The global agriculture drone market size was valued at USD 3.88 billion in 2025 and is expected to reach USD 16.79 billion by 2033, at a CAGR of 20.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of precision agriculture practices and the rapid integration of advanced technologies such as AI, GNSS, and data analytics into farming operations, leading to enhanced digitalization across agricultural activities

- Furthermore, rising demand for higher crop yields, efficient pesticide application, and labor cost reduction is establishing agriculture drones as essential tools for modern farm management. These converging factors are accelerating the deployment of drone-based solutions, thereby significantly boosting the overall growth of the agriculture drone market

Agriculture Drone Market Analysis

- Agriculture drones, equipped with advanced imaging sensors, spraying systems, and real-time data transmission capabilities, are becoming critical components of smart farming ecosystems across small, medium, and large-scale agricultural operations due to their ability to improve operational efficiency, monitor crop health, and optimize resource utilization

- The escalating demand for agriculture drones is primarily driven by increasing global food demand, shrinking arable land, rising labor shortages in rural areas, and the growing shift toward data-driven and automated farming practices aimed at improving productivity and sustainability

- North America dominated the agriculture drone market with a share of 34% in 2025, due to the rapid adoption of precision agriculture technologies and strong presence of advanced farming infrastructure

- Asia-Pacific is expected to be the fastest growing region in the agriculture drone market during the forecast period due to rapid urbanization, expanding agricultural activities, and increasing government initiatives supporting digital farming in countries such as China, Japan, and India

- Multi-rotor drones segment dominated the market with a market share of 62.9% in 2025, due to their superior maneuverability, vertical take-off and landing capability, and suitability for small to medium-sized farms. Farmers widely prefer multi-rotor drones for precision spraying, crop monitoring, and field scouting due to their ability to hover steadily over specific areas

Report Scope and Agriculture Drone Market Segmentation

|

Attributes |

Agriculture Drone Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Agriculture Drone Market Trends

Rising Adoption of AI-Enabled Precision Agriculture Drones

- A significant trend in the agriculture drone market is the increasing deployment of AI-enabled drones equipped with multispectral sensors and advanced analytics to enhance crop monitoring and farm decision-making. This integration is strengthening the role of drones as essential tools within precision agriculture systems aimed at maximizing yield and optimizing resource utilization

- For instance, DJI has introduced advanced agricultural drones such as the Agras series integrated with smart flight planning and real-time data analytics to improve spraying accuracy and operational efficiency. These systems enable farmers to automate large-scale spraying tasks while minimizing chemical wastage and improving coverage consistency

- The adoption of AI-powered imaging solutions is expanding as farmers increasingly rely on vegetation indices and predictive analytics to detect crop stress, pest infestations, and nutrient deficiencies at early stages. This is positioning agriculture drones as proactive farm management tools rather than only surveillance equipment

- Large agribusinesses are incorporating drone data into integrated farm management platforms where aerial insights support irrigation planning, soil analysis, and yield forecasting. This growing reliance on data-driven cultivation is reinforcing the transformation of conventional farming into technology-enabled precision agriculture

- Governments across key agricultural economies are promoting digital farming initiatives that encourage drone adoption to address labor shortages and improve productivity. This policy support is contributing to stronger market penetration and structured deployment across commercial farms

- The market is witnessing accelerated innovation in autonomous navigation, obstacle avoidance, and cloud-based analytics that enhance operational reliability and scalability. This rising integration of AI and automation is reinforcing the broader transition toward smart, efficient, and sustainable agricultural ecosystems

Agriculture Drone Market Dynamics

Driver

Increasing Demand for Enhanced Crop Yield and Operational Efficiency

- The increasing global demand for higher agricultural productivity is driving the adoption of drones capable of precise spraying, crop monitoring, and real-time field mapping. These technologies enable farmers to optimize fertilizer and pesticide application while reducing manual labor and operational inefficiencies

