Europe Hearing Aid Market

Marktgröße in Milliarden USD

CAGR :

%

USD

3.06 Billion

USD

5.06 Billion

2025

2033

USD

3.06 Billion

USD

5.06 Billion

2025

2033

| 2026 –2033 | |

| USD 3.06 Billion | |

| USD 5.06 Billion | |

| % | |

|

Marktsegmentierung für Hörgeräte in Europa nach Produkt (Hörgeräte und Hörimplantate), Gerätetyp (digitale und analoge Hörgeräte), Art des Hörverlusts (Schallkopfhörerschaft und Schallleitungshörerschaft), Patientengruppe (Erwachsene und Kinder), Vertriebskanal (große Einzelhandelsketten, herstellereigene Einzelhandelsketten, öffentliche Einrichtungen und Sonstige) – Branchentrends und Prognose bis 2033

Was ist die europäische Hearing Aid Market Size and Growth Rate

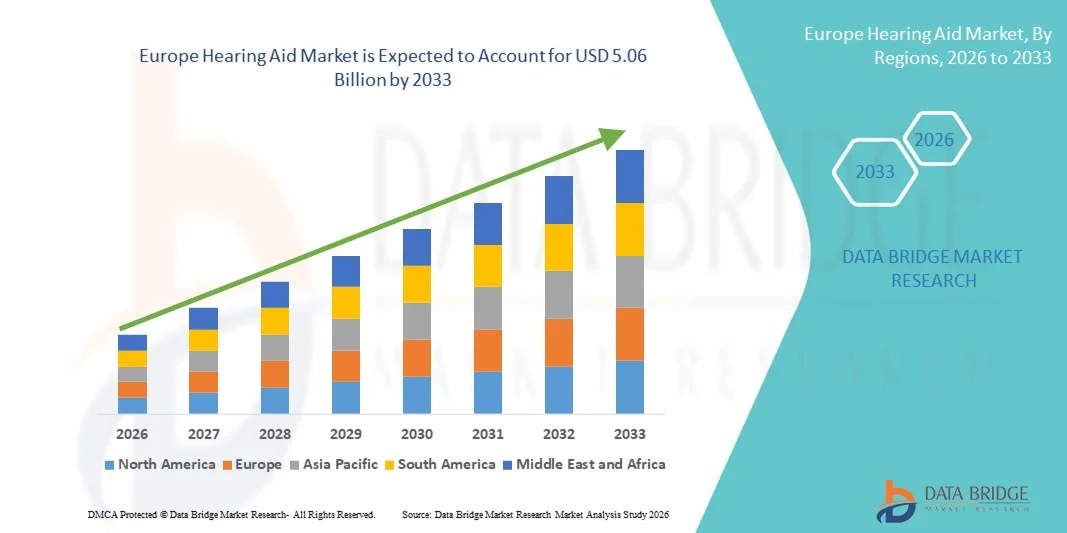

- Wie bei der Data Bridge Market Research Analysis wurde die Marktgröße für Hörgeräte in Europa geschätzt3,06 Milliarden USD in 2025und wird voraussichtlich erreichen5,06 Milliarden USD bis 2033, beiCAGR von 6,50 %während des Prognosezeitraums

- Das Marktwachstum wird größtenteils durch die zunehmende Prävalenz von Hörverlusten in allen Altersgruppen, verbunden mit zunehmendem Bewusstsein über Frühdiagnose und Behandlung, gefördert.

- Darüber hinaus werden technologische Weiterentwicklungen in Hörgeräten – wie digitale Klangbearbeitung, AI-getriebene Anpassung, Bluetooth-Konnektivität und wiederaufladbare Lösungen – die Benutzerfreundlichkeit und die Einführung in den entwickelten und aufstrebenden Märkten verbessern. Diese konvergierenden Faktoren beschleunigen die Aufnahme von Hörgerätelösungen, wodurch das Wachstum der Industrie deutlich erhöht wird

