Global Endocrinology Biosimilars Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

297.00 Million

USD

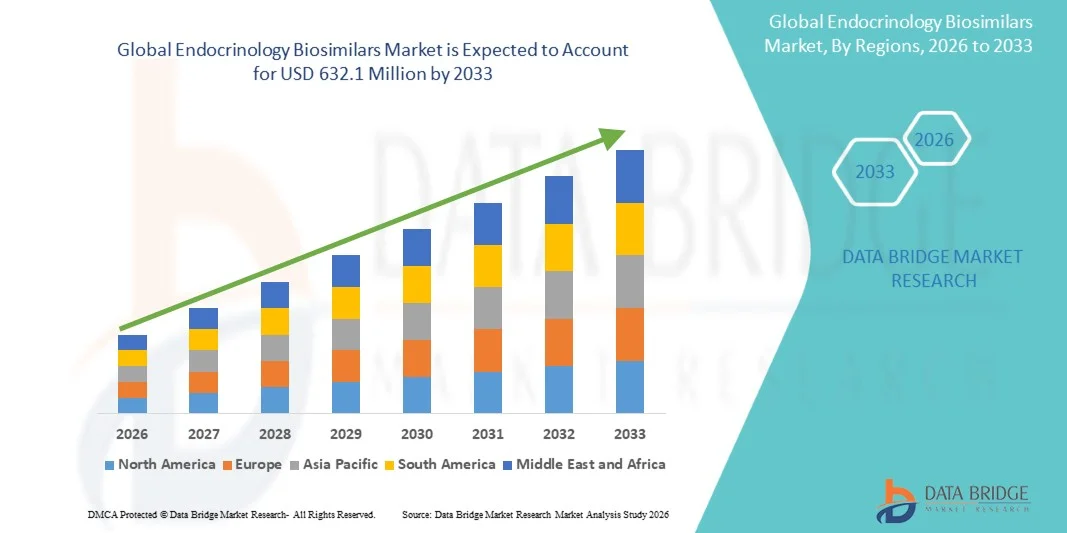

632.10 Million

2025

2033

USD

297.00 Million

USD

632.10 Million

2025

2033

| 2026 –2033 | |

| USD 297.00 Million | |

| USD 632.10 Million | |

| % | |

|

تصنيف الأسواق، حسب نوع المنتج (الانسولين البيولوجيا المتماثلة والنمو هرمون البيولوجي المشابه)، والتلميع (إدارة مرض السكري وعجز هرمون النمو) - اتجاهات الصناعة والتنبؤات حتى عام 2033

ما هو حجم ومعدل النمو في سوق علم الغدد الصماء؟

- وفقاً لتحليل بحوث سوق سوق جسر البيانات، قُيِّر حجم السوق العالمية لمشابس أحجام أحيائياً297 مليون دولار من دولارات الولايات المتحدة في عام 2025ومن المتوقع أن يتم ذلك63/21 مليون بحلول عام 2033, ما(ج أ أ أ أ أ أ أخلال الفترة التي

- ومما يغذي نمو السوق إلى حد كبير تزايد انتشار اضطرابات الغدد الصماء، وارتفاع الطلب على العلاجات البيولوجية الميسورة التكلفة، وهجرات البراءات للعديد من البيولوجيا المنشئة، مما يؤدي إلى اعتماد أشكال مماثلة أحيائية على نطاق أوسع في علاج السكري، وهرمونات النمو، وغيرها من علاجات الغدد الصماء.

- وبالإضافة إلى ذلك، فإن تزايد الوعي بين مقدمي الرعاية الصحية والمرضى، وسياسات السداد المواتية، واللوائح الحكومية الداعمة، تعجل باستيعاب حلول حلول البيولوجيا المتماثلة في علم الغدد الصماء، مما يؤدي إلى زيادة كبيرة في نمو الصناعة.

سوق الحجم و توقّر

- قيمة السوق العالميةالمصدر المصدر

- القيمة السوقية المتوقعة (2033)(أ) المصدر: الولايات المتحدة

- )٢٠٢٦-٢٠٣٣(: 9.90%

تحليل أسواق

- إن البيولوجيا الأحيائية المتشابهة في الغدة الصماء، بما في ذلك علاجات السكري، ونقص نمو هرمونات النمو، وغير ذلك من اضطرابات الغدد الصماء، تشكل بصورة متزايدة عناصر حيوية في الرعاية الصحية الحديثة نظراً لفعالية تكلفتها، وكفاءة مماثلة للبيولوجيا المنشئة، والتبني المتزايد بين الأطباء والمرضى.