- For instance, Yamaha Motor Co., Ltd. has deployed its RMAX unmanned helicopter systems for agricultural spraying across Japan and other countries to enhance large-scale crop management efficiency. These UAV platforms support uniform application and reduce time-intensive manual processes on extensive farmland

- Farmers are increasingly utilizing drones to monitor crop health through high-resolution aerial imagery, enabling early identification of stress factors and reducing potential yield losses. This proactive capability directly contributes to improved harvest outcomes and better resource allocation

- The rising pressure to feed a growing global population while managing limited arable land is encouraging investments in precision agriculture technologies. Drones provide scalable solutions that help maximize productivity without significantly expanding land usage

- The continuous emphasis on productivity enhancement and operational optimization is reinforcing this driver across both developed and emerging agricultural markets. The need for efficient, data-backed, and automated farming practices continues to accelerate agriculture drone market expansion

Restraint/Challenge

High Initial Investment and Regulatory Compliance Barriers

- The agriculture drone market faces challenges related to the high upfront cost associated with advanced drone systems, sensors, and data analytics platforms. Small and medium-scale farmers often encounter financial constraints that limit large-scale adoption despite operational benefits

- For instance, the Federal Aviation Administration imposes strict operational and certification requirements for agricultural drone usage in the U.S., which increases compliance complexity for commercial farm operators. These regulatory procedures can extend deployment timelines and add administrative burdens to drone implementation strategies

- The requirement for licensed pilots, operational training, and adherence to airspace restrictions further increases operational costs and limits accessibility in certain regions. Compliance with evolving aviation regulations remains a critical barrier for new market entrants

- Advanced agriculture drones equipped with AI analytics and multispectral sensors involve higher procurement and maintenance expenses, impacting affordability in price-sensitive markets. This cost factor restricts widespread penetration among smallholder farmers in developing economies

- Inconsistent regulatory frameworks across countries create uncertainty for manufacturers and service providers seeking global expansion. These regulatory and financial challenges collectively restrain faster market adoption despite strong technological advancements and productivity advantages

Agriculture Drone Market Scope

The market is segmented on the basis of type, product, battery life, components, mode of operation, range, technology, and application.

- By Type

On the basis of type, the agriculture drone market is segmented into fixed-wing drones, multi-rotor drones, and hybrid drones. The multi-rotor drones segment dominated the market with the largest revenue share of 62.9% in 2025, driven by their superior maneuverability, vertical take-off and landing capability, and suitability for small to medium-sized farms. Farmers widely prefer multi-rotor drones for precision spraying, crop monitoring, and field scouting due to their ability to hover steadily over specific areas. Their lower operational complexity and comparatively affordable pricing further strengthen adoption among individual farmers and agribusinesses. The segment continues to benefit from ongoing improvements in payload capacity and sensor integration enhancing operational efficiency.

The hybrid drones segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the growing need for longer flight endurance combined with vertical take-off capability. Hybrid models integrate the advantages of fixed-wing endurance and multi-rotor flexibility, making them suitable for large-scale farms requiring extensive field coverage. Increasing investments in advanced agricultural technologies and demand for high-efficiency aerial mapping solutions are accelerating adoption. Their ability to cover vast acreage with reduced energy consumption makes them increasingly attractive for commercial farming operations.

- By Product

On the basis of product, the agriculture drone market is segmented into software and hardware. The hardware segment dominated the market with the largest revenue share in 2025, driven by strong demand for drone platforms, sensors, cameras, propulsion systems, and batteries. Rising adoption of high-resolution imaging systems and advanced spraying mechanisms significantly contributes to hardware sales. Farmers and service providers invest heavily in durable drone structures and precision components to enhance field productivity. Continuous technological advancements in lightweight materials and improved battery systems further support hardware dominance.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by increasing reliance on data analytics, AI-based crop monitoring, and cloud-based farm management platforms. Advanced software solutions enable real-time field mapping, crop health assessment, and yield prediction improving decision-making accuracy. Integration of drone analytics with farm management systems enhances operational transparency and resource optimization. Growing awareness of precision agriculture practices is accelerating demand for subscription-based and data-driven software platforms.