Marktgröße und Prognose

- Globaler Marktwert (2025): USD 3.06 Milliarden

- Voraussichtlicher Marktwert (2033): USD 5.06 Milliarden

- Wettervorhersage CAGR (2026–2033): 6.50%

Europa Hörgerätemarktanalyse

- Hörgeräte, einschließlich Hinter-dem-Ohr (BTE), In-the-Ohr (ITE), und Empfänger-in-canal (RIC) Geräte, sind immer wichtiger medizinische Geräte, die Kommunikation, soziales Engagement und Lebensqualität für Menschen, die leicht bis tiefgreifenden Hörverlust erleben

- Die zunehmende Nachfrage nach Hörhilfen wird in erster Linie von der steigenden geriatrischen Bevölkerung, der zunehmenden Prävalenz von geräuschinduzierten Hörverlusten, der zunehmenden Sensibilisierung für die Früherkennung und kontinuierlichen technologischen Fortschritten wie der KI-fähigen Schallverarbeitung und der Bluetooth-Konnektivität angetrieben.

- Die USA dominierten den Hörgerätemarkt mit dem größten Umsatzanteil von etwa 34,6% im Jahr 2025, unterstützt durch eine starke öffentliche Gesundheitsversorgung, hohe Übernahme fortgeschrittenerdigitale Hörgeräte, und wachsende Sensibilisierungsprogramme für Hörgesundheit

- Deutschland wird voraussichtlich die am schnellsten wachsende Region auf dem Hörgerätemarkt sein, die im Prognosezeitraum eine CAGR von ca. 8,7 % registriert, die von steigender alter Bevölkerung, technologischer Innovation und zunehmender Erstattungspolitik angetrieben wird.

- Das Segment der Erwachsenen dominierte 2025 den größten Marktanteil von 83,4 %, der von der rasant wachsenden geriatrischen Bevölkerung weltweit getrieben wurde.

Report Scope und Hearing Aid Market Segmentation

|

Attribute |

Hearing Aid Schlüsselmarkt Einblicke |

|

Verdeckte Segmente |

|

|

Überarbeitete Länder |

Europa

|

|

Key Market Players |

|

|

Marktmöglichkeiten |

|

|

Daten Infos zum Wert hinzugefügt |

Neben den Erkenntnissen zu Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geographischer Erfassung und großen Akteuren umfassen die Marktberichte, die von der Data Bridge Market Research kuratiert werden, auch eingehende Expertenanalysen, Patientenepidemiologie, Pipelineanalyse, Preisanalyse und regulatorische Rahmenbedingungen. |

Was ist der Haupttrend im europäischen Hörgerätemarkt

Steigende Annahme von erweiterten digitalen und wiederaufladbaren Hörgeräten

- Ein großer Trend auf dem globalen Hörgerätemarkt ist die zunehmende Übernahme fortschrittlicher digitaler und wiederaufladbarer Hörgeräte mit verbesserter Klangqualität, Geräuschminderung und längerer Akkulaufzeit

- Sonova Group hat zum Beispiel im Februar 2023 die Phonak Audéo Paradise Wiederaufladbare Hörgeräte in Europa ins Leben gerufen, die ein verbessertes Sprachverständnis in lauten Umgebungen und eine erweiterte Akkulaufzeit aufweisen und die steigende Präferenz für bequeme und leistungsstarke Hörgeräte bieten.

- Digitale Signalverarbeitung in modernen Hörgeräten ermöglicht personalisierte Soundanpassungen und automatische Umweltanpassungen

- Wiederaufladbare Modelle reduzieren die Abhängigkeit von Einwegbatterien, verbessern Nachhaltigkeit und Benutzerfreundlichkeit

- Die Integration der drahtlosen Vernetzung für mobile Geräte und Streaming gewinnt auch an Traktion und unterstützt nahtlose Vernetzung für Musik-, Call- und Teleaudiologiedienste

- Unternehmen konzentrieren sich zunehmend auf kompakte Designs und Leichtbaumaterialien, um Komfort und Benutzerfreundlichkeit zu verbessern

Europa Hörgerätemarktdynamik

Fahrer

Wachsende Prävalenz von Hörverlusten und Alternde Bevölkerung

- Die zunehmende Prävalenz von Hörbeeinträchtigungen weltweit, insbesondere unter der alternden Bevölkerung, ist ein wichtiger Treiber für das Wachstum des Hörgerätemarktes

