North America Anesthesia And Respiratory Devices Market

Marktgröße in Milliarden USD

CAGR :

%

USD

18.11 Billion

USD

32.90 Billion

2025

2033

USD

18.11 Billion

USD

32.90 Billion

2025

2033

| 2026 –2033 | |

| USD 18.11 Billion | |

| USD 32.90 Billion | |

| % | |

|

North America Anesthesia and Respiratory Devices Market Segmentation, By Product (Anesthesia Devices and Respiratory Devices), End User (Hospitals, Clinics, Homecare, and Ambulatory Service Centers) - Industry Trends and Forecast to 2033

North America Anesthesia and Respiratory Devices Market Size

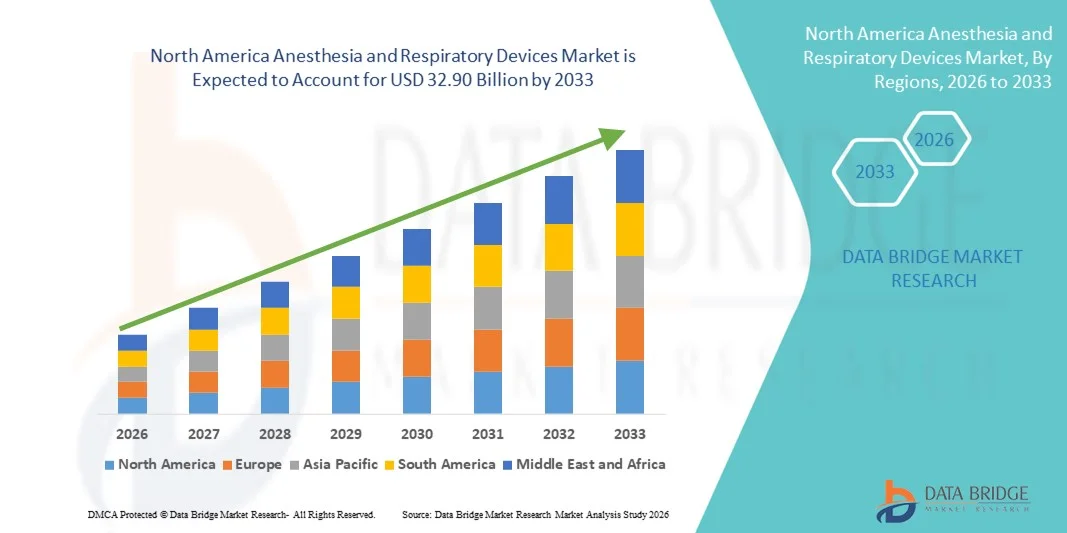

- The North America Anesthesia and Respiratory Devices market size was valued at USD 18.11 billion in 2025 and is expected to reach USD 32.90 billion by 2033, at a CAGR of 7.75% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced healthcare technologies, increasing demand for minimally invasive procedures, and continuous technological advancements in anesthesia and respiratory care devices across hospitals, clinics, and ambulatory care centers

- Furthermore, rising patient awareness, growing prevalence of respiratory disorders, and increasing surgical volumes are driving the adoption of innovative anesthesia and respiratory devices. These converging factors are accelerating the uptake of Anesthesia and Respiratory Devices solutions, thereby significantly boosting the industry's growth

North America Anesthesia and Respiratory Devices Market Analysis

- Anesthesia and respiratory devices, including advanced ventilators, anesthesia delivery systems, and monitoring equipment, are increasingly vital components of modern healthcare facilities in both hospitals and ambulatory care centers due to their critical role in patient safety, procedural efficiency, and clinical outcomes

- The escalating demand for anesthesia and respiratory devices is primarily fueled by rising surgical volumes, growing prevalence of respiratory disorders, increasing adoption of minimally invasive procedures, and continuous technological advancements in smart monitoring and ventilation systems

