Europe Internal Neuromodulation Devices Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

1.50 Billion

USD

2.30 Billion

2024

2032

USD

1.50 Billion

USD

2.30 Billion

2024

2032

| 2025 –2032 | |

| USD 1.50 Billion | |

| USD 2.30 Billion | |

| % | |

|

Europe Internal Neuromodulation Devices Market Segmentation, By Product Type (Spinal Cord Stimulator, Deep Brain Stimulator, Vagus Nerve Stimulator, Sacral Nerve Stimulator, Gastric Nerve Stimulator), Lead Type (Percutaneous, Paddle Lead), Biomaterial (Metallic, Polymeric, Ceramic), Application (Failed Back Surgery Syndrome, Parkinson’s disease, Urinary Incontinence, Epilepsy, Gastroparesis), End-User (Hospitals, Clinics, Home Healthcare, Community Healthcare)- Industry Trends and Forecast to 2032

Internal Neuromodulation Devices Market Size

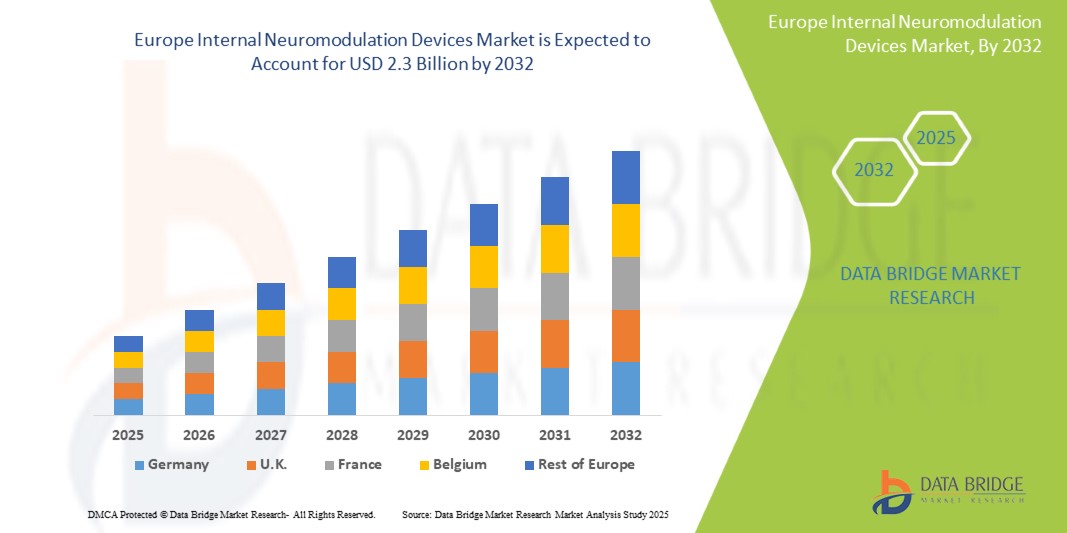

- The Europe Internal Neuromodulation Devices Market was valued atUSD1.5 Billionin 2024and is expected to reachUSD2.3 Billionby 2032,at aCAGR of 5.5%during the forecast period.

- The growth of the Europe Internal Neuromodulation Devices Market is propelled by several key factors. A primary driver is the rising prevalence of chronic neurological disorders such as Parkinson’s disease, epilepsy, and chronic pain conditions, which necessitate long-term and effective therapeutic solutions. Internal neuromodulation devices, such as spinal cord stimulators and deep brain stimulators, play a crucial role in managing these conditions by altering nerve activity through targeted electrical stimulation. Furthermore, the increasing geriatric population, which is more susceptible to neurodegenerative diseases, is fueling demand for these advanced devices. Technological advancements, such as miniaturization, rechargeable batteries, and MRI-compatible systems, are also enhancing device efficacy and patient comfort, thereby accelerating market adoption across the region.

Europe Internal Neuromodulation Devices Market Analysis

- Internal neuromodulation devices play a critical role in managing various chronic neurological and pain-related conditions, including Parkinson’s disease, epilepsy, chronic back pain, and urinary and fecal incontinence. These devices, which include spinal cord stimulators, deep brain stimulators, sacral nerve stimulators, and vagus nerve stimulators, work by delivering electrical impulses to specific parts of the nervous system, modulating nerve activity to alleviate symptoms and improve patients’ quality of life. They are widely used in hospitals, neurology centers, and pain management clinics across Europe.

- The demand for internal neuromodulation devices in Europe is primarily driven by the rising prevalence of neurological and chronic pain disorders, coupled with an aging population that is more prone to such conditions. Additionally, the growing awareness and adoption of minimally invasive treatment options, as well as the increasing limitations of pharmaceutical therapies due to side effects and tolerance development, are prompting both patients and physicians to consider device-based neuromodulation as an effective alternative.

- Europe holds a significant share of the global internal neuromodulation devices market, benefiting from its strong healthcare infrastructure, high diagnostic capabilities, and early adoption of innovative technologies. Countries such as Germany, France, the United Kingdom, and the Netherlands are leading the market due to robust neurology and pain treatment programs, well-established reimbursement frameworks, and active clinical research in the field of neuromodulation. These countries also see a higher number of clinical trials and faster integration of regulatory-approved innovations into clinical practice.

