Global Vehicle Subscription Market

حجم السوق بالمليار دولار أمريكي

CAGR :

%

USD

8.21 Billion

USD

23.75 Billion

2025

2033

USD

8.21 Billion

USD

23.75 Billion

2025

2033

| 2026 –2033 | |

| USD 8.21 Billion | |

| USD 23.75 Billion | |

| % | |

|

تقسيم سوق اشتراكات المركبات العالمية، حسب نوع الاشتراك (علامة تجارية واحدة وعلامات تجارية متعددة)، ومزود الخدمة (مصنعي المعدات الأصلية/الشركات التابعة، ومزودي خدمات التنقل، وشركات التكنولوجيا)، والباقة (الاقتصادية، والقياسية، والمميزة)، والمستخدم النهائي (الشركات والأفراد) - اتجاهات الصناعة وتوقعاتها حتى عام 2033

حجم سوق اشتراكات المركبات

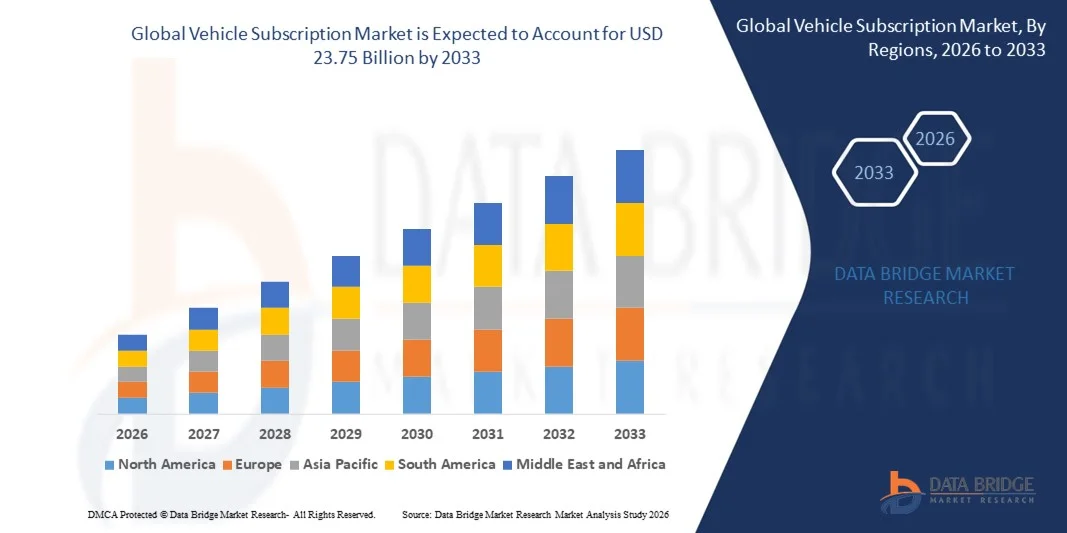

- بلغت قيمة سوق اشتراكات المركبات العالمية 8.21 مليار دولار أمريكي في عام 2025، ومن المتوقع أن تصل إلى 23.75 مليار دولار أمريكي بحلول عام 2033 ، بمعدل نمو سنوي مركب قدره 14.2% خلال فترة التوقعات.

- يعود نمو السوق إلى حد كبير إلى التحول المتزايد من ملكية المركبات التقليدية نحو نماذج التنقل المرنة القائمة على الاستخدام، مدعومًا بالرقمنة المتزايدة في جميع أنحاء منظومة السيارات والتنقل.

- علاوة على ذلك، فإن تزايد تفضيل المستهلكين لشفافية التكاليف والخدمات المجمعة والالتزامات قصيرة الأجل يجعل اشتراكات المركبات بديلاً جذابًا لكل من المستخدمين الأفراد والشركات، مما يسرع من توسع السوق بشكل عام

تحليل سوق اشتراكات المركبات

- أصبحت خدمات اشتراك المركبات، التي توفر وصولاً مرناً إلى المركبات من خلال دفعة متكررة واحدة تغطي التأمين والصيانة وخدمات الدعم، جزءاً لا يتجزأ من حلول التنقل الحديثة للمستخدمين الأفراد والشركات.

