Global Smart Orthopedic Implants Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

375.08 Billion

USD

627.78 Billion

2025

2033

USD

375.08 Billion

USD

627.78 Billion

2025

2033

| 2026 –2033 | |

| USD 375.08 Billion | |

| USD 627.78 Billion | |

| % | |

|

Global Smart Orthopedic Implants Market Segmentation, Product Type (Hip Reconstruction, Knee Reconstruction, Shoulder Implants, Spinal Implants, and Trauma Implants), Material (Bone Cement, Metal, Cobalt, Alloy, and Titanium), End User (Hospitals, Specialty Centers, Orthopedics Clinics, and Ambulatory Surgical Centers) - Industry Trends and Forecast to 2033

Smart Orthopedic Implants Market Size

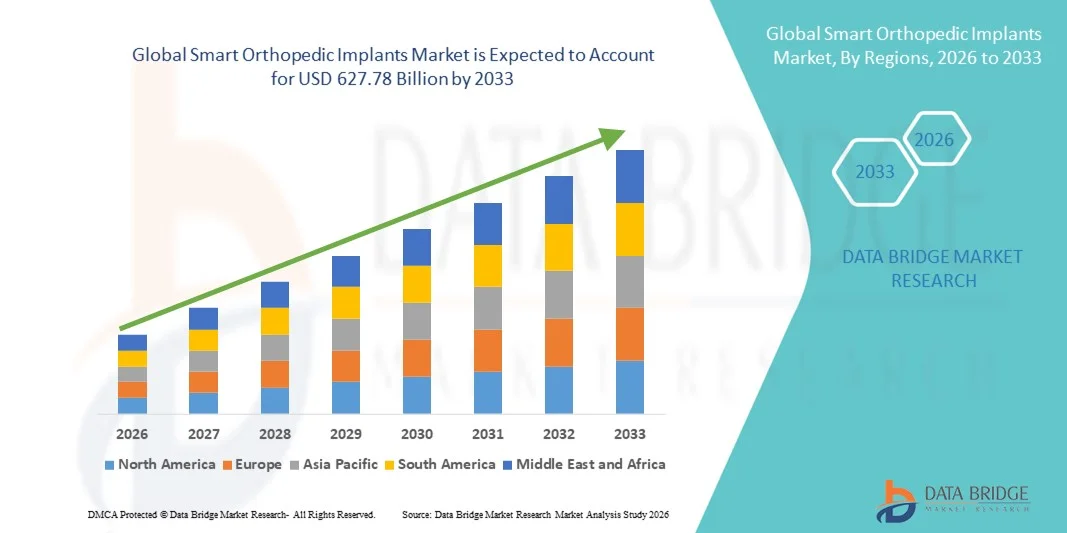

- The global smart orthopedic implants market size was valued at USD 375.08 billion in 2025 and is expected to reach USD 627.78 billion by 2033, at a CAGR of 6.65% during the forecast period

- The market growth is largely fueled by the increasing prevalence of orthopedic disorders, rising geriatric population, and rapid technological advancements in implant materials and digital integration systems, leading to enhanced adoption of smart orthopedic implants across hospitals and specialty orthopedic centers

- Furthermore, growing demand for minimally invasive surgeries, real-time post-operative monitoring, and improved patient-specific treatment outcomes is establishing smart orthopedic implants as an advanced solution in modern orthopedic care. These converging factors are accelerating the uptake of Smart Orthopedic Implants solutions, thereby significantly boosting the industry's growth

Smart Orthopedic Implants Market Analysis

- Smart orthopedic implants, integrating advanced sensors, microelectronics, and wireless connectivity within joint replacement and trauma fixation devices, are becoming increasingly vital components of modern orthopedic care due to their ability to enable real-time performance monitoring, improved implant longevity assessment, and data-driven post-operative management across hospitals and specialty orthopedic centers

- The escalating demand for smart orthopedic implants is primarily fueled by the rising prevalence of osteoarthritis and degenerative bone disorders, increasing geriatric population, growing preference for minimally invasive procedures, and the expanding adoption of digital health technologies that enhance surgical precision and long-term patient outcomes

