Europe Automated Liquid Handling Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

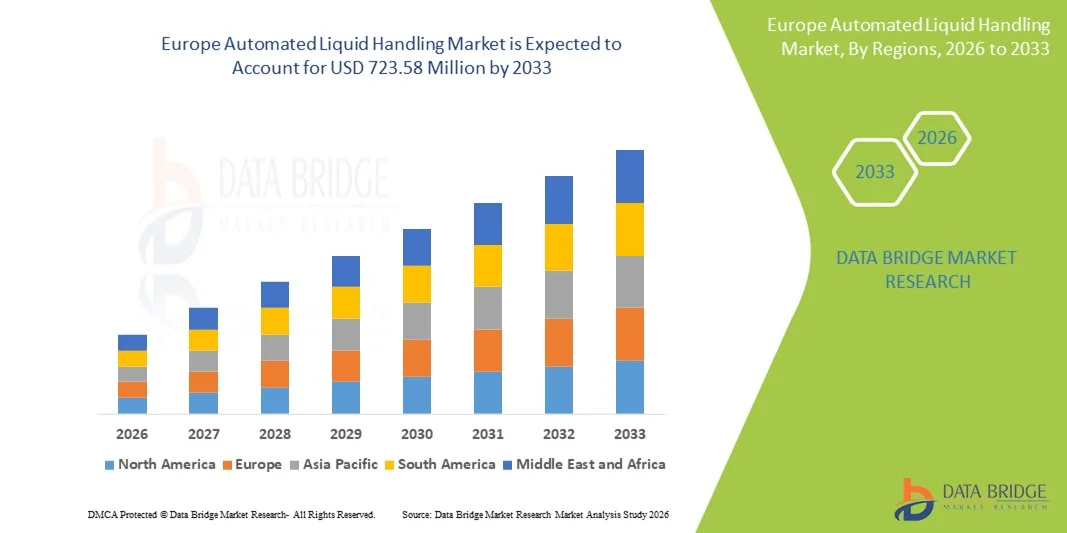

393.84 Million

USD

723.58 Million

2025

2033

USD

393.84 Million

USD

723.58 Million

2025

2033

| 2026 –2033 | |

| USD 393.84 Million | |

| USD 723.58 Million | |

| % | |

|

Europe Automated Liquid Handling Market Segmentation, By Product (Automated Liquid Handling Workstations, Reagents & Consumables and Others), Type (Automated Liquid Handling Systems and Semi-Automated Liquid Handling), Procedure (PCR Setup, Plate Replication, Serial Dilution, High Throughput Screening, Plate Reformatting, Cell Culture, Whole Genome Amplification, Array Printing, and Others), Modality (Disposable Tips and Fixed Tips), Application (Genomics, Drug Discovery, Clinical Diagnostics, Proteomics, and Others), End User (Biotechnology and Pharmaceutical Industries, Research Institutes, Hospitals, and Diagnostic Laboratories, Academic Institutes, and Others), Distribution Channel (Direct Tender, Retail Sales and Third Party Distributor)- Industry Trends and Forecast to 2033

ما هو حجم ومعدل النمو في أوروبا سوق التعامل الآلي مع السيولة؟

- وفقاً لتحليل بحوث سوق سوق جسر البيانات، قُيِّر حجم سوق مناولة سائلة مؤتمتة في أوروبا بقيمة(ب) 393.84 مليون دولار في عام 2025ومن المتوقع أن يتم ذلكباء -, ماالرقم الإجمالي الإجمالي لـ 7.9%خلال الفترة التي

- ويستمد نمو السوق إلى حد كبير وقوده من زيادة اعتماد تكنولوجيات التشغيل الآلي للمختبرات، ومن أنشطة البحث والتطوير القوية في جميع أنحاءالتكنولوجيا الحيوية(ج) زيادة الطلب على حلول المناولة السائلة العاليةالميجوالتشخيصات

- فضلاً عن ذلك، فإن ارتفاع الاستثمار في محطات العمل والكواشف المتقدمة، وزيادة التركيز على الدقة والقابلية للتكرار في تدفق العمل في المختبرات، والوجود القوي لمعاهد البحوث وشركات الصيدلة في مختلف أنحاء أوروبا، تؤدي إلى دفع الطلب على منصات المناولة السائلة الآلية. وهذه العوامل المتقاربة تعمل على التعجيل بامتصاص نظم المناولة السائلة الآلية، وبالتالي تعزيز نمو الصناعة بشكل كبير.