- U.S. dominated the Anesthesia and Respiratory Devices market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative surgical and respiratory technologies, and a strong presence of key industry players. The U.S. experienced substantial growth in anesthesia and respiratory device installations across hospitals, surgical centers, and intensive care units, driven by innovations from both established medical device companies and emerging startups focusing on AI-enabled monitoring and smart ventilation solutions

- Canada is expected to be the fastest-growing country in the Anesthesia and Respiratory Devices market during the forecast period, expanding at a CAGR of 9.1% from 2026 to 2033, supported by rising surgical volumes, increasing investments in hospital modernization, growing awareness of advanced respiratory care, and government initiatives promoting adoption of innovative medical devices

- The anesthesia devices segment dominated the largest market revenue share of 46.1% in 2025, driven by rising surgical procedures globally and increasing hospital investments in advanced anesthesia delivery systems

Report Scope and Anesthesia and Respiratory Devices Market Segmentation

|

Attributes |

Anesthesia and Respiratory Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Anesthesia and Respiratory Devices Market Trends

Adoption of Advanced Devices and Integrated Monitoring

- A significant and accelerating trend in the North America Anesthesia and Respiratory Devices market is the growing adoption of advanced anesthesia delivery systems and integrated patient monitoring solutions, which improve safety, precision, and workflow efficiency in operating rooms

- For instance, GE Healthcare’s Aisys CS² anesthesia machine is widely implemented in hospitals to provide automated ventilation and integrated monitoring, while Dräger’s Perseus A500 workstation supports advanced gas delivery and patient data management during surgery

- Hospitals and surgical centers are increasingly adopting portable and home-based respiratory devices, such as non-invasive ventilators and oxygen concentrators, to address the growing prevalence of chronic respiratory diseases like COPD and sleep apnea

- Integration with digital patient records and smart operating room infrastructure allows clinicians to monitor vital signs and anesthesia delivery in real time, enhancing clinical decision-making and patient outcomes

North America Anesthesia and Respiratory Devices Market Dynamics

Driver

Rising Surgical Procedures and Respiratory Care Needs

- The market is primarily driven by an increasing number of surgical procedures, rising chronic respiratory

- surgeries and ICU treatments is also driving adoption, as anesthesia and respiratory devices are disorders, and an aging population requiring advanced perioperative care

- Healthcare facilities are investing in high-performance devices to improve patient outcomes.

- For instance, the Philips Respironics Trilogy Evo ventilator is used extensively in home-based respiratory therapy, and the Mindray WATO EX-65 Pro anesthesia workstation is adopted in hospitals for enhanced patient safety and efficiency

- Supportive government healthcare initiatives and favorable reimbursement policies for critical care and respiratory therapy devices further encourage market growth

- The rising demand for minimally invasive essential for patient monitoring and ventilation management

Restraint/Challenge

High Costs and Regulatory Hurdles

- The high initial cost of advanced anesthesia and respiratory devices can limit adoption in smaller hospitals, clinics, or resource-limited healthcare facilities

- Regulatory compliance and certification requirements often delay market entry

- For instance, FDA approval for new anesthesia machines like Dräger Perseus A500 or GE Aisys CS² involves rigorous testing and clinical validation, impacting the speed at which hospitals can adopt these devices

- Specialized training requirements for clinicians to operate complex anesthesia and ventilation systems may also restrict rapid adoption in some facilities

- Maintenance, service requirements, and integration with existing hospital IT infrastructure add to operational costs, creating further barriers for smaller healthcare providers

- Limited access to advanced devices in rural or underfunded hospitals can impact uniform healthcare delivery across North America

North America Anesthesia and Respiratory Devices Market Scope

The market is segmented on the basis of product and end-user.

