Global Cheese Culture Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

1.27 Billion

USD

2.02 Billion

2025

2033

USD

1.27 Billion

USD

2.02 Billion

2025

2033

| 2026 –2033 | |

| USD 1.27 Billion | |

| USD 2.02 Billion | |

| % | |

|

Global Cheese Culture Market Segmentation, By Product (Cheddar, Continental, Pasta Filata/Mozzarella, Cottage, Propionic, Soft, Grana, and White Brined), Type (Mesophilic Culture, Thermophilic Culture, Starter Culture, Non Starter Culture, and Probiotics), Category (Fresh Cheese, Soft Cheese, and Hard Cheese), Cultures (Ripening, Protective Cultures, and Kosher), Application (Strains and Cultures Compounding), Sales Channel (Specialty Store, Direct Store, Third Party Online, and Other Sales Channel) - Industry Trends and Forecast to 2033

What is the Global Cheese Culture Market Size and Growth Rate?

- The global cheese culture market size was valued at USD 1.27 billion in 2025 and is expected to reach USD 2.02 billion by 2033, at a CAGR of 6.00% during the forecast period

- The surging consumption of ready-to-eat food and savoury snacks products especially among the working population is major factor contributing for growth in market

- The increasing awareness amongst health-conscious customers regarding various functionalities and the short and long-term health benefits to the overall wellness of cheese culture as good bacteria known as probiotics helps in restoring gut health and has various digestive enzymes is estimated to contribute to growth of the cheese culture market

What are the Major Takeaways of Cheese Culture Market?

- The easy availability of cheese cultures in both smooth and consistent form is expected to heighten demand for the cheese culture market

- However, the cheese is a major source of saturated fat which raises harmful LDL cholesterol, thus increasing possibilities of heart disease which is projected to act as a restraint, whereas the surging lactose intolerant people across the globe is projected to challenge the growth of the cheese culture market

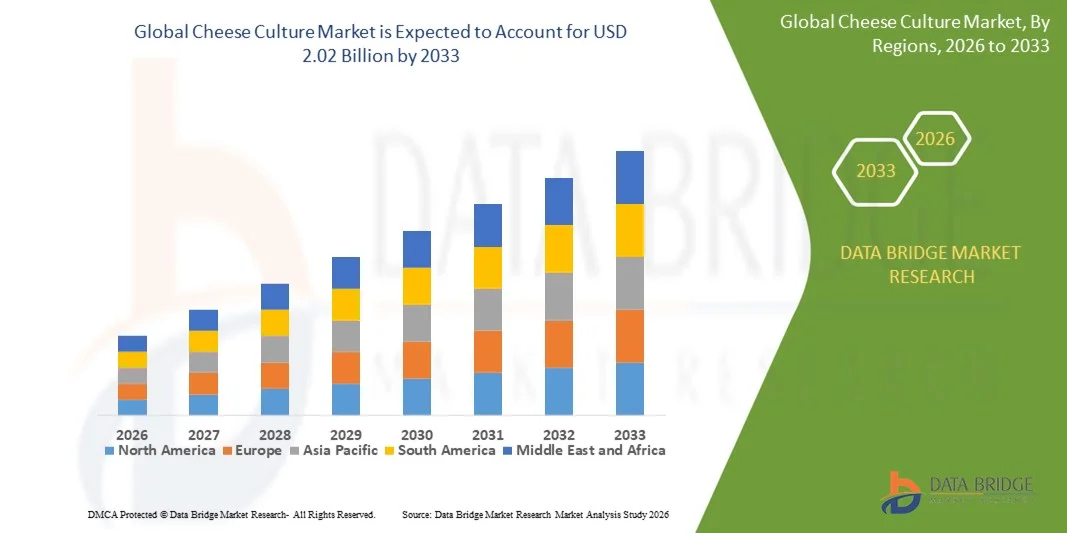

- North America dominated the cheese culture market with a revenue share of 41.23% in 2025, driven by high cheese consumption, advanced dairy processing infrastructure, and strong presence of industrial cheese manufacturers across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.42% from 2026 to 2033, driven by rapidly rising cheese consumption, westernization of diets, expanding foodservice chains, and growing dairy processing capacity across China, India, Japan, South Korea, and Southeast Asia

- The pasta filata/mozzarella segment dominated the market with a 31.6% share in 2025, driven by its extensive use in pizza, fast food, and ready-to-eat meals globally

Report Scope and Cheese Culture Market Segmentation

|

Attributes |

Cheese Culture Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Cheese Culture Market?