- يعود الطلب المتزايد على اشتراكات المركبات في المقام الأول إلى تغير أنماط التنقل الحضري، وزيادة قبول الخدمات القائمة على التطبيقات، والتفضيل القوي للراحة والمرونة وتقليل الالتزامات المالية طويلة الأجل.

- هيمنت أمريكا الشمالية على سوق اشتراكات السيارات بحصة بلغت 38.9% في عام 2025، وذلك بسبب تغير تفضيلات المستهلكين نحو الوصول المرن إلى السيارات وتقليل التزامات الملكية طويلة الأجل.

- من المتوقع أن تكون منطقة آسيا والمحيط الهادئ أسرع المناطق نموًا في سوق اشتراكات السيارات خلال الفترة المتوقعة، وذلك بسبب

- هيمنت شركات تصنيع المعدات الأصلية/الشركات التابعة على السوق بحصة بلغت 64.5% في عام 2025، وذلك بفضل وصولها المباشر إلى سلاسل توريد المركبات، وشبكات الموزعين الراسخة، وثقة العملاء بالعلامة التجارية. وتستفيد الاشتراكات التي تقودها شركات تصنيع المعدات الأصلية من أسعار مُحسّنة، ودعم متكامل لما بعد البيع، وخدمات تأمين وصيانة مُجمّعة.

نطاق التقرير وتجزئة سوق اشتراكات المركبات

|

صفات |

رؤى رئيسية حول سوق اشتراكات المركبات |

|

القطاعات التي تم تغطيتها |

|

|

الدول المشمولة |

أمريكا الشمالية

أوروبا

منطقة آسيا والمحيط الهادئ

الشرق الأوسط وأفريقيا

أمريكا الجنوبية

|

|

اللاعبون الرئيسيون في السوق |

|

|

فرص السوق |

|

|

مجموعات بيانات القيمة المضافة |

بالإضافة إلى رؤى السوق مثل قيمة السوق ومعدل النمو وقطاعات السوق والتغطية الجغرافية واللاعبين في السوق وسيناريو السوق، يتضمن تقرير السوق الذي أعده فريق أبحاث السوق في Data Bridge تحليلاً متعمقاً من قبل الخبراء، وتحليلاً للاستيراد والتصدير، وتحليلاً للتسعير، وتحليلاً لاستهلاك الإنتاج، وتحليلاً لـ PESTLE. |

اتجاهات سوق اشتراكات المركبات

تزايد التحول نحو الوصول المرن والقائم على الاستخدام للمركبات

- يُعدّ التحوّل المتزايد نحو الوصول المرن والقائم على الاستخدام إلى المركبات أحد أبرز الاتجاهات في سوق اشتراكات المركبات، مدفوعًا بتغيّر مواقف المستهلكين تجاه الملكية وتزايد الطلب على حلول التنقل المريحة. ويُفضّل المستهلكون بشكل متزايد الاشتراكات التي تتيح استخدامًا قصير الأجل دون التزامات مالية أو تعاقدية طويلة الأجل، لا سيما في البيئات الحضرية.

- على سبيل المثال، يُمكّن برنامج "كير باي فولفو" التابع لشركة فولفو للسيارات العملاء من الوصول إلى المركبات من خلال رسوم شهرية ثابتة تغطي التأمين والخدمة والصيانة، مما يعزز جاذبية استخدام المركبات المبسط والمرن. تُعيد هذه العروض تشكيل نظرة المستهلكين إلى الوصول إلى المركبات من خلال إعطاء الأولوية للسهولة والمرونة والخدمات المتكاملة.

- تُركز شركات صناعة السيارات بشكل متزايد على تقديم الاشتراكات كجزء لا يتجزأ من أنظمة التنقل الرقمية، حيث تدمج عمليات التسجيل عبر التطبيقات، واستبدال المركبات، وإدارة الحسابات. وهذا من شأنه أن يعزز تفاعل المستخدمين ويحسن تجربة العملاء بشكل عام عبر منصات الاشتراك.

- يكتسب هذا التوجه رواجاً متزايداً بين المستهلكين الشباب الذين يفضلون الوصول إلى الخدمات على امتلاكها، ويقدرون التكاليف الشهرية الثابتة. وتتوافق نماذج الاشتراك بشكل وثيق مع تفضيلات التنقل المرتبطة بنمط الحياة، لا سيما في المدن ذات الكثافة السكانية العالية.

