Global Aerospace 3d Printing Materials Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

4.96 Billion

USD

18.91 Billion

2025

2033

USD

4.96 Billion

USD

18.91 Billion

2025

2033

| 2026 –2033 | |

| USD 4.96 Billion | |

| USD 18.91 Billion | |

| % | |

|

تقسيم سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء العالمي، حسب القطاع (المواد والطابعات)، وتقنية الطباعة (الطباعة المجسمة الضوئية (SLA)، ونمذجة الترسيب بالانصهار (FDM)، والتلبيد الليزري المباشر للمعادن (DMLS)، والتلبيد الليزري الانتقائي (SLS)، والإنتاج المستمر للواجهة السائلة (CLIP)، وغيرها)، والمادة (البلاستيك، والمعادن، والسيراميك، وغيرها)، والتطبيق (النماذج الأولية السريعة، والأدوات، وإنتاج الأجزاء)، وأجزاء الطائرات (المحرك، والمكونات الهيكلية، والتركيبات والتجهيزات)، والاستخدام النهائي (الطائرات والمركبات الفضائية) - اتجاهات الصناعة وتوقعاتها حتى عام 2033

حجم سوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران

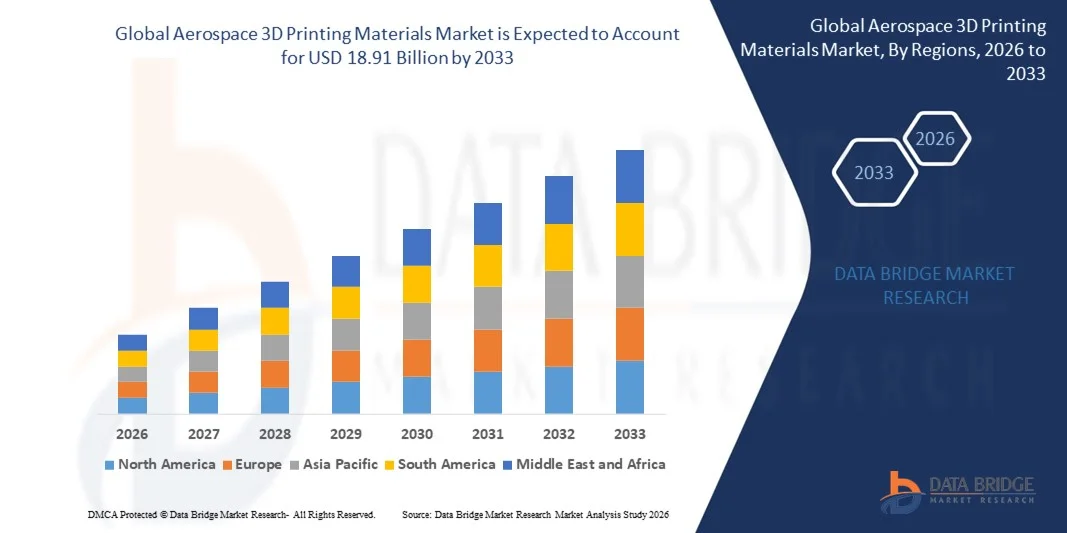

- بلغت قيمة سوق مواد الطباعة ثلاثية الأبعاد في صناعة الطيران والفضاء العالمية 4.96 مليار دولار أمريكي في عام 2025، ومن المتوقع أن تصل إلى 18.91 مليار دولار أمريكي بحلول عام 2033 ، بمعدل نمو سنوي مركب قدره 18.20% خلال فترة التوقعات.

- يعود نمو السوق إلى حد كبير إلى تزايد اعتماد التصنيع الإضافي في صناعة الطيران، مدفوعاً بالحاجة إلى مكونات خفيفة الوزن وعالية الأداء، والنماذج الأولية السريعة، والإنتاج الفعال من حيث التكلفة للأشكال الهندسية المعقدة.

- علاوة على ذلك، فإن التطورات في مواد الطباعة ثلاثية الأبعاد، بما في ذلك المعادن عالية القوة، والبوليمرات المستخدمة في صناعة الطيران، والمركبات المتخصصة، تُمكّن المصنّعين من إنتاج مكونات بالغة الأهمية ذات متانة ودقة محسّنتين، مما يُسرّع من توسع السوق.