Rising Demand for Specialized and Clean-Label Cheese Cultures

- The cheese cultures market is witnessing growing adoption of specialized starter and adjunct cultures designed to enhance flavor, texture, ripening control, and consistency across industrial and artisanal cheese production

- Manufacturers are increasingly developing strain-specific, region-tailored, and application-focused cultures to support diverse cheese varieties such as cheddar, mozzarella, feta, parmesan, and specialty cheeses

- Growing consumer preference for clean-label, natural, and minimally processed dairy products is driving demand for cultures with reduced additives and non-GMO formulations

- For instance, companies such as Chr. Hansen, DSM-Firmenich, Lallemand, and BIOPROX are expanding portfolios of mesophilic, thermophilic, and probiotic cheese cultures to meet evolving taste and functionality requirements

- Increased focus on texture optimization, shelf-life extension, and fermentation efficiency is accelerating the adoption of advanced culture blends

- As global cheese consumption rises and product differentiation becomes critical, cheese cultures are emerging as a core innovation driver in dairy processing

What are the Key Drivers of Cheese Culture Market?

- Rising global demand for cheese and fermented dairy products, supported by urbanization, westernized diets, and growing protein consumption

- For instance, in 2024–2025, companies such as DSM-Firmenich and Chr. Hansen introduced enhanced cultures enabling faster fermentation, consistent yields, and improved flavor development

- Expansion of industrial cheese manufacturing, quick-service restaurants, and ready-to-eat food products is increasing large-scale culture adoption

- Growing popularity of artisanal, specialty, and premium cheeses is driving demand for customized and region-specific culture strains

- Increasing focus on food safety, batch consistency, and production efficiency is encouraging dairy processors to adopt standardized, high-performance cultures

- Supported by innovation in microbial science and fermentation technology, the Cheese Cultures market is expected to witness steady long-term growth

Which Factor is Challenging the Growth of the Cheese Culture Market?

- High costs of specialized and proprietary culture strains limit adoption among small-scale and artisanal cheese producers

- For instance, premium cultures offering extended shelf life or accelerated ripening often require higher upfront investment and controlled storage conditions

- Sensitivity of cultures to temperature, handling, and storage increases logistics and cold-chain dependency

- Regulatory approval requirements and labeling compliance for microbial cultures vary across regions, increasing time-to-market complexity

- Limited technical expertise among small producers regarding culture selection and fermentation optimization can impact performance outcomes

- Despite these challenges, ongoing efforts in cost optimization, technical support, and culture standardization are expected to improve accessibility and adoption of cheese cultures globally

How is the Cheese Culture Market Segmented?

The market is segmented on the basis of product, type, category, cultures, application, and sales channel.

- By Product

On the basis of product, the cheese culture market is segmented into cheddar, continental, pasta filata/mozzarella, cottage, propionic, soft, grana, and white brined cheeses. The pasta filata/mozzarella segment dominated the market with a 31.6% share in 2025, driven by its extensive use in pizza, fast food, and ready-to-eat meals globally. Rising demand from QSR chains and frozen food manufacturers has significantly boosted culture consumption for mozzarella production. Cultures used in this segment focus on stretchability, melt behavior, and consistent texture.

The grana cheese segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by increasing consumption of premium aged cheeses such as parmesan and grana padano. Longer ripening cycles and strict quality requirements are driving demand for advanced ripening cultures that enhance flavor development, yield stability, and maturation efficiency.

- By Type

On the basis of type, the market is segmented into mesophilic culture, thermophilic culture, starter culture, non-starter culture, and probiotics. The starter culture segment dominated the market with a 42.3% share in 2025, as starter cultures form the foundation of cheese fermentation by controlling acidification, texture formation, and flavor consistency. They are widely used across industrial and artisanal cheese production due to reliability and standardized performance.

The probiotics segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising consumer interest in functional foods and gut-health-enhancing dairy products. Incorporation of probiotic strains in cheese offers health benefits while maintaining taste and shelf life, making them increasingly attractive to premium and health-focused cheese brands.

- By Category

On the basis of category, the cheese culture market is segmented into fresh cheese, soft cheese, and hard cheese. The fresh cheese segment held the largest market share of 38.9% in 2025, attributed to high consumption of products such as cottage cheese, cream cheese, and ricotta. Short fermentation cycles, high production volumes, and growing demand for high-protein fresh dairy products are supporting culture demand in this segment.

The hard cheese segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing popularity of aged and premium cheeses. Hard cheese production requires precise culture formulations for controlled ripening, flavor depth, and texture development, increasing demand for advanced and strain-specific cultures.

- By Cultures

On the basis of cultures, the market is segmented into ripening cultures, protective cultures, and kosher cultures. The ripening cultures segment dominated the market with a 45.1% share in 2025, as these cultures play a critical role in developing flavor, aroma, and texture during cheese maturation. They are extensively used in semi-hard and hard cheeses where aging is essential.

The protective cultures segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing focus on natural preservation and clean-label cheese production. Protective cultures inhibit spoilage organisms and pathogens, helping manufacturers extend shelf life while reducing reliance on chemical preservatives.