- Zum Beispiel inJuli 2022, GN AnhörunghatReSound ONEHörhilfe weltweit, mit dem Ziel, altersbedingte Hörverluste zu bekämpfen und verbesserte Sprachverstehen und individuelle Beschlagnahmung zu beleuchten, die die Annahme älterer Erwachsener beschleunigte

- Das zunehmende Bewusstsein für die gesundheitlichen Auswirkungen unbehandelter Hörverluste motiviert sowohl Patienten als auch Gesundheitsdienstleister, sich für fortgeschrittene Hörlösungen zu entscheiden

- Die staatlichen Gesundheitsinitiativen und die Versicherungsdeckung in den entwickelten Ländern unterstützen die Markterweiterung durch die Verbesserung der Zugänglichkeit

- Die Nachfrage nach diskreten, hinter-dem-Ohr- und in-Ohr-Lösungen treibt Innovation und Produktdifferenzierung auf dem Markt

- Technologische Fortschritte wie Rückkopplungsunterdrückung, Richtmikrofone und Tinnitus-Relief-Funktionen sind weitere attraktive Nutzer, die Premium-Lösungen suchen

Zurückhaltung/Challenge

Hohe Kosten und begrenzte Aufmerksamkeit in Entwicklungsregionen

- Hohe Preise für fortgeschrittene digitale und wiederaufladbare Hörgeräte und ein begrenztes Bewusstsein in aufstrebenden Märkten stellen erhebliche Herausforderungen für das Marktwachstum dar

- So hat beispielsweise im Oktober 2021 eine Studie der Weltgesundheitsorganisation (WHO) darauf hingewiesen, dass weniger als 10% der Menschen mit Hörverlust in Ländern mit niedrigem Einkommen Zugang zu Hörgeräten haben, hohe Kosten und begrenzte Audiologie-Infrastruktur als Schlüsselschranken zu nennen.

- Die Kosten für personalisierte Beschlag- und professionelle Audiologie-Dienste ergänzen die Gesamtkosten, deterring preissensitive Verbraucher

- Mangel an ausgebildeten Audiologen und eingeschränkten Vertriebsnetzen in bestimmten Regionen schränken die Marktdurchdringung weiter ein

- Verbraucher zögern in Bezug auf Gerätewartung, Anpassungszeitraum und wahrgenommene Komplexität kann auch langsame Annahme

- Die Bemühungen, erschwingliche Hörlösungen einzuführen, die Sensibilisierungskampagnen zu erhöhen und professionelle Audiologie-Dienste zu erweitern, werden entscheidend für das anhaltende Marktwachstum sein

Europäischer Markt für Hörgeräte

Der Markt wird auf Basis von Produkt, Gerätetyp, Art von Hörverlust, Patiententyp und Verteilungskanal segmentiert.

- Nach Produkt

Auf Basis des Produkts wird der Hearing Aids-Markt in Hörgeräte und Hörimplantate segmentiert. Das Segment Hörgeräte dominierte den größten Marktanteil von 64,8% im Jahr 2025, angetrieben durch ihre weit verbreitete Annahme bei Patienten mit milder bis mäßiger Hörbehinderung. Diese Geräte sind nicht-invasive, kostengünstige und leicht zugänglich im Vergleich zu chirurgischen Implantaten, so dass sie die erste Behandlungslinie weltweit. Die zunehmende geriatrische Bevölkerung, steigende Fälle von Lärm verursachten Hörverlusten und das zunehmende Bewusstsein in Bezug auf die Frühdiagnose tragen maßgeblich zur Segmentherrschaft bei. Technologische Weiterentwicklungen wie KI-betriebene Klangbearbeitung, Bluetooth-Konnektivität, wiederaufladbare Batterien und fast unsichtbare Designs haben den Produktreiz verbessert. Darüber hinaus haben die unterstützenden Rückzahlungspolitiken in entwickelten Volkswirtschaften und die überzählige Verfügbarkeit in bestimmten Regionen die Zugänglichkeit erweitert. Die Präsenz großer Hersteller, die digitale Hörlösungen kontinuierlich innovieren, stärkt die Marktdurchdringung. Die wachsende Nachfrage nach diskreten, komfortablen und leistungsstarken Geräten sorgt für eine nachhaltige Führung dieses Segments.

