Middle East And Africa Glyoxal Market

Marktgröße in Milliarden USD

CAGR :

%

USD

54.00 Million

USD

76.64 Million

2025

2033

USD

54.00 Million

USD

76.64 Million

2025

2033

| 2026 –2033 | |

| USD 54.00 Million | |

| USD 76.64 Million | |

| % | |

|

Mittlere Ost- und Afrika Glyoxalmarktsegmentierung, Methylgrad (Industrial Grad, Pharmaceutical Grade), durch Reinheit (90%–99%, 40%–60%, Andere), Herstellungsverfahren (katalytische Oxidation von Ethylenglykol, Oxidation von Acetylen, Andere), Verpackung (Bottles, Jerrycans, Composite IBC, Bulk)

Was ist der Nahe Osten und Afrika Glyoxal Markt Größe und Überblick

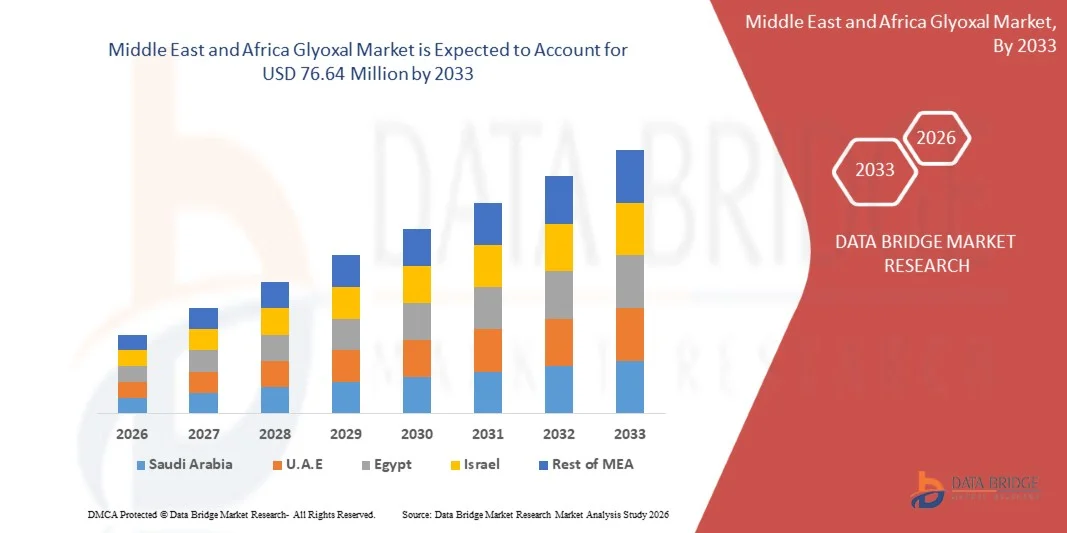

- Wie pro Data Bridge Market Research Analysis wird der Nahe Osten und Afrika Glyoxal Market voraussichtlich erreichen76,64 Mio. USD bis 2033vonUSD 54.00 Millionen im Jahr 2025mit einemCAGR von 4,5%in der Prognosezeit von 2026 bis 2033.

- Der Middle East and Africa Glyoxal Market zeigt ein stetiges Wachstum, das durch seinen wachsenden Einsatz in der Textil-, Papier-, Leder-, Pharma-, Agrochemie- und Öl- und Gasindustrie getrieben wird, wo Glyoxal für seine Vernetzungs-, Binde- und Veredelungseigenschaften geschätzt wird.

- Darüber hinaus verstärkt die wachsende Nachfrage nach preisgünstigen chemischen Lösungen, einschließlich kundenspezifischer Glyoxal-Formulierungen für spezifische industrielle Prozesse und nachgelagerte Integration innerhalb chemischer Lieferketten, die Marktreife und unterstützt langfristiges Wachstum in den entwickelten und Schwellenländern.

Marktgröße und Prognose

- Naher Osten und Afrika Marktwert (2033):76,64 Mio. USD

- Voraussichtlicher Marktwert (2025):54.00 Mio. USD

- Wettervorhersage CAGR (2026–2033): 4.5%

Naher Osten und Afrika Glyoxalmarktanalyse

- Der Nahost- und Afrika-Glyoxalmarkt bietet vielfältige Branchen wie Textilien, Papier, Harze, Pharmazeutika, Kosmetik und Wasserbehandlung. Die Nachfrage wird durch ihre starken Vernetzungseigenschaften und Rolle als zentrales Zwischenprodukt in speziellen und leistungschemischen Formulierungen getrieben.

- Die steigenden Textilveredelungsaktivitäten, der zunehmende Verbrauch von Papierverpackungen und der zunehmende Einsatz von umweltfreundlichen Harzen sind große Nachfragetreiber. Erweiterung der pharmazeutischen Fertigung und strengere Abwasserbehandlungsvorschriften unterstützen den anhaltenden Glyoxalverbrauch weltweit.

- Der Markt verfügt über eine Mischung aus multinationalen Chemieherstellern und regionalen Herstellern. Der Wettbewerb basiert auf Produktreinheit, anwendungsspezifischen Güten, Preisgestaltung, Lieferzuverlässigkeit und Einhaltung von Umwelt- und Sicherheitsvorschriften in Schlüsselbranchen.

- Saudi-Arabien dominiert den Nahen Osten und Afrika-Glyoxalmarkt, unterstützt durch große Produktionskapazität, geringe Produktionskosten und reichliche Rohstoffverfügbarkeit. Die starke nachgelagerte Nachfrage aus Textil-, Harz-, Papier- und Lederindustrie sowie eine umfangreiche Chemie-Versorgungskette verstärkt weiter ihre Führung.

- Der US-amerikanische Naher Osten und Afrika-Glyoxalmarkt dürfte von 2026 bis 2033 mit einem CAGR von rund 5,4% wachsen, der durch steigende Nachfrage aus der Textil- und Agrarindustrie und zunehmenden Einsatz in Harzen und Beschichtungen für industrielle Anwendungen angetrieben wird. Ausbau der Industrialisierung und Urbanisierung in der Region weiteres Wachstum des Brennstoffmarktes.

- Im Jahr 2025 wird erwartet, dass das Segment Industrial Grade durch seinen weit verbreiteten Einsatz in der Herstellung von Harzen, Klebstoffen und Papierbehandlungschemikalien den Mittleren Osten und Afrika-Glyoxalmarkt dominiert. Das Segment profitiert von der hohen Nachfrage in großtechnischen Anwendungen und der Wirtschaftlichkeit für die Massenproduktion, so dass es die bevorzugte Wahl gegenüber anderen Sorten.

Bericht Umfang und Mittlerer Osten und Afrika Glyoxalmarktsegmentierung

|

Attribute |

Naher Osten und Afrika Glyoxalmarkt Einblicke |

|

Verdeckte Segmente |

|

|

Überarbeitete Länder |

Naher Osten und Afrika

|

|

Key Market Players |

|

|

Marktmöglichkeiten |

|

|

Daten Infos zum Wert hinzugefügt |

Neben den Markteinblicken wie Marktwert, Wachstumsrate, Marktsegmente, geographischer Erfassung, Marktteilnehmer und Marktszenario umfasst der vom Data Bridge Market Research Team kuratierte Marktbericht eine tiefgreifende Expertenanalyse, Import/Export-Analyse, Preisanalyse, Produktionsverbrauchsanalyse und pestle-Analyse. |

Was ist der wichtigste Trend im Nahen Osten und Afrika Glyoxalmarkt

„Integration mit intelligenten Fertigungs-, Lager- und E-Commerce-Verpackungsökosystemen„

- Glyoxal wird zunehmend in intelligenten Fertigungsumgebungen für Textilveredelung, Papierbehandlung und Harzanwendungen eingesetzt, um einheitliche Qualitätskontrolle, Prozessoptimierung und datengesteuerte Produktionsentscheidungen im Einklang mit Industrie 4.0-Initiativen zu unterstützen.

- In Lager- und Verarbeitungsanlagen helfen glyoxalbasierte Formulierungen bei der Materialstabilisierung, der Beschichtungsleistung und der Feuchtigkeitsbeständigkeit, der Verbesserung der Handlingeffizienz, der Lagerstabilität und der nachgelagerten Verarbeitungssicherheit.

- Der zunehmende Einsatz von Glyoxal in Verpackungsklebern, Papierverstärkung und Oberflächenbehandlungen unterstützt den Ausbau des E-Commerce durch die Verbesserung der Verpackungsintegrität, der Laststabilität und des Produktschutzes in Logistiknetzwerken.

Für das Gericht

- Im Januar 2025 wurden glyoxalbasierte chemische Lösungen zunehmend in automatisierte Textil- und Papierverarbeitungslinien integriert, kombiniert mit fortschrittlichen Prozesskontrollen und digitalen Überwachungssystemen, um Effizienz, Konsistenz und Nachhaltigkeit im industriellen Betrieb zu verbessern und die Rolle von glyoxal in der nächsten Generation von Fertigungsökosystemen hervorzuheben.

- Neuere Branchenentwicklungen zeigen eine steigende Übernahme spezieller aldehydbasierter Chemikalien, einschließlich Glyoxal, in leistungsstarken Verpackungs- und Industrieanwendungen, da E-Commerce- und Logistikvolumina wachsen und ihre wachsende Rolle jenseits traditioneller Endverwendungssektoren stärken.

Naher Osten und Afrika Glyoxalmarktdynamik

Fahrer

„Verbesserung der industriellen Modernisierung und leistungsorientierten Anforderungen an chemische Anwendungen„

- Der Industriebereich Naher Osten und Afrika zeigt eine beschleunigte Einführung von glyoxalbasierten Lösungen, die durch immer komplexere Leistungsanforderungen an Textil-, Papier-, Harz-, Leder- und Spezialchemieanwendungen angetrieben werden. Die Hersteller priorisieren Glyoxal für ihre Vernetzungs-, Binde- und Finisheigenschaften, die die Produktstärke, Haltbarkeit und Funktionsleistung verbessern. Da industrielle Prozesse zu einer höheren Effizienz und Qualitätskonsistenz entwickeln, wächst die Nachfrage nach chemischen Formulierungen, die kontrollierte Reaktionen, reduzierte Emissionen und verbesserte Endproduktsicherheit unterstützen.