- By Product

On the basis of product, the Anesthesia and Respiratory Devices market is segmented into anesthesia devices and respiratory devices. The anesthesia devices segment dominated the largest market revenue share of 46.1% in 2025, driven by rising surgical procedures globally and increasing hospital investments in advanced anesthesia delivery systems. Adoption of multi-functional anesthesia workstations that integrate monitoring and ventilation functionalities contributes to segment dominance. Growing awareness regarding patient safety and perioperative care supports demand. Technological advancements in automated and closed-circuit anesthesia systems enhance precision and efficiency. Expanding geriatric and comorbid patient populations further drive utilization. High prevalence of chronic conditions requiring surgery increases procedure volumes. Favorable reimbursement frameworks in developed regions bolster segment growth. Continuous product innovations, including compact and portable anesthesia systems, strengthen market penetration. Training initiatives for anesthesiologists and nurses enhance adoption. Rising collaborations between manufacturers and healthcare providers promote wider reach. Increasing outpatient and ambulatory surgical procedures further support revenue growth. Strong regulatory approvals and certifications ensure safety compliance, reinforcing trust in the segment.

The respiratory devices segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, fueled by growing prevalence of chronic respiratory diseases such as COPD and asthma. Rising demand for non-invasive ventilation, portable oxygen therapy, and advanced ventilators accelerates market expansion. Technological improvements, including smart ventilators with IoT connectivity and AI-enabled monitoring, enhance patient care. Expanding adoption in home healthcare and ambulatory settings supports rapid growth. Government initiatives for respiratory disease management and increasing awareness about home-based respiratory care boost demand. Increasing pediatric and geriatric patient populations further contribute to adoption. Rising prevalence of respiratory infections and pandemics reinforces market need. Availability of compact, cost-effective, and user-friendly devices promotes accessibility. Integration with telemedicine platforms enables remote monitoring and care, supporting segment growth. Expanding healthcare infrastructure in emerging markets drives wider distribution. Continuous innovation in respiratory therapeutics strengthens adoption. Favorable insurance coverage and reimbursement policies further accelerate the CAGR in this segment.

- By End-User

On the basis of end-user, the Anesthesia and Respiratory Devices market is segmented into hospitals, clinics, homecare, and ambulatory service centers. The hospitals segment accounted for the largest market revenue share of 49.5% in 2025, driven by higher surgical procedure volumes, availability of advanced critical care units, and established anesthesia and ventilator infrastructure. Hospitals remain primary centers for perioperative and intensive respiratory care. Increasing investments in hospital modernization and expansion of critical care services further reinforce segment dominance. Growing number of inpatient procedures and emergency care interventions contributes to higher device utilization. Favorable reimbursement frameworks and government support strengthen adoption. Collaborations with device manufacturers for training and maintenance programs enhance operational efficiency. Rising prevalence of chronic diseases requiring surgical intervention or respiratory support fuels sustained growth. Availability of skilled healthcare professionals ensures optimal usage. Expansion of multi-specialty and tertiary care hospitals supports further market penetration. Continuous clinical validation of devices improves reliability and trust. High procedure safety standards and regulatory compliance drive hospital preference for advanced devices.

The homecare segment is expected to witness the fastest CAGR of 13.6% from 2026 to 2033, driven by increasing patient preference for at-home anesthesia support in palliative care and respiratory therapy. Rising prevalence of chronic respiratory conditions requiring continuous monitoring and therapy fuels adoption. Portable ventilators and home-use anesthesia monitoring systems enhance convenience and compliance. Integration with telehealth solutions allows remote monitoring by clinicians, improving patient safety. Awareness campaigns on early intervention and homecare benefits accelerate uptake. Technological advancements in compact, battery-operated, and user-friendly devices support growth. Expanding elderly population and preference for reduced hospital visits further drive demand. Favorable reimbursement and insurance policies enhance affordability. Homecare adoption reduces healthcare system burden and lowers treatment costs. Continuous innovation in device ergonomics improves usability for caregivers. Availability of dedicated support services ensures proper device operation. Increasing partnerships between manufacturers and homecare providers strengthen market expansion.