Das Segment Hörimplantate wird erwartet, dass das schnellste CAGR von 9,8% von 2026 bis 2033 bezeugt wird, was durch steigende Prävalenz von schweren bis tiefgreifenden Hörverlustfällen weltweit getrieben wird. Die zunehmende Einführung von Cochlea-Implantaten und Knochen-anchored Hörsystemen, insbesondere bei Kinder- und älteren Patienten, unterstützt das Wachstum. Technologische Fortschritte zur Verbesserung der Implantateffizienz, Haltbarkeit und Klangklarheit sind ermutigende Akzeptanz. Die Erweiterung der Gesundheitsinfrastruktur in Schwellenländern und die steigende Regierungsfinanzierung für Hör-Restaurierungsprogramme treiben die Nachfrage weiter an. Verbesserte chirurgische Ergebnisse und kürzere Erholungszeiten haben das Vertrauen des Arztes in Implantatverfahren erhöht. Auch die zunehmende Sensibilisierung der Eltern bei der Frühimplantation trägt wesentlich zur Markterweiterung bei.

- Mit Gerätetyp

Auf Basis des Gerätetyps wird der Hearing Aids-Markt in digitale Hörgeräte und analoge Hörgeräte segmentiert. Das digitale Hörgerätesegment hatte 2025 den größten Marktanteil von 72,3 %, was durch überlegene Klangbearbeitungsfähigkeiten und anpassbare Eigenschaften bedingt ist. Digitale Geräte bieten eine verbesserte Geräuschreduktion, Feedback-Stornierung, mehrkanalige Verarbeitung und drahtlose Anschlussmöglichkeiten, was die Nutzererfahrung deutlich verbessert. Die zunehmende Verbraucherpräferenz für technologisch fortschrittliche Gesundheitseinrichtungen beschleunigt die Nachfrage weiter. Die Integration mit Smartphones und Remote-Anpassungsfunktionen durch mobile Anwendungen verbessern Komfort und Personalisierung. Die Erhöhung der verfügbaren Einkommensniveaus und das Bewusstsein für die Hörgesundheit unterstützen auch die Annahme. Kontinuierliche Innovation führender Hersteller in der Miniaturisierung und Akkutechnologie stärkt die Segmentherrschaft.

Das analoge Hörhilfesegment wird von 2026 bis 2033, insbesondere in kostensensitiven Märkten in Entwicklungsregionen, mit 7,6% am schnellsten CAGR rechnen. Analoge Geräte bleiben erschwinglich und einfach zu bedienen, so dass sie für ältere Bevölkerungen geeignet sind, die nicht mit fortschrittlichen digitalen Technologien vertraut sind. Regierungsgeführte Vertriebsprogramme und öffentliche Gesundheitsinitiativen in Niedrigeinkommensländern unterstützen das Wachstum weiter. Obwohl digitale Geräte global dominieren, sind analoge Modelle weiterhin auf die ländliche und unterhaltsame Bevölkerung ausgerichtet. Zunehmende Anstrengungen zur Bereitstellung erschwinglicher Hörlösungen in Schwellenländern werden erwartet, dass stetiges Wachstum erhalten bleibt.

- Nach Art der Hörverluste

Auf der Grundlage der Art des Hörverlusts wird der Markt für Hörgeräte in sensorische Hörverluste und leitfähige Hörverluste segmentiert. Das Segment sensorineurale Hörverluste entfiel auf den größten Marktanteil von 78,5% im Jahr 2025, der durch seine hohe globale Prävalenz, insbesondere unter der alternden Bevölkerung, getrieben wurde. Alterbedingte Degeneration, längere Lärmexposition und genetische Faktoren tragen maßgeblich dazu bei. Patienten mit sensorinuralem Hörverlust benötigen typischerweise einen langfristigen Einsatz von Hörgeräten oder Implantaten, wodurch die wiederkehrende Nachfrage steigt. Technologische Fortschritte in digitalen Amplifikationssystemen haben deutlich verbesserte Managementergebnisse. Wachsende Sensibilisierungskampagnen und Frühdiagnostikprogramme unterstützen auch das Marktwachstum.