- Die zunehmende Rolle von Glyoxal innerhalb der industriellen Modernisierungsinitiativen hat ein dynamisches Umfeld für chemische Hersteller geschaffen, um zu Innovationen zu führen, was zu Fortschritten in der Formulierung Reinheit, Anwendungsvielfalt und Prozessverträglichkeit führt. Als Reaktion auf diese bedarfsgerechte Verschiebung investieren die Hersteller in die Entwicklung von kundenspezifischen, auf spezifische Endverwendungsanforderungen zugeschnittenen Glyoxal-Typen, darunter auch Low-Formaldehyd-Systeme, Spezialharze und leistungsstarke Textilbehandlungen.

- Diese Innovationen werden größtenteils von den betrieblichen Erfordernissen moderner Industrien angetrieben, die anpassungsfähige chemische Lösungen erfordern, die unter unterschiedlichen Verarbeitungsbedingungen und regulatorischen Zwängen zuverlässig durchführbar sind. Da die Industrien weiterhin glyoxal in fortgeschrittene Fertigungs- und Finish-Workflows integrieren, beeinflusst diese Dynamik nicht nur die Investitionsstrategien von Lieferanten, sondern verstärkt auch die Rolle von glyoxal als kritisches Zwischenprodukt zur Steigerung der industriellen Produktivität und der Materialleistung.

Rechtssachen

- Im September 2023 hoben die Industriepublikationen eine verstärkte Einführung von Glyoxal in fortgeschrittenen Textilveredelungsprozessen hervor, die darauf abzielten, die Festigkeit und die Resistenz der Gewebe zu verbessern und gleichzeitig strengere Umweltnormen zu erfüllen.

- Seit Februar 2024 zeigten die Erkenntnisse der chemischen Industrie, dass die Hersteller im Nahen Osten und Afrika den Einsatz von Glyoxal-basierten Harzen und Papierbehandlungslösungen zur Unterstützung nachhaltiger Produktionspraktiken verstärkten und die Abhängigkeit von höhertoxischen Alternativen verringern.

- Im Februar 2025 betonten die regionalen Industrieentwicklungen in ganz Asien-Pazifik die wachsenden Investitionen in die Spezial-Aldehyd-Produktion, einschließlich Glyoxal, um die steigende Nachfrage aus den Bereichen Verpackung, Bau und Industrieproduktion zu erfüllen, die sich auf Leistungssteigerung und regulatorische Ausrichtung konzentrierten.

- Die zunehmende Übernahme von Glyoxal im globalen Industriesektor unterstreicht seine zunehmende Bedeutung als multifunktionale chemische Lösung, die auf die Entwicklung von Leistungs-, Effizienz- und Nachhaltigkeitsanforderungen ausgerichtet ist. Da die Industrien weiterhin in Richtung qualitativ hochwertiger Produktionen und kontrollierteren Fertigungsprozessen voranschreiten, positionieren sie die Vernetzungs-, Binde- und Veredelungsfähigkeit von glyoxal als kritischer Energator für verbesserte Materialstärke, Haltbarkeit und funktionale Konsistenz.

- Die fortschreitenden Innovationen in der Formulierungsreinheit und anwendungsspezifischer Anpassung verstärken ihre Relevanz für Textilien, Papier, Harze, Leder und Spezialchemikalien weiter. Unterstützt durch steigende Investitionen, regulatorische Ausrichtungsbemühungen und den Ausbau industrieller Anwendungsfälle in den großen Regionen wird glyoxal eine strategisch bedeutsame Rolle bei der Förderung der industriellen Produktivität und der Unterstützung des Übergangs zu nachhaltigeren und leistungsfähigeren Herstellungspraktiken erwarten.

Zurückhaltung/Challenge

„Lack of Harmonized Middle East and Africa Regulatory Frameworks for Chemical Manufacturing and Usage“

- Das Fehlen harmonisierter Vorschriften des Nahen Ostens und Afrikas zur chemischen Herstellung, Handhabung und Endverwendung stellt eine bemerkenswerte Herausforderung für den Nahen Osten und den Afrika-Glyoxalmarkt dar, da sich die regulatorischen Anforderungen in Ländern und Regionen deutlich unterscheiden.

- Die Regulierungsbehörden wenden unterschiedliche Normen in Bezug auf chemische Einstufung, zulässige Expositionsgrenzen, Umweltverträglichkeit, Kennzeichnung, Transport und Abwasserableitung an. Diese regulatorische Fragmentierung erzwingt glyoxale Hersteller und nachgeschaltete Anwender, Formulierungen, Dokumentationen, Sicherheitsprotokolle und Compliance-Strategien für jeden Markt zu ändern, die operative Komplexität zu erhöhen, Compliance-Kosten und Zeit auf den Markt zu bringen.

- Infolgedessen stehen Unternehmen vor Einschränkungen bei der Skalierung von Glyoxalproduktion und -verteilung Naher Osten und Afrika, insbesondere bei grenzüberschreitenden Handels- und multinationalen Lieferketten, die Textil-, Papier-, Harz- und Spezialchemieanwendungen bedienen.

Rechtssachen

- Ende 2025 führten die regionalen Umweltbehörden in Asien und dem Mittleren Osten und Afrika unterschiedliche Compliance-Anforderungen für aldehydbasierte Chemikalien, einschließlich Glyoxal, mit Variationen der Emissionsschwellen und Meldepflichten ein, die regulatorische Unstimmigkeiten illustrieren, die standardisierte Produktions- und Exportstrategien komplizieren.

- Im Mai 2025 erzwingten nationale und lokale Regulierungsbehörden in aufstrebenden Märkten strengere chemische Handhabungs- und Transportbeschränkungen über die bestehenden zentralen Richtlinien hinaus, wodurch vorübergehende operative Störungen für Glyoxalhersteller und -Vertreiber geschaffen wurden, die während der Durchsetzungsperiode zusätzliche Genehmigungen erhalten und Logistik-Workflows ändern mussten.

- Der Mangel an harmonisierten globalen Regulierungsrahmen stellt weiterhin eine strukturelle Herausforderung für den globalen Nahen Osten und Afrika-Glyoxalmarkt dar, wodurch die Leichtigkeit der standardisierten Produktion, Verteilung und grenzüberschreitenden Handel begrenzt wird. Divergente regionale Anforderungen in Bezug auf chemische Einstufung, Umweltverträglichkeit, Handhabung und Transport erhöhen die operative Komplexität und erhöhen die Compliance-Kosten für Hersteller und nachgeschaltete Anwender.

- Diese regulatorischen Inkonsistenzen verlangsamen nicht nur Markteintritt und Skalierbarkeit, sondern erfordern auch häufige Anpassungen an Formulierungen, Dokumentationen und Logistikstrategien in Regionen. Infolgedessen bleibt die Regulierungsfragmentation eine zentrale Voraussetzung für die globale Markterweiterung und unterstreicht die Notwendigkeit einer stärkeren Ausrichtung und Transparenz in der chemischen Governance, um effizientere internationale Lieferketten und nachhaltiges Marktwachstum zu unterstützen.

Mittlerer Osten und Afrika

Der Markt wird auf der Grundlage von Qualität, Reinheit, Produktionsprozess, Verpackung Anwendung, Endverwendung Chemikalien und Endverwendung Industrie

Von Grad

Basierend auf der Qualität wird der Nahe Osten und Afrika Glyoxalmarkt in erster Linie in Industrial Grade und Pharmaceutical Grade segmentiert.

Bis 2026 wird das Segment Industrial Grade den Markt dominieren, was 82,29% des Gesamtanteils ausmacht. Diese Dominanz ist auf seine umfangreichen Anwendungen in verschiedenen Branchen zurückzuführen, darunter Textilien, Papierverarbeitung, Harze, Lederbehandlung und Wasserbehandlung. Der hochvolumige Verbrauch von Industrie-Glyoxal wird durch seine Wirtschaftlichkeit und Effizienz im Großbetrieb weiter unterstützt. Darüber hinaus treibt die rasche Expansion der Industrie- und Fertigungssektoren in der Region Naher Osten und Afrika eine starke und anhaltende Nachfrage. Infolgedessen wird erwartet, dass das industrielle Glyoxal der entscheidende Wachstumstreiber auf dem regionalen Markt bleibt.

Das Segment Pharmazeutische Grade im Nahen Osten und Afrika Glyoxal Markt wird von 2026 bis 2033 am schnellsten wachsen, angetrieben durch steigende Nachfrage in der Pharmasynthese, strenge regulatorische Anforderungen an hochreine Chemikalien, und die Erweiterung der fortschrittlichen Arzneimittelherstellung und Spezialanwendungen. Diese Faktoren erhöhen die Annahme von qualitativ hochwertigem Glyoxal in APIs und innovativen Arzneimittelformulierungen.

Mit der Reinheit

Auf der Grundlage der Reinheit wird der Nahe Osten und Afrika Glyoxalmarkt zu 90%–99%, 40%–60% und Anderen segmentiert.

Bis 2026 wird erwartet, dass das Segment der Reinheit von 40% bis 60% den Markt dominiert, was 72,25 % des Gesamtanteils ausmacht. Die Prominenz dieses Segments ist auf seine überlegene Leistung, höhere Reaktivität und Eignung für fortgeschrittene Anwendungen in Pharma, Spezialharzen, Textilien und Kosmetik zurückzuführen. Seine gleichbleibende Qualität, zusammen mit der Einhaltung strenger Branchenstandards, treibt weiterhin starke und anhaltende Nachfrage. Darüber hinaus macht die Balance zwischen Effektivität und Kosteneffizienz diesen Reinheitsbereich von Herstellern sehr bevorzugt. Infolgedessen wird das 40%–60% Reinheitssegment als primärer Beitrag für das Wachstum im Nahen Osten und im Afrika Glyoxalmarkt prognostiziert.