- ويؤجّي الطلب المتزايد على البيولوجيا المتماثلة في علم الغدد الصماء أساساً بسبب ارتفاع انتشار اضطرابات الغدد الصم، وهجرات براءات الاختراع للعديد من البيولوجيا المنشئة، وتزايد الوعي بين مقدمي الرعاية الصحية، والسياسات الداعمة للحكومة والدفعة التي تشجع على الاعتماد البيولوجي المتماثل.

- وتهيمن أمريكا الشمالية على سوق بيولوجيا علم الغدة الصماء، مع أكبر حصة من الإيرادات تبلغ نحو 38.6 في المائة في عام 2025، مدفوعة بالهياكل الأساسية القوية للرعاية الصحية، وارتفاع معدلات اعتماد المتشابهات البيولوجية، وسياسات سداد التكاليف الراسخة، ووجود قوي للجهات الفاعلة الرئيسية في الصناعة، لا سيما في الولايات المتحدة، حيث يؤدي الاعتماد المبكر والوعي المبكران إلى تغذية نمو السوق

- ومن المتوقع أن تكون منطقة آسيا والمحيط الهادئ أسرع المناطق نمواً في سوق بيولوجيا المتماثلات في علم الغدد الصماء خلال الفترة المتوقعة، حيث تسجل معدلاً قوياً لسجلات الدخل الإجمالي الإجمالية البالغة 10.2 في المائة، مدعوماً بزيادة انتشار اضطرابات الغدد الصماء، وزيادة فرص الحصول على الرعاية الصحية، وتحسين سياسات سداد التكاليف، وتوسيع نطاق القدرات المحلية في مجال تصنيع المستحضرات الصيدلانية في بلدان مثل الهند والصين واليابان.

- وسيطر الجزء المتعلق بمعالجة مرض السكري على أكبر حصة من إيرادات السوق بلغت 65 في المائة في عام 2025، وذلك بسبب ارتفاع معدل انتشار السكري من النوع 1 والنوع 2 في جميع أنحاء العالم، وارتفاع عدد السكان المسنين، وزيادة المبادرات الحكومية الرامية إلى تحسين إمكانية الحصول على العلاجات الأنسولين الفعالة من حيث التكلفة.

تقرير عن النطاق والجليـد

|

الصفات الأولى |

(أ) الأسواق الرئيسية |

|

المُسَجَّل |

|

|

البلدان |

أمريكا الشمالية

أوروبا

منطقة آسيا والمحيط الهادئ

الشرق الأوسط وأفريقيا

جنوب أمريكا الجنوبية

|

|

& مفتاح |

|

|

ما |

|

|

جاري |

وبالإضافة إلى الرؤى المتعلقة بسيناريوهات السوق مثل القيمة السوقية، ومعدل النمو، والتجزئة، والتغطية الجغرافية، واللاعبين الرئيسيين، فإن تقارير السوق التي تُقيِّمها بحوث سوق جسر البيانات تشمل أيضاً تحليلاً متعمقاً للخبراء، وعلم وبائيات المرضى، وتحليل خطوط الأنابيب، وتحليل الأسعار، والإطار التنظيمي. |

ما هو الاتجاه الرئيسي في سوق علم الغدد الصماء البيولوجي المتماثل؟

"التقدم المحرز في مجال علم"

- ومن الاتجاهات الهامة والمتسارعة في السوق العالمية للبيولوجيا المتشابهة في علم الغدد الصماء التطور المتزايد واعتماد الجيل المقبل من العلاجات البيولوجية المتماثلة في الجيل المقبل لعلاج اضطرابات الغدد الصماء المزمنة مثل السكري، وقصور نمو الهرمونات، واضطرابات الغدة الدرقية. إن الابتكارات في تقنيات التصنيع، واستقرار التركيب، والموافقة التنظيمية تعمل على تعزيز إمكانية الوصول والقدرة على تحمل التكاليف، مما يجعل هذه العلاجات أكثر جاذبية لمقدمي الرعاية الصحية والمرضى على حد سواء.