- تتجه الشركات إلى تبني اشتراكات المركبات لدعم احتياجاتها التشغيلية قصيرة الأجل وتسهيل تنقل القوى العاملة. وهذا من شأنه أن يوسع نطاق أهمية الاشتراكات ليشمل فئات أخرى غير المستخدمين الأفراد، ويعزز دورها في استراتيجيات التنقل الحديثة.

- The continued expansion of subscription offerings across multiple vehicle categories and regions is reinforcing this trend. Flexible vehicle access is increasingly becoming a core component of the evolving global mobility landscape

Vehicle Subscription Market Dynamics

Driver

Rising Preference for Cost-Transparent and All-Inclusive Mobility Solutions

- A key driver of the vehicle subscription market is the rising preference for cost-transparent mobility solutions that bundle insurance, maintenance, roadside assistance, and servicing into a single recurring payment. This structure eliminates unexpected ownership costs and simplifies vehicle usage for consumers and businesses

- For instance, Volkswagen Group of America, through its VW Flex program, offers subscribers a single monthly fee covering insurance, maintenance, and roadside assistance. This approach directly addresses consumer demand for predictable expenses and simplified vehicle management

- Corporate users are increasingly drawn to subscriptions as they reduce capital expenditure and administrative complexity associated with traditional fleet ownership. This is driving adoption among businesses seeking flexible and scalable mobility solutions

- Private consumers are responding positively to subscription models that remove long-term financing commitments and depreciation risks. The clarity and convenience of bundled pricing are strengthening trust and accelerating adoption

- As consumers increasingly prioritize simplicity and financial predictability, all-inclusive subscription models continue to act as a strong catalyst for market growth

Restraint/Challenge

High Operational and Fleet Management Costs

- The vehicle subscription market faces significant challenges due to high operational and fleet management costs associated with maintaining, insuring, and rotating vehicles across subscriber bases. These costs place pressure on profitability, particularly for providers operating large and diverse fleets

- For instance, mobility providers such as Lyft, Inc. incur substantial expenses related to vehicle acquisition, maintenance, insurance, and asset depreciation when supporting flexible access models. Managing these cost structures remains a key operational challenge

- Frequent vehicle turnover and short subscription cycles increase wear and tear, raising maintenance and refurbishment costs. This impacts operational efficiency and complicates fleet optimization efforts

- Insurance premiums and regulatory compliance requirements further add to the financial burden for subscription providers operating across multiple regions. These factors limit pricing flexibility and margin expansion

- These challenges continue to influence provider strategies, encouraging investments in operational optimization, digital fleet management tools, and partnerships to improve cost control and long-term sustainability

Vehicle Subscription Market Scope

The market is segmented on the basis of subscription type, service provider, package, and end user.

- By Subscription Type

On the basis of subscription type, the vehicle subscription market is segmented into single brand and multi brand offerings. The single brand segment dominated the market in 2025, driven by strong OEM-backed programs, better control over vehicle quality, and consistent brand experience. Automakers leverage single brand subscriptions to improve customer retention and monetize idle inventory while offering predictable pricing and maintenance coverage. Consumers often prefer these plans for assured service standards, warranty continuity, and seamless integration with OEM financing and insurance ecosystems. The dominance is further supported by growing OEM focus on direct-to-consumer mobility models.

The multi brand segment is expected to register the fastest growth from 2026 to 2033, fueled by rising consumer demand for flexibility and vehicle variety under a single subscription. Multi brand platforms attract urban users seeking short-term access to different vehicle types without long-term ownership commitments. The ability to switch between brands and models enhances perceived value, supporting rapid adoption across metro regions.

- By Service Provider

On the basis of service provider, the market is segmented into OEM/Captives, mobility providers, and technology companies. The OEM/Captives segment held the largest revenue share of 64.5% in 2025 due to their direct access to vehicle supply chains, established dealer networks, and brand trust. OEM-led subscriptions benefit from optimized pricing, integrated aftersales support, and bundled insurance and maintenance services. These providers use subscriptions as a strategic tool to manage residual values and extend customer lifecycle engagement. Strong financial backing and regulatory familiarity further reinforce their market leadership.