تحليل سوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران والفضاء

- أصبحت مواد الطباعة ثلاثية الأبعاد المستخدمة في صناعة الطيران، بما في ذلك مساحيق المعادن والبوليمرات والمواد المركبة، جزءًا لا يتجزأ من إنتاج المكونات الهيكلية وأجزاء المحركات والأدوات، حيث توفر مرونة في التصميم، ووزنًا أقل، وأوقات تسليم أسرع مقارنة بأساليب التصنيع التقليدية.

- يعود الطلب المتزايد على التصنيع الإضافي في المقام الأول إلى سعي مصنعي المعدات الأصلية وموردي صناعة الطيران والفضاء إلى الحصول على مكونات طائرات خفيفة الوزن وموفرة للوقود، وزيادة اعتماد المواد المتقدمة، ودمج تقنيات التصميم الرقمي والمحاكاة لتحسين الأداء وتقليل دورات الإنتاج.

- هيمنت أمريكا الشمالية على سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء بحصة بلغت 40.70% في عام 2025، وذلك بفضل وجود كبرى شركات تصنيع الطيران والفضاء، والاعتماد الكبير لتقنيات التصنيع المتقدمة، والاستثمارات القوية في البحث والتطوير.

- من المتوقع أن تكون منطقة آسيا والمحيط الهادئ أسرع المناطق نمواً في سوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران والفضاء خلال الفترة المتوقعة، وذلك نتيجة لزيادة الاستثمارات في تصنيع الطيران والفضاء، والتوسع الحضري السريع، والتقدم التكنولوجي في دول مثل الصين واليابان والهند.

- هيمن قطاع المعادن على السوق بحصة بلغت 57.6% في عام 2025، وذلك نظراً للحاجة الماسة إلى قطع غيار عالية القوة وخفيفة الوزن ومقاومة للحرارة في صناعة الطيران. وتوفر معادن مثل التيتانيوم والألومنيوم والإنكونيل أداءً ميكانيكياً فائقاً للمحركات والمكونات الهيكلية والتجميعات الحيوية في صناعة الطيران.

نطاق التقرير وتجزئة سوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران

|

صفات |

أهم رؤى السوق لمواد الطباعة ثلاثية الأبعاد في قطاع الطيران |

|

القطاعات التي تم تغطيتها |

|

|

الدول المشمولة |

أمريكا الشمالية

أوروبا

منطقة آسيا والمحيط الهادئ

الشرق الأوسط وأفريقيا

أمريكا الجنوبية

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات بيانات القيمة المضافة |

بالإضافة إلى رؤى السوق مثل قيمة السوق ومعدل النمو وقطاعات السوق والتغطية الجغرافية واللاعبين في السوق وسيناريو السوق، يتضمن تقرير السوق الذي أعده فريق أبحاث السوق في Data Bridge تحليلاً متعمقاً من قبل الخبراء، وتحليلاً للاستيراد والتصدير، وتحليلاً للتسعير، وتحليلاً لاستهلاك الإنتاج، وتحليلاً لـ PESTLE. |

اتجاهات سوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران والفضاء

اعتماد مواد الطباعة ثلاثية الأبعاد المعدنية والبوليمرية عالية الأداء

- A key trend in the aerospace 3D printing materials market is the growing use of metal powders and high-performance polymers for additive manufacturing of critical aircraft components, driven by the need for lightweight structures, complex geometries, and improved fuel efficiency. These materials are enabling designers and engineers to reduce production lead times and increase design flexibility in aerospace manufacturing

- For instance, companies such as GE Additive and EOS supply titanium and nickel-based metal powders for 3D printing structural components and engine parts that meet stringent aerospace standards. Such materials allow for weight reduction while maintaining mechanical strength and thermal resistance in operational environments

- High-performance polymers such as PEKK and PEEK are increasingly incorporated in the fabrication of interior cabin parts and structural elements where weight savings and chemical resistance are critical. The adoption of these polymers is expanding the range of aerospace applications suitable for additive manufacturing

- The trend toward hybrid manufacturing approaches that combine 3D-printed metal or polymer parts with traditional machining is gaining traction. This approach supports enhanced material utilization, cost optimization, and improved component performance

- The aerospace sector is integrating additive manufacturing for prototyping, tooling, and low-volume production where complex geometries or customized designs are required. This practice is accelerating innovation cycles and reducing overall development costs in aircraft and spacecraft programs