North America Anesthesia and Respiratory Devices Market Regional Analysis

- North America dominated the anesthesia and respiratory devices market with the largest revenue share in 2025, driven by advanced healthcare infrastructure, increasing surgical procedures, and the rising prevalence of chronic respiratory diseases

- Hospitals and surgical centers are increasingly adopting innovative anesthesia machines, ventilators, and monitoring systems to enhance patient safety and improve operational efficiency

- High disposable incomes, technologically advanced healthcare facilities, and a well-trained workforce have further contributed to widespread adoption. Moreover, the growing demand for home-based respiratory therapies and portable anesthesia solutions has encouraged both public and private healthcare institutions to invest in modern medical equipment

U.S. Anesthesia and Respiratory Devices Market Insight

The U.S. anesthesia and respiratory devices market held the largest revenue share of 39.8% in 2025, characterized by robust healthcare infrastructure, high adoption of innovative surgical and respiratory technologies, and the strong presence of key medical device manufacturers. The country experienced substantial growth in anesthesia and respiratory device installations across hospitals, surgical centers, and intensive care units, fueled by innovations from established medical device companies as well as emerging startups focusing on advanced monitoring and ventilation solutions. The high prevalence of chronic respiratory conditions, such as COPD and sleep apnea, is driving the adoption of portable ventilators and home-use respiratory devices, supporting better patient care and reducing hospitalization rates.

Canada Anesthesia and Respiratory Devices Market Outlook

Canada anesthesia and respiratory devices market is expected to be the fastest-growing country in this market, expanding at a CAGR of 9.1% from 2026 to 2033. This growth is supported by rising surgical volumes, increasing investments in hospital modernization, growing awareness of advanced respiratory care, and government initiatives promoting innovative medical devices. Furthermore, favorable healthcare policies and supportive reimbursement frameworks are encouraging hospitals and clinics to adopt state-of-the-art anesthesia and respiratory equipment, improving patient safety and clinical efficiency.

North America Anesthesia and Respiratory Devices Market Share

The Anesthesia and Respiratory Devices industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- GE Healthcare (U.S.)

- Philips Healthcare (Netherlands)

- Drägerwerk (Germany)

- Smiths Medical (U.K.)

- Becton Dickinson (U.S.)

- Fresenius Kabi (Germany)

- CareFusion (U.S.)

- Vyaire Medical (U.S.)

- Hill-Rom Holdings (U.S.)

- Harvard Apparatus (U.S.)

- ResMed (U.S.)

- Nihon Kohden (Japan)

- Invacare Corporation (U.S.)

- Masimo Corporation (U.S.)

- Covidien (U.S.)

- Aramed (Germany)

- Tyco Healthcare (U.S.)

- Sutures & Medical Devices Co. (China)

- Allied Healthcare Products (U.S.)

Latest Developments in North America Anesthesia and Respiratory Devices Market

- In September 2023, Drägerwerk AG & Co. KGaA received regulatory approval and launched the Atlan® anesthesia workstation family, a next‑generation anesthesia delivery platform equipped with precision ventilation systems and extensive safety features. Designed for use from neonates to adults, it offers tailored configurations, advanced hygiene routines, and integration with clinical analytics tools to improve operating room efficiency and patient care quality

- In August 2023, Mindray Medical International introduced upgrades to its A Series anesthesia systems (including enhanced A7 and A5 models), focusing on improved patient safety, precise anesthetic delivery, smart alarm systems, and performance analytics — reflecting the industry’s trend toward smarter, data‑enabled perioperative care

- In April 2025, Fisher & Paykel Healthcare Corporation Limited launched two new nasal high‑flow interface devices — the Optiflow Switch and Optiflow Trace — developed specifically for anesthesia and respiratory applications to deliver high‑flow oxygen therapy with enhanced patient comfort and optimized work of breathing during perioperative and ICU care

- In April 2025, Dräger announced the India launch of the Atlan® A100 anesthesia workstation, an innovative platform engineered to improve perioperative care by combining advanced lung protective ventilation modes, low‑flow anesthesia delivery and infection prevention features, helping clinicians manage diverse surgical cases more effectively

- In January 2025, GE HealthCare Korea launched the Carestation 600 series V2 anesthesia system, a compact gas anesthesia machine designed for narrow operating rooms with integrated real‑time driving pressure calculations to help prevent excessive ventilation pressures and support safer ventilation during surgery

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.