Global Industrial Wood And Metal Packaging Market

Marktgröße in Milliarden USD

CAGR :

%

USD

75.20 Billion

USD

122.50 Billion

2025

2033

USD

75.20 Billion

USD

122.50 Billion

2025

2033

| 2026 –2033 | |

| USD 75.20 Billion | |

| USD 122.50 Billion | |

| % | |

|

Segmentierung des globalen Marktes für industrielle Holz- und Metallverpackungen nach Verpackungsart (Paletten, Kisten, Fässer und Sonstige), Endverbraucherbranche (Lebensmittel und Getränke, Chemie und Petrochemie, Pharmazeutika, Automobilindustrie, Bauwesen und Sonstige) – Branchentrends und Prognose bis 2033

Marktgröße für industrielle Holz- und Metallverpackungen

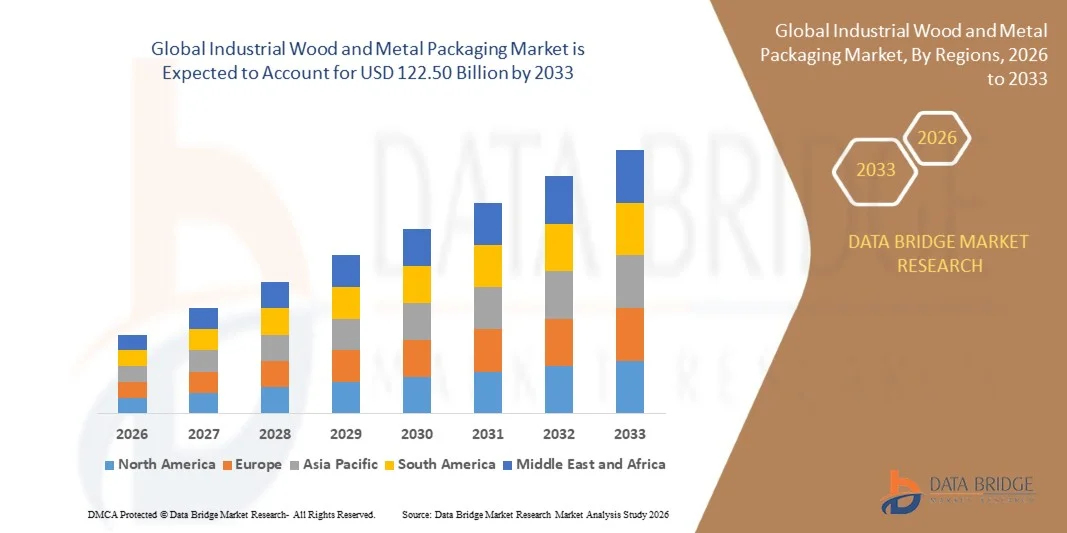

- Der globale Markt für industrielle Holz- und Metallverpackungen hatte im Jahr 2025 einen Wert von 75,20 Milliarden US-Dollar und wird voraussichtlich bis 2033 auf 122,50 Milliarden US-Dollar anwachsen , was einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 5,20 % im Prognosezeitraum entspricht.

- Das Marktwachstum wird maßgeblich durch die steigende Nachfrage nach nachhaltigen und wiederverwendbaren Verpackungslösungen in den Bereichen Logistik, Lebensmittel und Getränke sowie Chemie angetrieben.

- Der zunehmende internationale Handel und der Bedarf an sicherem Warentransport treiben die Verwendung langlebiger Holz- und Metallverpackungen voran.

Marktanalyse für industrielle Holz- und Metallverpackungen

- Der Markt verzeichnet ein starkes Wachstum, bedingt durch eine Kombination aus regulatorischer Unterstützung für nachhaltige Verpackungen, technologischen Innovationen in den Herstellungsprozessen und einem steigenden Bewusstsein für Produktsicherheit und Schadensvermeidung.