سوق الحجم و توقّر

- القيمة السوقية (2025)المبلغ: 393.84

- القيمة السوقية المتوقعة (2033): 723.58

- )٢٠٢٦-٢٠٣٣(: 7.9%

تحليل أسواق مناولة

- نظم المناولة الآلية للمعالجة السائلة، التي تتيح نقلاً سائلاً دقيقاً وقابلاً للتكرار وتجهيزاً للعينات وتجهيزاً للسوائل، أصبحت بشكل متزايد من المكونات الحيوية للمختبرات الحديثة في كل من البحث والسياقين البحثي والإكلينيكي نظراً لدقتها المعززة، وقدراتها العالية الإنتاجية، وتكاملها السلس مع تدفقات سير العمل في المختبرات

- ويؤجج الطلب المتزايد على المناولة الآلية للسائل الآلي في المقام الأول من تزايد اعتماد تكنولوجيات التشغيل الآلي للمختبرات، وزيادة أنشطة البحث والتطوير في قطاعي المستحضرات الصيدلانية والتكنولوجيا الأحيائية، وتزايد الحاجة إلى تجهيز العينات بسرعة أكبر وأكثر موثوقية وخالية من التلوث.

- تهيمن ألمانيا على سوق المناولة السائلة الآلية بأكبر حصة من الإيرادات بلغت 38.2 في المائة في عام 2025، وتميزت بالهياكل الأساسية البحثية المتقدمة، والدعم الحكومي القوي لعلوم الحياة، والتركيز العالي للجهات الفاعلة الرئيسية في الصناعة

- ومن المتوقع أن تكون إيطاليا أسرع البلدان نموا في سوق المناولة الآلية السائلة للمناولة خلال الفترة المتوقعة بسبب توسيع نطاق بحوث التكنولوجيا الحيوية، وزيادة الاستثمارات المختبرية، وزيادة الطلب على التشغيل الآلي في التطبيقات الصيدلانية والتشخيصية

- هيمنة قطاع محطات العمل الآلية لمناولة المناولة السائلة على سوق أوروبا بحصة سوقية قدرها 42.9 في المائة في عام 2025، مدفوعة بسمعتها الراسخة في التنوع والدقة والاندماج السلس في تدفقات العمل المختبرية الحالية

ألف - التقرير عن

|

الصفات الأولى |

أوروبا أوروبا |

|

المُسَجَّل |

|

|

البلدان |

أوروبا

|

|

& مفتاح |

|

|

ما |

|

|

جاري |

وبالإضافة إلى الرؤى المتعلقة بسيناريوهات السوق مثل القيمة السوقية، ومعدل النمو، والتجزئة، والتغطية الجغرافية، والجهات الفاعلة الرئيسية، فإن تقارير السوق التي تُعدها بحوث سوق جسر البيانات تتضمن أيضاً تحليلاً متعمقاً للخبراء، وعلم الأوبئة للمرضى، وتحليل خطوط الأنابيب، وتحليل الأسعار، والإطار التنظيمي. |

ما هي الاتجاهات الرئيسية في أوروبا

تعزيز الكفاءة من خلال التكامل مع الروبوتات والمساعـدة

- وثمة اتجاه هام ومتسارع في سوق المناولة السائلة الآلية لأوروبا يتمثل في التكامل المتزايد مع النظم الآلية والاستخبارات الاصطناعية، مما يمكِّن المختبرات من أداء تدفقات عمل معقدة بالحد الأدنى من التدخل البشري وزيادة إمكانية إعادة المعالجة.

- فعلى سبيل المثال، تدمج محطة العمل المعنية بالتشغيل الآلي المفلورة في Tecan Tecan Tecon Flan Automatation Techan Tean Techan Automatation Technan Techan Complements Teigning Procutetes بموجّهات AI مع المناولة الآلية للطبقات، مما يتيح للباحثين تبسيط عمليات فحص النواتج العالية وإعداد العينات.

- ويمكّن التكامل في المناولة السائلة المؤتمتة من تمكين سمات من قبيل كشف الخطأ التنبؤي، والتعظيم الأمثل لسُبل النقل السائلة، وتعديلات بروتوكول التكيف استناداً إلى نوع العينة.

- يتيح التكامل السلس لنظم المناولة السائلة المؤتمتة مع نظم إدارة المعلومات المختبرية الأوسع نطاقاً (LIMS) ومنصات التشغيل الآلي التحكم المركزي في عمليات متعددة، بما في ذلك تركيب نظام مراقبة مراقبة

- إن هذا الاتجاه نحو إيجاد حلول أكثر ذكاءً ودقة وترابطاً للتشغيل الآلي للمختبرات هو في الأساس إعادة تشكيل جذرية لكفاءة تدفق العمل ومعايير إعادة القابلية للتكرار. ونتيجة لذلك، تعمل شركات مثل شركة Agilent Technologies على تطوير متعاملين آليين آليين قادرين على وضع جداول تنبؤية وبروتوكولات تكيف للتعامل مع السوائل.

