Global Tank Insulation Market

Marktgröße in Milliarden USD

CAGR :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

Global Tank Insulation Market Segmentation, nach Typ (Speichern und Transportieren), Materialtyp (Expanded Polystyrene (EPS), Rockwool, Cellular Glass, Fiberglass, Elastomer Foam, Polyurethane (PU) und andere), Temperaturtyp (Hot Insulation und Kalte Insulation), Tanktyp (Vertical Tank, Horizontal Tank, Feste Tank, und gereinigte Tank-Ende)

Tank Insulation Market Size

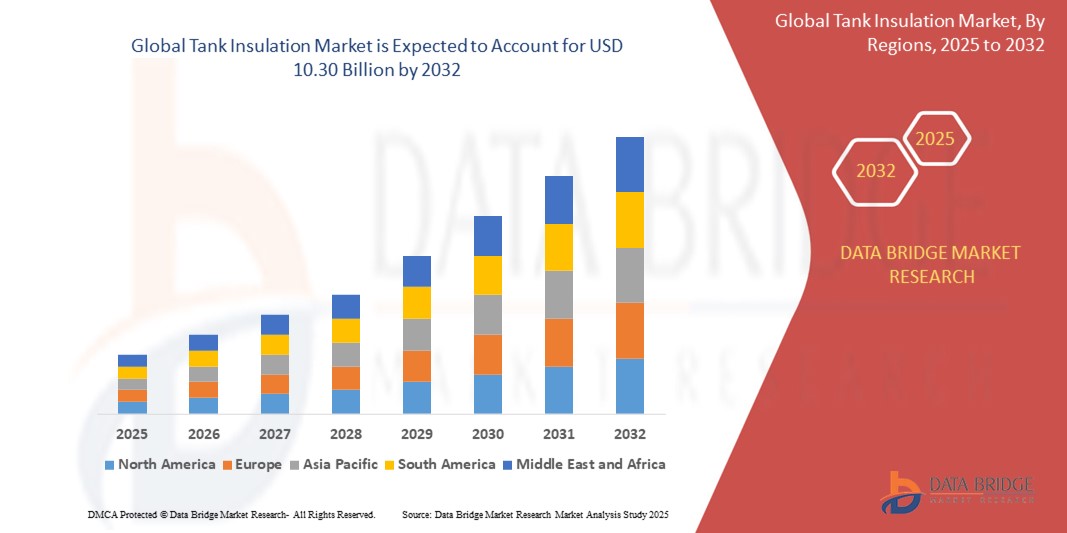

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Inhaltsverzeichnis

INHALTSVERZEICHNIS

1 EINLEITUNG

1.1 ZIELE DES STUDY 1.2 MARKT-VERFAHRENS 1.3 ÜBERPRÜFUNG DER GLOBAL-TANK-INSULATIONSMARKT 1.4 URRENCY UND PRICING 1.5 LIMITATIONEN

2 MARKET SEGMENTATION

2.1 BERUFSBILDUNG 2.2 GEOGRAPHISCHES ANWENDUNGSBEREICH 2.3 JAHRE FÜR DIE STUDIE 2.4 AUSBILDUNG UND PREISUNG 2.5 DBMR-TRIPOD-DATEN VALIDIERUNG MODEL 2.6 TECHNOLOGIE LEBENSMITTELLINIE 2.7 MULTIVARIAT MODELLUNG 2.8 PRIMÄREBEN

3 MARKET ÜBERBLICK

3.1 VERFAHREN

3.1.1 INKREISUNG DER INDUSTRIE INDUSTRIE 3.1.2 ENTWICKLUNG DER ENTWICKLUNG DER ENTWICKLUNG IN LNG STORAGE UND TRANSPORTATION 3.1.3 ENTWICKLUNG DER TEMPERATUR KONTROLLE FÜR PHARMAZEUTISCHE BESCHÄFTIGUNGEN

3.2 AUSBILDUNGEN

3.2.1 FINANZIERUNG DER MATERIALPREISE 3.2.2 VERÄNDERUNG DER CHEMISCHEN STRUKTUR DURCH DIENSTLEISTUNG DURCH DIE NACHRICHTUNG VON MATERIAL 3.2.3 UNAVAILABILITÄT VON PROFICIENT INSULATING MATERIAL FÜR IRON- UND STAHLINDUSTRIE ZU BETRIEBEN MOLTEN METALIEN IN ZUM