- Die zunehmende Präferenz für maßgeschneiderte und leichte Verpackungslösungen verbessert die betriebliche Effizienz für Endanwender in verschiedenen Branchen.

- Nordamerika dominierte 2025 mit einem Umsatzanteil von 38,75 % den Markt für industrielle Holz- und Metallverpackungen. Treiber dieser Entwicklung waren die Präsenz großflächiger Produktions- und Logistikunternehmen sowie der zunehmende Fokus auf nachhaltige und wiederverwendbare Verpackungslösungen.

- Im asiatisch-pazifischen Raum wird voraussichtlich das höchste Wachstum im globalen Markt für industrielle Holz- und Metallverpackungen verzeichnet , angetrieben durch steigende Produktionsaktivitäten, den expandierenden E-Commerce- und Logistiksektor sowie den zunehmenden Fokus auf nachhaltige und effiziente Verpackungslösungen.

- Das Palettensegment hielt 2025 den größten Marktanteil aufgrund seiner weitverbreiteten Verwendung in Lagerhaltung, Logistik und Transport. Paletten bieten einfache Handhabung und Kompatibilität mit Materialflusssystemen. Dank standardisierter Abmessungen vereinfachen sie das Stapeln, Verladen und den Versand in globalen Lieferketten. Ihre Langlebigkeit und Wiederverwendbarkeit reduzieren die Betriebskosten und minimieren Produktschäden während des Transports.

Berichtsumfang und Marktsegmentierung für industrielle Holz- und Metallverpackungen

|

Attribute |

Wichtige Markteinblicke in die industrielle Holz- und Metallverpackungsindustrie |

|

Abgedeckte Segmente |

|

|

Abgedeckte Länder |

Nordamerika

Europa

Asien-Pazifik

Naher Osten und Afrika

Südamerika

|

|

Wichtige Marktteilnehmer |

|

|

Marktchancen |

|

|

Mehrwertdaten-Infosets |

Zusätzlich zu Erkenntnissen über Marktszenarien wie Marktwert, Wachstumsrate, Segmentierung, geografische Abdeckung und Hauptakteure enthalten die von Data Bridge Market Research erstellten Marktberichte auch Import-Export-Analysen, einen Überblick über die Produktionskapazität, eine Analyse des Produktionsverbrauchs, eine Preistrendanalyse, ein Klimawandelszenario, eine Lieferkettenanalyse, eine Wertschöpfungskettenanalyse, einen Überblick über Rohstoffe/Verbrauchsmaterialien, Kriterien für die Lieferantenauswahl, eine PESTLE-Analyse, eine Porter-Analyse und den regulatorischen Rahmen. |

Markttrends für industrielle Holz- und Metallverpackungen

„Aufstieg nachhaltiger und langlebiger Industrieverpackungen“

Der zunehmende Fokus auf nachhaltige und wiederverwendbare Industrieverpackungen aus Holz und Metall verändert den Markt, indem er die Umweltbelastung reduziert und die Produktsicherheit erhöht. Langlebige Verpackungen minimieren Beschädigungen bei Lagerung und Transport, insbesondere bei schweren oder zerbrechlichen Gütern, was zu Kosteneinsparungen und verbesserter betrieblicher Effizienz führt. Die steigende Bedeutung der Reduzierung des CO₂-Fußabdrucks fördert zudem die Verwendung umweltfreundlicher Verpackungsmaterialien und unterstützt so die Nachhaltigkeitsziele von Unternehmen.

Die steigende Nachfrage nach leichten, stapelbaren und modularen Verpackungslösungen beschleunigt die Einführung von Holzwerkstoffpaletten, Metallfässern und kundenspezifischen Behältern. Diese Lösungen optimieren die Lagerfläche und vereinfachen die Logistik, was insbesondere Branchen mit hohem Versandaufkommen zugutekommt. Die Integration in automatisierte Materialflusssysteme steigert die betriebliche Effizienz zusätzlich und reduziert den Personalaufwand.