- Rising investments in R&D for new 3D printing materials with higher temperature tolerance, corrosion resistance, and improved mechanical properties are reinforcing the adoption of additive manufacturing in aerospace. These developments are positioning 3D printing materials as essential enablers of next-generation aircraft design and production

Aerospace 3D Printing Materials Market Dynamics

Driver

Rising Demand for Lightweight and Complex Aerospace Components

- The demand for lighter, more fuel-efficient aircraft and spacecraft is driving adoption of 3D printing materials that support complex geometries and reduced component weight. These materials allow aerospace manufacturers to optimize performance while adhering to strict safety and regulatory standards

- For instance, Boeing leverages titanium and aluminum 3D-printed parts in its 787 Dreamliner and other aircraft programs to reduce weight and enhance structural efficiency. These components contribute to lower fuel consumption and increased payload capacity

- The need for rapid prototyping and faster production of low-volume, highly specialized components is expanding the use of additive manufacturing in aerospace supply chains. 3D printing materials support iterative design, customization, and accelerated time-to-market

- Manufacturers are increasingly focusing on high-strength metals and polymers to produce engine parts, brackets, and structural components that were previously impossible to fabricate efficiently. This capability is enabling more advanced designs and higher component integration

- The requirement for continuous innovation in aerospace systems and the expansion of commercial and defense aerospace programs are reinforcing the importance of 3D printing materials. These materials are central to achieving performance, safety, and efficiency objectives across aircraft and spacecraft

Restraint/Challenge

High Material Costs and Certification Requirements

- The aerospace 3D printing materials market faces challenges due to the high cost of metal powders and high-performance polymers that meet strict aerospace standards. These costs impact production budgets and slow widespread adoption of additive manufacturing across the industry

- For instance, companies such as Safran utilize rigorous testing and certification protocols for 3D-printed titanium engine components, which increase material selection constraints and development timelines. Compliance with FAA and EASA regulations adds complexity and cost

- Ensuring repeatability, traceability, and quality assurance for critical flight components requires specialized manufacturing environments and extensive validation procedures. This further elevates operational expenses and limits scalability

- Limited availability of certified aerospace-grade 3D printing powders and filaments can create supply bottlenecks, especially for high-demand alloys and polymers. Manufacturers must carefully manage material sourcing to maintain production schedules

- Balancing material performance with economic feasibility continues to challenge aerospace manufacturers. Overcoming cost and certification hurdles is essential to broaden the adoption of 3D printing materials across commercial, defense, and space applications

Aerospace 3D Printing Materials Market Scope

The market is segmented on the basis of vertical, printer technology, material, application, aircraft parts, and end-use.

- By Vertical

On the basis of vertical, the aerospace 3D printing materials market is segmented into material and printer. The material segment dominated the market with the largest revenue share in 2025, driven by the increasing demand for advanced aerospace-grade materials that can withstand extreme temperatures, high stress, and corrosion. Aerospace manufacturers are prioritizing high-performance materials to achieve weight reduction and fuel efficiency, making material innovations central to market growth. The growing adoption of additive manufacturing for producing complex components has further amplified the need for specialized materials, as they enable the production of parts with precise mechanical properties and geometries. In addition, partnerships between material suppliers and aerospace companies are fostering continuous development and availability of next-generation 3D printing materials.

The printer segment is expected to witness the fastest growth from 2026 to 2033, fueled by advancements in 3D printer technologies tailored for aerospace applications. For instance, companies such as Stratasys and EOS are introducing high-precision printers that support multiple materials, allowing manufacturers to create lightweight and structurally robust parts efficiently. Increasing investments in in-house 3D printing facilities by aerospace OEMs to reduce lead times and production costs are further accelerating printer adoption. The expansion of industrial-scale 3D printing services for aerospace also contributes to the segment’s rapid growth, enabling flexible and on-demand production of critical components.

- By Printer Technology

On the basis of printer technology, the market is segmented into Stereolithography (SLA), Fusion Deposition Modelling (FDM), Direct Metal Laser Sintering (DMLS), Selective Laser Sintering (SLS), Continuous Liquid Interface Production (CLIP), and others. The DMLS segment dominated the market in 2025 due to its capability to produce high-strength metal parts with complex geometries, meeting the stringent structural and safety requirements of aerospace applications. DMLS allows precise control over material properties, enabling lightweight, high-performance components that reduce fuel consumption and operational costs. Its established track record for reliability in producing structural aerospace parts also reinforces its dominance. In addition, collaborations between aerospace companies and DMLS printer manufacturers have facilitated optimized workflows and material integration, driving consistent demand.