Das 90%-99% Reinheitssegment im Nahen Osten und Afrika Glyoxal Markt wird erwartet, dass das schnellste Wachstum von 2026 bis 2033, angetrieben durch seine weit verbreitete Verwendung in pharmazeutischen und speziellen chemischen Anwendungen, die hohe Reinheit Glyoxal erfordern, sowie steigende Nachfrage nach fortschrittlichen Arzneimittelformulierungen und regulatorischen Produktionsverfahren.

durch Produktionsverfahren

Auf Basis des Herstellungsverfahrens wird der Nahe Osten und Afrika Glyoxalmarkt in die katalytische Oxidation von Ethylenglykol, Oxidation von Acetylen und anderen segmentiert.

Bis 2026 wird erwartet, dass das Segment der katalytischen Oxidation von Ethylenglykol den Markt dominiert, was 90.15% des Gesamtanteils ausmacht. Die Dominanz dieses Segments wird durch seine höhere Produktionseffizienz, bessere Ertragskontrolle und geringere Verunreinigungen im Vergleich zu Acetylen-basierten Prozessen angetrieben. Darüber hinaus bietet es eine verbesserte Sicherheit und ist umweltfreundlicher und eignet sich hervorragend für die großtechnische Fertigung. Die Wirtschaftlichkeit und Skalierbarkeit dieses Verfahrens stärkt seine Vorliebe bei den Herstellern weiter. Dadurch wird die katalytische Oxidationsstrecke als primärer Wachstumstreiber im Nahen Osten und im Afrika-Glyoxalmarkt gepolt.

Das Segment „Oxidation of Acetylen“ im Nahen Osten und Afrika Glyoxal Markt wird erwartet, dass das schnellste Wachstum von 2026 bis 2033, angetrieben durch seine Fähigkeit, hochreines Glyoxal für pharmazeutische und spezielle chemische Anwendungen, sowie steigende Nachfrage nach fortgeschrittenen Arzneimittelformulierungen und Einhaltung strenger Qualitäts- und Regulierungsstandards zu produzieren.

Durch Verpackung

Auf der Grundlage der Verpackung wird der Nahe Osten und Afrika Glyoxalmarkt in Drums, Composite IBC, Bulk, Jerrycans und Flaschen segmentiert.

Bis 2026 wird erwartet, dass das Segment Drums den Markt dominiert, was 41,53% des Gesamtanteils ausmacht. Diese Dominanz ist auf ihre Vielseitigkeit, einfache Handhabung und sichere Lagerung, insbesondere für Kleinmengenanwendungen zurückzuführen. Flaschen eignen sich besonders fürArzneimittel, Kosmetika und spezielle chemische Anwendungen, wo Präzision und Sicherheit kritisch sind. Darüber hinaus treiben ihre breite Verfügbarkeit und kostengünstige Produktion eine starke Übernahme in allen Branchen. Die Bequemlichkeit und Zuverlässigkeit von Flaschenverpackungen machen es zu einer bevorzugten Wahl für Hersteller und Endverbraucher gleichermaßen.

Das Verpackungssegment „Composite IBC“ im Nahen Osten und Afrika Glyoxal Markt wird erwartet, dass das schnellste Wachstum von 2026 bis 2033, angetrieben durch seine Effizienz bei der Lagerung und dem Transport von Massenchemikalien, erhöhte Sicherheit und chemische Beständigkeit sowie steigende Nachfrage von Pharma-, Spezialchemie- und Industrieanwendern, die zuverlässige, großkapazitätsfähige Verpackungslösungen benötigen, zu beobachten ist.

Anwendung

Auf der Grundlage der Verpackung wird der Nahe Osten und Afrika Glyoxalmarkt in Application Cross-Linking, Chemical Intermediates, Others segmentiert.

Bis 2026 wird erwartet, dass das Segment Cross-Linking den Markt dominiert, was 66,19% des Gesamtanteils ausmacht. Diese Dominanz ist auf ihre Vielseitigkeit, einfache Handhabung und sichere Lagerung, insbesondere für Kleinmengenanwendungen zurückzuführen. Flaschen eignen sich besonders für Pharmazeutika, Kosmetika und spezielle chemische Anwendungen, wo Präzision und Sicherheit kritisch sind. Darüber hinaus treiben ihre breite Verfügbarkeit und kostengünstige Produktion eine starke Übernahme in allen Branchen. Die Bequemlichkeit und Zuverlässigkeit von Flaschenverpackungen machen es zu einer bevorzugten Wahl für Hersteller und Endverbraucher gleichermaßen.

Das Anwendungssegment Chemical Intermediates im Nahen Osten und Afrika Glyoxal Market wird von 2026 bis 2033 das am schnellsten wachsende Segment sein, das durch steigende Nachfrage nach Harzen, Polymeren und Spezialchemikalien, die Expansion der chemischen Fertigungsindustrie und die Verwendung von Glyoxal als vielseitiges Vernetzungs- und reaktives Zwischenprodukt in industriellen und Spezialanwendungen angetrieben wird.

Von End-Use Chemicals

Basierend auf Endverwendungschemikalien wird der Nahe Osten und Afrika Glyoxalmarkt in Dihydroxyethylen Urea (DHEU), 2-Imidazolidinon, Glyoxalatiertes Polyacrylamid (GPAM), Glyoxylsäure, Glyoxalatiertem Starch, Glyoxalphenol Resin, Glyoxal Urea Resin, Ethylenglykoldiformiat, Urea-Glyoxal Concentrat, Quinoxacoldium

Bis 2026 wird erwartet, dass das Segment Dihydroxyethylen Urea (DHEU) den Markt dominiert, was 22.12% des Gesamtanteils ausmacht. Seine Dominanz wird durch seine breite Anwendbarkeit in der Textilveredelung, Papierbehandlung und Harzherstellung angetrieben. Das Segment profitiert von hoher Reaktivität, gleichbleibender Leistung und Kompatibilität mit verschiedenen industriellen Prozessen. Darüber hinaus unterstützt die wachsende Nachfrage nach hochwertigen Textilien und Spezialchemieprodukten im Nahen Osten und Afrika seine starke Marktposition. Die Wirtschaftlichkeit und Effizienz der DHEU stärken ihre Präferenzen bei Herstellern und Endverbrauchern weiter.

Das 2-Imidazolidinon-Endverwendungs-Chemikalien-Segment im Nahen Osten und Afrika-Glyoxalmarkt wird von 2026 bis 2033 am schnellsten wachsen und wird durch den zunehmenden Einsatz in Pharma-, Agrochemikalien- und Spezialchemieanwendungen angetrieben. Sein Wachstum wird durch die steigende Nachfrage nach hochreinem Glyoxal als zentrales Zwischenprodukt bei der Synthese von 2-Imidazolidinon für fortgeschrittene Formulierungen und regulatorisch-konforme chemische Produktion getrieben.

Von End-User

Auf der Grundlage des Endverbrauchers wird der Nahe Osten und Afrika Glyoxalmarkt in Textil, Pulp und Papier, Leder, Farben und Beschichtungen, Wasseraufbereitung, Pharmazeutika, Haushaltsprodukte, Kosmetik und persönliche Pflege, Verpackung, Elektro und Elektronik, Öl und Gas und andere segmentiert.

Bis 2026 wird erwartet, dass das Segment Textile den Markt dominiert, was 37,05% des Gesamtanteils ausmacht. Dieses Wachstum wird durch seinen weit verbreiteten Einsatz in der Stoffveredelung, Faltenbeständigkeit und faltenfesten Behandlungen angetrieben. Die zunehmende Nachfrage nach langlebigen und hochwertigen Textilien, verbunden mit einer schnellen Expansion in der Bekleidungs- und Haushaltsausstattungsindustrie, unterstützt das Marktwachstum. Zusätzlich erhöht die steigende Verbraucherpräferenz für Premium- und langlebige Stoffe die Einführung von glyoxalbasierten Lösungen. Dadurch wird das Segment Textile als Schlüsselfaktor für den Nahen Osten und den Afrika-Glyoxalmarkt betrachtet.

Das Segment Pulp und Paper Endbenutzer im Nahen Osten und Afrika Glyoxal Markt wird von 2026 bis 2033 am schnellsten wachsen, angetrieben durch die steigende Nachfrage nach Nassfestharzen und chemischen Additiven, die die Papierstabilität und Qualität verbessern. Das Wachstum wird durch den Ausbau der Papier- und Verpackungsindustrie und den Übergang zu leistungsstarken, nachhaltigen Papierprodukten unterstützt.

Naher Osten und Afrika Glyoxalmarkt Einblick

- Saudi-Arabien dominiert den regionalen Markt, angetrieben durch seine robuste petrochemische Basis, große Produktionskapazität und starke nachgelagerte Nachfrage. Die laufenden Investitionen in nachhaltige und hochreine chemische Lösungen unterstützen die langfristige regionale Markterweiterung.

- Der Saudi-Arabien Mittlerer Osten und Afrika-Glyoxalmarkt expandiert rasant, angetrieben durch große chemische Produktionskapazität, starke Nachfrage aus Textilien, Papier, Bauchemikalien und Agrarchemikalien und unterstützende Regierungspolitiken. Technologische Weiterentwicklungen und kostspielige Produktionsposition China als bedeutender Mittlerer Osten und Afrika-Glyoxallieferant mit erheblichem Wachstumspotenzial.

U.A.E. Naher Osten und Afrika Glyoxalmarkt Einblick

Der US-A.E Middle East and Africa Glyoxal Market zeigt ein starkes Wachstum, unterstützt durch den Ausbau der Textil- und Papierindustrie, die steigende chemische Produktionsaktivität und die zunehmende Einführung von Glyoxal in Harzen und Spezialanwendungen. Die Regierungsinitiativen zur Förderung der inländischen chemischen Produktion und des industriellen Wachstums verstärken weiterhin die Marktdynamik.