- الطلب على نظم المناولة السائلة المؤتمتة التي تتيح التكامل في مجال الذكاء المتطور والروبوتات يتزايد بسرعة في جميع قطاعات التكنولوجيا الأحيائية، والصيدلة، والبحوث السريرية، حيث تعطي المختبرات الأولوية بشكل متزايد لسرعة ودقة وأتمتة تدفقات العمل المعقدة

- أصبح من الشائع استخدام أدوات المناولة الآلية لمعالجة السائل الآلي إلى الحدين إلى الحدين إلى الحدين الأدنى والنمائط في هذه الأدوات، مما يتيح للمختبرات الأصغر اعتماد نظم قابلة للتطوير مع الحفاظ في الوقت نفسه على الدقة والإنتاج لمختلف التطبيقات

أوروبا أوروبا

سائق

الحاجة المتزايدة إلى توسيع نطاق البحث والتطوير في مجال التكنولوجيا الأحيائية والتشغيل الآلي للمختبرات

- الاستثمار المتزايد في بحوث التكنولوجيا الأحيائية وفي البحث والتطوير في مجال التكنولوجيا الأحيائية وفي البحث والتطوير في مجال المستحضرات الصيدلانية، إلى جانب الطلب المتزايد على التشغيل الآلي للمختبرات ذات الأداء العالي، هو عامل محرك رئيسي لاعتماد المعالجة السائلة الآلية

- فعلى سبيل المثال، في آذار/مارس 2025، أعلن بيكمان كولتر نشر نظم آلية لمناولة السوائل في مختبرات الجينوم الأوروبية للتعجيل باكتشاف المخدرات وسير سير العمل في تسلسلها الجيني

- وبينما تسعى المختبرات إلى المناولة السائلة بصورة أسرع وأكثر موثوقية وأكثر خلوا من التلوث، توفر النظم المؤتمتة سمات متقدمة من قبيل الأنابيب المتعددة القنوات، والبروتوكولات القابلة للبرمجة، والتكامل مع نظام إدارة المعلومات المصغرة (LMS)، مما يتيح تحسيناً مقنعاً على التقنية اليدوية.

- وعلاوة على ذلك، فإن الاتجاه التصاعدي لبحوث الطب الشخصي والبحوث المتعلقة بالجينومات يجعل من المناولة السائلة المؤتمتة جزءا لا يتجزأ من تدفق العمل في المختبرات، مما يمكّن من معالجة العينات بطريقة قابلة للتكرار والقياس.

- إن القدرة على أداء إجراءات معقدة مثل تركيب نظام مراقبة إطلاق مبيدات الآفات، والتمرير التسلسلي، والفرز العالي الإنتاجية مع الحد الأدنى من التدخل البشري، تدفع إلى اعتماد نظم آلية لمناولة السوائل عبر معاهد البحوث والمستشفيات والشركات الصيدلانية

- زيادة المتطلبات التنظيمية للقابلية للتكرار وتعقب البيانات في المختبرات السريرية والتشخيصية تؤدي أيضا إلى اعتماد المناولة السائلة الآلية، بما يكفل الامتثال لمعايير الاتحاد الأوروبي والمعايير الدولية

- :: تزايد التعاون بين الجامعات ومعاهد البحوث وشركات المستحضرات الصيدلانية وتسريع وتيرة الاستثمارات في الحلول الآلية لمعالجة المناولة السائلة من أجل تحسين الكفاءة وتقصير الجداول الزمنية لاكتشاف المخدرات

التعرّض/التحديي

التكاليف الرأسمالية العالية والخبرة التقنية

- ويشكل الاستثمار الأولي المرتفع نسبياً المطلوب لوسائل المناولة الآلية السائلة، إلى جانب تكاليف الصيانة المستمرة، تحدياً أمام اعتماد أوسع نطاقاً، لا سيما للمختبرات الصغيرة أو المُقيَّدة في الميزانية.

- فعلى سبيل المثال، تأخرت بعض المعاهد الأكاديمية الأوروبية في تنفيذ محطات عمل متقدمة لمناولة السوائل بسبب الإنفاق الأولي الكبير والحاجة إلى حيز مختبري مخصص.

- إن التصدي لهذه التحديات من خلال نظم نموذجية قابلة للقياس، وخيارات التأجير، ونماذج الخدمات المشتركة أمر بالغ الأهمية لتوسيع نطاق الاعتماد. وبالإضافة إلى ذلك، يتطلب التعامل الآلي بالسائل موظفين مدربين على الإعداد والبرمجة وحل المشاكل، وهو ما قد يحد من نشر المختبرات المحدودة الموارد.