Mobility providers are anticipated to witness the fastest growth rate during the forecast period, supported by asset-light models and data-driven fleet optimization. Their focus on app-based access, flexible tenure options, and competitive pricing appeals strongly to younger and corporate users. Rapid expansion into tier-1 and tier-2 cities accelerates their growth trajectory.

- By Package

On the basis of package, the vehicle subscription market is segmented into budget, standard, and premium plans. The standard package segment dominated the market in 2025, driven by its balanced pricing structure and inclusion of essential services such as maintenance, insurance, and roadside assistance. Standard packages cater to a broad consumer base seeking convenience without the higher costs of premium offerings. They are widely adopted by both private users and small businesses due to predictable monthly expenses. The segment benefits from high scalability across passenger vehicle categories.

The premium package segment is projected to grow at the fastest pace from 2026 to 2033, supported by rising demand for luxury vehicles and personalized mobility experiences. High-income consumers increasingly value access to premium models without ownership risks. Enhanced features such as concierge services, vehicle upgrades, and shorter replacement cycles further drive adoption.

- By End User

On the basis of end user, the market is segmented into business and private users. The business segment accounted for the largest market share in 2025, driven by increasing corporate focus on flexible fleet management and cost optimization. Vehicle subscriptions enable businesses to avoid capital expenditure while ensuring operational agility and predictable mobility costs. Companies across consulting, logistics, and sales functions favor subscriptions for employee transportation and short-term projects. Tax efficiency and simplified fleet administration strengthen segment dominance.

The private segment is expected to experience the fastest growth during the forecast period, supported by changing consumer attitudes toward vehicle ownership. Urban consumers increasingly prefer access-based mobility solutions that reduce long-term financial commitments. Convenience, bundled services, and the ability to upgrade vehicles periodically make subscriptions attractive to private users.

Vehicle Subscription Market Regional Analysis

- North America dominated the vehicle subscription market with the largest revenue share of 38.9% in 2025, driven by changing consumer preferences toward flexible vehicle access and reduced long-term ownership commitments

- Consumers in the region increasingly value all-inclusive pricing models that bundle insurance, maintenance, and roadside assistance, offering predictability and convenience

- The strong presence of OEM-led subscription programs, high vehicle penetration, advanced digital infrastructure, and a mature mobility ecosystem continue to position vehicle subscriptions as an attractive alternative for both individual and corporate users

U.S. Vehicle Subscription Market Insight

The U.S. vehicle subscription market captured the largest revenue share within North America in 2025, supported by high consumer awareness of subscription-based mobility and strong participation from major automakers and mobility providers. Consumers are increasingly drawn to subscription models that offer flexibility to switch vehicles and avoid depreciation risks. The growth of urban populations, rising acceptance of app-based mobility solutions, and strong demand from corporate fleets are accelerating market expansion. In addition, the integration of digital platforms for seamless onboarding and vehicle management continues to strengthen adoption.

Europe Vehicle Subscription Market Insight

The Europe vehicle subscription market is projected to grow at a notable CAGR during the forecast period, driven by shifting attitudes toward car ownership and increasing regulatory pressure on emissions and sustainability. Consumers across the region are favoring flexible mobility solutions that align with urban living and environmental considerations. The growing adoption of electric vehicles within subscription models is further supporting market growth. Strong OEM involvement and expanding mobility service providers are enhancing accessibility across major European cities.

U.K. Vehicle Subscription Market Insight

The U.K. vehicle subscription market is anticipated to grow steadily during the forecast period, fueled by rising demand for short-term vehicle access and cost transparency. Consumers are increasingly opting for subscriptions to avoid upfront payments and long-term financing obligations. The presence of digitally advanced mobility platforms and a well-established automotive retail ecosystem supports adoption. Corporate demand for flexible fleet solutions is also contributing to sustained market growth.

Germany Vehicle Subscription Market Insight

The Germany vehicle subscription market is expected to expand at a considerable CAGR, supported by strong automotive manufacturing capabilities and high consumer trust in OEM-backed programs. German consumers value reliability, vehicle quality, and service assurance, which aligns well with structured subscription offerings. The increasing focus on electric mobility and sustainability is encouraging automakers to introduce EV-based subscription plans. The market benefits from a technologically advanced infrastructure and a growing preference for flexible mobility solutions.