Mittlerer Osten und Afrika

Das Glyoxal wird in erster Linie von etablierten Unternehmen geleitet, darunter:

- Amzole India Pvt. Ltd (Indien)

- Asis Scientific Pty Ltd (Australien)

- Ataman Chemicals (Indien)

- BASF SE (Deutschland)

- Bidvest Chemical (Südafrika)

- Bisley Asia (M) Sdn Bhd (Malaysia)

- Eastman Chemical Company (USA)

- Fluorochem Limited (USA)

- Fujifilm Wako Pure Chemical Corporation (Japan)

- Glentham Life Sciences Limited (USA)

- GetChem Co., Ltd. (China)

- Hanna Instruments Ltd (USA)

- Himedia Laboratories (Indien)

- Kanto Kagaku (Japan)

- Kemira Oyj (Finnland)

- Merck KGaA (Deutschland)

- Meru Chem Pvt. Ltd (Indien)

- Muby Chemicals (Indien)

- Multichem Specialities Private Limited (Indien)

- Oakwood Products Inc. (USA)

- Otto Chemie Pvt. Ltd. (Indien)

- Oxford Lab Fine Chem LLP (Indien)

- Santa Cruz Biotechnology Inc. (USA)

- Sasol (Südafrika)

- Silver Fern Chemical, Inc. (USA)

- Thermo Fisher Scientific Inc. (USA)

- Univar Solutions LLC (USA)

- Weylchem International GmbH (Deutschland)

- Zhishang Chemical (China)

Neueste Entwicklungen im Nahen Osten und Afrika Glyoxalmarkt

- Im Oktober 2025 wurde Multichem Specialities Private Limited unter den Top 10 Specialty Chemical Distributors 2025 von Industry Outlook Magazine anerkannt, was seine Qualität, Innovation und zuverlässigen Service im Bereich der Spezialchemie hervorhebt. Im Juli 2025 organisierte das Unternehmen in Zusammenarbeit mit dem Breach Candy Hospital Trust auch einen erfolgreichen Blutspende-Antrieb, der Mitarbeiter und Community-Mitglieder zur Unterstützung des Gesundheitsbedarfs engagierte.

- Im Februar 2024 nahm Multichem Specialities Private Limited an Vitafoods Indien teil und verstärkte seine Präsenz im Segment Nutraceuticals und Spezialitäten und engagierte sich mit Kunden und Partnern, um ihr expandierendes chemisches Portfolio zu präsentieren.

- Im Oktober 2024 erweiterte Otto Chemie Pvt. Ltd. sein Portfolio an hochreinen Laborchemikalien und Reagenzien, was seine Präsenz in der Pharma-, Forschungs- und Industriebranche verbessert. Das Unternehmen verstärkte auch seine Vertriebsnetzwerk- und Lieferkettenkapazitäten, um die wachsende Nachfrage in Indien und internationalen Märkten zu decken.

- Im Juli 2024 organisierte Otto Chemie Pvt. Ltd. in Zusammenarbeit mit lokalen Krankenhäusern einen Blutspende- und Gesundheitsbewusstseinsantrieb, der das Engagement des Unternehmens im Bereich des Gemeinwohls und der Beteiligung der Arbeitnehmer an sozialen Verantwortungsinitiativen widerspiegelt.

- Oxford Lab Fine Chem LLP hat im März 2025 umweltfreundliche Verpackungslösungen und optimierte Abfallmanagement-Praktiken in den Produktions- und Distributionsprozessen implementiert und das Engagement des Unternehmens für eine nachhaltige und verantwortungsvolle chemische Fertigung gestärkt.

SKU-

Erhalten Sie Online-Zugriff auf den Bericht zur weltweit ersten Market Intelligence Cloud

- Interaktives Datenanalyse-Dashboard

- Unternehmensanalyse-Dashboard für Chancen mit hohem Wachstumspotenzial

- Zugriff für Research-Analysten für Anpassungen und Abfragen

- Konkurrenzanalyse mit interaktivem Dashboard

- Aktuelle Nachrichten, Updates und Trendanalyse

- Nutzen Sie die Leistungsfähigkeit der Benchmark-Analyse für eine umfassende Konkurrenzverfolgung

Inhaltsverzeichnis

1 EINLEITUNG

1.1 ZIELE DER STUDIE

1.2 MARKET DEFINITION

1.3 ÜBERBLICK ÜBER MIDDLE EAST UND AFRICA GLYOXALMARKT

1.4 LIMITATIONEN

1.5 MARKEITEN

2 MARKET SEGMENTATION

2.1 REGIERUNGEN

2.2 GEOGRAPHISCHE ANWENDUNGSBEREICH

2.3 JAHRE FÜR DIE STUDIE

2.4 KURZ UND PREISUNG

2.5 DBMR TRIPOD DATENWERTUNG MODEL

2.6 MULTIVARIAT MODELLEN

2.7 ERZEUGNISSE LEBENLINIEN

2.8 PRIMARY INTERVIEWS MIT STELLUNGNAHMEN

2.9 DBMR MARKET POSITION GRID

2.1 MARKET END USER COVERAGE GRID

2.11 GERICHTSHOFES

2.12 VERBRAUCHUNGEN

3 ZUSAMMENFASSUNG

4 VORSCHRIFTEN

4.1 MIDDLE EAST UND AFRICA GLYOXAL MARKET: VALUE CHAIN ANALYSIS

4.1.1 RAW MATERIAL & FEEDSTOCK SUPPLY (5%–10% VALUE SHARE)

4.1.2 VERARBEITUNG UND VERARBEITUNG (15%–25% VALUE SHARE)

4.1.3 VERTEILUNG & LOGISTICS (30%–40% VALUE SHARE)

4.1.4 END-USE INDUSTRIES & SALES CHANNELs (10%–20% VALUE SHARE)

4.2 WICHTIGSTEN ANALYSE

4.2.1 RAW MATERIALSOURCEN & VERFAHREN

4.2.2 VERARBEITUNG und ERZEUGNISSE (PRODUKTION)

4.2.3 SUPPLY CHAIN & DISTRIBUTION LOGISTICS (TRANSPORTATION)

4.2.4 RETAIL & COMMERCIAL BUYER CHANNELs (DISTRIBUTION & SALES)

4.3 PORTER’s FIVE FORCES ANALYSIS

4.3.1 BARGAINING POWER of BUYERS / CONSUMERS – HIGH

4.3.2 DAS NEUE HANDELNEN – WIEDER MODERATE

4.3.3 DURCHFÜHRLICHE ERZEUGNISSE – MODERATE FÜR HIGH

4.3.4 BARGAINING POWER of SUPPLIERS – MODERATE

4.3.5 INTENSITÄT DER WETTBEWERBSREGELUNG – HIGH

5 MARKET ÜBERBLICK

5.1 DRIVERS

5.1.1 RISING UTILIZATION of GLYOXAL AS A CROSSLINKING AGENT IN TEXTILE FINISHING.

5.1.2 VERWENDUNGSBEREICH DER ZUSAMMENARBEIT FÜR WET-STRENGTH- UND SURFACE-TREATATIONEN

5.1.3 AUSSCHUSS DER INTERMEDIATE CHEMISCHEN DEMAND IN PHARMACEUTICALS UND AGROCHEMICALs.

5.1.4 INCREASING PREFERENCE FÜR LOW-MOLECULAR-WEIGHT ALDEHYDES IN RESIN UND ADHESIVE SYSTEME.

5.2 AUSBILDUNGEN

5.2.1 HANDLUNG DER ZUSAMMENFASSUNG DER HOHEN AKTIVITÄT UND STABILITÄT

5.2.2 VERFÜGBARKEIT DER ANWENDUNGSSPEZIFISCHEN CHEMISCHES SUBSTITUTES.

5.3 STELLUNGNAHME

5.3.1 VOLATILITÄT IN FEEDSTOCK PRICKTUR

5.3.2 STRINGENT UMWELT- UND RECHTLICHE SICHERHEITSORDNUNGEN

5.3.3 LIMITED PRODUKTE DIFFERENTIATION IN EINER PREIS-KOMPETITIVER MARKT

5.4 HANDELN

5.4.1 ENTWICKLUNG VON MODIFIED AND APPLICATION-SPECIFIC GLYOXAL GRADES.

5.4.2 RISIKO DER INDUSTRIEWIRTSCHAFT

6 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE

6.1 ÜBERBLICK

6.2 INDUSTRIEGRADE

6.3 PHARMACEUTISCHER GRADE

6.4 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS

6.4.1 INDUSTRIEGRADE

6.4.2 PHARMACEUTISCHER GRADE

6.5 MIDDLE EAST AND AFRICA INDUSTRIAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.5.1 ASIEN-PAKIFIK

6.5.2 NORTH AMERIKA

6.5.3 EUROPA

6.5.4 MIDDLE EAST & AFRICA

6.5.5 SOUTH AMERIKA

6.6 MIDDLE EAST UND AFRICA PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

6.6.1 ASIEN-PAKIF

6.6.2 NORTH AMERIKA

6.6.3 EUROPA

6.6.4 MIDDLE EAST & AFRICA

6.6.5 AUSSCHUSS

7 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PURITY

7.1 ÜBERBLICK

7.1.1 40%-60%

7.1.2 90%-99%

7.1.3 SONSTIGE

7.2 MIDDLE EAST UND AFRICA 40%-60% IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.2.1 ASIEN-PAKIFIK

7.2.2 NORTH AMERIKA

7.2.3 EUROPA

7.2.4 MIDDLE EAST & AFRICA

7.2.5 SOUTH AMERIKA

7.3 MIDDLE EAST UND AFRICA 90%-99% IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.3.1 ASIEN-PAKIFIK

7.3.2 NORTH AMERIKA

7.3.3 EUROPA

7.3.4 MIDDLE EAST & AFRICA

7.3.5 ANMERIKA

7.4 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

7.4.1 ASIEN-PAKIF

7.4.2 NORTH AMERIKA

7.4.3 EUROPA

7.4.4 MIDDLE EAST & AFRICA

7.4.5 SOUTH AMERIKA

8 MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH PRODUKTION

8.1 ÜBERBLICK

8.1.1 CATALYTIC OXIDation von ETHYLENE GLYCOL

8.1.2 OXIDIERUNG VON ACETYLENE

8.1.3 SONSTIGE

8.2 MIDDLE EAST UND AFRICA CATALYTIC OXIDATION ETHYLENE GLYCOL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.2.1 ASIEN-PAKIFIK