- وفي الوقت الذي يحسن فيه التشغيل الآلي الكفاءة وقابلية إعادة التجديد، فإن منحنى التعلم المرتبط بالنظم المعقدة يمكن أن يؤدي إلى إبطاء التنفيذ، ولا سيما في المؤسسات التي تنتقل من مسارات العمل اليدوية

- والتغلب على هذه التحديات من خلال تبسيط الوصلات البينية، وبرامج تدريب الموظفين، وتصميم نظم فعالة من حيث التكلفة سيكون أمراً حيوياً للنمو المستدام لاعتماد المناولة الآلية السائلة في جميع أنحاء أوروبا.

- ويمكن أن تطرح مسائل التوافق مع معدات وبرمجيات المختبرات القديمة، ومعدات وبرامجيات المختبرات القديمة، تحديات تتعلق بالتكامل، مما يتطلب استثمارا إضافيا في تحسين النظم أو في الوصلات البينية الجمركية

- ويمكن أيضاً أن يعوق اعتماد الأسواق ضعف الوعي بين المختبرات الصغيرة فيما يتعلق بفوائد التشغيل الآلي، مما يستلزم قيام المورِّدين بتسويق محدد الهدف ومبادرات تعليمية.

أوروبا أوروبا

ويتم تقسيم السوق على أساس المنتج، والنوع، والإجراء، والأسلوب، والتطبيق، والمستعمل النهائي، وقناة التوزيع.

- )

وعلى أساس المنتج، فإن سوق المناولة السائلة المؤتمتة في أوروبا مقسمة إلى وحدات عمل آلية لمناولة البضائع السائلة، وموازين ومواد استهلاكية وغير ذلك. وكانت أجزاء محطات المناولة السائلة الآلية هي المهيمنة على السوق بأكبر حصة من الإيرادات بلغت 42.9% في عام 2025، مدفوعة بارتفاع تنوعها وقدرتها على التشغيل الآلي لتدفقات العمل المعقدة عبر تجهيزات أجهزة تحديد PCR، والتخفيف التسلسلي، والفحص العالي الإنتاجية. وتفضِّل البحوث والمختبرات السريرية على نحو متزايد محطات العمل من حيث قدرتها على الحد من الأخطاء البشرية، وتحسين القدرة على الانتقاص، والتعامل بكفاءة مع أحجام كبيرة من العينات. وتتكامل محطات العمل أيضاً مع المنصات الآلية ونظام LIMS، مما يمكِّن من التحكم المركزي وسير العمل على النحو الأمثل. ومما يزيد من تعزيز قيادة هذا القطاع الابتكارات المستمرة في دقة الأنابيب، وتكييف البروتوكولات، وتكامل الذكاء النووي. وبالإضافة إلى ذلك، فإن الوجود القوي للجهات الفاعلة الرئيسية التي تقدم حلولاً موحدة وقابلة للقياس يساهم في استمرار الهيمنة.

ومن المتوقع أن يشهد قطاع الكواشف والأصناف الاستهلاكية أسرع نمو من 2026 إلى 2033، الذي يغذيه ارتفاع عدد الدراسات المجينية والبروتيوميكية ذات الإنتاجية العالية التي تتطلب دراسات دقيقة وخالية من التلوث، والبقايا، والألواح، والكواشف. فالمواد الاستهلاكية ضرورية لأداء النظام على نحو سليم، والطلب المتكرر يضمن نمو الإيرادات بشكل ثابت. كما أن زيادة التركيز على الجودة، والتوحيد القياسي، والأصناف المستهلكة قبل المطابقة، تؤدي أيضاً إلى تبنيها. وتستثمر مختبرات التكنولوجيا الحيوية والتشخيص الناشئة في أوروبا، وخاصة في بلدان مثل إيطاليا وإسبانيا، في كواشف ومستهلكات متوافقة لتعزيز كفاءة تدفق العمل.

- نوع

وعلى أساس النوع، فإن سوق المناولة السائلة المؤتمتة في أوروبا مقسمة إلى نظم مناولة سائلة مؤتمتة ومناولة سوائل شبه مؤتمتة، وقد هيمنة قطاع نظم المناولة السائلة المؤتمتة على السوق في عام 2025 بسبب قدراتها الكاملة على التشغيل الآلي، مما مكّن عمليات مختبرية واسعة النطاق وعالية الإنتاجية مع الحد الأدنى من التدخل البشري، وهذه النظم تعتمد على نطاق واسع في مختبرات البحث والتطوير والجينومات والتشخيص السريري الصيدلانية حيث تكون السرعة والقابلية للتعديل والتعقب بالغة الأهمية.