3.3 STELLUNGNAHMEN

3.3.1 HIGDEMAND FÜR DIE ZWISCHEN ZWISCHEN ZWISCHEN ZWISCHEN INDUSTRIE IN CHINA UND INDIEN 3.3.2 WEITERBILDUNG DER ZWECKUNGSMATERIALEN IN WASSERZEN FÜR MULTI-STOREN RESIDENTIAL UND COMMERCIAL BUILDINGS 3.3.3 INKREISIERUNG DER INDUSTRIE

3.4 HANDELN

3.4.1 FIRE UND EXPLOSION DACH CHEMISCHEN REAKTION MIT INSULATIERTEN MATERIAL IN TANK 3.4.2 GESUNDHEITSZAHL DER INSULATING MEDIEN

4 ZUSAMMENFASSUNG 5 VORSCHRIFTEN 6 INDUSTRIERECHTE 7 GLOBAL TANK INSULATION MARKET, NACH TYPE

7.1 ÜBERBLICK 7.2 STORAGE 7.3 VERKEHR

8 GLOBAL TANK INSULATION MARKT, NACH MATERIAL TYPE

8.1 ÜBERBLICK 8.2 AUSGEWÄHLTE POLYSTYRENE (EPS) 8.3 ROCKWOOL 8.4 CELLULAR GLASS 8.5 FIBERGLASS 8.6 ELASTOMERIC FOAM 8.7 POLYURETHANE (PU) 8.8 ANDERE

9 GLOBAL TANK INSULATION MARKET, NACH TEMPERATUR

9.1 ÜBERBLICK 9.2 GESCHÄFTSBEDINGUNGEN 9.3 BETEILIGUNG

10 GLOBAL TANK INSULATION MARKET, BY TANK TYPE

10.1 ÜBERBLICK 10.2 VERTISCHE TANK 10.3 HORIZONTAL TANK 10.4 FIXED TANK 10.5 Geänderte TANK

11 GLOBAL TANK INSULATION MARKET, BY TANK ENDS

11.1 ÜBERBLICK 11.2 PARABOLIC DISH 11.3 FLAT

12 GLOBAL TANK INSULATION MARKET, BY END-USER

12.1 ÜBERBLICK 12.2 OIL UND GAS

12.2.1 OIL

12.2.1.1 CRUDE OIL 12.2.1.2 PETROCHEMISCHER 12.2.1.3 ANDERE RUDE OIL DERIVATIVEN

1.2.2 GAS

12.2.2.1 NATURAL GAS 12.2.2.2 SYNTHETIK GAS

12.3 ENERGIE UND POWER 12.4 CHEMISCHER 12.5 LEBENSMITTEL UND GEBIETE

12.5.1 LEBENSMITTEL 12.5.2 BEVERAGE

12.5.2.1 ALCOHOLIC BEVERAGE 12.5.2.2 DAIRY 12.5.2.3 AERATED DRINKS 12.5.2.4 JUICES UND FLAVORED WASSER 12.5.2.5 ANDERE

12.6 WASSERSTELLUNG

12.6.1 COMMERCIAL BUILDINGs 12.6.2 MUNIKIPALITÄT 12.6.3 ERGEBNISSE

12.7 WASSERBILDUNG

12.7.1 COMMERCIAL BUILDINGs 12.7.2 MUNIKIPALITY 12.7.3 RESIDENTIAL BUILDINGS

12.8 SONSTIGE

13 GLOBAL TANK INSULATION MARKET, NACH GEOGRAPHIE

13.1 ÜBERBLICK 13.2 NORTH AMERICA

13.2.1 U.S. 13.2.2 CANADA 13.2.3 MEXICO

13.3 EUROPA

13.3.1 DEUTSCHLAND 13.3.2 U.K 13.3.3 ITALIEN 13.3.4 FRANKREICH 13.3.5 SPANIEN 13.3.6 SCHWEIZ 13.3.7 RUSSIEN 13.3.8 TURKEY 13.3.9 BELGIEN 13.3.10 NIEDERLANDE 13.3.11 REST EUROPA