- North America dominated the smart orthopedic implants market with the largest revenue share of 44.6% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, strong presence of leading medical device manufacturers, and early adoption of digitally integrated orthopedic solutions. The U.S. continues to witness substantial growth in smart joint replacement procedures, supported by favorable reimbursement frameworks and rapid technological innovation

- من المتوقع أن تكون منطقة آسيا والمحيط الهادئ المنطقة الأسرع نموًا في سوق زراعة العظام الذكية خلال فترة التوقعات، وذلك بفضل زيادة الاستثمارات في مجال الرعاية الصحية، وارتفاع أحجام جراحات العظام، وتوسع السياحة العلاجية، وتزايد الوعي بتقنيات الزرع المتقدمة في دول مثل الصين والهند واليابان وكوريا الجنوبية.

- استحوذ قطاع التيتانيوم على أكبر حصة من إيرادات السوق بنسبة 38.9% في عام 2025، مدفوعًا بخصائصه الفائقة في التوافق الحيوي ومقاومة التآكل.

نطاق التقرير وتجزئة سوق غرسات العظام الذكية

|

صفات |

رؤى رئيسية حول سوق الغرسات العظمية الذكية |

|

القطاعات التي تم تغطيتها |

|

|

الدول المشمولة |

أمريكا الشمالية

أوروبا

منطقة آسيا والمحيط الهادئ

الشرق الأوسط وأفريقيا

أمريكا الجنوبية

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات بيانات القيمة المضافة |

بالإضافة إلى المعلومات المتعلقة بسيناريوهات السوق مثل قيمة السوق ومعدل النمو والتجزئة والتغطية الجغرافية واللاعبين الرئيسيين، تتضمن تقارير السوق التي أعدتها شركة Data Bridge Market Research أيضًا تحليلًا متعمقًا من قبل الخبراء، وعلم الأوبئة الخاص بالمرضى، وتحليل خطوط الإنتاج، وتحليل التسعير، والإطار التنظيمي. |

اتجاهات سوق زراعة العظام الذكية

التقدم التكنولوجي من خلال أجهزة الاستشعار المدمجة والمراقبة في الوقت الفعلي

- يُعدّ دمج أجهزة الاستشعار المدمجة والاتصال اللاسلكي داخل الغرسات اتجاهاً هاماً ومتسارعاً في سوق غرسات العظام الذكية العالمية، وذلك لتمكين المراقبة الآنية لصحة المريض وأداء الغرسة. وتتيح هذه الأنظمة المتقدمة تتبعاً مستمراً لمعايير مثل توزيع الحمل، وتغيرات درجة الحرارة، واستقرار الغرسة، وتقدم عملية الشفاء.

- For instance, certain smart knee and hip implant prototypes incorporate micro-sensors that transmit post-operative performance data to clinicians, enabling early detection of implant loosening, misalignment, or infection risks. This enhances clinical decision-making and reduces the likelihood of revision surgeries

- The incorporation of Bluetooth-enabled and cloud-connected monitoring platforms allows orthopedic specialists to remotely assess rehabilitation progress and personalize treatment strategies. This data-driven approach improves long-term patient outcomes and optimizes recovery timelines

- The increasing focus on minimally invasive surgeries and precision-based orthopedic procedures is further accelerating the demand for technologically advanced implants capable of providing actionable performance insights. Hospitals and specialty orthopedic centers are gradually adopting such smart systems to enhance procedural success rates

- This shift toward connected, data-enabled orthopedic solutions is redefining post-surgical care standards and strengthening collaboration between patients and healthcare providers. As a result, manufacturers are investing heavily in R&D to develop next-generation smart orthopedic implants with enhanced durability, biocompatibility, and integrated monitoring capabilities

Smart Orthopedic Implants Market Dynamics

Driver

Rising Prevalence of Orthopedic Disorders and Increasing Geriatric Population

- The growing prevalence of orthopedic disorders such as osteoarthritis, rheumatoid arthritis, osteoporosis, and traumatic injuries is a major driver fueling demand for smart orthopedic implants worldwide