The FDM segment is projected to experience the fastest CAGR from 2026 to 2033, driven by its cost-effectiveness, versatility, and suitability for rapid prototyping. For instance, companies such as Stratasys are expanding their FDM offerings to accommodate larger aerospace components with enhanced accuracy. The ability to quickly iterate designs and produce functional prototypes reduces development timelines, which is critical for aerospace R&D. Moreover, FDM printers’ compatibility with a wide range of thermoplastic materials allows manufacturers to test material performance efficiently, accelerating product development cycles.

- By Material

On the basis of material, the market is segmented into plastic, metals, ceramic, and others. The metals segment dominated the market with the largest share of 57.6% in 2025 due to the critical requirement for high-strength, lightweight, and heat-resistant parts in aerospace manufacturing. Metals such as titanium, aluminum, and Inconel provide superior mechanical performance for engines, structural components, and critical aerospace assemblies. The rising need for weight reduction in aircraft and spacecraft to enhance fuel efficiency and payload capacity further drives the adoption of metal 3D printing materials. In addition, metal powders compatible with advanced 3D printing technologies are increasingly available through partnerships between material suppliers and aerospace manufacturers, reinforcing the segment’s dominance.

The plastics segment is expected to witness the fastest growth from 2026 to 2033, fueled by the increasing use of high-performance thermoplastics for tooling, jigs, and rapid prototyping. For instance, Stratasys offers aerospace-grade thermoplastics that provide dimensional stability and chemical resistance, allowing manufacturers to produce functional prototypes and low-volume parts efficiently. The cost-effectiveness of plastic materials and the ability to reduce production lead times make them an attractive option for non-structural components. Growing innovation in reinforced plastics with improved thermal and mechanical properties is further supporting their adoption in aerospace applications.

- By Application

استنادًا إلى التطبيقات، يُقسّم السوق إلى النماذج الأولية السريعة، والأدوات، وإنتاج الأجزاء. وقد هيمن قطاع إنتاج الأجزاء على السوق في عام 2025 نظرًا لتزايد استخدام الطباعة ثلاثية الأبعاد لإنتاج مكونات وظيفية نهائية الاستخدام في صناعة الطيران والفضاء، تتميز بوزنها الخفيف وتصاميمها الهندسية المعقدة. ويستفيد المصنّعون من التصنيع الإضافي لاستبدال عمليات التصنيع التقليدية التي تعتمد على الطرح في إنتاج مكونات المحركات، والأجزاء الهيكلية، والتجميعات بالغة الأهمية للطيران، مما يقلل من هدر المواد ووقت الإنتاج. كما أن القدرة على طباعة مكونات مُخصصة ودمج مواد متطورة ذات خصائص ميكانيكية دقيقة تُعزز جاذبية الطباعة ثلاثية الأبعاد في إنتاج أجزاء الطيران والفضاء. بالإضافة إلى ذلك، ساهمت الموافقات التنظيمية من سلطات الطيران على المكونات النهائية المصنعة بتقنية الطباعة ثلاثية الأبعاد في تعزيز الثقة في هذا التطبيق.

من المتوقع أن يشهد قطاع النماذج الأولية السريعة أسرع نمو له بين عامي 2026 و2033، مدفوعًا بالحاجة إلى تسريع عملية التحقق من صحة التصميم واختباره. فعلى سبيل المثال، تستخدم شركة بوينغ النماذج الأولية السريعة لإجراء الاختبارات الوظيفية للمكونات المعقدة قبل البدء بالإنتاج على نطاق واسع. وتتيح سرعة ومرونة النماذج الأولية بتقنية الطباعة ثلاثية الأبعاد، بالإضافة إلى انخفاض تكلفتها، لشركات تصنيع الطائرات والفضاء الابتكار بوتيرة أسرع وتقليص دورات تطوير المنتجات. كما يُعزز التكامل مع تقنيات المحاكاة والتوائم الرقمية كفاءة النماذج الأولية، مما يدعم مسار نمو هذا القطاع.