Das leitfähige Hörverlustsegment wird von 2026 bis 2033 am schnellsten CAGR von 8,9 % bezeugt, unterstützt durch verbesserte Diagnosefähigkeiten und zunehmenden Zugang zu ENT-Spezialisten. Pädiatrische Fälle aufgrund von Infektionen und strukturellen Abnormitäten zu stärken, tragen zum Segmentwachstum bei. Fortschritte bei der Knochenleitung und minimalinvasiven chirurgischen Implantaten beschleunigen die Adoption weiter. Auch staatliche Initiativen zur Förderung von Früherkennungsprogrammen spielen eine wichtige Rolle bei der Nachfrage.

- Nach Patiententyp

Auf Basis des Patiententyps wird der Hearing Aids-Markt zu Erwachsenen und Kinderärzten segmentiert. Das Segment der Erwachsenen dominierte 2025 den größten Marktanteil von 83,4%, der von der weltweit stark expandierenden geriatrischen Bevölkerung getrieben wurde. Alterbedingte Hörverluste, berufliche Lärmexposition und lebenswichtige Hörschäden tragen maßgeblich zur Segmentherrschaft bei. Erwachsene suchen zunehmend frühe Behandlung, um Kommunikationsfähigkeiten und Lebensqualität zu erhalten. Technologische Weiterentwicklungen wie diskrete Designs und wiederaufladbare Geräte erhöhen die Akzeptanz von Berufstätigen und älteren Nutzern gleichermaßen.

Das Segment der Pädiatrie wird voraussichtlich die schnellste CAGR von 10,4% von 2026 bis 2033 erleben, die durch den Ausbau von neugeborenen Hör-Screening-Programmen weltweit gefördert wird. Die Erhöhung der elterlichen Bewusstseins- und Früherkennungsinitiativen haben die Behandlungsraten deutlich verbessert. Regierungen und Gesundheitsorganisationen investieren in pädiatrische Audiologiedienste und Cochlea-Implantationsprogramme. Die kontinuierliche Innovation bei kinderfreundlichen Hörgeräten mit verbesserter Sicherheit und Komfort unterstützt das Wachstum.

- Durch den Verteilerkanal

Auf der Grundlage des Vertriebskanals wird der Hearing Aids-Markt in große Einzelhandelsketten, Hersteller-Händler-Ketten, Öffentlichkeit und andere segmentiert. Das Segment Retail-Ketten des Herstellers entfiel auf den größten Marktanteil von 39,7% im Jahr 2025, angetrieben durch starke Markenpräsenz, professionelle audiologistische Unterstützung und maßgeschneiderte Montagedienstleistungen. Diese Kanäle gewährleisten Produkt-Authentizität, Garantieabdeckung und hochwertige After-Sales-Services. Die zunehmende Expansion exklusiver Markenauslässe in den Stadtzentren verstärkt die Segmentherrschaft weiter.

Das große Segment der Einzelhandelsketten wird voraussichtlich die schnellsten CAGR von 2026 bis 2033 von 9.5% beobachten, die durch eine wachsende Verbraucherpräferenz für bequeme Kaufoptionen und wettbewerbsfähige Preisstrukturen getrieben werden. Die Erweiterung der organisierten Einzelhandels-Ketten und Partnerschaften mit Audiologie-Experten verbessern die Zugänglichkeit. Die Integration von Online-Vertriebsplattformen und Omnichannel-Strategien beschleunigt das Wachstum weiter. Auch die Sensibilisierung und verbesserte Erschwinglichkeit in Entwicklungsregionen tragen zu einer raschen Expansion bei.

Europa Hörgerätemarkt Regionale Analyse

- Der europäische Hörhilfemarkt soll sich während des gesamten Prognosezeitraums in einem beträchtlichen CAGR ausweiten, vor allem durch die steigende Prävalenz von Hörverlust, eine rasch alternde Bevölkerung und eine starke staatliche Unterstützung für Hörgeräte im Bereich Hörmedizin.