- The rapidly expanding geriatric population, which is more susceptible to degenerative bone conditions and joint-related disorders, is significantly increasing the volume of joint replacement and reconstructive surgeries

- For instance, rising cases of knee and hip replacement procedures globally are encouraging healthcare providers to adopt advanced implant systems that offer improved durability and enhanced post-operative monitoring capabilities

- In addition, increasing sports-related injuries and road accident cases are contributing to the demand for technologically advanced implants that ensure better structural stability and faster recovery

- Government initiatives to improve healthcare infrastructure, growing healthcare expenditure, and greater patient awareness regarding advanced treatment options are further supporting market expansion across both developed and emerging economies

Restraint/Challenge

Concerns Regarding Cybersecurity and High Initial Costs

- The high cost associated with technologically advanced smart orthopedic implants remains a significant challenge for widespread adoption, particularly in developing regions with limited reimbursement coverage and budget-constrained healthcare systems

- Smart implants integrated with embedded sensors, wireless data transmission modules, and advanced biocompatible materials involve higher research, manufacturing, and validation costs compared to conventional orthopedic implants, resulting in premium pricing

- For instance, sensor-enabled knee or hip implants designed to provide post-operative performance monitoring can cost substantially more than traditional implants, making hospitals and patients in cost-sensitive markets hesitant to adopt these advanced solutions without clear reimbursement support

- Complex and stringent regulatory approval processes for combination products (medical device plus digital component) further increase time-to-market and compliance expenses. Manufacturers must conduct extensive clinical validation to demonstrate both mechanical safety and digital reliability before obtaining approvals from regulatory authorities

- In addition, concerns related to long-term device durability, cybersecurity of transmitted medical data, and integration with hospital IT infrastructure may slow procurement decisions among healthcare providers

- Overcoming these challenges through cost optimization, expanded reimbursement frameworks, regulatory harmonization, and enhanced data security measures will be essential to ensure sustained and widespread adoption of smart orthopedic implants globally

Smart Orthopedic Implants Market Scope

The market is segmented on the basis of product type, material, and end user.

- By Product Type

On the basis of product type, the Global Smart Orthopedic Implants market is segmented into Hip Reconstruction, Knee Reconstruction, Shoulder Implants, Spinal Implants, and Trauma Implants. The Knee Reconstruction segment dominated the largest market revenue share of 34.7% in 2025, driven by the rising global prevalence of osteoarthritis and degenerative joint disorders. The increasing geriatric population significantly contributes to higher knee replacement procedures worldwide. Technological advancements such as sensor-enabled smart knee implants allow real-time post-operative monitoring of joint performance. Growing obesity rates further increase the risk of knee joint deterioration, supporting procedure volumes. Improved surgical techniques and robotic-assisted orthopedic surgeries enhance implant accuracy and outcomes. Higher awareness regarding early joint replacement improves patient acceptance rates. Favorable reimbursement policies in developed regions also support market expansion. Continuous innovation in minimally invasive knee reconstruction procedures reduces recovery time. Increasing sports-related injuries further stimulate demand. Expansion of orthopedic specialty hospitals globally strengthens procurement. Rising healthcare expenditure in emerging economies supports accessibility. The durability and long-term success rate of smart knee implants further reinforce dominance.

The Spinal Implants segment is anticipated to witness the fastest CAGR of 9.4% from 2026 to 2033, fueled by the growing incidence of spinal disorders such as degenerative disc disease and spinal stenosis. Rising sedentary lifestyles and poor posture contribute significantly to spinal complications. Smart spinal implants equipped with monitoring sensors are gaining traction for post-surgical recovery tracking. Increasing adoption of minimally invasive spine surgeries enhances segment growth. Technological integration enabling data-driven rehabilitation supports patient outcomes. Growing aging populations globally further drive procedural demand. Expansion of advanced neurosurgical centers strengthens adoption. Increasing awareness regarding early intervention for spinal deformities also supports growth. Healthcare infrastructure development in Asia-Pacific and Latin America accelerates demand. Rising research investments in bio-compatible smart materials enhance product innovation. Higher success rates of spinal fusion procedures improve patient confidence. Continuous product approvals and clinical trials further strengthen segment momentum.