- على سبيل المثال، تعمل شركات صيدلانية مثل ساندوز وبيوكون بنشاط على تطوير نسخ مماثلة أحيائية من أشكال تناظريات الانسولين الراسخة وهرمونات النمو المتآزرة مع تحسين الاستقرار وامتثال المرضى. وتعمل هذه التطورات على تيسير الاعتماد على نطاق أوسع في الأسواق المتقدمة والناشئة على حد سواء، وخاصة في أميركا الشمالية وأوروبا وآسيا والمحيط الهادئ، حيث يتزايد الطلب على علاجات الغدد الصماء الفعالة من حيث التكلفة.

- فأوجه التقدم في تكنولوجيا التركيب، بما في ذلك التناظرات الطويلة المفعول للإنسولين والأجهزة الجاهزة للاستخدام بالحقن، تتيح تحسين دقة الجرعة، وخفض تواتر الإدارة، وتعزيز تقيد المرضى. فعلى سبيل المثال، توفر الآن عدة منتجات حديثة العهد في مجال الانسولين، نظم إيصال قائمة على القِلة، تبسّط الإدارة المنزلية وتحد من القلق المتصل بالحقن بين المرضى، ولا سيما في أوساط الأطفال والمسنين.

- إن التكامل المتزايد بين برامج مراقبة مراقبة صيدليات الصيدلة وما بعد التسويق يعمل على تعزيز رصد السلامة لمشابهات أحيائيات علم الغدد الصماء، وتزويد الأطباء بدليل حقيقي على الفعالية والأحداث المعاكسة. وهذا ييسر اتخاذ قرارات علاجية مستنيرة، ويعزز الثقة فيما بين المهنيين العاملين في مجال الرعاية الصحية، ويشجع على استيعاب العلاجات المتماثلة أحيائياً على نطاق أوسع.

- وهذه التطورات هي إعادة تشكيل نماذج العلاج في الغدد الصماء من خلال توفير بدائل ميسورة التكلفة وفعالة وقابلة للمقارنة سريرياً للبيولوجيا المنشئة، مما يؤدي في نهاية المطاف إلى توسيع فرص الحصول على العلاجات المنقذة للحياة لعدد أكبر من السكان المرضى عبر الأسواق العالمية.

- ولا يزال الطلب على البيولوجيا المتماثلة في علم الغدد الصماء يتزايد بسبب ارتفاع انتشار اضطرابات الغدد الصم المزمنة، وزيادة الإنفاق على الرعاية الصحية، والسياسات الحكومية الداعمة التي تهدف إلى خفض تكاليف العلاج وتحسين سبل حصول المرضى على العلاج.

(أ)

سائق

" تزايد معدلات اضطرابات الغدد الصم وتجمع المرضى المتزايدين "

- وتؤدي الزيادة العالمية في السكري، ونقص نمو الهرمونات، والاضطرابات المتصلة بالغدة الدرقية، إلى دفع الطلب على خيارات علاجية فعالة من حيث التكلفة، مما يجعل من البيولوجيا المتشابهة في الغدد الصماء بديلا مفضلا عن البيولوجيا المنشئة المكلفة

- فعلى سبيل المثال، أبلغ الاتحاد الدولي لمرضى السكري عن ارتفاع كبير في معدل انتشار السكري من النوع 2، ولا سيما في آسيا والمحيط الهادئ وأمريكا الشمالية، وشجع نظم الرعاية الصحية على اعتماد علاجات إنسولين متماثلة أحيائياً لتحسين القدرة على تحمل التكاليف والتغطية بالمرضى.

- وبالإضافة إلى ذلك، يساهم شيخوخة السكان وارتفاع معدلات البدانة في زيادة عدد المرضى الذين يتطلبون تدخلات في الغدد الصماء، مما يزيد من دفع نمو الأسواق إلى الأمام.

- وعلاوة على ذلك، فإن إدخال أجهزة إيصال ملائمة للمريض، مثل الأقلام المعبأة مسبقا، والمحاقن الذاتية، ومضخات الأنسولين المحمولة المتوافقة مع المشابهات البيولوجية، يزيد من الالتزام بالمعالجة ورضاها، ولا سيما بين الأطفال والمراهقين والمسنين.

- كما أن مبادرات الرعاية الصحية وسياسات التغطية التأمينية التي تشجع البدائل البيولوجية البيولوجية الفعالة من حيث التكلفة تشجع الأطباء والمستشفيات على إدماج المتماثلات البيولوجية في بروتوكولات العلاج الموحدة، مما يعزز اختراق السوق.