Asia-Pacific Vehicle Subscription Market Insight

The Asia-Pacific vehicle subscription market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and evolving mobility preferences. The region is witnessing increasing acceptance of subscription-based models among younger consumers seeking convenience and flexibility. Expanding digital ecosystems and smartphone penetration are supporting app-based vehicle access. The growing presence of regional mobility providers and OEM initiatives is further accelerating adoption.

Japan Vehicle Subscription Market Insight

The Japan vehicle subscription market is gaining traction due to the country’s strong digital adoption, urban density, and preference for efficient mobility solutions. Consumers are increasingly attracted to subscription models that simplify vehicle usage and ownership-related complexities. The integration of advanced technology, connected vehicle systems, and seamless digital interfaces is supporting market growth. In addition, demand from corporate users and urban residents continues to strengthen adoption.

China Vehicle Subscription Market Insight

The China vehicle subscription market accounted for the largest revenue share in Asia Pacific in 2025, driven by rapid urbanization, a growing middle class, and high acceptance of digital mobility platforms. Consumers are increasingly opting for subscription services to access vehicles without long-term financial commitments. Strong government support for shared mobility and electric vehicles is encouraging OEMs and mobility providers to expand subscription offerings. The availability of competitively priced vehicles and advanced digital ecosystems continues to propel market growth in China.

Vehicle Subscription Market Share

The vehicle subscription industry is primarily led by well-established companies, including:

- Fair Financial Corp. (U.S.)

- Clutch Technologies, LLC (U.S.)

- CarNext (Netherlands)

- FlexDrive (U.S.)

- Cluno GmbH (Germany)

- DriveMyCar Rentals Pty Ltd (Australia)

- BMW AG (Germany)

- Daimler AG (Germany)

- General Motors (U.S.)

- Hyundai Motor India (India)

- Tata Motors (India)

- Tesla (U.S.)

- Volkswagen (Germany)

- Volvo Car Corporation (Sweden)

- ZoomCar (India)

- Cox Automotive (U.S.)

- Wagonex Limited (U.K.)

- LeasePlan (Netherlands)

- Lyft, Inc. (U.S.)

Latest Developments in Global Vehicle Subscription Market

- In October 2024, Volkswagen Group of America, together with Volkswagen Financial Services, launched the VW Flex vehicle subscription program in the Atlanta metro area, marking a strategic move to strengthen OEM-led participation in the vehicle subscription market. By offering a month-to-month model with a single payment covering insurance, maintenance, and 24/7 roadside assistance, the initiative lowers entry barriers for consumers hesitant about long-term ownership. This development reinforces the market shift toward flexible, bundled mobility solutions and enhances competitive pressure on independent mobility providers

- In January 2023, FINN expanded its car subscription service for businesses into the U.S. market, building on the proven success of its B2B model in Germany. The launch strengthened FINN’s international footprint while accelerating adoption of subscription-based fleet solutions among corporate users. By emphasizing flexibility, full-service coverage, and continuous customer support, this move contributed to growing acceptance of subscriptions as a viable alternative to traditional corporate leasing

- In October 2022, Carvolution secured USD 16.12 million in Series D funding from Redalpine to scale its car subscription operations. The investment enabled the company to expand its subscription fleet and improve digital processes, enhancing overall service efficiency. This funding round highlighted strong investor confidence in subscription-based mobility models and supported market maturity through improved access and operational scalability

- في مارس 2022، أطلقت شركة أرفال حل الاشتراك المرن الخاص بها، أرفال أدابتيف، مستهدفةً العملاء الأفراد الباحثين عن خيارات تنقل قابلة للتخصيص. ومن خلال السماح للمشتركين بالاختيار من بين مجموعة من طرازات السيارات التي تعمل بمحركات الاحتراق الداخلي والسيارات الكهربائية مع فترات تعاقد قابلة للتعديل، دعم هذا الإطلاق الطلب المتزايد على الوصول الشخصي والمستدام إلى المركبات. وقد عزز هذا التطور شريحة المستخدمين النهائيين من الأفراد، وربط عروض الاشتراك بتفضيلات المستهلكين المتغيرة في مجال التنقل.