- By Material

On the basis of material, the Global Smart Orthopedic Implants market is segmented into Bone Cement, Metal, Cobalt Alloy, and Titanium. The Titanium segment held the largest market revenue share of 38.9% in 2025, driven by its superior biocompatibility and corrosion resistance properties. Titanium implants are lightweight yet highly durable, making them ideal for load-bearing orthopedic applications. The material promotes better osseointegration, enhancing implant stability and longevity. Growing preference for long-lasting implant materials supports its widespread adoption. Technological advancements in 3D-printed titanium implants further strengthen demand. Titanium’s compatibility with smart sensor integration enhances its suitability for next-generation implants. Increasing joint replacement procedures globally contribute to volume growth. The material also reduces allergic reactions compared to other metals. Expanding orthopedic research supports development of advanced titanium alloys. Favorable regulatory approvals further encourage adoption. Rising patient awareness regarding implant quality influences material preference. Continuous innovation in surface modification technologies enhances performance outcomes.

The Cobalt Alloy segment is projected to register the fastest CAGR of 8.7% from 2026 to 2033, owing to its exceptional strength and wear resistance in high-stress orthopedic procedures. Cobalt alloys are particularly suitable for knee and hip implants requiring long-term mechanical durability. Increasing demand for revision surgeries supports material growth. The alloy’s resistance to fatigue and fracture enhances implant lifespan. Growing research into advanced alloy combinations improves performance characteristics. Expansion of complex joint reconstruction procedures further drives usage. Rising demand for high-performance implants in sports injury treatments supports adoption. Improved manufacturing technologies enhance precision and reliability. Emerging markets are witnessing growing acceptance of durable alloy-based implants. Increased surgeon preference for mechanically robust materials strengthens growth. Continuous clinical trials evaluating improved alloy formulations support expansion. Rising healthcare spending globally further contributes to segment acceleration.

- By End User

On the basis of end user, the Global Smart Orthopedic Implants market is segmented into Hospitals, Specialty Centers, Orthopedic Clinics, and Ambulatory Surgical Centers. The Hospitals segment accounted for the largest market revenue share of 45.3% in 2025, driven by the high volume of complex joint replacement and spinal surgeries performed in hospital settings. Hospitals are equipped with advanced surgical infrastructure and robotic-assisted systems. Availability of skilled orthopedic surgeons further strengthens dominance. Higher patient inflow for trauma and emergency cases supports procedural volume. Integration of smart implant monitoring systems is more feasible in hospital environments. Favorable reimbursement frameworks encourage hospital-based surgeries. Expansion of multi-specialty hospitals globally contributes to procurement growth. Increasing government healthcare investments strengthen hospital infrastructure. Access to post-operative care facilities enhances patient outcomes. Rising medical tourism in developed nations further boosts hospital procedures. Continuous technology upgrades support adoption of sensor-enabled implants. The presence of research and clinical trial units further strengthens segment leadership.

من المتوقع أن يشهد قطاع مراكز الجراحة النهارية (ASCs) أسرع معدل نمو سنوي مركب بنسبة 10.1% خلال الفترة من 2026 إلى 2033، مدفوعًا بتزايد الإقبال على إجراءات جراحة العظام ذات التكلفة المنخفضة والتدخل الجراحي المحدود. توفر هذه المراكز إقامة أقصر في المستشفى وتكاليف جراحية أقل. كما أن زيادة الإقبال على جراحات استبدال المفاصل في نفس اليوم يُسرّع من هذا النمو. وتتيح التطورات التكنولوجية مراقبة ذكية للزرعات حتى في العيادات الخارجية. ويدعم تزايد رغبة المرضى في التعافي السريع إجراءات مراكز الجراحة النهارية. ويعزز توسع مرافق الرعاية الصحية الخاصة عالميًا البنية التحتية. كما تُسهم نماذج السداد المواتية لجراحات العيادات الخارجية في زيادة الإقبال عليها. ويُفضل الجراحون بشكل متزايد مراكز الجراحة النهارية لإجراء العمليات الاختيارية. وتجذب مخاطر العدوى المنخفضة مقارنةً بالإقامة التقليدية في المستشفى المرضى. ويساهم تزايد خصخصة الرعاية الصحية في الاقتصادات الناشئة في توسع هذا القطاع. كما تدعم التحسينات المستمرة في التخدير وكفاءة الجراحة هذا النمو. ويؤدي ازدياد الوعي برعاية جراحة العظام في العيادات الخارجية إلى زيادة تدفق المرضى.