8.2.2 NORTH AMERIKA

8.2.3 EUROPA

8.2.4 MIDDLE EAST & AFRICA

8.2.5 SOUTH AMERIKA

8.3 MIDDLE EAST UND AFRICA OXIDIERUNG VON ACETYLENE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

8.3.1 ASIEN-PAKIFIK

8.3.2 NORTH AMERIKA

8.3.3 EUROPA

8.3.4 MIDDLE EAST & AFRICA

8.3.5 AMERIKA

8.4 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.4.1 ASIEN-PAKIFIK

8.4.2 NORTH AMERIKA

8.4.3 EUROPA

8.4.4 MIDDLE EAST & AFRICA

8.4.5 SOUTH AMERIKA

9 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PACKAGING

9.1 ÜBERBLICK

9.2 DRUMS

9.3 COMPOSITE IBC

9.4 BULK

9.5 JERRYCANS

9.6 BOTTES

9.7 MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.7.1 PLASTIC DRUMS (HDPE)

9.7.2 TIGHT-HEAD DRUMS

9.7.3 LINERS INSIDE DRUMS

9.7.4 ERLÄUTERUNGEN MIT CHEMISCHEN ZUSAMMENARBEIT

9.7.5 OPEN-TOP DRUMS

9.8 MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.8.1 ASIEN-PAKIFIK

9.8.2 NORTH AMERIKA

9.8.3 EUROPA

9.8.4 MIDDLE EAST & AFRICA

9.8.5 SOUTH AMERIKA

9.9 MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.9.1 COMPOSITE IBCS

9.9.2 RIGID IBCS

9.9.3 IBCS MIT INSULATION

9.9.4 SONSTIGE

9.1 MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.10.1 ASIEN-PAKIFIK

NORTH AMERIKA

9.10.3 EUROPA

9.10.4 MIDDLE EAST & AFRICA

9.10.5 SOUTH AMERIKA

9.11 MIDDLE EAST UND AFRICA BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 ASIEN-PAKIFIK

NORTH AMERIKA

9.11.3 EUROPA

9.11.4 MIDDLE EAST & AFRICA

9.11.5 SOUTH AMERIKA

9.12 MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.12.1 PLASTOFFE

9.12.2 STACKABLE JERRYCANS

9.12.3 METAL JERRYCANS

9.12.4 SONSTIGE JERRYCANS

9.13 MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.13.1 ASIEN-PAKIFIK

9.13.2 NORTH AMERIKA

9.13.3 EUROPA

9.13.4 MIDDLE EAST & AFRICA

9.13.5 ANMERIKA

9.14 MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.14.1 SMALL LABORATOREN

9.14.2 ZUSAMMENARBEIT / PERSONALKAREN

9.14.3 SONDERAUSGABEN

9.14.4 ANDERE BOTTLES

9.15 MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 ASIEN-PAKIFIK

9.15.2 NORTH AMERIKA

9.15.3 EUROPA

9.15.4 MIDDLE EAST & AFRICA

9.15.5 SÜDAMERIKA

10 MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH ANWENDUNG

10.1 ÜBERBLICK

10.2 KROSS-LINKING

10.3 CHEMISCHE INTERMEDIATE

10.4 SONSTIGE

10.5 MIDDLE EAST UND AFRICA CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.5.1 GLYOXALATED POLYACRYLAMIDE (GPAM)

10.5.2 GLYOXALATE STARCH

10.6 MIDDLE EAST UND AFRICA CROSS-LINKING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.6.1 ASIEN-PAKIFIK

10.6.2 NORTH AMERIKA

10.6.3 EUROPA

10.6.4 MIDDLE EAST & AFRICA

10.6.5 SOUTH AMERIKA

10.7 MIDDLE EAST UND AFRICA CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

10.7.1 BULK CHEMISCHE ENTWICKLUNG

10.7.2 POLYMER VERARBEITUNG

10.8 MIDDLE EAST UND AFRICA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

10.8.1 2-IMIDAZOLIDINONE

10.8.2 ETHYLENE GLYCOL DIFORMATE

10.8.3 QUINOXALINE DERIVATIVEN

10.9 MIDDLE EAST UND AFRICA POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.9.1 GLYOXAL UREA RESIN

10.9.2 GLYOXAL PHENOL RESIN

10.9.3 GLYOXAL-BIS(2-HYDROXYANIL)

10.1 MIDDLE EAST UND AFRICA CHEMISCHE INTERMEDIATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.10.1 ASIEN-PAKIFIK

10.10.2 NORTH AMERIKA

10.10.3 EUROPA

10.10.4 MIDDLE EAST & AFRICA

10.10.5 SOUTH AMERIKA

10.11 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.11.1 DIHYDROXYETHYLENE UREA (DHEU)

10.11.2 METHYLOL GLYOXAL

10.12 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.12.1 ASIEN-PAKIFIK

10.12.2 NORTH AMERIKA

10.12.3 EUROPA

10.12.4 MIDDLE EAST & AFRICA

10.12.5 SOUTH AMERIKA

11 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END-USE CHEMICALs

11.1 ÜBERBLICK

11.2 DIHYDROXYETHYLENE UREA (DHEU)

11.3 2-IMIDAZOLIDINONE

11.4 GLYOXALATED POLYACRYLAMIDE (GPAM)

11.5 GLYOXYLIC ACID

11.6 GLYOXALATE STARCH

11.7 GLYOXAL PHENOL RESIN

11.8 GLYOXAL-UREA RESIN

11.9 ETHYLENE GLYCOL DIFORMAT

11.1 UREA-GLYOXAL-KONZENTRATE

11.11 QUINOXALINE DERIVATIVEN

11.12 METHYLOL GLYOXAL

11.13 GLYOXAL-BIS(2-HYDROXYANIL)

11.14 GLYOXAL SODIUM BISULFITE

11.15 QUINOXALINE

11.16 2-METHYLIMIDAZO

11.17 IMIDAZO

11.18 GLYCOLURIL

11.19 ALLANTOEN

11.2 TETRAMETHYLOL ACETYLENEDIUREA

11.21 MIDDLE EAST UND AFRICA DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.21.1 ASIEN-PAKIFIK

11.21.2 NORTHAMERIKA

11.21.3 EUROPA

11.21.4 MIDDLE EAST & AFRICA

11.21.5 AUSSCHUSS

11.22 MIDDLE EAST UND AFRICA 2-IMIDAZOLIDINONE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.22.1 ASIEN-PAKIFIK

11.22.2 NORTH AMERIKA

11.22.3 EUROPA

11.22.4 MIDDLE EAST & AFRICA

11.22.5 AUSSCHUSS

11.23 MIDDLE EAST UND AFRICA GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.23.1 ASIEN-PAKIFIK

11.23.2 NORTH AMERIKA

11.23.3 EUROPA

11.23.4 MIDDLE EAST & AFRICA

11.23.5 AUSSCHUSS

11.24 MIDDLE EAST UND AFRICA GLYOXYLIC ACID in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.24.1 ASIEN-PAKIF

11.24.2 NORTH AMERICA

11.24.3 EUROPA

11.24.4 MIDDLE EAST & AFRICA

11.24.5 AUSSCHUSS

11.25 MIDDLE EAST UND AFRICA GLYOXALATE STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.25.1 ASIEN-PAKIFIK

11.25.2 NORTH AMERIKA

11.25.3 EUROPA

11.25.4 MIDDLE EAST & AFRICA

11.25.5 SÜDAMERIKA

11.26 MIDDLE EAST UND AFRICA GLYOXAL PHENOL RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.26.1 ASIEN-PAKIFIK

11.26.2 NORTH AMERIKA

11.26.3 EUROPA

11.26.4 MIDDLE EAST & AFRICA

11.26.5 SÜDAMERIKA

11.27 MIDDLE EAST UND AFRICA GLYOXAL UREA RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.27.1 ASIEN-PAKIFIK

11.27.2 NORTH AMERIKA

11.27.3 EUROPA

11.27.4 MIDDLE EAST & AFRICA

11.27.5 SÜD AMERIKA

11.28 MIDDLE EAST UND AFRICA ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.28.1 ASIEN-PAKIFIK

11.28.2 NORTH AMERIKA

11.28.3 EUROPA

11.28.4 MIDDLE EAST & AFRICA

11.28.5 SÜDAMERIKA

11.29 MIDDLE EAST UND AFRICA UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.29.1 ASIEN-PAKIFIK

11.29.2 NORTH AMERIKA

11.29.3 EUROPA

11.29.4 MIDDLE EAST & AFRICA

11.29.5 AMERIKA

11.3 MIDDLE EAST UND AFRICA QUINOXALINE DERIVATIVEN IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

11.30.1 ASIEN-PAKIFIK

NORTH AMERIKA

11.30.3 EUROPE

11.30.4 MIDDLE EAST & AFRICA

ANMERIKA

11.31 MIDDLE EAST UND AFRICA METHYLOL GLYOXAL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.31.1 ASIEN-PAKIFIK

11.31.2 NORTH AMERIKA

11.31.3 EUROPE

11.31.4 MIDDLE EAST & AFRICA

11.31.5 AUSSCHUSS

11.32 MIDDLE EAST UND AFRICA GLYOXAL-BIS(2-HYDROXYANIL) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.32.1 ASIEN-PAKIFIK