- في فبراير 2022، دخلت شركة Avis في شراكة مع FlexClub لتقديم اشتراكات سيارات بأسعار تنافسية في جنوب إفريقيا، موسعةً بذلك نموذج الاشتراك ليشمل الأسواق الناشئة. ركز هذا التعاون على عقود طويلة الأجل ومرنة عبر منصة إلكترونية، مما حسّن من القدرة على تحمل التكاليف وسهولة الوصول. وقد وسّعت هذه المبادرة النطاق الجغرافي لاشتراكات السيارات، وأظهرت قدرة النموذج على التكيف مع أسواق السيارات الأخرى غير الأسواق الناضجة.

SKU-

احصل على إمكانية الوصول عبر الإنترنت إلى التقرير الخاص بأول سحابة استخبارات سوقية في العالم

- لوحة معلومات تحليل البيانات التفاعلية

- لوحة معلومات تحليل الشركة للفرص ذات إمكانات النمو العالية

- إمكانية وصول محلل الأبحاث للتخصيص والاستعلامات

- تحليل المنافسين باستخدام لوحة معلومات تفاعلية

- آخر الأخبار والتحديثات وتحليل الاتجاهات

- استغل قوة تحليل المعايير لتتبع المنافسين بشكل شامل

منهجية البحث

يتم جمع البيانات وتحليل سنة الأساس باستخدام وحدات جمع البيانات ذات أحجام العينات الكبيرة. تتضمن المرحلة الحصول على معلومات السوق أو البيانات ذات الصلة من خلال مصادر واستراتيجيات مختلفة. تتضمن فحص وتخطيط جميع البيانات المكتسبة من الماضي مسبقًا. كما تتضمن فحص التناقضات في المعلومات التي شوهدت عبر مصادر المعلومات المختلفة. يتم تحليل بيانات السوق وتقديرها باستخدام نماذج إحصائية ومتماسكة للسوق. كما أن تحليل حصة السوق وتحليل الاتجاهات الرئيسية هي عوامل النجاح الرئيسية في تقرير السوق. لمعرفة المزيد، يرجى طلب مكالمة محلل أو إرسال استفسارك.

منهجية البحث الرئيسية التي يستخدمها فريق بحث DBMR هي التثليث البيانات والتي تتضمن استخراج البيانات وتحليل تأثير متغيرات البيانات على السوق والتحقق الأولي (من قبل خبراء الصناعة). تتضمن نماذج البيانات شبكة تحديد موقف البائعين، وتحليل خط زمني للسوق، ونظرة عامة على السوق ودليل، وشبكة تحديد موقف الشركة، وتحليل براءات الاختراع، وتحليل التسعير، وتحليل حصة الشركة في السوق، ومعايير القياس، وتحليل حصة البائعين على المستوى العالمي مقابل الإقليمي. لمعرفة المزيد عن منهجية البحث، أرسل استفسارًا للتحدث إلى خبراء الصناعة لدينا.

التخصيص متاح

تعد Data Bridge Market Research رائدة في مجال البحوث التكوينية المتقدمة. ونحن نفخر بخدمة عملائنا الحاليين والجدد بالبيانات والتحليلات التي تتطابق مع هدفهم. ويمكن تخصيص التقرير ليشمل تحليل اتجاه الأسعار للعلامات التجارية المستهدفة وفهم السوق في بلدان إضافية (اطلب قائمة البلدان)، وبيانات نتائج التجارب السريرية، ومراجعة الأدبيات، وتحليل السوق المجدد وقاعدة المنتج. ويمكن تحليل تحليل السوق للمنافسين المستهدفين من التحليل القائم على التكنولوجيا إلى استراتيجيات محفظة السوق. ويمكننا إضافة عدد كبير من المنافسين الذين تحتاج إلى بيانات عنهم بالتنسيق وأسلوب البيانات الذي تبحث عنه. ويمكن لفريق المحللين لدينا أيضًا تزويدك بالبيانات في ملفات Excel الخام أو جداول البيانات المحورية (كتاب الحقائق) أو مساعدتك في إنشاء عروض تقديمية من مجموعات البيانات المتوفرة في التقرير.