- Die zunehmende Sensibilisierung für die Früherkennung und Behandlung von Hörbehinderungen fördert die stärkere Übernahme fortschrittlicher digitaler Hörgeräte in der gesamten Region. Technologische Weiterentwicklungen wie wiederaufladbare Geräte, Bluetooth-fähige Hörgeräte und verbesserte Klangverarbeitungstechnologien stärken das Marktwachstum weiter

- Auch in mehreren europäischen Ländern sind günstige Erstattungsrahmen für den Patientenzugang zu Premium-Geräten vorgesehen. In der Region wird die Nachfrage in Krankenhäusern, Audiologie-Kliniken und Einzelhandels-Hörzentren immer größer, wobei Hörgeräte in öffentliche Gesundheitssysteme und private Gesundheitsdienste integriert werden

U.K. Hörgerätemarkt Insight

Der US-Hörhilfemarkt dominierte den Hearing Aid-Markt mit dem größten Umsatzanteil von rund 34,6% im Jahr 2025, unterstützt durch eine starke öffentliche Gesundheitsversorgung, eine hohe Übernahme fortschrittlicher digitaler Hörgeräte und wachsende Sensibilisierungsprogramme für Hörgesundheit. Das Vorhandensein des National Health Service (NHS), der Zugang zu Hörbeurteilungen und subventionierten Hörgeräten bietet, trägt maßgeblich zur weit verbreiteten Annahme bei. Zusätzlich hat die zunehmende Sensibilisierung für altersbedingte Hörverluste und Frühinterventionsprogramme verbesserte Diagnoseraten. Die wachsende ältere Bevölkerung und steigende Fälle von geräuschinduzierten Hörbehinderungen erhöhen die Nachfrage weiter. Die etablierte Audiologie-Infrastruktur der U.K., kombiniert mit der Verfügbarkeit von technologisch fortschrittlichen wiederaufladbaren und drahtlosen Hörgeräten, unterstützt die stetige Markterweiterung während der Prognosezeit.

Deutschland Hörgerätemarktaufsicht

Der deutsche Hörgerätemarkt wird voraussichtlich die am schnellsten wachsende Region im Hearing Aid-Markt sein, die im Voraus eine CAGR von etwa 8,7% registriert, die von einer steigenden alternden Bevölkerung, technologischen Innovation und einer Ausweitung der Erstattungspolitik angetrieben wird. Das starke Gesundheitssystem Deutschlands und die Betonung der vorbeugenden Pflege fördern die Früherkennung und Behandlung von Hörstörungen. Die zunehmende Nachfrage nach hochwertigen digitalen und wiederaufladbaren Hörgeräten sowie die wachsende Verbraucherpräferenz für diskrete und leistungsstarke Geräte beschleunigt die Annahme. Darüber hinaus gewinnen Fortschritte in der Klangverstärkungstechnologie und die Integration mit den mobilen Konnektivitätsmerkmalen bei tech-savvy Verbrauchern an Popularität. Der Ausbau von Audiologie-Kliniken und spezialisierten Hörzentren in städtischen und halbstädtischen Gebieten unterstützt auch das Marktwachstum. Der Fokus Deutschlands auf Gesundheitswesen-Innovation und unterstützende Versicherungsdeckungsrahmen positioniert es als den am schnellsten wachsenden Markt in Europa.

Welche sind die Top-Unternehmen in Europa Hörgerätemarkt

Die Hearing Aid-Industrie wird in erster Linie von etablierten Unternehmen geleitet, darunter:

- Sonova Holding AG (Schweiz)

- Demant A/S (Dänemark)

- WS Audiology (Dänemark)

- GN Store Nord A/S (Dänemark)

- Starkey Laboratories, Inc. (USA)

- Cochlear Limited (Australien)

- MED-EL (Österreich)

- Widex A/S (Dänemark)

- RION Co., Ltd. (Japan)

- Amplifon S.p.A. (Italien)

- Eargo, Inc. (USA)

- Audina Hörgeräte, Inc. (USA)

- Arphi Electronics Private Limited (Indien)

- Sivantos Pte. Ltd.