NORTH AMERIKA

11.32.3 EUROPA

11.32.4 MIDDING EAST & AFRICA

11.32.5 AUSSCHUSS

11.33 MIDDLE EAST UND AFRICA GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.33.1 ASIEN-PAKIFIK

NORTH AMERIKA

11.33.3 EUROPA

11.33.4 MIDDLE EAST & AFRICA

1.1.33.5 AMERIKA

11.34 MIDDLE EAST UND AFRICA QUINOXALINE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.34.1 ASIEN-PAKIF

1.1.34.2 NORTH AMERIKA

11.34.3 EUROPA

11.34.4 MIDDLE EAST & AFRICA

11.34.5 AUSSCHUSS

11.35 MIDDLE EAST UND AFRICA 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

11.35.1 ASIEN-PAKIFIK

11.35.2 NORTH AMERIKA

11.35.3 EUROPA

11.35.4 MIDDING EAST & AFRICA

11.35.5 SÜDAMERIKA

11.36 MIDDLE EAST UND AFRICA IMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.36.1 ASIEN-PAKIFIK

11.36.2 NORTH AMERIKA

11.36.3 EUROPA

11.36.4 MIDDLE EAST & AFRICA

11.36.5 SÜDAMERIKA

11.37 MIDDLE EAST UND AFRICA GLYCOLURIL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.37.1 ASIEN-PAKIFIK

11.37.2 NORTH AMERIKA

11.37.3 EUROPA

11.37.4 MIDDLE EAST & AFRICA

11.37.5 SOUTH AMERIKA

11.38 MIDDLE EAST UND AFRICA ALLANTOIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.38.1 ASIEN-PAKIFIK

11.38.2 NORTH AMERIKA

11.38.3 EUROPA

11.38.4 MIDDLE EAST & AFRICA

11.38.5 SÜDAMERIKA

11.39 MIDDLE EAST UND AFRICA TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.39.1 ASIEN-PAKIFIK

11.39.2 NORTH AMERIKA

11.39.3 EUROPA

11.39.4 MIDDLE EAST & AFRICA

11.39.5 AMERIKA

12 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END USER

12.1 ÜBERBLICK

12.2 TEXTIL

12.3 PAPIER UND PAPIER

12.4 LEATHER

12.5 WICHTIGE UND KATINGUNGEN

12.6 WASSERSTELLUNG

12.7 PHARMACEUTICALs

12.8 HAUSHALTSPRODUKTE

12.9 ZUSAMMENARBEIT UND PERSONALKARE

12.1 VERPACKUNG

12.11 ELEKTRISCHE UND ELEKTRONIK

12.12 OIL UND GAS

12.13 SONSTIGE

12.14 MIDDLE EAST UND AFRICA TEXTILE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.14.1 ASIEN-PAKIF

I2.14.2 NORTH AMERIKA

12.14.3 EUROPA

12.14.4 MIDDLE EAST & AFRICA

12.14.5 AUSSCHUSS

12.15 MIDDLE EAST UND AFRICA PULP UND PAPER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.15.1 ASIEN-PAKIFIK

12.15.2 NORTH AMERIKA

12.15.3 EUROPA

12.15.4 MIDDLE EAST & AFRICA

12.15.5 SÜDAMERIKA

12.16 MIDDLE EAST UND AFRICA LEATHER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.16.1 ASIEN-PAKIFIK

12.16.2 NORTH AMERIKA

12.16.3 EUROPA

12.16.4 MIDDLE EAST & AFRICA

12.16.5 SÜDAMERIKA

12.17 MIDDLE EAST AND AFRICA PAINTS UND COATINGS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.17.1 ASIEN-PAKIFIK

12.17.2 NORTH AMERIKA

12.17.3 EUROPA

12.17.4 MIDDLE EAST & AFRICA

12.17.5 AUSSCHUSS

12.18 MIDDLE EAST UND AFRICA WASSERREATMENT IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.18.1 ASIEN-PAKIFIK

12.18.2 NORTH AMERIKA

12.18.3 EUROPA

12.18.4 MIDDLE EAST & AFRICA

12.18.5 SÜDAMERIKA

12.19 MIDDLE EAST UND AFRICA PHARMACEUTICALs IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.19.1 ASIEN-PAKIFIK

12.19.2 NORTH AMERIKA

12.19.3 EUROPA

12.19.4 MIDDLE EAST & AFRICA

12.19.5 AMERIKA

12.2 MIDDLE EAST UND AFRICA HAUSHALTSPRODUKTE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

12.20.1 ASIEN-PAKIFIK

12.20.2 NORTH AMERIKA

12.20.3 EUROPA

12.20.4 MIDDLE EAST & AFRICA

12.20.5 AUSSCHUSS

12.21 MIDDLE EAST UND AFRIKA KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

12.21.1 LOTIONEN UND CREAMS

12.21.2 PERFUMEN UND DEODORANZEN

12.21.3 SONSTIGE

12.22 MIDDLE EAST UND AFRICA COSMETICs UND PERSONAL CARE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

12.22.1 ASIEN-PAKIFIK

12.22.2 NORTH AMERIKA

12.22.3 EUROPA

12.22.4 MIDDLE EAST & AFRICA

12.22.5 SOUTH AMERIKA

12.23 MIDDLE EAST UND AFRICA PACKAGING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.23.1 ASIEN-PAKIFIK

12.23.2 NORTH AMERIKA

12.23.3 EUROPA

12.23.4 MIDDLE EAST & AFRICA

12.23.5 AUSSCHUSS

12.24 MIDDLE EAST UND AFRICA ELECTRICAL UND ELECTRONICS IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

12.24.1 ASIEN-PAKIF

12.24.2 NORTH AMERIKA

12.24.3 EUROPA

12.24.4 MIDDLE EAST & AFRICA

12.24.5 AUSSCHUSS

12.25 MIDDLE EAST UND AFRICA OIL UND GAS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.25.1 ASIEN-PAKIFIK

12.25.2 NORTH AMERIKA

12.25.3 EUROPA

12.25.4 MIDDLE EAST & AFRICA

12.25.5 SÜDAMERIKA

12.26 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.26.1 ASIEN-PAKIFIK

12.26.2 NORTH AMERIKA

12.26.3 EUROPA

12.26.4 MIDDLE EAST & AFRICA

12.26.5 SÜDAMERIKA

13 MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH REGION

13.1 MIDDAT UND AFRIKA

13.1.1 SAUDI ARABIA

13.1.2 U.A.E.

13.1.3 EGYPT

13.1.4 IRAN

13.1.5 AFRIKA

13.1.6 KUWAIT

13.1.7 QATAR

13.1.8 REST VON MIDDLE EAST & AFRICA

14 MIDDLE EAST UND AFRICA GLYOXAL MARKET, COMPANY LANDSCAPE

14.1 WETTBEWERBSANALYSE: GLOBAL

15 SCHLUSSANTRÄGE

16 WETTBEWERBSPROFIL

16.1 BASF

16.1.1 WETTBEWERBSPOLITIK

16.1.2 REVENTIONSANALYSE

16.1.3 ERZEUGNISSE

16.1.4 ENTWICKLUNG

16.2 MERCK KGAA

16.2.1 WETTBEWERBSPOLITIK

16.2.2 REVENTIONSANALYSE

16.2.3 ERZEUGNISSE

ENTWICKLUNG

16.3 THERMO FISHER SCIENTIFIC INC.

16.3.1 WETTBEWERBSPOLITIK

16.3.2 REVENTIONSANALYSE

16.3.3 PRODUKTPORTFOLI

16.3.4 RECENT DEVELOPTION

16.4 WEYLCHEM INTERNATIONALES GMBH

16.4.1 WETTBEWERBSPOLITIK

16.4.2 ERZEUGNISSE

16.4.3 ENTWICKLUNG

16.5 ALPHA CHEMIKA.

16.5.1 WETTBEWERBSPOLITIK

16.5.2 ERZEUGNISSE

16.5.3 RECENT ENTWICKLUNG

16.6 AMZOLE INDIA PVT. LTD

16.6.1 VERGLEICHEN SNAPSHOT

16.6.2 ERZEUGNISSE

ENTWICKLUNG DES GERICHTSHOFES

16.7 EMCO DYESTUFF

16.7.1 COMPANY SNAPSHOT

16.7.2 ERZEUGNISSE

ENTWICKLUNG

16.8 FLUOROCHEM LIMI

16.8.1 VEREINIGTES NAPSHOT

16.8.2 ERZEUGNISSE

16.8.3 RECENT ENTWICKLUNG

16.9 FUJIFILM WAKO PURE CHEMISCHE ZUSAMMENARBEIT

16.9.1 VEREINIGTES NAPSHOT

16.9.2 ERZEUGNISSE

16.9.3 RECENT ENTWICKLUNG

16.1 GETCHEM CO., LTD.

16.10.1 WETTBEWERBSPOLITIK

16.10.2 ERZEUGNISSE

ENTWICKLUNG DES GERICHTSHOFS

16.11 GLENTHAM LIFE SCIENCES LIMITED

16.11.1 VEREINIGTES SNAPSHOT

16.11.2 ERZEUGNISSE

16.11.3 ENTWICKLUNG

16.12 HANNA EQUIPMENTS (INDIA) PVT. LTD.

16.12.1 WETTBEWERBSPOLITIK

16.12.2 ERZEUGNISSE

16.12.3 ENTWICKLUNG

16.13 HEZE RUNQUAN CHEMICAL CO., LTD.

16.13.1 WETTBEWERBSPOLITIK

16.13.2 ERZEUGNISSE

16.13.3 ENTWICKLUNG

16.14 HIMEDIA LABORATOREN

16.14.1 COMPANY SNAPSHOT

16.14.2 ERZEUGNISSE

16.14.3 ENTWICKLUNG

16.15 HUBEI SHUNHUI BIO-TECHNOLOGY CO., LTD.

16.15.1 COMPANY SNAPSHOT

16.15.2 ERZEUGNISSE

16.15.3 ENTWICKLUNG

16.16 KANTO KAGAKU

16.16.1 VEREINIGTES NAPSHOT

16.16.2 ERZEUGNISSE

16.16.3 ENTWICKLUNG

16.17 KEMIRA

16.17.1 COMPANY SNAPSHOT

16.17.2 REVENUE ANALYSE

16.17.3 ERZEUGNISSE

16.17.4 ENTWICKLUNG

16.18 LOBACHEMIE PVT. LTD.

16.18.1 WETTBEWERBSPOLITIK

16.18.2 ERZEUGNISSE

16.18.3 ENTWICKLUNG

16.19 MERU CHEM PVT.LTD.

16.19.1 GESUNDHEITSSCHUTZ

16.19.2 ERZEUGNISSE

16.19.3 ENTWICKLUNG

16.2 MULTICHEM SPEZIALITÄTEN PRIVATE LIMITED

16.20.1 COMPANY SNAPSHOT

16.20.2 ERZEUGNISSE

16.20.3 VERÖFFENTLICHUNGEN

16.21 OTTO CHEMIE PVT. LTD

16.21.1 COMPANY SNAPSHOT

16.21.2 ERZEUGNISSE

16.21.3 RECENT DEVELOPTIONEN

16.22 OXFORD LAB FINE CHEM LLP.

16.22.1 WETTBEWERBSPOLITIK

16.22.2 ERZEUGNISSE

16.22.3 ENTWICKLUNG

16.23 SANTA CRUZ BIOTECHNOLOGY INC.

16.23.1 WETTBEWERBSPOLITIK

16.23.2 ERZEUGNISSE

16.23.3 ENTWICKLUNG

16.24 SHANDONG ZHISHANG CHEMISCHE CO.LTD,

16.24.1 COMPANY SNAPSHOT

16.24.2 ERZEUGNISSE

16.24.3 ENTWICKLUNG

16.25 SIHAULI CHEMICALs PRIVATE LIMITED

16.25.1 WETTBEWERBSPOLITIK

16.25.2 ERZEUGNISSE

16.25.3 ENTWICKLUNG

16.26 SILVER FERN CHEMICAL LLC

16.26.1 VERGLEICH SNAPSHOT

16.26.2 ERZEUGNISSE

16.26.3 ENTWICKLUNG

16.27 SIMSON PHARMA LIMI

16.27.1 COMPANY SNAPSHOT

16.27.2 ERZEUGNISSE

16.27.3 ENTWICKLUNG

16.28 TOKYO CHEMISCHE INDUSTRIE UK LTD.

16.28.1 COMPANY SNAPSHOT

16.28.2 ERZEUGNISSE

16.28.3 ENTWICKLUNG

16.29 UNIVAR SOLUTIONS LLC

16.29.1 GESELLSCHAFTSSCHUTZ

16.29.2 ERZEUGNISSE

16.29.3 ENTWICKLUNG

16.3 WUXI LANSEN CHEMICALS CO., LTD.

16.30.1 COMPANY SNAPSHOT

16.30.2 ERZEUGNISSE

16.30.3 VERÖFFENTLICHUNGEN

17 QUESTIONNAIRE

18 BERICHTE

Tabellenverzeichnis

TABELLE 1 MAJOR END USE ERZEUGNISSE FÜR GLYOXAL

TABELLE 2 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 3 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 4 MIDDLE EAST UND AFRICA INDUSTRIAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 5 MIDDLE EAST UND AFRICA PHARMACEUTICAL GRADE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 6 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 7 MIDDLE EAST UND AFRICA 40%-60% IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 8 MIDDLE EAST UND AFRICA 90%-99% IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 9 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 10 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 11 MIDDLE EAST UND AFRICA CATALYTIC OXIDATION ETHYLENE GLYCOL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 12 MIDDLE EAST UND AFRIKA OXIDIERUNG VON ACETYLENE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