13.4 ASIEN-PAKIFIK

13.4.1 CHINA 13.4.2 INDIEN 13.4.3 SOUTH KOREA 13.4.4 JAPAN 13.4.5 AUSTRALIEN 13.4.6 SINGAPORE 13.4.7 THAILAND 13.4.8 INDONESIEN 13.4.9 MALAYSIEN 13.4.10 PHILIPPINE 13.4.11 REST DER ASIEN-PAKIFIK

13.5 AMERIKA

13.5.1 BRAZIL 13.5.2 ARGENTINA 13.5.3 REST OF SOUTH AMERICA

13.6 MIDDLE EAST UND AFRIKA

13.6.1 VAE 13.6.2 SAUDI ARABIA 13.6.3 ISRAEL 13.6.4 SOUTH AFRICA 13.6.5 EGYPT 13.6.6 REST VON MIDDLE EAST UND AFRICA

14 GLOBAL TANK INSULATION MARKET, COMPANY LANDSCAPE

14.1 GESELLSCHAFTSANALYSE: GLOBAL 14.2 GESELLSCHAFTSANALYSE: NORTH AMERICA 14.3 GESELLSCHAFTSANALYSE: EUROPA 14.4 GESELLSCHAFTSANALYSE: ASIEN- PAKIFIK 14,5 MERGER UND QUISITIONEN 14.6 NEUE PRODUKTE ENTWICKLUNG & GENEHMIGKEITEN 14.7 AUSGABEN

15 WETTBEWERBSVERFAHREN

15.1 BASF SE

15.1.1 WETTBEWERBSPOLITIK 15.1.1 WETTBEWERBSPOLITIK 15.1.4 WETTBEWERBSPOLITIK 15.1.5 GEOGRAPHISCHE PRESSE 15.1.6 PRODUKTPORTFOLIO 15.1.7 RECENT DEVELOPMENTS 15.1.8 DATEN BRIDGE MARKET FORSCHUNGSANALYSE

15.2 WIEDER CHEMISCHE GEMEINSCHAFT

15.2.1 WETTBEWERBSPOLITIK 15.2.4 WETTBEWERBSPOLITIK 15.2.5 GEOGRAPHISCHER PRESSE 15.2.6 PRODUKTPORTFOLIO 15.2.7 RECENT DEVELOPMENTS 15.2.8 DATEN BRIDGE MARKET FORSCHUNGSANALYSE

15.3 SAINT-GOBAIN

15.3.1 WETTBEWERBSPOLITIK 15.3.2 GEOGRAPHISCHE ERZEUGNISSE 15.3.6 PORTFOLIO 15.3.7 RECENT DEVELOPMENTE 15.3.8 DATEN BRIDGE MARKET FORSCHUNG ANALYSE

15.4 HUNTSMAN INTERNATIONAL LLC

15.4.1 WETTBEWERBSREGELN 15.4.2 SCHLUSSANTRÄGE 15.4.3 REVENUE ANALYSE 15.4.4 WETTBEWERBSANALYSE 15.4.5 GEOGRAPHISCHE PRESSE 15.4.6 PRODUKTPORTFOLIO 15.4.7 RECENT DEVELOPMENTE 15.4.8 DATEN BRIDGE MARKET FORSCHUNGSANALYSE

15.5 KINGSPAN GROUP

15.5.1 WETTBEWERBSPOLITIK 15.5.2 GEOGRAPHISCHE ERZEUGNISSE 15.5.4 WETTBEWERBSANIEN 15.5.5 GEOGRAPHISCHE PRESSE 15.5.6 WAREN PORTFOLIO 15.5.7 RECENT DEVELOPMENTE 15.5.8 DATEN BRIDGE MARKT FORSCHUNGSANALYSE

15.6 ARMACELL LLC

15.6.1 GESUNDHEITSSCHUTZ 15.6.2 ANALYSE 15.6.3 GEOGRAPHISCHE ERZEUGNISSE 15.6.4 PORTFOLIO 15.6.5 RECENT ENTWICKLUNGEN

15.7 CABOT CORPOR

15.7.1 WETTBEWERBSPOLITIK 15.7.2 REVENUE ANALYSE 15.7.3 GEOGRAPHISCHE ERGEBNIS 15.7.4 PRODUKTPORTFOLIO 15.7.5 RECENT DEVELOPMENTE