التعرّض/التحديي

"المُعقد التنظيمي والتكاليف الإنمائية المرتفعة"

- إن المتطلبات التنظيمية المعقدة والصرامة نسبياً للموافقة على البيولوجيا المتماثلة في علم الغدد الصماء تشكل تحدياً كبيراً أمام دخول الأسواق. ويتعين على الصانعين أن يبرهنوا على التماثل الأحيائي من حيث الفعالية والسلامة والانتقائية مقارنة بالبيولوجيا المرجعية، وهو ما يتطلب تجارب ووثائق سريرية واسعة النطاق.

- فعلى سبيل المثال، تتطلب مسارات الموافقة المتماثلة أحيائياً التي حددتها هيئة التنمية الحرجية في الولايات المتحدة وهيئة تقييم البيئة في الولايات المتحدة إجراء دراسات سريرية مقارنة وصيدلية وصيدلية وصيدلية وصيدلية دقيقة، مما يؤدي إلى ارتفاع تكاليف التنمية وطول الوقت إلى الأسواق للمنتجات الجديدة.

- وعلاوة على ذلك، فإن تردد الأطباء وشواغل المرضى بشأن قابلية تبادل المشابكات البيولوجية وسلامتها على المدى الطويل يمكن أن تحد من الاعتماد، لا سيما في الأسواق التي أسست فيها البيولوجيا المنشئة الثقة.

- ويمكن أن يؤدي ارتفاع تكلفة الإنتاج لبعض الجزيئات البيولوجية المتشابهة، بالاقتران مع التحديات في مجال اللوجستيات والتخزين والتوزيع في سلسلة التبريد، إلى الحد من توافر الموارد في الاقتصادات الناشئة، مما يؤدي إلى تباطؤ دخول الأسواق.

- والتغلب على هذه التحديات من خلال المواءمة التنظيمية، وبرامج التوعية المعززة، وتقنيات التصنيع التي تتسم بكفاءة التكلفة، والشراكات التعاونية بين المصنعين المبتكرين والمصنعين البيولوجيين المتماثلين، سيكون عاملاً حاسماً في نمو السوق المطرد في قطاع مُشابهات علم الغدد الصماء

(ج)

وتقسم السوق على أساس نوع المنتج والإشارة إليه.

• حسب نوع المنتج

واستناداً إلى نوع المنتج، فإن سوق بيولوجيا الانكلونكس تتجزأ إلى سوق Insulin Biosimilates و Hormone Biosimilates، ويهيمن قطاع الانسولين البيولوجي على أكبر حصة من إيرادات السوق قدرها 61 في المائة في عام 2025، مدفوعة بتزايد انتشار السكري على الصعيد العالمي، وزيادة اعتماد علاجات الانسولين الفعالة من حيث التكلفة، ودعم السداد في كل من البلدان المتقدمة والناشئة، ويستفيد هذا القطاع من القبول السريري القوي، وخطوط الأنابيب التحويلية الواسعة النطاق، والمعرفة المرضى بنظام الانسولين. وتشجع الحكومات وأرباب مدفوعات الرعاية الصحية على الاعتماد الأحيائي المتماثل للحد من تكاليف العلاج، في حين تفضل المستشفيات والعيادات المشابهات الأحيائية بالليزر بسبب سهولة التخزين والإدارة. كما أن الابتكار المستمر في تركيبات المعالجة الطويلة المفعول والسريعة النشاط في مجال التزليق يزيد من تعزيز قيادة السوق، وخاصة في أمريكا الشمالية وأوروبا.

ومن المتوقع أن يشهد قطاع هرمون الأحيائي المشابه للنمو أسرع مستويات النمو في الجمهورية التشيكية حيث بلغ 14.3 في المائة من عام 2026 إلى عام 2033، وهو ما يغذيه الوعي بالمعالجة الناجمة عن نقص هرمونات النمو لدى الأطفال والبالغين، وزيادة معدلات التشخيص، وتحسين الوصول من خلال برامج الرعاية الصحية الحكومية والخاصة. وتطلق شركات صناعة الأدوية الجيل القادم من المشابهات البيولوجية مع تحسين الفعالية، وموجزات السلامة، وأجهزة الإيصال، الأمر الذي يعجل من عملية الاعتماد. ويساهم التوسع في مراكز أمراض الغدد الصماء لدى الأطفال وإدارة هرمونات النمو في الرعاية المنزلية أيضاً في النمو السريع للأسواق على مستوى العالم. ومن المتوقع أن تدفع الأسواق الناشئة في آسيا والمحيط الهادئ وأمريكا اللاتينية جزءاً كبيراً من هذا السجل.