ومن المتوقع أن يشهد قطاع المناولة السائلة شبه المؤتمتة أسرع نمو من 2026 إلى 2033، مدفوعاً بطلب من مختبرات متوسطة الحجم ومؤسسات بحث أكاديمية تتطلب التشغيل الآلي الجزئي بتكلفة أقل. وتوفر النظم شبه الآلية المرونة، مما يسمح للمستعملين بالتدخل يدوياً في الوقت الذي لا يزالون يستفيدون فيه من السرعة والدقة. ومن الأسهل أيضاً الاندماج في تدفقات العمل الحالية في المختبرات وتتطلب تدريباً أقل تخصصاً مقارنة بالنظم الآلية الكاملة. والواقع أن الاعتماد المتزايد للمختبرات المختلطة في أوروبا، وزيادة توافر المنصات شبه المؤتمتة النموذجية، يعملان على تغذية هذا النمو.

- براتج

وعلى أساس الإجراءات المتبعة، فإن سوق المناولة السائلة المؤتمتة لأوروبا مقسمة إلى تركيبات PCR، وتكرار لوحاتها، وتسارع تسلسلها، وفرزها العالي الإنتاجية، وإصلاح صفائحها، وثقافة الخلايا، وتضخيم الجينوم بأكمله، وطباعة المصفوفات، وغير ذلك.(والمختبرات التشخيصية الأوروبية تعطي الأولوية لأتمية اختبار PCR للتعامل مع أحجام كبيرة من الاختبارات، والامتثال للمعايير التنظيمية، والحد من مخاطر التلوث. كما أن الابتكارات المستمرة في استخدام الأنابيب الآلية والاستخدام الأمثل للبروتوكول الموجه من قبل منظمة العفو الدولية تزيد من تعزيز الهيمنة.

ومن المتوقع أن يشهد قطاع فحص الناتج المرتفع أسرع نمو من عام 2026 إلى عام 2033، مدفوعاً بتزايد الطلب في اكتشاف العقاقير والبحوث المتعلقة بالبروتينات. وتحتاج شركات الأدوية وشركات التكنولوجيا الحيوية إلى معالجة سائلة آلية من أجل تجهيز آلاف العينات بكفاءة، والتعجيل بتحديد هوية الرصاص، وتحسين إمكانية إعادة تقييمه. ويتعزز النمو بزيادة الاستثمارات في المكتبات المركبة، والأدوية الشخصية، ومنصات الفحص التي تحركها مبادرة الذكاء الفلكي. وتتبنى الأسواق الأوروبية الناشئة على نحو متزايد نظماً عالية الإنتاجية للحد من الجداول الزمنية وتكاليف البحث والتطوير.

- من خلال الطريقة

وعلى أساس الطريقة المتبعة، فإن سوق المناولة السائلة الآلية الأوروبية تُقسم إلى نصائح غير قابلة للتصرف وإكراميات ثابتة. وكانت شريحة البقشيشات المستعملة تهيمن على السوق في عام 2025، مدفوعة بقدرتها على الحد من مخاطر التلوث المتبادل، وضمان المناولة السائلة الدقيقة، والامتثال للمتطلبات التنظيمية الصارمة في التطبيقات الإكلينيكية والجينومية. ويُفضَّل النصائح القابلة للإزالة في مختبرات عالية الإنتاجية نظراً لصلاحيتها، وموثوقيتها، وسهولة استبدالها. ويدعم الابتكار المستمر في تصميم البقشيش، بما في ذلك البقشيش المنخفض الحيازة والمصفاة، الاعتماد الواسع النطاق. كما يستفيد هذا الجزء من الطلب المتكرر، حيث إن المواد الاستهلاكية تشكل جزءاً لا يتجزأ من العمليات المختبرية اليومية، بما يضمن النمو المستدام للإيرادات.

ومن المتوقع أن يشهد الجزء المتعلق بالإكراميات الثابتة أسرع نمو من عام 2026 إلى عام 2033، ولا سيما في المختبرات والمؤسسات الأكاديمية التي تراعي التكاليف، والتي تسعى إلى استثمارات طويلة الأجل مع خفض النفقات الاستهلاكية المتكررة. فالتركات الثابتة دائمة، وتتيح الاستخدام المتكرر مع التنظيف السليم، وتتكامل بشكل متزايد مع النظم الآلية النموذجية. ويزيد زيادة الوعي بممارسات المختبرات المستدامة والحد من النفايات البلاستيكية في المختبرات من التعجيل باعتماد نظم اللمبات الثابتة في أوروبا.