Die Vielseitigkeit und Kompatibilität moderner Holz- und Metallverpackungen mit Automatisierungs- und Materialflusssystemen machen sie für den industriellen Routinebetrieb attraktiv. Unternehmen profitieren von standardisierten, langlebigen Verpackungen, die Ersatzkosten senken und die Effizienz der Lieferkette verbessern. Modulare Designs ermöglichen zudem eine einfache Anpassung, sodass Unternehmen unterschiedlichsten Lager- und Versandanforderungen gerecht werden können.

Beispielsweise berichteten im Jahr 2023 mehrere Chemie- und Lebensmittelverarbeitungsbetriebe in Europa von einer deutlichen Reduzierung von Produktschäden und Lagerineffizienzen nach der Umstellung auf verstärkte Metallfässer und Holzpaletten, was die betriebliche Produktivität steigerte. Die Unternehmen berichteten außerdem von weniger Verpackungsmüll und einer verbesserten Einhaltung von Umweltauflagen, was zu einer Stärkung des Unternehmensimages führte.

Nachhaltige und langlebige Verpackungslösungen steigern zwar die Effizienz und senken die Kosten, ihre Wirkung hängt jedoch von kontinuierlicher Materialinnovation, der Einhaltung gesetzlicher Vorschriften und der breiten Akzeptanz in der Branche ab. Hersteller müssen sich auf leichte, recycelbare und skalierbare Designs konzentrieren, um die wachsende Nachfrage optimal zu nutzen. Kontinuierliche Forschung und Entwicklung im Bereich robusterer und nachhaltigerer Materialien wird die Marktchancen weiter ausbauen.

Marktdynamik der industriellen Holz- und Metallverpackungen

Treiber

„Steigende Nachfrage nach nachhaltigen und effizienten Verpackungslösungen“

Der zunehmende Fokus auf ökologische Nachhaltigkeit und Kreislaufwirtschaft treibt die Nachfrage nach Holz- und Metallverpackungen an. Unternehmen suchen verstärkt nach umweltfreundlichen, wiederverwendbaren und recycelbaren Lösungen, um Umweltauflagen zu erfüllen und den Erwartungen der Verbraucher gerecht zu werden. Der Wandel hin zu grüner Logistik und nachhaltigen Lieferketten fördert die Akzeptanz dieser Technologien in globalen Branchen zusätzlich.

Die Industrie erkennt zunehmend die betrieblichen Vorteile langlebiger und standardisierter Verpackungen, darunter weniger Produktschäden, effizientere Transporte und geringere Logistikkosten. Dieses Bewusstsein fördert Investitionen in hochwertige Verpackungslösungen aus Holz und Metall. Die Möglichkeit, Verpackungsmaterialien wiederzuverwenden und umzufunktionieren, hilft Unternehmen zudem, ihre Verpackungsausgaben insgesamt zu reduzieren.

Staatliche Initiativen und regulatorische Rahmenbedingungen zur Förderung nachhaltiger Verpackungspraktiken haben deren Akzeptanz in allen Industriezweigen gestärkt. Von verbindlichen Verpackungsstandards bis hin zu Anreizen für Nachhaltigkeit – unterstützende Maßnahmen beschleunigen das Marktwachstum. Die Einhaltung gesetzlicher Vorschriften in Regionen wie der EU und Nordamerika ermutigt Hersteller, innovative Verpackungslösungen aus Holz und Metall einzuführen, um Strafen zu vermeiden.

Beispielsweise führte die Europäische Union 2022 aktualisierte Verpackungsvorschriften ein, die Recyclingfähigkeit und Materialeffizienz in den Vordergrund stellten. Dies veranlasste Hersteller, entlang der gesamten Lieferkette Verpackungslösungen aus Metall und Holzwerkstoffen einzusetzen. Unternehmen berichteten von verbesserter Einhaltung der Vorschriften, weniger Abfall und einer höheren Logistikeffizienz infolge dieser Vorgaben.