- قطع غيار الطائرات

استنادًا إلى قطع غيار الطائرات، يُقسّم السوق إلى محركات، ومكونات هيكلية، وقوالب وتجهيزات. هيمنت المكونات الهيكلية على السوق في عام 2025 نظرًا للطلب المتزايد على قطع غيار خفيفة الوزن وعالية المتانة تُحسّن أداء الطائرات وكفاءتها في استهلاك الوقود. تُمكّن تقنية التصنيع الإضافي من إنتاج هياكل ذات أشكال هندسية معقدة تُقلّل الوزن دون المساس بالسلامة الهيكلية. كما يسمح استخدام المكونات الهيكلية المطبوعة ثلاثية الأبعاد للمصنّعين بدمج العديد من التجميعات في قطع منفردة، مما يُقلّل وقت التجميع وتكاليفه. إضافةً إلى ذلك، تُسهّل الشراكات بين مُصنّعي المعدات الأصلية في قطاع الطيران والفضاء ومتخصصي الطباعة ثلاثية الأبعاد عملية اعتماد وإنتاج المكونات الهيكلية الحيوية، مما يُعزّز هيمنة السوق.

من المتوقع أن يشهد قطاع أدوات التثبيت والتركيب أسرع نمو خلال الفترة من 2026 إلى 2033، مدفوعًا بالحاجة إلى حلول أدوات مخصصة وفعّالة من حيث التكلفة في تجميع وصيانة الطائرات. فعلى سبيل المثال، تستخدم شركة إيرباص أدوات تثبيت وتركيب مطبوعة بتقنية الطباعة ثلاثية الأبعاد لتبسيط خطوط التجميع وتقليل وقت توقف الإنتاج. وتتيح مرونة التصنيع الإضافي إجراء تعديلات سريعة على التصميم وإنتاجًا أسرع للأدوات المتخصصة، مما يُحسّن الكفاءة التشغيلية. كما يُسهم نمو منشآت صناعة الطيران الصغيرة والمتوسطة الحجم التي تستثمر في الطباعة ثلاثية الأبعاد داخليًا في زيادة استخدام أدوات التثبيت والتركيب.

- حسب الاستخدام النهائي

استنادًا إلى الاستخدام النهائي، يُقسّم السوق إلى قطاعي الطائرات والمركبات الفضائية. وقد هيمن قطاع الطائرات على السوق في عام 2025 نظرًا لحجم الإنتاج الكبير للطائرات التجارية والعسكرية، والانتشار الواسع لتقنية الطباعة ثلاثية الأبعاد لتقليل الوزن وخفض التكاليف. تُمكّن تقنية التصنيع الإضافي مُصنّعي الطائرات من إنتاج أجزاء المحركات والمكونات الهيكلية والتجميعات الداخلية بأداء مُحسّن وهدر أقل للمواد. وقد ساهمت الموافقات التنظيمية على المكونات المصنّعة بتقنية الطباعة ثلاثية الأبعاد في الطائرات التجارية في تعزيز تبني هذه التقنية في السوق. كما تُعزز الشراكات بين مُصنّعي المعدات الأصلية في قطاع الطيران وموردي مواد الطباعة ثلاثية الأبعاد موثوقية المكونات والامتثال لمعايير الاعتماد، مما يُرسّخ هيمنتها.

من المتوقع أن يشهد قطاع المركبات الفضائية أسرع نمو له بين عامي 2026 و2033، مدفوعًا بزيادة الاستثمار في إطلاق الأقمار الصناعية، ومهام استكشاف الفضاء، ومشاريع الطيران والفضاء الخاصة. فعلى سبيل المثال، تستفيد شركات مثل سبيس إكس وبلو أوريجين من الطباعة ثلاثية الأبعاد لإنتاج محركات الصواريخ، ومكونات الدفع، وهياكل المركبات الفضائية خفيفة الوزن. وتتيح القدرة على تصنيع أشكال هندسية معقدة يصعب تصنيعها بالطرق التقليدية تحسين كفاءة استهلاك الوقود ومرونة المهام. كما أن التوسع المتزايد في استخدام التصنيع الإضافي في برامج الفضاء الناشئة عالميًا يُسهم في تعزيز نمو السوق في هذا القطاع.