تحليل إقليمي لسوق غرسات العظام الذكية

- هيمنت أمريكا الشمالية على سوق زراعة العظام الذكية بحصة إيرادات بلغت 44.6% في عام 2025.

- تتميز المنطقة ببنية تحتية متطورة للرعاية الصحية، وإنفاق مرتفع عليها، وحضور قوي لشركات تصنيع الأجهزة الطبية الرائدة، واعتماد مبكر لحلول تقويم العظام المتكاملة رقميًا. وتستفيد المنطقة من شبكات مستشفيات راسخة، وتزايد أعداد جراحات استبدال المفاصل، والدمج السريع لتقنيات الزرع المعتمدة على أجهزة الاستشعار والبيانات.

- تتعزز ريادة المنطقة بفضل أطر التعويض المواتية، وقدرات البحث السريري القوية، والابتكار التكنولوجي المستمر في مواد الزرع وأنظمة المراقبة المدمجة. ويستمر الطلب المتزايد على إجراءات جراحة العظام الدقيقة وتحسين تتبع نتائج ما بعد الجراحة في تعزيز توسع السوق في المستشفيات ومراكز جراحة العظام المتخصصة.

نظرة عامة على سوق زراعة العظام الذكية في الولايات المتحدة

استحوذ سوق زراعة العظام الذكية في الولايات المتحدة على الحصة الأكبر من الإيرادات في أمريكا الشمالية عام 2025، ومن المتوقع أن يشهد نموًا ملحوظًا بمعدل نمو سنوي مركب خلال الفترة المتوقعة. ويعزى هذا النمو إلى ارتفاع معدلات انتشار التهاب المفاصل العظمي واضطرابات الجهاز العضلي الهيكلي، وتزايد عدد كبار السن، والطلب المتزايد على إجراءات استبدال المفاصل المتقدمة. وتشهد البلاد إقبالًا متزايدًا على زراعة مفاصل الركبة والورك الذكية المزودة بتقنيات مراقبة الأداء. إضافةً إلى ذلك، تُسهم سياسات التعويض الداعمة، والاستثمارات الكبيرة في البحث والتطوير، ووجود الشركات الرائدة في هذا القطاع، في تسريع وتيرة ابتكار وتسويق حلول الجيل القادم من زراعة العظام الذكية في الولايات المتحدة.

نظرة عامة على سوق زراعة العظام الذكية في أوروبا

من المتوقع أن يشهد سوق زراعة العظام الذكية في أوروبا نموًا ملحوظًا بمعدل نمو سنوي مركب كبير خلال الفترة المتوقعة، مدفوعًا بشكل أساسي بزيادة عمليات جراحة العظام، وتزايد عدد كبار السن، والتركيز المتزايد على أساليب العلاج المتقدمة تقنيًا والأقل توغلاً. وتدعم المعايير التنظيمية الصارمة والتركيز على الأجهزة الطبية عالية الجودة اعتماد زراعة العظام المتكاملة رقميًا في جميع أنحاء المنطقة. وتشهد المنطقة طلبًا متزايدًا في المستشفيات العامة والعيادات التخصصية الخاصة والمراكز الطبية الأكاديمية، حيث يتم دمج تقنيات زراعة العظام الذكية في عمليات استبدال المفاصل الأولية والتصحيحية.