• While sustainability and operational efficiency are key growth drivers, adoption depends on material innovation, cost-effectiveness, and compatibility with modern industrial logistics. Continuous collaboration between manufacturers, suppliers, and regulatory bodies is vital to ensure solutions meet both environmental and operational requirements

Restraint/Challenge

“High Material Costs and Limited Availability of Raw Materials”

• The high cost of premium wood and metal materials, particularly for treated or engineered products, limits adoption among small and mid-sized industrial operators. Upfront investment for durable packaging can be a significant barrier to entry. In addition, fluctuating raw material prices can affect profit margins, making budgeting challenging for smaller firms

• Supply chain disruptions and limited availability of sustainably sourced raw materials restrict the production and timely delivery of wood and metal packaging. This can affect industries that rely on just-in-time manufacturing and global logistics. Delays in sourcing certified wood or specialty metals can lead to production slowdowns and increased operational costs

• Market penetration is further constrained by the need for specialized handling and storage of metal containers and engineered wood pallets. Many facilities require additional infrastructure to store, maintain, and transport these packaging solutions safely. Training staff to handle heavy or fragile packaging components also adds to operational complexity and costs

• For instance, in 2023, several packaging manufacturers in Asia-Pacific reported delays and increased costs due to raw material shortages and rising lumber and steel prices, affecting market expansion. The shortage led some companies to seek alternative suppliers, driving up procurement costs and slowing adoption of new packaging solutions

• While industrial wood and metal packaging technologies continue to advance, addressing cost, supply, and infrastructure challenges is essential to unlock the market’s full growth potential. Strategic partnerships, local sourcing, and investment in alternative sustainable materials could mitigate these constraints and enhance market resilience

Industrial Wood and Metal Packaging Market Scope

The market is segmented on the basis of material type, packaging type, and end-user industry.

• By Packaging Type

On the basis of packaging type, the market is segmented into pallets, crates, drums, barrels, and others. The pallets segment held the largest market share in 2025 due to its extensive use in warehousing, storage, and transportation, providing easy handling and compatibility with material handling systems. Pallets offer standardized dimensions, which simplify stacking, loading, and shipping across global supply chains. Their durability and reusability reduce operational costs and minimize product damage during transit.

The drums segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand in chemical, pharmaceutical, and food industries for safe and durable liquid containment solutions. Drums offer leak-proof storage, stackability, and compliance with industry regulations, making them highly suitable for industrial logistics.

• By End-User Industry

On the basis of end-user industry, the market is segmented into food and beverage, chemicals and petrochemicals, pharmaceuticals, automotive, construction, and others. The food and beverage segment held the largest market revenue share in 2025, fueled by the need for hygienic, durable, and transport-efficient packaging solutions.

The chemicals and petrochemicals segment is expected to witness the fastest growth rate from 2026 to 2033, driven by strict regulations regarding safe storage and transportation of hazardous materials. Industries increasingly prefer metal and reinforced wood packaging for compliance, durability, and operational efficiency.

Industrial Wood and Metal Packaging Market Regional Analysis

• North America dominated the industrial wood and metal packaging market with the largest revenue share of 38.75% in 2025, driven by the presence of large-scale manufacturing and logistics industries, along with increasing emphasis on sustainable and reusable packaging solutions

• Businesses in the region highly value durable, stackable, and modular packaging solutions that enhance operational efficiency, reduce product damage, and optimize warehouse space

• This widespread adoption is further supported by strong industrial infrastructure, technological advancements in material handling, and stringent regulations on packaging sustainability, establishing wood and metal packaging as a preferred choice across multiple industrial sectors

U.S. Industrial Wood and Metal Packaging Market Insight

The U.S. market captured the largest revenue share in 2025 within North America, fueled by growing demand for engineered wood pallets, metal drums, and reusable containers across food and beverage, chemical, and pharmaceutical industries. Companies are increasingly investing in durable packaging solutions to reduce logistics costs, prevent product damage, and enhance supply chain efficiency. Moreover, government initiatives promoting sustainable packaging and recycling practices are significantly contributing to market expansion.