- By Battery Life

On the basis of battery life, the agriculture drone market is segmented into < 30 minutes, 30–60 minutes, 60–100 minutes, and > 100 minutes. The 30–60 minutes segment dominated the market with the largest revenue share in 2025, driven by its balanced combination of operational endurance and cost efficiency. Most commercial agriculture drones are designed within this flight duration range to support spraying and mapping tasks efficiently. The segment meets the requirements of medium-sized farms while maintaining manageable battery weight and charging time. Manufacturers continue to optimize lithium-based battery systems to enhance reliability within this range.

The > 100 minutes segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for large-scale field surveillance and extended mapping operations. Long-endurance drones reduce the need for frequent battery replacements, improving productivity in expansive agricultural lands. Technological progress in high-density battery chemistries and hybrid power solutions supports this segment’s expansion. Commercial agribusinesses are increasingly investing in extended-flight drones to maximize operational efficiency.

- By Components

On the basis of components, the agriculture drone market is segmented into flight controllers, propulsion systems, camera system, batteries, and global positioning system. The camera system segment dominated the market with the largest revenue share in 2025, driven by increasing demand for multispectral and thermal imaging to assess crop health and soil conditions. High-resolution imaging systems enable farmers to detect pest infestations, nutrient deficiencies, and irrigation issues at early stages. Continuous innovation in sensor accuracy and imaging capabilities significantly boosts adoption. The rising importance of data-driven farming practices further strengthens the dominance of camera systems.

The flight controllers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in autonomous navigation and precision flight stabilization technologies. Modern flight controllers integrate AI algorithms and real-time data processing to improve route planning and obstacle avoidance. Growing emphasis on automation in agriculture increases demand for intelligent control systems. Enhanced compatibility with GNSS and analytics platforms further accelerates segment expansion.

- By Mode of Operation

On the basis of mode of operation, the agriculture drone market is segmented into fully-autonomous, semi-autonomous, and remotely operated. The fully-autonomous segment dominated the market with the largest revenue share in 2025, driven by increasing adoption of automated flight planning and minimal human intervention systems. Farmers prefer fully-autonomous drones for consistent spraying patterns and efficient field mapping reducing labor dependency. Integration with AI-powered analytics enhances operational precision and productivity. Expanding digital transformation across agriculture further supports segment leadership.

The semi-autonomous segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by the need for flexible control combined with automation. Semi-autonomous drones allow operators to intervene when necessary while benefiting from automated navigation systems. This operational balance makes them suitable for farms transitioning toward advanced automation. Increasing training programs and user-friendly interfaces are accelerating adoption across developing agricultural economies.

- By Range

On the basis of range, the agriculture drone market is segmented into extended visual line of sight, beyond line of sight, and visual line of sight. The visual line of sight segment dominated the market with the largest revenue share in 2025, driven by regulatory compliance requirements in several countries and ease of operational approval. Most small and medium-scale farmers operate drones within visible range to ensure safety and control. Lower technical complexity and reduced regulatory barriers further strengthen adoption. The segment remains widely preferred for localized crop monitoring and spraying activities.

The beyond line of sight segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by regulatory advancements and increasing demand for large-area coverage. BVLOS operations enable efficient monitoring of expansive agricultural fields reducing operational time. Technological improvements in communication systems and collision avoidance enhance safety and reliability. Growing commercial farming activities are driving investment in long-range drone capabilities.

- By Technology

On the basis of technology, the agriculture drone market is segmented into GNSS, obstacle detection and collision avoidance technology, drone analytics, and others. The GNSS segment dominated the market with the largest revenue share in 2025, driven by its critical role in ensuring accurate positioning and navigation during spraying and mapping operations. Precision agriculture heavily depends on satellite-based guidance systems to optimize input application. Reliable GNSS integration enhances flight stability and field coverage accuracy. Increasing deployment of high-precision GPS modules strengthens segment dominance.