تحليل إقليمي لسوق مواد الطباعة ثلاثية الأبعاد في مجال الطيران

- هيمنت أمريكا الشمالية على سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء، محققةً أكبر حصة من الإيرادات بلغت 40.70% في عام 2025، مدفوعةً بوجود كبرى شركات تصنيع الطيران والفضاء، والاعتماد الكبير لتقنيات التصنيع المتقدمة، والاستثمارات القوية في البحث والتطوير.

- تدمج شركات صناعة الطيران والفضاء في المنطقة بشكل متزايد التصنيع الإضافي لإنتاج مكونات خفيفة الوزن وعالية الأداء للطائرات والمركبات الفضائية

- ويدعم هذا التبني أيضاً بنية تحتية صناعية متينة، وتوافر قوى عاملة ماهرة، وسياسات حكومية مواتية تشجع حلول التصنيع المتقدمة.

نظرة عامة على سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء الأمريكي

استحوذ سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء الأمريكي على الحصة الأكبر من الإيرادات في أمريكا الشمالية عام 2025، مدفوعًا بالانتشار الواسع لاستخدام المعادن ومواد البوليمر عالية الأداء في صناعة الطائرات والمركبات الفضائية. فعلى سبيل المثال، تستخدم شركات مثل بوينغ ولوكهيد مارتن تقنية التصنيع الإضافي لتقليل وزن المكونات، وتحسين كفاءة استهلاك الوقود، وإنتاج أشكال هندسية معقدة يصعب تحقيقها بالطرق التقليدية. كما أن التركيز على خفض التكاليف، وتسريع عملية النماذج الأولية، وتخصيص الأجزاء لتطبيقات الطيران والفضاء العسكرية والتجارية على حد سواء، يدفع نمو السوق. إضافةً إلى ذلك، يُسهم التكامل المتزايد للطباعة ثلاثية الأبعاد مع أدوات التصميم والمحاكاة الرقمية في تعزيز دقة العمليات وموثوقية المكونات.

نظرة عامة على سوق مواد الطباعة ثلاثية الأبعاد في قطاع الطيران والفضاء الأوروبي

The Europe aerospace 3D printing materials market is projected to expand at a substantial CAGR during the forecast period, driven by the region’s emphasis on innovation, sustainable manufacturing, and the production of lightweight aerospace components. Aerospace OEMs and tier-1 suppliers in Germany, France, and Italy are increasingly adopting additive manufacturing for engine parts, structural components, and tooling. The European market is also supported by stringent quality standards, increasing demand for fuel-efficient aircraft, and government initiatives to promote digital manufacturing technologies. The incorporation of 3D printing in both new aircraft programs and retrofitting of existing fleets is further strengthening market growth.

Germany Aerospace 3D Printing Materials Market Insight

The Germany aerospace 3D printing materials market is expected to grow at a significant CAGR, fueled by the country’s strong aerospace industry, technological expertise, and focus on precision engineering. Germany’s aerospace sector is increasingly leveraging additive manufacturing for structural components, engine parts, and jigs & fixtures to reduce weight, enhance performance, and shorten production timelines. The adoption is further supported by collaborations between material suppliers and aerospace manufacturers to develop high-performance metals and polymers suitable for 3D printing. In addition, Germany’s emphasis on sustainability and eco-friendly manufacturing promotes the use of advanced 3D printing materials in aerospace applications.

Asia-Pacific Aerospace 3D Printing Materials Market Insight

The Asia-Pacific aerospace 3D printing materials market is poised to grow at the fastest CAGR during the forecast period, driven by increasing investments in aerospace manufacturing, rapid urbanization, and technological advancements in countries such as China, Japan, and India. The region is witnessing rising adoption of additive manufacturing to produce lightweight and complex components for both commercial and defense aerospace applications. Government initiatives promoting digitalization and smart manufacturing are further supporting market growth. Furthermore, Asia-Pacific is emerging as a key hub for aerospace 3D printing material production, making high-performance metals and polymers more accessible and affordable to local manufacturers.

Japan Aerospace 3D Printing Materials Market Insight

The Japan aerospace 3D printing materials market is gaining momentum due to the country’s high-tech culture, demand for precision manufacturing, and strong aerospace R&D capabilities. Japanese aerospace manufacturers are increasingly using 3D printing to produce lightweight structural components and engine parts that improve fuel efficiency and performance. The integration of additive manufacturing with digital design, simulation, and quality assurance tools is enhancing production accuracy and reducing development cycles. In addition, Japan’s aging workforce and the need for automation in manufacturing processes are driving the adoption of 3D printing solutions for both commercial and defense aerospace applications.