TABELLE 13 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 14 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 15 MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 16 MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 17 MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 18 MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 19 MIDDLE EAST UND AFRICA BULK IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 20 MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 21 MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 22 MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 23 MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 24 MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 25 MIDDLE EAST UND AFRICA CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 26 MIDDLE EAST UND AFRICA CROSS-LINKING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 27 MIDDLE EAST UND AFRICA CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 28 MIDDLE EAST AND AFRICA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 29 MIDDLE EAST UND AFRIKA POLYMER VERARBEITUNG IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 30 MIDDLE EAST UND AFRICA CHEMISCHE INTERMEDIATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 31 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 32 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 33 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 34 MIDDLE EAST UND AFRICA DIHYDROXYETHYLENE UREA (DHEU) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 35 MIDDLE EAST UND AFRICA 2-IMIDAZOLIDINONE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 36 MIDDLE EAST UND AFRICA GLYOXALATED POLYACRYLAMIDE (GPAM) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 37 MIDDLE EAST UND AFRICA GLYOXYLIC ACID in GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 38 MIDDLE EAST AND AFRICA GLYOXALATE STARCH IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 39 MIDDLE EAST UND AFRICA GLYOXAL PHENOL RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 40 MIDDLE EAST UND AFRICA GLYOXAL UREA RESIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 41 MIDDLE EAST UND AFRICA ETHYLENE GLYCOL DIFORMATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 42 MIDDLE EAST AND AFRICA UREA-GLYOXAL CONCENTRATE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 43 MIDDLE EAST UND AFRICA QUINOXALINE DERIVATIVEN IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

TABELLE 44 MIDDLE EAST UND AFRICA METHYLOL GLYOXAL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 45 MIDDLE EAST UND AFRICA GLYOXAL-BIS(2-HYDROXYANIL) IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 46 MIDDLE EAST UND AFRICA GLYOXAL SODIUM BISULFITE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 47 MIDDLE EAST UND AFRICA QUINOXALINE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 48 MIDDLE EAST UND AFRICA 2-METHYLIMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 49 MIDDLE EAST UND AFRICA IMIDAZOLE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 50 MIDDLE EAST UND AFRICA GLYCOLURIL IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 51 MIDDLE EAST UND AFRICA ALLANTOIN IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 52 MIDDLE EAST UND AFRICA TETRAMETHYLOL ACETYLENEDIUREA IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 53 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 54 MIDDLE EAST UND AFRICA TEXTILE IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 55 MIDDLE EAST AND AFRICA PULP UND PAPER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 56 MIDDLE EAST UND AFRICA LEATHER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 57 MIDDLE EAST AND AFRICA PAINTS UND COATINGS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 58 MIDDLE EAST UND AFRICA WASSERSTREATUNG IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 59 MIDDLE EAST UND AFRICA PHARMACEUTICALs IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 60 MIDDLE EAST UND AFRICA HAUSHALTSPRODUKTE IN GLYOXAL MARKET, NACH REGION, 2018-2033 (USD THOUSAND)

TABELLE 61 MIDDLE EAST UND AFRIKA KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 62 MIDDLE EAST UND AFRIKA KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH REGION, 2018-2033 (USD THOUSAND)

TABELLE 63 MIDDLE EAST UND AFRICA PACKAGING IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 64 MIDDLE EAST UND AFRICA ELECTRICAL UND ELECTRONICS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 65 MIDDLE EAST UND AFRICA OIL UND GAS IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 66 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABELLE 67 MIDDLE EAST & AFRICA GLYOXAL MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABELLE 68 MIDDLE EAST & AFRICA GLYOXAL MARKET, BY COUNTRY, 2018-2033 (THOUSAND TONS)

THOOSAND

TABELLE 70 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 71 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 72 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 73 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 74 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 75 MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 76 MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 77 MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 78 MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 79 MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 80 MIDDLE EAST UND AFRICA CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 81 MIDDLE EAST UND AFRICA CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 82 MIDDLE EAST UND AFRICA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 83 MIDDLE EAST UND AFRICA POLYMER PROCESSING IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 84 MIDDLE EAST UND AFRICA SONDER IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 85 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 86 MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 87 MIDDLE EAST UND AFRICA KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 88 SAUDI ARABIA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 89 SAUDI ARABIA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 90 SAUDI ARABIA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 91 SAUDI ARABIA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 92 SAUDI ARABIA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 93 SAUDI ARABIA DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 94 SAUDI ARABIA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 95 SAUDI ARABIA JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 96 SAUDI ARABIA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 97 SAUDI ARABIA GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 98 SAUDI ARABIA CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 99 SAUDI ARABIA CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 100 SAUDI ARABIA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 101 SAUDI ARABIA POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 102 SAUDI ARABIA ANDERE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 103 SAUDI ARABIA GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

TABELLE 104 SAUDI ARABIA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 105 SAUDI ARABIA COSMETICs UND PERSONAL CARE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 106 U.A.E GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 107 U.A.E GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 108 U.A.E GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 109 U.A.E GLYOXAL MARKET, BY PRODUKTIONSPROZESS, 2018-2033 (USD THOUSAND)

TABELLE 110 U.A.E GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 111 U.A.E. DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 112 U.A.E COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 113 U.A.E JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 114 U.A.E BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 115 U.A.E GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 116 U.A.E CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 117 U.A.E CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 118 U.A.E BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 119 U.A.E. POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 120 SONDERE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 121 U.A.E GLYOXAL MARKET, BY END-USE CHEMICALS, 2018-2033 (USD THOUSAND)

TABELLE 122 U.A.E GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 123 U.A.E COSMETICs UND PERSONAL CARE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 124 EGYPT GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 125 EGYPT GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 126 EGYPT GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 127 EGYPT GLYOXAL MARKET, NACH PROZESSPRODUKTION, 2018-2033 (USD THOUSAND)

TABELLE 128 EGYPT GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 129 EGYPT DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 130 EGYPT COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 131 EGYPT JERRYCANS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 132 EGYPT BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 133 EGYPT GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 134 EGYPT KROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 135 EGYPT CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 136 EGYPT BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 137 EGYPT POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 138 EGYPT ANDERE IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 139 EGYPT GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 140 EGYPT GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 141 EGYPTKOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 142 IRAN GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 143 IRAN GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 144 IRAN GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 145 IRAN GLYOXAL MARKT, NACH PROZESSPRODUKTION 2018-2033 (USD THOUSAND)