The drone analytics segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for actionable agricultural insights derived from aerial data. Advanced analytics platforms convert raw drone imagery into crop health indices and yield forecasts supporting strategic farm management. Integration with AI and machine learning technologies enhances predictive capabilities. Expanding adoption of data-centric farming models accelerates growth within this segment.

- By Application

On the basis of application, the agriculture drone market is segmented into spraying, field mapping, scouting, soil and field analysis, crop monitoring, health assessment, irrigation, crop spraying, aerial planting, precision agriculture, livestock monitoring, agricultural photography, precision fish farming, and others. The crop spraying segment dominated the market with the largest revenue share in 2025, driven by the growing need for efficient pesticide and fertilizer application with minimal wastage. Drones enable uniform chemical distribution reducing labor costs and environmental impact. Increasing focus on precision input management significantly boosts adoption in this segment. Continuous improvements in payload systems further enhance operational effectiveness.

The precision agriculture segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing global emphasis on sustainable farming and resource optimization. Precision agriculture integrates drone-based analytics, GNSS mapping, and automated decision-making to maximize yield and minimize input costs. Rising government support for smart farming technologies strengthens market expansion. Growing awareness among farmers regarding data-driven crop management continues to accelerate adoption across developed and emerging economies.

Agriculture Drone Market Regional Analysis

- North America dominated the agriculture drone market with the largest revenue share of 34% in 2025, driven by the rapid adoption of precision agriculture technologies and strong presence of advanced farming infrastructure

- Farmers in the region highly value drone-based crop monitoring, field mapping, and spraying solutions to improve yield efficiency and reduce operational costs

- This widespread adoption is further supported by favorable regulatory frameworks, high awareness regarding smart farming practices, and strong investment in agri-tech innovation, establishing agriculture drones as a critical component of modern farm management

U.S. Agriculture Drone Market Insight

The U.S. agriculture drone market captured the largest revenue share in 2025 within North America, fueled by early adoption of precision farming tools and increasing farm consolidation across large agricultural lands. Farmers are increasingly prioritizing data-driven crop management and automated spraying systems to enhance productivity and optimize input usage. Strong government support for smart agriculture initiatives, combined with the presence of leading drone manufacturers such as DJI and AeroVironment operating in the market, further accelerates industry expansion.

Europe Agriculture Drone Market Insight

The Europe agriculture drone market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing emphasis on sustainable farming and strict environmental regulations regarding pesticide usage. Rising demand for precision agriculture tools to enhance crop yield while minimizing environmental impact is fostering drone adoption. The region is witnessing steady growth across countries investing in digital agriculture transformation and advanced farm monitoring technologies.

U.K. Agriculture Drone Market Insight

The U.K. agriculture drone market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing digitalization of farming operations and demand for efficient crop surveillance systems. Farmers are adopting drone-based analytics to improve soil assessment and crop health monitoring. Supportive agricultural policies and rising interest in autonomous farm equipment are expected to continue stimulating market growth in the country.

Germany Agriculture Drone Market Insight

The Germany agriculture drone market is expected to expand at a considerable CAGR during the forecast period, fueled by strong focus on technological innovation and sustainable agricultural practices. Germany’s advanced manufacturing capabilities and emphasis on precision engineering promote the integration of drones in crop monitoring and livestock management. Increasing investment in smart farming solutions and digital infrastructure further strengthens market development.

Asia-Pacific Agriculture Drone Market Insight

The Asia-Pacific agriculture drone market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, expanding agricultural activities, and increasing government initiatives supporting digital farming in countries such as China, Japan, and India. Rising food demand and labor shortages are encouraging farmers to adopt automated aerial solutions for efficient farm management. In addition, the region’s growing role as a manufacturing hub for drone components is improving affordability and accessibility across emerging economies.