• بالزك

وعلى أساس الإشارة إلى ذلك، فإن سوق بيولوجيا الغدد الصماء مقسمة إلى سوق لإدارة مرض السكر ومرض هرمون النمو، وسيطر قسم إدارة مرض السكر على أكبر حصة من إيرادات السوق بلغت 65 في المائة في عام 2025، وذلك بسبب ارتفاع معدل انتشار مرض السكري من النوع 1 والنوع 2 في جميع أنحاء العالم، وارتفاع أعداد المسنين، وزيادة المبادرات الحكومية الرامية إلى تحسين فرص الحصول على علاجات الانسولين الفعالة من حيث التكلفة، ويشمل هذا الجزء كلا من مشابهات إنسولين حيوية ذات تأثير طويل وسريع تستخدم على نطاق واسع في المستشفيات والعيادات والرعاية المنزلية، مع اتباع سياسات ملائمة لسداد التكاليف تدعم التبني والحاجة إلى رصد مراقبة الجسيليات بصورة متكررة وزيادة الوعي بالمضاعفات المتعلقة بمرض السكري مما يدعم الطلب المرتفع على بيولوجيا الأنسولين على الصعيد العالمي.

ومن المتوقع أن يشهد الجزء الخاص بنقص هرمون النمو أسرع نمو في معدل النمو العام، حيث بلغ 13.8 في المائة من 2026 إلى 2033، مدفوعاً بزيادة تشخيص نقص المناعة البشرية العالمي، والتوسع في اعتماد العلاجات المتماثلة أحيائياً، والتقدم التكنولوجي في نظم إيصال الأدوية مثل الأقلام المملوءة مسبقاً والحقن الذاتية. وتوسعت عيادات طب الأطفال وأمراض الغدد الصماء للكبار على الصعيد العالمي، مما أتاح إمكانية أفضل للحصول على العلاجات. كما أن إطلاق المشابهات البيولوجية الفعالة من حيث التكلفة مقارنة بهرمونات النمو الناشئة يزيد من دعم استيعابها في الاقتصادات الناشئة. وعلاوة على ذلك، فإن ارتفاع حملات التوعية وتعزيز تغطية التأمين الصحي يعملان على تسريع توسع الأسواق.

تحليل إقليمي

- وتهيمن أمريكا الشمالية على سوق المشابهات البيولوجية لعلوم الغدد الصماء، حيث بلغت حصة الإيرادات الأكبر نحو 38.6 في المائة في عام 2025.

- مدفوعة بالهياكل الأساسية القوية للرعاية الصحية، وارتفاع معدلات اعتماد المتشابهات البيولوجية، وسياسات سداد راسخة جيدا، ووجود قوي للاعبي الصناعة الرئيسيين، لا سيما في الولايات المتحدة، حيث يؤدي الاعتماد المبكر والوعي المبكران إلى تغذية نمو السوق

- وتشهد السوق استيعاباً كبيراً للمشابهات البيولوجية عبر علاجات أمراض الغدد الصماء مثل السكري، ونقص هرمونات النمو، واضطرابات الغدة الدرقية، مدعومة بقبول سريري قوي وزيادة وعي المرضى

سوق الولايات المتحدة الأمريكية

إن سوق الولايات المتحدة للمشابهات البيولوجية في علم الغدد الدرقية استولت على أغلبية إيرادات أميركا الشمالية، التي يغذيها الاعتماد السريع للمشابهات البيولوجية في المستشفيات وخارجها على حد سواء. والواقع أن عوامل مثل تثقيف الأطباء الاستباقيين، وحملات توعية المرضى، وسياسات السداد المواتية تدفع النمو عبر قطاعات السكري، وهرمونات النمو، وعلاج الغدة الدرقية.

أوروبا أوروبا

ومن المتوقع أن تتوسع سوق أوروبا للبيولوجيا المتماثلة في الغدد الصماء في ظل معدل كبير من النمو العالمي خلال الفترة المتوقعة، وذلك بسبب تزايد تبني المتماثلات البيولوجية عبر علاجات الغدد الصماء، والأنظمة الحكومية الداعمة، وارتفاع الإنفاق على الرعاية الصحية. وتشهد بلدان مثل ألمانيا، والمملكة المتحدة، وفرنسا نمواً بسبب البنية الأساسية الراسخة للرعاية الصحية ووجود شركات تصنيع رئيسية مماثلة للبيولوجيا.