TABELLE 146 IRAN GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 147 IRAN DRUMS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 148 IRAN COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 149 IRAN JERRYCANS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 150 IRAN BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 151 IRAN GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 152 IRAN CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 153 IRAN CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 154 IRAN BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 155 IRAN POLYMER VERARBEITUNG IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 156 IRAN SONDERE IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 157 IRAN GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 158 IRAN GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 159 IRAN KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 160 SOUTH AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 161 SOUTH AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 162 SOUTH AFRICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 163 SOUTH AFRICA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 164 SOUTH AFRICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 165 SOUTH AFRICA DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 166 SOUTH AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 167 SOUTH AFRICA JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 168 SOUTH AFRICA BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 169 SOUTH AFRICA GLYOXAL MARKET, BY ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 170 SOUTH AFRICA KROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 171 SOUTH AFRICA CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 172 SOUTH AFRICA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 173 SOUTH AFRICA POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 174 SOUTH AFRICA SONDERE IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 175 SOUTH AFRICA GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 176 SOUTH AFRICA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 177 SOUTH AFRIKA ZUSAMMENARBEIT UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 178 KUWAIT GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 179 KUWAIT GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 180 KUWAIT GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 181 KUWAIT GLYOXAL MARKET, BY PRODUKTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 182 KUWAIT GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 183 KUWAIT DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 184 KUWAIT COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 185 KUWAIT JERRYCANS IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 186 KUWAIT BOTTLES IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 187 KUWAIT GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 188 KUWAIT KROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 189 KUWAIT CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 190 KUWAIT BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 191 KUWAIT POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 192 KUWAIT ANDERE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 193 KUWAIT GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 194 KUWAIT GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 195 KUWAIT KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 196 QATAR GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 197 QATAR GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 198 QATAR GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 199 QATAR GLYOXAL MARKT, NACH PROZESSPROZESSEN, 2018-2033 (USD THOUSAND)

TABELLE 200 QATAR GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 201 QATAR DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 202 QATAR COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 203 QATAR JERRYCANS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 204 QATAR BOTTLES IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 205 QATAR GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 206 QATAR CROSS-LINKING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 207 QATAR CHEMISCHE INTERMEDIATE, IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 208 QATAR BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 209 QATAR POLYMER PROCESSING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 210 SONDERE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 211 QATAR GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 212 QATAR GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 213 QATAR-COSMETIK UND PERSONAL-KARE IN GLYOXAL-MARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 214 REST OF MIDDLE EAST AND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (USD THOUSAND)

TABELLE 215 REST OF MIDDLE EAST AND AFRICA GLYOXAL MARKET, BY GRADE, 2018-2033 (THOUSAND TONS)

TABELLE 216 REST OF MIDDLE EAST AND AFRICA GLYOXAL MARKET, BY PURITY, 2018-2033 (USD THOUSAND)

TABELLE 217 REST VON MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY PRODUCTION PROCESS, 2018-2033 (USD THOUSAND)

TABELLE 218 REST OF MIDDLE EAST AND AFRICA GLYOXAL MARKET, BY PACKAGING, 2018-2033 (USD THOUSAND)

TABELLE 219 REST VON MIDDLE EAST UND AFRICA DRUMS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 220 REST VON MIDDLE EAST UND AFRICA COMPOSITE IBC IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 221 REST VON MIDDLE EAST UND AFRICA JERRYCANS IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 222 REST VON MIDDLE EAST UND AFRICA BOTTLES IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 223 REST VON MIDDLE EAST UND AFRICA GLYOXAL MARKET, NACH ANWENDUNG, 2018-2033 (USD THOUSAND)

TABELLE 224 REST OF MIDDLE EAST UND AFRICA KROSS-LINKING IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 225 REST OF MIDDLE EAST AND AFRICA CHEMICAL INTERMEDIATE, IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 226 REST VON MIDDLE EAST UND AFRICA BULK CHEMICALs MANUFACTURING IN GLYOXAL MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABELLE 227 REST VON MIDDLE EAST UND AFRICA POLYMER VERARBEITUNG IN GLYOXAL MARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 228 REST OF MIDDLE EAST UND AFRICA SONDERE IN GLYOXAL MARKET, NACH TYPE, 2018-2033 (USD THOUSAND)

TABELLE 229 REST VON MIDDLE EAST UND AFRICA GLYOXAL MARKET, BY END-USE CHEMICALs, 2018-2033 (USD THOUSAND)

TABELLE 230 REST OF MIDDLE EAST AND AFRICA GLYOXAL MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABELLE 231 REST VON MIDDLE EAST UND AFRICA KOSMETIK UND PERSONALKARE IN GLYOXALMARKT, NACH TYPE, 2018-2033 (USD THOUSAND)

Abbildungsverzeichnis

Abbildung 1 MIDDLE EAST UND AFRICA GLYOXAL MARKET: SEGMENTATION

Abbildung 2 MIDDLE EAST UND AFRICA GLYOXAL MARKET: DATEN TRIANGULATION

Abbildung 3 MIDDLE EAST UND AFRICA GLYOXAL MARKET: DROC ANALYSIS

Abbildung 4 MIDDLE EAST UND AFRICA GLYOXAL MARKET: PHILIPPINE VS REGIONAL ANALYSE

Abbildung 5 MIDDLE EAST UND AFRICA GLYOXAL MARKET: GESUNDHEITSFORSCHUNGSANALYSE

Abbildung 6 MIDDLE EAST UND AFRICA GLYOXALMARKT: INTERVIEW DEMOGRAPHICS

Abbildung 7 MIDDLE EAST UND AFRICA GLYOXAL MARKET: DBMR MARKET POSITION GRID

Abbildung 8 DBMR VENDOR SHARE ANALYSE

Abbildung 9 MIDDLE EAST UND AFRICA GLYOXAL MARKET: SEGMENTATION

Fig. 10 ZUSAMMENFASSUNG

ZAHLUNG 11 STRATEGISCHE ENTSCHEIDUNGEN

Abbildung 12 SIX SEGMENTE WICHTIGSTEN MIDDLE EAST UND AFRICA GLYOXAL MARKT, NACH PRODUKT (2025)

Abbildung 13 RISING UTILIZIERUNG VON GLYOXAL AS A CROSSLINKING AGENT IN TEXTILE FINISHING wird auf den Weg gebracht, den MIDDLE EAST UND AFRICA GLYOXAL MARKET DURING THE FORECAST PERIOD von 2026 bis 2033

Abbildung 14 INDUSTRIELLE GRADE-GRADE-GRADE-GRUPPEN FÜR DIE LARGESTELLUNG DES MIDDLE EAST UND AFRICA GLYOXAL MARKET in 2026 & 2033

Abbildung 15 VALUE CHAIN ANALYSE

Fig. 16 SUPPLY CHAIN ANALYSE

Abbildung 17 PORTER’s FIVE FORCES ANALYSE

Abbildung 18 VERWENDUNGSBEREICHE, BERICHTE, OPPORTUNITÄTEN UND KALLE VON MIDDLE EAST UND AFRICA GLYOXAL MARKET

Figur 19 GLYOXAL-MARKET: NACH GRADE, 2025

Figur 20 GLYOXAL-MARKET: NACH PURITY, 2025

Abbildung 21 GLYOXALMARKT: NACH PRODUKTIONSPROZESS, 2025

Abbildung 22 MIDDLE EAST UND AFRICA GLYOXAL MARKET: BY PACKAGING, 2025

Abbildung 23 MIDDLE EAST UND AFRICA GLYOXAL MARKET: NACH ANWENDUNG, 2025

Abbildung 24 MIDDLE EAST UND AFRICA GLYOXAL MARKET: NACH END-USE CHEMICALs, 2025

Abbildung 25 MIDDLE EAST UND AFRICA GLYOXAL MARKET: BY END USER, 2025

Abbildung 26 MIDDLE EAST UND AFRICA GLYOXAL MARKET: GEOGRAPHISCHE ANALYSE

Abbildung 27 MIDDLE EAST UND AFRICA GLYOXALMARKT: GESELLSCHAFTSSCHUTZ 2025 (%)

Abbildung 28 MIDDLE EAST UND AFRICA GLYOXAL MARKET, SNAPSHOT (2025)

Forschungsmethodik

Die Datenerfassung und Basisjahresanalyse werden mithilfe von Datenerfassungsmodulen mit großen Stichprobengrößen durchgeführt. Die Phase umfasst das Erhalten von Marktinformationen oder verwandten Daten aus verschiedenen Quellen und Strategien. Sie umfasst die Prüfung und Planung aller aus der Vergangenheit im Voraus erfassten Daten. Sie umfasst auch die Prüfung von Informationsinkonsistenzen, die in verschiedenen Informationsquellen auftreten. Die Marktdaten werden mithilfe von marktstatistischen und kohärenten Modellen analysiert und geschätzt. Darüber hinaus sind Marktanteilsanalyse und Schlüsseltrendanalyse die wichtigsten Erfolgsfaktoren im Marktbericht. Um mehr zu erfahren, fordern Sie bitte einen Analystenanruf an oder geben Sie Ihre Anfrage ein.

Die wichtigste Forschungsmethodik, die vom DBMR-Forschungsteam verwendet wird, ist die Datentriangulation, die Data Mining, die Analyse der Auswirkungen von Datenvariablen auf den Markt und die primäre (Branchenexperten-)Validierung umfasst. Zu den Datenmodellen gehören ein Lieferantenpositionierungsraster, eine Marktzeitlinienanalyse, ein Marktüberblick und -leitfaden, ein Firmenpositionierungsraster, eine Patentanalyse, eine Preisanalyse, eine Firmenmarktanteilsanalyse, Messstandards, eine globale versus eine regionale und Lieferantenanteilsanalyse. Um mehr über die Forschungsmethodik zu erfahren, senden Sie eine Anfrage an unsere Branchenexperten.

Anpassung möglich

Data Bridge Market Research ist ein führendes Unternehmen in der fortgeschrittenen formativen Forschung. Wir sind stolz darauf, unseren bestehenden und neuen Kunden Daten und Analysen zu bieten, die zu ihren Zielen passen. Der Bericht kann angepasst werden, um Preistrendanalysen von Zielmarken, Marktverständnis für zusätzliche Länder (fordern Sie die Länderliste an), Daten zu klinischen Studienergebnissen, Literaturübersicht, Analysen des Marktes für aufgearbeitete Produkte und Produktbasis einzuschließen. Marktanalysen von Zielkonkurrenten können von technologiebasierten Analysen bis hin zu Marktportfoliostrategien analysiert werden. Wir können so viele Wettbewerber hinzufügen, wie Sie Daten in dem von Ihnen gewünschten Format und Datenstil benötigen. Unser Analystenteam kann Ihnen auch Daten in groben Excel-Rohdateien und Pivot-Tabellen (Fact Book) bereitstellen oder Sie bei der Erstellung von Präsentationen aus den im Bericht verfügbaren Datensätzen unterstützen.