- ألف -

وعلى أساس التطبيق، فإن سوق المناولة السائلة المؤتمتة الأوروبية تُقسم إلى جينومات، واكتشافات للمخدرات، وتشخيصات سريرية، وبروتيوميكس، وغير ذلك. وكان الجزء المتعلق بالجينومات مهيمناً على السوق في عام 2025 بسبب تزايد عدد المشاريع المتوالية، ودراسات التعبير الجينات، وبحوث الطب الشخصي في مختلف أنحاء أوروبا. وتكفل المناولة الآلية السائلة قابلية إعادة التجديد، وإعداد عينات عالية الإنتاجية، والحد الأدنى من التلوث في التحليلات الجينية الحساسة. وتستثمر الحكومات ومؤسسات البحوث الخاصة استثماراً كبيراً في البنية الأساسية للجينومات، مما يعزز هيمنة القطاعات.

ومن المتوقع أن يشهد قطاع اكتشاف المخدرات أسرع نمو من عام 2026 إلى عام 2033، مدفوعاً بارتفاع الإنفاق على البحث والتطوير من جانب شركات المستحضرات الصيدلانية وشركات التكنولوجيا الحيوية. فنظم المناولة السائلة الآلية تتسارع من الفرز، وتختبر المركبات، وتطوير القراءات، وتخفض من الجداول الزمنية والتكاليف التشغيلية. كما أن التركيز المتزايد على الطب الدقيق والبيولوجيا يعمل على زيادة تطوير الوقود. والواقع أن مراكز البحوث الناشئة في أسبانيا وإيطاليا وبلدان الشمال الأوروبي تستثمر بشكل كبير في منصات اكتشاف العقاقير الآلية، الأمر الذي يساهم في النمو السريع.

- هذا

واستناداً إلى المستخدم النهائي، فإن سوق المناولة السائلة الآلية الأوروبية مقسمة إلى التكنولوجيا الأحيائية والصناعات الصيدلانية، ومعاهد البحوث، والمستشفيات ومختبرات التشخيص، والمعاهد الأكاديمية، وغيرها. وكان قطاع التكنولوجيا الأحيائية والصناعات الصيدلانية يهيمن على السوق في عام 2025، مدفوعاً باعتماد واسع النطاق لاكتشاف المخدرات، وتطوير البيولوجيا، والفحص العالي الإنتاجية. وأعطت هذه المنظمات الأولوية للتشغيل الآلي لتحسين كفاءة تدفق العمل، والتكرير، والامتثال التنظيمي. والاستثمار المستمر في البحث والتطوير وتوسيع مرافق المختبرات يعزز الهيمنة.

ومن المتوقع أن يشهد قطاع المعاهد الأكاديمية أسرع نمو من عام 2026 إلى عام 2033، مدعوماً بزيادة تمويل البحوث، والتعاون مع الصناعة، واعتماد نظم شبه آلية للتدريب والتجريب. وتستثمر المختبرات الأكاديمية في التشغيل الآلي لتحسين الإنتاج، والتقليل إلى أدنى حد من الأخطاء، وتوفير الخبرة العملية للطلبة في تقنيات البحث الحديثة. والمبادرات الحكومية الداعمة للابتكار في علوم الحياة تدفع النمو القطاعي إلى الأمام.

- حسب التوزيع

وعلى أساس قناة التوزيع، تُقسم سوق المناولة السائلة الآلية في أوروبا إلى مناقصات مباشرة، ومبيعات بالتجزئة، وموزعات من طرف ثالث. وكان قطاع العطاء المباشر مسيطراً على السوق في عام 2025، مدفوعاً بالأفضلية بين المستشفيات الكبرى، ومختبرات التشخيص، وشركات المستحضرات الصيدلانية في الشراء المباشر من الصانعين لضمان تكييف النظام، ودعم الصيانة، واتفاقات الخدمات الطويلة الأجل. كما تسمح العطاءات المباشرة باتفاقات الشراء بالجملة، والتسليم الأسرع، والدعم التقني، وهو أمر بالغ الأهمية بالنسبة للمختبرات العالية الإنتاجية.

ومن المتوقع أن يشهد قطاع الموزعين من الأطراف الثالثة أسرع نمو من 2026 إلى 2033، وخاصة في الأسواق الأوروبية الناشئة حيث تعتمد المختبرات الصغيرة على الموزعين في الوصول إلى النظم الميسورة التكلفة، والمواد الاستهلاكية، وعقود الخدمات. كما يوفر الموزعون التدريب، والدعم الموقعي، وخيارات التمويل المرنة، مما يجعل التشغيل الآلي أيسر منالاً لقاعدة عملاء أوسع نطاقا. كما يدعم النمو الموزعون الذين يقدمون الحلول المجمعة، والمواد الاستهلاكية، وخدمات الصيانة جنباً إلى جنب مع منصات التشغيل الآلي.