Europe Industrial Wood and Metal Packaging Market Insight

The Europe market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict regulations on packaging sustainability, rising industrial automation, and the increasing adoption of reusable and modular packaging solutions. Industries across automotive, chemicals, and construction sectors are implementing engineered wood and metal containers to improve transport efficiency, reduce product loss, and comply with circular economy practices. Urbanization, advanced material handling systems, and growing environmental awareness are further accelerating market adoption.

U.K. Industrial Wood and Metal Packaging Market Insight

The U.K. market is expected to witness significant growth from 2026 to 2033, driven by increasing demand for sustainable and standardized packaging in industrial operations. Companies are focusing on reducing packaging waste, improving logistics efficiency, and complying with environmental regulations through the adoption of engineered wood pallets, crates, and metal drums. The country’s robust industrial base and growing trend of green manufacturing practices are further supporting market expansion.

Germany Industrial Wood and Metal Packaging Market Insight

The Germany market is expected to witness strong growth from 2026 to 2033, fueled by the country’s focus on sustainable industrial practices and innovative packaging solutions. Industrial operators are adopting durable wood and metal packaging to reduce product damage, streamline supply chains, and comply with environmental regulations. Integration with automated logistics systems and advanced handling equipment is also becoming increasingly common, enhancing operational efficiency and market adoption.

Asia-Pacific Industrial Wood and Metal Packaging Market Insight

The Asia-Pacific market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing industrialization, rising exports, and growing awareness of sustainable packaging solutions in countries such as China, India, and Japan. The adoption of engineered wood pallets, metal drums, and modular containers is rising across food processing, chemicals, and automotive industries. Furthermore, as APAC emerges as a major manufacturing hub for industrial packaging components, affordability, scalability, and accessibility of wood and metal packaging solutions are expanding to a wider industrial base.

Japan Industrial Wood and Metal Packaging Market Insight

The Japan market is expected to witness strong growth from 2026 to 2033, owing to the country’s focus on efficiency, automation, and environmentally responsible packaging solutions. Companies are investing in high-quality wood and metal packaging to protect products, optimize warehouse storage, and streamline supply chains. The increasing integration of packaging solutions with automated handling systems and the trend toward sustainable manufacturing are driving market adoption in both domestic and export-oriented industries.

Einblick in den chinesischen Markt für industrielle Holz- und Metallverpackungen

Der chinesische Markt wird 2025 den größten Umsatzanteil im asiatisch-pazifischen Raum erzielen. Dies ist auf die breit gefächerte Industriebasis des Landes, das rasante Wachstum der Fertigungsindustrie und die zunehmenden Exportaktivitäten zurückzuführen. Die Nachfrage nach langlebigen, wiederverwendbaren und modularen Holz- und Metallverpackungen wächst in den Bereichen Lebensmittel und Getränke, Chemie und Automobil. Das Streben nach nachhaltigen Praktiken, gepaart mit kostengünstiger lokaler Produktion und starken inländischen Herstellern, sind die Schlüsselfaktoren für das Marktwachstum in China.

Marktanteil der industriellen Holz- und Metallverpackungen

Die Industrie für Holz- und Metallverpackungen wird hauptsächlich von etablierten Unternehmen dominiert, darunter:

- IFCO Systems GmbH (Deutschland)

- Greif, Inc. (USA)

- Conitex Sonoco (USA)

- Schäfer Containersysteme (Deutschland)

- BWAY Corporation (USA)

- Pall-Ex Ltd (UK)

- CABKA Group GmbH (Deutschland)

- Mauser Packaging Solutions (Deutschland)

- ORBIS Corporation (USA)

- Linpac Packaging Ltd (UK)

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.