نظرة عامة على سوق زراعة العظام الذكية في المملكة المتحدة

من المتوقع أن يشهد سوق زراعة العظام الذكية في المملكة المتحدة نموًا مطردًا خلال الفترة المتوقعة، مدعومًا بتزايد حالات اضطرابات المفاصل التنكسية ووجود نظام رعاية صحية عامة قوي. ويشجع تركيز البلاد على التشخيص المبكر، والعلاجات العظمية الدقيقة، وتحسين المتابعة بعد الجراحة، على تبني تقنيات زراعة العظام المتقدمة. كما تساهم مبادرات تحديث الرعاية الصحية المستمرة والتعاون البحثي في تحفيز نمو السوق.

نظرة عامة على سوق زراعة العظام الذكية في ألمانيا

من المتوقع أن يشهد سوق زراعة العظام الذكية في ألمانيا نموًا ملحوظًا بمعدل نمو سنوي مركب كبير خلال الفترة المتوقعة، مدفوعًا بالطلب المتزايد على الزرعات عالية الأداء وقاعدة تصنيع الأجهزة الطبية القوية في البلاد. ويُسهم تركيز ألمانيا على دقة الهندسة والابتكار السريري والبنية التحتية الجراحية المتطورة في تعزيز استخدام الجيل القادم من زرعات العظام الذكية، لا سيما في عمليات استبدال مفصل الورك والركبة.

نظرة عامة على سوق زراعة العظام الذكية في منطقة آسيا والمحيط الهادئ

من المتوقع أن يشهد سوق زراعة العظام الذكية في منطقة آسيا والمحيط الهادئ أسرع معدل نمو سنوي مركب خلال الفترة المتوقعة، مدفوعًا بزيادة الاستثمارات في قطاع الرعاية الصحية، وارتفاع عدد عمليات جراحة العظام، وتوسع السياحة العلاجية، وتزايد الوعي بتقنيات زراعة العظام المتقدمة في دول مثل الصين والهند واليابان وكوريا الجنوبية. كما تُسهم التحسينات السريعة في البنية التحتية للرعاية الصحية وزيادة إمكانية الوصول إلى خدمات جراحة العظام المتخصصة في دعم النمو الإقليمي. ومع تحديث أنظمة الرعاية الصحية وارتفاع الدخل المتاح، يتزايد إقبال المرضى على زراعة العظام المتطورة تقنيًا والتي توفر متانة معززة ونتائج سريرية أفضل.

نظرة عامة على سوق زراعة العظام الذكية في اليابان

يشهد سوق زراعة العظام الذكية في اليابان نموًا متسارعًا نتيجة لشيخوخة السكان السريعة وانتشار أمراض العظام التنكسية. وتدعم القدرات التكنولوجية المتقدمة والبنية التحتية المتطورة للمستشفيات والتبني المبكر للتقنيات الطبية المبتكرة هذا النمو المطرد للسوق. ويبرز الطلب بشكل خاص في السوق اليابانية على غرسات العظام طويلة الأمد وعالية الدقة والمتكاملة مع إمكانيات المراقبة.

نظرة عامة على سوق زراعة العظام الذكية في الصين

استحوذ سوق زراعة العظام الذكية في الصين على الحصة الأكبر من الإيرادات في منطقة آسيا والمحيط الهادئ عام 2025، ويعزى ذلك إلى ارتفاع عدد عمليات جراحة العظام، وتوسع الطبقة المتوسطة، والاستثمارات الحكومية الكبيرة في البنية التحتية للرعاية الصحية. ويُعدّ ازدياد السياحة العلاجية، وتحسين الوصول إلى الرعاية الجراحية المتقدمة، وتزايد حضور الشركات المصنعة للزراعات محلياً وعالمياً، من العوامل الرئيسية الدافعة لنمو السوق. كما يُسهم التحديث المستمر للمستشفيات وارتفاع الوعي بتقنيات استبدال المفاصل المتقدمة في تسريع تبني هذه التقنيات في جميع أنحاء البلاد.