السوق الآلية لمعالجة المناولة في أوروبا

- تهيمن ألمانيا على سوق المناولة السائلة الآلية بأكبر حصة من الإيرادات بلغت 38.2 في المائة في عام 2025، وتميزت بالهياكل الأساسية البحثية المتقدمة، والدعم الحكومي القوي لعلوم الحياة، والتركيز العالي للجهات الفاعلة الرئيسية في الصناعة

- المختبرات في ألمانيا تقدِّر تقديرا عالياً ما تتيحه نظم المناولة السائلة المؤتمتة من قدرات دقيقة وقابلة للتكرير ونافعة عالية الإنتاجية تتيحه من دقة، وقابلية للتنقيح، وقدرة عالية الإنتاجية، مما يبسِّط إجراءات معقدة مثل تركيب أجهزة أجهزة من قبيل أجهزة أجهزة تحديد الكَرْب المبرَد، والمُميِّز التسلسلي، والفرز العالي الفعالية مع التقليل من الخطأ البشري إلى أدنى حد

- ويحظى هذا الاعتماد الواسع الانتشار بدعم إضافي من التمويل الحكومي للبحث والتطوير، ومعايير امتثال تنظيمية قوية، والتعاون بين معاهد البحوث والصناعة، وإنشاء نظم آلية لمناولة السوائل كحل مفضل للمختبرات الأكاديمية والإكلينيكية والصناعية.

ألمانيا سوق المناولة المُيسأة

ومن المتوقع أن تتوسع سوق المناولة السائلة الآلية في ألمانيا في إطار نظام إدارة المخاطر البيئية أثناء الفترة المتوقعة، والذي تغذيه البنية الأساسية البحثية المتقدمة، والدعم الحكومي القوي لعلوم الحياة، ووجود لاعبين رئيسيين في الصناعة. ومن المتوقع أن يؤدي تركيز ألمانيا على الإبداع والكفاءة إلى تشجيع تبني أنظمة المناولة السائلة الآلية، وخاصة في علم الجينوم، واكتشاف العقاقير، والتشخيص السريري. ويتزايد انتشار التكامل مع أنظمة إدارة المعلومات المختبرية والروبوتات، الأمر الذي يسمح بالمعالجة العالية الإنتاجية مع الحد الأدنى من التدخل البشري. ويتماشى التركيز المتزايد على إعادة الهيكلة ومراقبة الجودة مع المعايير المختبرية المحلية، الأمر الذي يدفع نمو السوق إلى النمو.

المملكة المتحدة. سوق مناولة سائلة مؤتمتة

ومن المتوقع أن تنمو سوق المناولة السائلة الآلية في المملكة المتحدة عند مستوى جدير بالملاحظة في سجل مراجعة الحسابات الشامل خلال الفترة المتوقعة، وذلك بسبب زيادة أنشطة البحث والتطوير في قطاعي التكنولوجيا الحيوية والصيدلانية، وتزايد الطلب على التشغيل الآلي في المختبرات الأكاديمية والإكلينيكية. ومن المتوقع أن تؤدي المخاوف المتعلقة بسلامة العينة، وكفاءة تدفق العمل، والامتثال التنظيمي إلى تشجيع المختبرات على تبني حلول آلية لمعالجة السوائل. ومن المتوقع أن يؤدي النظام الإيكولوجي القوي للبحوث في المملكة المتحدة والمبادرات الحكومية الداعمة للابتكار إلى زيادة تحفيز توسع السوق.

فرنسا السوق الآلية لمعالجة المناولة

ومن المتوقع أن تشهد سوق المناولة الآلية للسوائل الفرنسية توسعاً مطرداً خلال الفترة المتوقعة بسبب تزايد الاعتماد في البحث والتطوير في مجال الصيدلة ومختبرات التشخيص السريري. وتعمل المختبرات في فرنسا بشكل متزايد على تنفيذ أنظمة آلية لفحص الإنتاج العالي، ووضع نظام للفرز المتسلسل للكيماويات، والتخفيف التسلسلي من أجل تعزيز الكفاءة، والقابلية للتكرار، والقدرة على التعقب. كما يعمل الدعم الحكومي لعلوم الحياة والتعاون بين معاهد البحوث والشركات الخاصة على دفع عملية تكامل النظم واعتمادها. كما تساهم زيادة الاستثمارات في البحوث الوراثية والطب الشخصي في نمو الأسواق.