- By Application

On the basis of application, the cheese culture market is segmented into strains and cultures compounding. The cultures compounding segment dominated the market with a 100% functional share in 2025, as compounding enables customization of multiple strains to achieve desired fermentation behavior, flavor profiles, and textural outcomes. Dairy processors increasingly rely on compounded cultures to meet product differentiation and batch consistency requirements.

The same segment is also expected to grow steadily at a high CAGR from 2026 to 2033, supported by growing demand for tailor-made culture solutions across industrial, artisanal, and specialty cheese producers.

- By Sales Channel

On the basis of sales channel, the market is segmented into specialty stores, direct store, third-party online, and other sales channels. The direct store segment dominated the market with a 41.7% share in 2025, driven by long-term supply contracts between culture manufacturers and large dairy processors. Direct sales ensure technical support, consistent supply, and customized culture solutions.

The third-party online segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by rising adoption among small-scale, artisanal, and home cheesemakers. Increased availability of cultures through e-commerce platforms and global distribution networks is expanding accessibility and market reach.

Which Region Holds the Largest Share of the Cheese Culture Market?

- North America dominated the cheese culture market with a revenue share of 41.23% in 2025, driven by high cheese consumption, advanced dairy processing infrastructure, and strong presence of industrial cheese manufacturers across the U.S. and Canada. Widespread adoption of standardized starter and adjunct cultures supports consistent quality, large-scale production, and regulatory compliance across the region

- Leading culture producers are continuously introducing advanced strains for improved flavor development, texture control, yield optimization, and shelf-life extension, strengthening North America’s technological leadership

- Strong R&D ecosystems, high consumer demand for natural and clean-label cheese products, and sustained investments in dairy innovation further reinforce the region’s market dominance

U.S. Cheese Culture Market Insight

The U.S. is the largest contributor in North America, supported by high consumption of mozzarella, cheddar, and specialty cheeses, along with a well-established dairy processing industry. Rising demand from quick-service restaurants, packaged food manufacturers, and retail cheese brands is increasing adoption of customized starter, ripening, and protective cultures. Strong presence of global culture suppliers, advanced cold-chain logistics, and continuous innovation in probiotic and clean-label cheese products further drive market growth

Canada Cheese Culture Market Insight

Canada contributes significantly to regional growth, driven by steady demand for natural and specialty cheeses, strong dairy cooperatives, and regulated milk production systems. Increasing focus on quality consistency, extended shelf life, and sustainable dairy processing is supporting adoption of advanced cheese cultures. Government-backed food safety regulations and innovation programs further strengthen market expansion.

Asia-Pacific Cheese Culture Market

Asia-Pacific is projected to register the fastest CAGR of 7.42% from 2026 to 2033, driven by rapidly rising cheese consumption, westernization of diets, expanding foodservice chains, and growing dairy processing capacity across China, India, Japan, South Korea, and Southeast Asia. Increasing adoption of mozzarella and processed cheese in pizzas, bakery products, and ready-to-eat foods is fueling demand for starter and thermophilic cultures. Expansion of local cheese manufacturing facilities, rising disposable income, and growing awareness of functional and probiotic dairy products are accelerating market growth across the region.

China Cheese Culture Market Insight

China is the largest contributor in Asia-Pacific due to rapid growth in processed food consumption, expanding domestic cheese production, and strong investment in modern dairy infrastructure. Increasing use of cultures for mozzarella, cream cheese, and processed cheese applications is driving market adoption.

Japan Cheese Culture Market Insight

Japan shows steady growth supported by demand for premium, high-quality cheeses and strict food safety standards. Advanced fermentation expertise and preference for consistent flavor profiles drive adoption of specialized and ripening cultures.

India Cheese Culture Market Insight

India is emerging as a high-growth market, driven by rapid expansion of pizza chains, bakery applications, and packaged cheese products. Growing investments in dairy processing and rising demand for cost-efficient starter cultures are accelerating adoption.

South Korea Cheese Culture Market Insight

South Korea contributes strongly due to increasing consumption of processed and western-style cheeses, growth in convenience foods, and strong emphasis on food quality and safety. Rising demand for functional and probiotic cheese products supports continued market expansion.

Which are the Top Companies in Cheese Culture Market?

The cheese culture industry is primarily led by well-established companies, including:

- Cultures For Health (U.S.)

- Chr. Hansen Holding A/S (Denmark)

- Home Make It (U.S.)

- New England Cheesemaking Supply Company (U.S.)

- GEA Group Aktiengesellschaft (Germany)

- DSM (Netherlands)

- Dairy Connection, Inc. (U.S.)

- BIOPROX (France)

- Hjemmeriet (Denmark)

- Lallemand Inc. (Canada)

- Vivolac (U.S.)

- Mooreland Cheesemaking LTD (U.K.)

- Biena Snacks (U.S.)

- Make Cheese Inc. (U.S.)

- KPM Analytics (U.S.)

- Posh Flavours (India)

- Siemens (Germany)

- Benny Impex (India)

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.