China Aerospace 3D Printing Materials Market Insight

The China aerospace 3D printing materials market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly growing aerospace industry, expanding middle-class demand for air travel, and strong domestic manufacturing capabilities. China is increasingly leveraging additive manufacturing to produce engine components, structural parts, and tooling for commercial aircraft and spacecraft. The push towards smart manufacturing and the availability of cost-effective high-performance 3D printing materials are key factors driving market adoption. Collaboration between local material suppliers, printer manufacturers, and aerospace OEMs further strengthens the ecosystem and supports rapid market growth in China.

Aerospace 3D Printing Materials Market Share

The aerospace 3D printing materials industry is primarily led by well-established companies, including:

- Stratasys Ltd (U.S.)

- 3D Systems, Inc (U.S.)

- ExOne (U.S.)

- EOS GmbH (Germany)

- GENERAL ELECTRIC (U.S.)

- Ultimaker BV (Netherlands)

- Höganäs AB (Sweden)

- Materialise NV (Belgium)

- Solvay (Belgium)

- Sandvik AB (Sweden)

- Arconic (U.S.)

- MTU Aero Engines AG (Germany)

- Moog Inc (U.S.)

- Norsk Titanium AS (Norway)

- Renishaw plc (U.K.)

- SLM Solutions Group AG (Germany)

- Carpenter Technology Corporation (U.S.)

- LPW Technology Ltd (U.K.)

- UBE Industries, Ltd (Japan)

Latest Developments in Global Aerospace 3D Printing Materials Market

- In March 2025, Stratasys launched two new aerospace‑grade validated materials — AIS Antero 800NA and AIS Antero 840CN03 — for its F900 3D printing system, developed in collaboration with leading aerospace and defense manufacturers. These materials are specifically designed to withstand high temperatures, chemical exposure, and mechanical stress, making them suitable for mission-critical aerospace components. The launch enhances material reliability, reduces the cost and time required for part qualification, and accelerates the adoption of additive manufacturing in highly regulated aerospace segments, enabling manufacturers to produce more complex and durable parts for both aircraft and spacecraft

- In March 2024, 3DEO secured an investment from IHI Aerospace Co., Ltd., focusing on integrating its Intelligent Layering metal 3D printing technology into Japan’s precision-oriented aerospace sector. This collaboration aims to combine advanced additive manufacturing capabilities with Japan’s engineering expertise, improving production efficiency and enabling the creation of high-strength, lightweight metal components. The partnership is expected to expand manufacturing opportunities and enhance productivity in Japan and also for North American aerospace operations, strengthening global supply chains and fostering innovation in aerospace material applications

- In November 2023, Markforged introduced the FX10 and Vega 3D printing systems, equipped with dual printhead-mounted optical sensors and an advanced vision module for quality assurance. These systems allow aerospace manufacturers to produce precise, composite-based components that can replace traditional aluminum parts, reducing weight and improving part performance. By integrating enhanced sensing and quality monitoring, the systems streamline production workflows, minimize material waste, and shorten manufacturing timelines, supporting the broader adoption of additive manufacturing across aerospace design and production processes

- In July 2022, The Peekay Group partnered with Bengaluru Airport City Limited to establish a dedicated 3D printing facility focusing on engineering, design, and metal additive manufacturing. This initiative aims to transform the Airport City into a technology and innovation hub, fostering research and development in aerospace materials and component production. The facility is expected to accelerate the development of specialized aerospace-grade metal 3D printing solutions, support prototyping and tooling needs, and expand India’s capabilities in the aerospace additive manufacturing supply chain

- In May 2022, EOS collaborated with Hyperganic to integrate AI-powered algorithmic design software with its laser powder bed fusion 3D printers. This integration allows aerospace engineers to generate complex, optimized designs for propulsion and structural components without relying on conventional part design methods. By automating design processes and enabling more efficient use of advanced materials, the collaboration enhances manufacturing flexibility, reduces development cycles, and supports the production of high-performance, lightweight aerospace parts, further driving additive manufacturing adoption in critical aerospace applications

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.