المملكة المتحدة

ومن المتوقع أن تنمو سوق الولايات المتحدة الأمريكية للمشابهات البيولوجية في الغدد الصماء خلال الفترة المتوقعة، مدعومة بأطر سداد مواتية، وزيادة وعي الأطباء، والمبادرات الحكومية التي تشجع العلاجات الفعالة من حيث التكلفة.

ألمانيا ألمانيا

ومن المتوقع أن تنمو سوق ألمانيا للبيولوجيا التماثلية في الغدد الصماء بمعدل كبير خلال الفترة المتوقعة، بفضل زيادة اعتماد المشابهات البيولوجية، ونظم الرعاية الصحية المتطورة، والمبادرات الرامية إلى خفض تكاليف العلاج.

منظمة التعاون والتنمية في الميدان الاقتصادي

ومن المتوقع أن تكون سوق بيولوجيا الغدد الصماء في آسيا والمحيط الهادئ أسرع المناطق نمواً في سوق بيولوجيا الاند الصماء خلال الفترة المتوقعة، حيث سجلت معدلاً قوياً لمعدلات الخصوبة الإجمالية يبلغ نحو 10.2 في المائة، مدعوماً بزيادة انتشار اضطرابات الغدد الصماء، وزيادة فرص الحصول على الرعاية الصحية، وتحسين سياسات سداد التكاليف، وتوسيع نطاق القدرات المحلية في مجال تصنيع المستحضرات الصيدلانية في بلدان مثل الهند والصين واليابان. كما يشكل النمو السريع في البنية الأساسية للمستشفيات والوعي بشأن المتماثلات البيولوجية بين الأطباء والمرضى عوامل رئيسية تدفع الطلب الإقليمي.

اليابان (بآلاف دولارات الولايات المتحدة)

الواقع أن سوق اليابان لعلوم الغدد الصماء البيولوجية المتماثلة تكتسب قوة جريئة بسبب تزايد تبني المشابهات البيولوجية للسكري، ونقص نمو الهرمونات، واضطرابات الغدة الدرقية. والواقع أن سياسات الرعاية الصحية الداعمة، والوعي العالي بالمريضين، والتقدم التكنولوجي في تصنيع المستحضرات الصيدلانية تعمل على تغذية نمو السوق.

منظمة التعاون والتنمية

كانت سوق الصين للبيولوجيا المتماثلة في الغدد الصماء تشكل أكبر حصة من الإيرادات في آسيا والمحيط الهادئ في عام 2025، وذلك بفضل توسيع البنية الأساسية للرعاية الصحية، وارتفاع انتشار اضطرابات الغدد الصماء، وزيادة تركيز الحكومة على العلاجات الفعالة من حيث التكاليف، والقدرات المحلية القوية في مجال التصنيع الصيدلاني. ويشكل الوعي المتنامي في الصين بالمشابهات البيولوجية وزيادة الموافقات على علاجات الغدد الصماء عاملين رئيسيين في دفع السوق.

الإقليم الذي يحمل أكبر حصة من سوق علم البيئة والبيولوجيا؟

وتقود صناعة علم الغدد الصماء البيولوجي المتماثلة في المقام الأول شركات راسخة، من بينها:

- BC BC (الهند)

- (الولايات المتحدة الأمريكية)

- Amgen (الولايات المتحدة الأمريكية)

- سامسونغ بيوبيبيس (كوريا الجنوبية)

- الرعاية الصحية في الخلايا (كوريا الجنوبية)

- Teva Ad الصيدليات (إسرائيل)

- Stada Arzneimittel (ألمانيا)

- فريسينيوس كابي (ألمانيا)

- هيترو بيافرار (الهند)

- مختبرات الدكتور ريدي (الهند)

- تكافل العلوم البيولوجية (الولايات المتحدة الأمريكية)

- الصيدلاعيات (الهند)

- نوفارتيس (سويسرا)

- (الولايات المتحدة الأمريكية)

- أُبفي (الولايات المتحدة الأمريكية)

- جينور بيافار (الصين)

- Hsoh Hoh Rochsedal (الصين)