Japan Agriculture Drone Market Insight

The Japan agriculture drone market is gaining momentum due to labor shortages in rural areas and strong adoption of advanced robotics and automation technologies. Japanese farmers are increasingly deploying drones for crop spraying and precision monitoring to enhance productivity and reduce manual effort. Integration of drone systems with smart agriculture platforms and IoT-based farm management tools is further contributing to market growth.

China Agriculture Drone Market Insight

The China agriculture drone market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid modernization of agricultural practices and strong domestic manufacturing capabilities. The country has witnessed widespread deployment of crop spraying drones across large-scale farms to improve efficiency and reduce chemical wastage. Presence of major drone manufacturers such as DJI and supportive government policies promoting agricultural mechanization are key factors propelling market expansion in China.

Agriculture Drone Market Share

The agriculture drone industry is primarily led by well-established companies, including:

- AeroVironment Inc. (U.S.)

- AGCO Corporation (U.S.)

- AgEagle Aerial Systems Inc. (U.S.)

- Delair (France)

- DroneDeploy (U.S.)

- Trimble Inc. (U.S.)

- Parrot Drone SAS (France)

- Yamaha Motor Co., Ltd. (Japan)

- OPTiM Corp. (Japan)

- Sentera (U.S.)

- Insitu Pacific Pty Ltd (Australia)

- ALTI UAS (PTY) LTD (South Africa)

- senseFly (Switzerland)

- AgEagle Sensor Systems Inc. (U.S.)

- Pix4D SA (Switzerland)

- DJI (China)

Latest Developments in Global Agriculture Drone Market

- In December 2025, Jyoti Global Plast introduced the AeroCrop UAS agricultural drone to enhance precision, operational safety, and spraying efficiency for farmers across India. This launch marks the company’s strategic expansion from plastic and FRP moulding into the unmanned aerial systems segment, strengthening domestic manufacturing capabilities. The development is expected to accelerate the adoption of precision agriculture technologies in India by addressing labor shortages, reducing chemical wastage, and improving crop productivity, thereby contributing to overall agriculture drone market growth

- In December 2025, Connecticut, United States, enacted Public Act 25-152 permitting the expanded use of agricultural drones for seeding, spraying, and crop surveying activities. The updated regulatory framework streamlines compliance requirements in alignment with Federal Aviation Administration standards, enabling farms to integrate UAV technologies more efficiently. This legislative support is anticipated to enhance commercial drone deployment across the state, encouraging investment and innovation within the regional agriculture drone market

- In August 2025, Terra Drone Corporation entered into a sales partnership with PT. Yanmar Diesel Indonesia, a subsidiary of Yanmar Co., Ltd., to distribute its G20 and E16 agricultural drones to rice and field crop farmers in Indonesia. This collaboration strengthens Terra Drone’s footprint in Southeast Asia by leveraging Yanmar’s established agricultural distribution network. The partnership is expected to expand drone accessibility among local farmers, driving regional adoption and reinforcing market penetration in emerging agricultural economies

- In April 2024, DJI announced the global launch of the Agras T50 and T25 agricultural drones, targeting both large-scale and small-field farming operations. The T50 offers high-efficiency performance for extensive farmland coverage, while the T25 emphasizes portability and operational flexibility. Integration with the SmartFarm application enhances aerial spraying management and data-driven decision-making, strengthening DJI’s competitive position and advancing technological standards within the global agriculture drone market

- In July 2023, Pix4D SA launched PIX4Dfields 2.4 featuring an upgraded workflow designed to streamline precision agriculture applications. The introduction of Targeted Operations enables users to generate customized prescription maps more efficiently, improving resource optimization and crop management accuracy. This innovation enhances software-driven value within drone ecosystems, supporting broader adoption of data-centric farming solutions and reinforcing growth in the agriculture drone analytics segment

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.