15.8 COMMERCIAL THERMAL SOLUTIONEN, INC.

15.8.1 WETTBEWERBSPOLITIK 15.8.2 WETTBEWERBSPOLITIK 15.8.3 RECENTENTWICKLUNG

15.9 TECHNOLOGIEN, INC.

15.9.1 WETTBEWERBSPOLITIK 15.9.2 WETTBEWERBSPOLITIK 15.9.3 RECENTENTWICKLUNG

15.10 DUNMORE

15.10.1 GESUNDHEITSSCHUTZ 15.10.2 GEOGRAPHISCHE ERGEBNISSE 15.10.3 PRODUKTPORTFOLIO 15.10.4 RECENT DEVELOPMENTE

15.11 GILSULATE INTERNATIONAL, INC.

15.11.1 WETTBEWERBSREGELN 15.11.2 PRODUKTE PORTFOLIO 15.11.3 RECENT DEVELOPMENTE

15.12 GULF COOL THERM FACTORY LTD

15.12.1 WETTBEWERBSREGELN 15.12.2 PRODUKTE PORTFOLIO 15.12.3 ENTWICKLUNG

15.13 ITW INSULATIONSSYSTEME

15.13.1 WETTBEWERBSPOLITIK

15.14 JOHNS MANVILLE

15.14.1 WETTBEWERBSPOLITIK

15.15 J.H. ZIEGLER GMBH

15.15.1 WETTBEWERBSPOLITIK 15.15.2 GEOGRAPHISCHE ERGEBNIS 15.15.3 PRODUKTPORTFOLIO 15.15.4 RECENT DEVELOPMENT

15.16 KNAUF INSULATION

15.16.1 GESUNDHEITSSCHUTZ

15.17 MAYES COATINGS & INSULATION, INC.

15.17.1 WETTBEWERBSPOLITIK 15.17.2 PRODUKTE PORTFOLIO 15.17.3 ENTWICKLUNGEN

15.18 OWENS

15.18.1 GESUNDHEITSSCHUTZ 15.18.2 REVENUE ANALYSE 15.18.3 GEOGRAPHISCHE ERGEBNIS 15.18.4 PORTFOLIO 15.18.5 RECENT DEVELOPMENTE

15.19 POLARCLAD TANK INSULATION

15.19.1 GESUNDHEITSSCHUTZ 15.19.2 PRODUKTPORTFOLIO 15.19.3 ENTWICKLUNG

15.20 RÖCHLING GROUP

15.20.1 COMPANY SNAPSHOT 15.20.2 GEOGRAPHISCHE ERGEBNISSE 15.20.3 PORTFOLIO 15.20.4 RECENTENTWICKLUNGEN

15.21 ROCKWOOL INTERNATIONALES A/S

15.21.1 WETTBEWERBSPOLITIK 15.21.2 ENTWICKLUNG DER ANALYSE 15.21.3 GEOGRAPHISCHE ERGEBNISSE 15.21.4 PORTFOLIO 15.21.5 ENTWICKLUNGEN

15.22 SPX TRANSFORMER LÖSUNGEN INC.

15.22.1 WETTBEWERBSPOLITIK 15.22.2 PRODUKTPORTFOLIO 15.22.3 RECENT DEVELOPMENTE

15.23 SYNAVAX

15.23.1 WETTBEWERBSPOLITIK 15.23.3 ENTWICKLUNGEN

15.24 THERMACON

15.24.1 GESUNDHEITSSCHUTZ 15.24.2 PRODUKTPORTFOLIO 15.24.3 ZUR ENTWICKLUNG

15.25 T.F.WARREN GROUP

15.25.1 WETTBEWERBSPOLITIK 15.25.2 GEOGRAPHISCHE ERGEBNIS 15.25.3 PRODUKTE PORTFOLIO 15.25.4 RECENT DEVELOPMENTE

16 QUESTIONNAIRE 17 SCHLUSSFOLGERUNG 18 BERICHTE

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.