- Horentek (China)

Aktuelle Entwicklungen in Europa Hörgerätemarkt

- Im August 2022 beendete die US Food and Drug Administration (FDA) eine Grundmarkenregel, die eine neue Kategorie von Over-the-counter (OTC) Hörgeräten für Erwachsene mit leichtem bis mäßigem Hörverlust festlegte, so dass Verbraucher Hörgeräte direkt ohne eine medizinische Prüfung, Verschreibung oder Montage durch einen Audiologen erwerben können. Diese Regulierungsverschiebung senkte die Zugangshindernisse, verbesserte Erreichbarkeit und erweiterte Zugänglichkeit deutlich und markiert eine der transformierendsten Entwicklungen in der globalen Hörgeräteindustrie

- Im Januar 2023 kündigte Sony Electronics die Einführung der ersten überzähligen Hörgeräte, CRE-C10 und CRE-E10, die in Zusammenarbeit mit WS Audiology entwickelt wurden, um diskrete Formfaktoren, wiederaufladbare Batterien und app-basierte Self-Fitting-Funktionen bereitzustellen. Dieser Start signalisierte den Einstieg großer Consumer-Elektronik-Marken in den regulierten Markt für Hörmedizin, beschleunigte Wettbewerb und Innovation

- Im Februar 2023 startete Starkey seine Genesis AI Hörgeräteplattform mit einem neu entwickelten Prozessor, fortschrittlicher Neuro Sound Technologie, verbesserter Sprachklarheit und verbesserter Haltbarkeit gegen Feuchtigkeit und Schweiß. Die Plattform Genesis AI stellte einen bedeutenden technologischen Fortschritt dar, der sich auf künstliche Intelligenz, Schallbearbeitungsgeschwindigkeit und Benutzerkomfort konzentrierte.

- Im März 2024 führte Oticon die Oticon Intent Hörgeräte ein, die innovative 4D-Sensortechnologie, die sich an die Benutzerbewegung, die Gesprächsintensität und die Umweltveränderungen in Echtzeit anpasst. Diese Entwicklung verstärkte die Position von Oticon in KI-fähigen Hörlösungen durch Verbesserung des Sprachverständnisses in komplexen Hörumgebungen

- Im März 2024 erweiterte GN Hearing seine ReSound Nexia Produktfamilie, anerkannt als die weltweit ersten Hörgeräte kompatibel mit Bluetooth LE Audio und Auracast-Audiotechnologie. Diese Weiterentwicklung verbesserte die drahtlose Vernetzung, verbesserte Streaming-Qualität und ermöglichte es Benutzern, direkt mit öffentlichen Audioübertragungen zu verbinden, was einen großen Schritt nach vorne in der digitalen Integration

- Im September 2024 erhielt Apple die FDA-Autorisierung für das Hörgerät Feature in AirPods Pro (2. Generation) und ermöglichte es dem Gerät, als überzähliges Hörgerät für Erwachsene mit wahrgenommen mildem bis mäßigem Hörverlust zu fungieren. Diese Entwicklung verschlimmerte die Linien zwischen Unterhaltungselektronik und medizinischen Hörgeräten, was das Mainstream-Bewusstsein und das Adoptionspotenzial deutlich erweitert

- Im Februar 2025 stellte Beltone seine Hörhilfen von Beltone Envision vor, die mit fortschrittlichen Algorithmen für das Rauschen, verbesserten Funktionen für die Sprachverstärkung und verbesserten Konnektivität ausgestattet sind. Der Start verstärkte den wachsenden Trend zur AI-getriebenen Personalisierung und nahtlose Smartphone-Integration

- Im Juni 2025 kündigte Demant A/S den Erwerb der KIND-Gruppe für ca. 700 Mio. € an, stärkte ihren Retail-Fußabdruck in Deutschland und baute ihr globales Vertriebsnetz aus. Diese strategische Akquisition unterstreicht die kontinuierliche Konsolidierung im Hörgerätemarkt und unterstreicht den Fokus der Unternehmen auf vertikale Integration und globale Expansion

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.