التطورات في السوق العالمية لسجلات الدندن

- وفي تموز/يوليه 2021، وافقت إدارة الأغذية والعقاقير في الولايات المتحدة على مشروع سيمغلي (insulin glargine overfggn) كمشابه أحيائي قابل للتبادل مع المنتج المرجعي للانسولين لانتوس، الذي يُعَدّ أحد أوائل المشابهات البيولوجية للإنسولين القابل للتبادل في الولايات المتحدة. وقد وسّعت هذه الموافقة إلى حد كبير خيارات العلاج الميسور التكلفة لمعالجة مرض السكري، وأرست سابقة للمشابهات الأحيائية المستقبلية لل الغدد الصماء القابلة للتبادل، مما شجع على اعتماد أوسع وتنافس أكبر في العلاج بالانسولين.

- في أبريل/نيسان 2023، أطلق إيلي ليلي وشركة Rezvoglar (insulin glarggine waglr)، وهو ثاني مشابهة أحيائياً متناظرة في الولايات المتحدة للإنسولين grgine، مما زاد من تعزيز المنافسة في قطاع الانسولين. وقد وفر دخول ريزفوغلار إلى الأسواق خياراً إضافياً يمكن الوصول إليه للعلاج بالإنسولين الطويل التعاطي، مما ساعد على معالجة التكاليف والحواجز التي تحول دون وصول المرضى إلى مرض السكري.

- في سبتمبر/أيلول 2024، أعلنت ساندوز عن إطلاق نموذج بيولوجي جديد مشابه للإنسولين جلارجين في مجموعة مختارة من بلدان أوروبا الشرقية، يهدف إلى تعزيز بصمة علم الغدد الصماء البيولوجية المتماثلة عبر الأسواق الإقليمية. وبتوجيه هذه الأسواق الناشئة، وسعت ساندوز من نطاق الوصول إلى علاجات الأنسولين الفعالة من حيث التكلفة، وأسهمت في إتاحة التماثل البيولوجي على نطاق أوسع خارج الأسواق الغربية التقليدية.

- وفي تشرين الثاني/نوفمبر 2024، حصلت البيولوجيا البيولوجية على إذن تنظيمي لتوسيع نطاق إمداداتها البيولوجية المتماثلة للأنسولين إلى أسواق أوروبية متعددة بعد نجاح عمليات مراجعة حسابات التصنيع، وتعزيز دورها العالمي في المشابهات الأحيائية في علم الغدد الصماء، وإتاحة إمكانية أوسع نطاقا للوصول إلى تناظريات الأنسولين العالية الجودة في أوروبا.

- وفي شباط/فبراير 2025، وافقت هيئة تنمية الحراجة في الولايات المتحدة على استخدام الميرلوج (insulin costaspartsszjj) كمشابه أحيائي لنوفولوغ (insulin aspart)، وهو أول منتج أحيائي مشابه للأشعة السريعة التي تُحدث الأنسولين في الولايات المتحدة. وقد وسعت هذه الموافقة خيارات العلاج لكل من مرضى السكري البالغين ومرض الأطفال بإدخال المنافسة في قطاع الأنسولين السريع التأثير، ومعالجة الاحتياجات الرئيسية غير الملباة في مجال مكافحة الجلوكوز وقت الوجبة.

- وفي تموز/يوليه 2025، منحت هيئة التنمية الحرجية الموافقة إلى Kirsty (Insulin Aspart oxjjhz) باعتبارها أول ووحيد متماثل بيولوجياً متماثلاً إلى NovoLog (insulin aspart) في الولايات المتحدة الأمريكية. وقد عزز هذا المعلم العرض من عرض الانسولين الأحيائي المماثل من خلال السماح بالاستبدال التلقائي على مستوى الصيدلية، وتعزيز وصول المرضى، واحتمال خفض تكاليف العلاج.

- في أيار/مايو 2025، أعلن نوفو نورديسك عن شراكة إنتاج مع التكنولوجيا الأحيائية في مجال التكنولوجيات الأحيائية في فوجيفيلم ديوسينث لتطوير تصنيع الأنسولين كأجزاء من المشابهات البيولوجية التي تستهدف الطلب الآسيوي والأوروبي، مع التأكيد على الجهود الاستراتيجية التي تبذلها الصناعة لتلبية الاحتياجات العالمية من علاجات السكري الفعالة من حيث التكلفة من خلال زيادة القدرة الإنتاجية والمدى الجغرافي.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.