سوق مناولة سائلة آلية

ومن المتوقع أن تنمو سوق المناولة الآلية للسوائل في إيطاليا بأسرع ما يمكن خلال الفترة المتوقعة، وذلك بفضل التوسع في بحوث التكنولوجيا الحيوية، وزيادة الاستثمارات في المختبرات، وتزايد الحاجة إلى التشغيل الآلي في المختبرات السريرية والأكاديمية. وتتبنى المختبرات الإيطالية نظم المناولة السائلة الآلية لتحسين ناتج العينة، والحد من الأخطاء البشرية، والامتثال للأنظمة الصارمة للاتحاد الأوروبي. وبالإضافة إلى ذلك، فإن الوجود المتزايد لشركات الصيدلة والتشخيص التي تسعى إلى تحقيق سير العمل بكفاءة هو الطلب المتزايد. كما أن توفر الأنظمة النموذجية وشبه الآلية يدعم أيضاً تبنيها عبر مجموعة أوسع من أحجام المختبرات.

أوروبا

وتقود صناعة المناولة الآلية للسوائل في أوروبا في المقام الأول شركات راسخة، بما في ذلك:

- (الولايات المتحدة الأمريكية)

- مؤسسة Terrmo Fisher Science Inc. (الولايات المتحدة الأمريكية)

- شركة هاملتون (الولايات المتحدة الأمريكية)

- Tcan Group Ltd. (سويسرا)

- بيركين إلمرر (الولايات المتحدة الأمريكية)

- إيبندورف SE (ألمانيا)

- بيكمان كولتر، Inc. (الولايات المتحدة)

- أناييتيك جينا غمبه (ألمانيا)

- صكوك بيولوجية (الولايات المتحدة الأمريكية)

- غيلسون، In Inc. (الولايات المتحدة الأمريكية)

- (الولايات المتحدة الأمريكية)

- الفريق المعني بعلوم البيولوجيا (سويسرا)

- )ألمانيا(

- (كندا)

- لابسييتي، Inc. (الولايات المتحدة الأمريكية)

- (الولايات المتحدة الأمريكية)

- مؤسسة كورننغ (الولايات المتحدة الأمريكية)

- QIAG (هولندا)

- (U.K.)

- التشخيصات التشخيصية (بلجيكا)

ما هي التطورات الأخيرة في أوروبا سوق المناولة الآلية للسوائل؟

- وفي حزيران/يونيه 2025، اعترف برنامج الأساليب المُحَقَّقة في إيلومينا ببرنامج التشغيل الآلي لنظام المعلومات الجغرافية التابع للجنة الفرعية لمنع التعذيب (NGS) التابع للجنة الفرعية لمنع الجريمة والعدالة الجنائية، الذي يؤكد على صحة الصناعة لسير عملها الآلي في مجال المناولة السائلة بالنسبة لمجموعات المواد التحضيرية للحمض النووي للحمض النووي في إيلومينا، مما يعزز القابلية لإعادة التجديد ويقلل من الوقت الذي تستغرقه المختبرات في التعاقب.

- وفي أيار/مايو 2024، اختارت العلوم البيولوجية المساحية منصة المناولة السائلة للحرائق الذبابية التابعة للجنة الفرعية لمنع التعذيب التابعة للجنة الفرعية لمنع الجريمة والعدالة الجنائية لتسريع وتيرة قدرات التعاقب التعاقبي المقبل، مع تسليط الضوء على الكيفية التي يجري بها نشر المعالجين السائلين الآليين خارج المختبرات التقليدية لدعم بحوث الجينومات الواسعة النطاق والتنوع البيولوجي بنواتج ودقة محسّنة.

- وفي شباط/فبراير 2024، أطلقت اللجنة الفرعية لمنع التعذيب، Labtetech، منصة الشعلة +، وهي توسيع لكل منصة المناولة السائلة التابعة لها، التي تدمج في كل منظومتها دورة حرارة في الموقع، وقدرة أكبر على استخدام معدات المختبرات، مما يمكّن من القيام على نحو كامل ومتحرر من الأيدي، بإتاحة تدفق الأعمال التحضيرية لمكتبة NGS للمختبرات ذات الحيز المحدود والموظفين المحدودين.

- وفي تشرين الثاني/نوفمبر 2023، أطلقت اللجنة الفرعية لابتك تحسينات على منصة التطفّل بالحرائق الخاصة بها للاختبارات المطورة في المختبرات، مما مكّن المختبرات السريرية من تبسيط وتسريع التجهيزات الممهدة للمكتبات التي تقوم بها مجموعة الخدمات التقنية الوطنية من خلال المعالجة السائلة بالبرمجيات السهلة الاستعمال وأتمتة سير العمل المصممة خصيصاً للبيئات المنظمة.

- في مايو 2023، قدم Opentrons الروبوت Opentrons Flex، وهو جيل جديد من روبوتات المناولة السائلة البسيطة الرخيصة والبسيطة، مصممة لتوسيع نطاق الوصول إلى تدفق العمل الآلي، لا سيما في بيئات البحوث والمختبرات الأصغر حجما.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.