حصة سوق غرسات العظام الذكية

تتصدر شركات راسخة صناعة زراعة العظام الذكية، بما في ذلك:

- شركة زيمر بايوميت القابضة (الولايات المتحدة الأمريكية)

- شركة سترايكر (الولايات المتحدة الأمريكية)

- شركة سميث آند نيفيو بي إل سي (المملكة المتحدة)

- شركة ميدترونيك بي إل سي (أيرلندا)

- شركة غلوبوس الطبية (الولايات المتحدة الأمريكية)

- شركة NuVasive (الولايات المتحدة الأمريكية)

- شركة إكزاكتيك (الولايات المتحدة الأمريكية)

- شركة مايكروبورت العلمية (الصين)

- B. Braun Melsungen AG (ألمانيا)

- شركة آرثريكس (الولايات المتحدة الأمريكية)

- مجموعة رايت الطبية (الولايات المتحدة)

- شركة كونفورميس (الولايات المتحدة الأمريكية)

- شركة ليما كوربوريت (إيطاليا)

- شركة دي جيه أو جلوبال (الولايات المتحدة الأمريكية)

- مجموعة كورين (المملكة المتحدة)

- شركة إنتغرا لعلوم الحياة (الولايات المتحدة الأمريكية)

- أنظمة زراعة الأسنان من شركة إيسكولاب (ألمانيا)

- شركة أمبليتود الجراحية (فرنسا)

شركة أومني لايف ساينس (الولايات المتحدة الأمريكية)

آخر التطورات في سوق زراعة العظام الذكية العالمية

- في أغسطس 2021، حصلت ركبة زيمر بايوميت الذكية Persona IQ على تصنيف De Novo من إدارة الغذاء والدواء الأمريكية، مما جعلها واحدة من أوائل أنظمة استبدال الركبة المزودة بأجهزة استشعار والمسموح باستخدامها سريريًا في الولايات المتحدة. وقد سمح هذا الإنجاز التنظيمي للزرعة بنقل بيانات ميكانيكية حيوية في الوقت الفعلي إلى أجهزة خارجية لمراقبة تعافي المريض وأداء المفصل، مما يمثل تقدمًا رئيسيًا في تكنولوجيا زراعة العظام المتصلة.

- في أبريل 2022، دخلت شركة eCential Robotics في شراكة مع شركة Amplitude Surgical لتطوير حل جراحي روبوتي للركبة يهدف إلى تحسين الدقة والنتائج في عمليات زراعة العظام الذكية. وقد أبرز هذا التعاون التكامل المتزايد بين الأنظمة الروبوتية والغرسات الذكية لدعم اتخاذ القرارات أثناء العمليات الجراحية وسير العمل الجراحي القائم على البيانات.

- في مارس 2024، حصلت شركة Intellirod Spine على موافقة إدارة الغذاء والدواء الأمريكية (FDA) لنظام زراعة دمج الفقرات LoadSmart، الذي يتضمن مستشعرات مدمجة قادرة على قياس الحمل والإجهاد عبر قطاعات الفقرات لتحسين نتائج ما بعد الجراحة. وقد أكدت هذه الموافقة على الابتكار المستمر في غرسات العمود الفقري المدمجة بالمستشعرات والمصممة لتحسين مراقبة الأداء واستراتيجيات إعادة التأهيل.

- في مارس 2025، وسّعت شركة زيمر بايوميت محفظتها من منتجات تقويم العظام الذكية بإطلاق ساق Persona IQ 30 مم، وهي امتداد جديد مزود بمستشعرات لحلول الركبة الذكية، مصمم ليناسب نطاقًا أوسع من تشريح المرضى ويعزز جمع البيانات لخطط التعافي الشخصية. وقد عزز إطلاق هذا المنتج ريادة الشركة في تقنيات الزرع القائمة على المستشعرات، ووسع نطاق تطبيقاتها السريرية.

- In June 2025, NanoHive Medical LLC partnered with DirectSync Surgical to co-develop Hive Soft Titanium spinal interbody fusion implants with integrated piezoelectric sensors and remote monitoring capabilities, combining advanced 3D-printed structures with smart sensor technology to enable bone stimulation and enhanced data capture for patient-specific care. This strategic collaboration illustrated the trend toward highly customized and connected implant solutions in the smart orthopedic segment

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.