- The European market is also supported by stringent but progressive regulatory frameworks such as the EU Medical Device Regulation (MDR) and the oversight of the European Medicines Agency (EMA), ensuring that neuromodulation devices meet high safety and efficacy standards. Furthermore, the emergence of MRI-compatible devices, rechargeable battery systems, wireless programming, and closed-loop feedback technologies is enhancing treatment outcomes and patient compliance.

- Additionally, the shift toward personalized medicine and the integration of AI-driven diagnostics and monitoring tools are expected to further drive innovation and adoption in the internal neuromodulation space. As the burden of chronic neurological and pain conditions continues to grow, and as patient awareness and access to advanced neuromodulation therapies expand, the Europe Internal Neuromodulation Devices Market is poised for steady and sustained growth over the coming years.

Report ScopeInternal Neuromodulation DevicesMarket Segmentation

|

Attributes |

Internal Neuromodulation DevicesKeyMarket Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Internal Neuromodulation Devices Market Trends

“Personalized Therapies and Technological Advancements in Neurostimulation Precision”

- The European market is experiencing a shift toward personalized neuromodulation, with devices now offering individualized stimulation parameters based on real-time patient feedback and neurological response. This trend is enhancing therapeutic efficacy, improving patient comfort, and reducing side effects associated with one-size-fits-all approaches.

- The incorporation of intraoperative imaging, neuronavigation, and computer-assisted programming in neuromodulation procedures is increasing across Europe. These technologies provide clinicians with enhanced precision for implant placement, especially in deep brain and spinal cord stimulation surgeries, reducing complications and improving patient outcomes.

- In line with broader healthcare trends, there is rising demand for minimally invasive neurosurgical procedures. New-generation neuromodulation devices are smaller, easier to implant, and involve reduced surgical trauma, resulting in shorter recovery times and increased acceptance among elderly and high-risk patients.

- For instance, France has been at the forefront in adopting deep brain stimulation therapies for treating advanced Parkinson’s disease, with major neurological centers in Paris and Lyon conducting pioneering research and offering specialized neurosurgical procedures.

- Advances in biocompatible materials and battery life have led to the development of durable, rechargeable implantable devices, minimizing the need for frequent replacements. This is particularly beneficial for chronic disease management, improving cost-efficiency and long-term therapy adherence in European healthcare systems.

- The emergence of smart neuromodulation systems equipped with artificial intelligence and cloud connectivity is enabling remote monitoring, automated adjustments, and predictive analytics. These innovations are facilitating proactive care management and allowing clinicians to fine-tune therapy in real time, significantly enhancing patient engagement and outcomes.

Internal Neuromodulation Devices Market Dynamics

Driver

“Rising Prevalence of Neurological Disorders and Demand for Targeted, Long-Term Therapies”

- The Europe internal neuromodulation devices market is primarily driven by the increasing prevalence of chronic neurological and neurodegenerative conditions such as Parkinson’s disease, epilepsy, essential tremor, and chronic pain syndromes. These conditions require sustained, targeted interventions that internal neuromodulation devices are well-equipped to provide.

- An aging population across major European countries—such as Germany, Italy, and the United Kingdom—is contributing to a growing patient base susceptible to neurological disorders and movement-related impairments, thus increasing the demand for advanced neuromodulation therapies.

- As awareness grows around non-pharmacologic treatment alternatives—amid rising concerns over opioid use and medication side effects—neuromodulation is gaining popularity as a safer, long-term therapeutic option for managing chronic pain and neurological dysfunctions.

- Technological advancements in the design and functionality of neuromodulation systems—such as adaptive stimulation, MRI compatibility, and wireless remote programming—are enhancing treatment outcomes, patient convenience, and clinical precision, thereby supporting broader clinical adoption.

For instance,

- In 2023, Medtronic plc (Ireland) launched the Percept™ PC neurostimulator in Europe with BrainSense technology, enabling real-time brain signal sensing to personalize therapy for Parkinson’s disease patients, marking a breakthrough in precision neuromodulation

- The growth is further supported by favorable regulatory frameworks under the EU Medical Device Regulation (MDR), increasing neurology expertise across Europe, and expanding availability of advanced neurostimulation procedures in specialized hospitals and academic medical centers.

Opportunity

“Expansion of Personalized Neuromodulation Therapies in Outpatient and Ambulatory Settings”

- The ongoing shift toward outpatient and ambulatory care across Europe is opening new avenues for internal neuromodulation devices that support less invasive procedures, faster patient recovery, and reduced healthcare costs. These developments are making advanced neurostimulation therapies more accessible outside traditional hospital settings.

- Rising demand for day surgeries and decentralized treatment delivery is driving the adoption of compact, patient-specific neuromodulation systems that can be implanted through minimally invasive techniques, enabling shorter procedure times and same-day discharges in neurology and pain management clinics.

- Digital planning platforms and remote programming tools are increasingly being integrated into outpatient care workflows, allowing clinicians to pre-configure stimulation protocols and adjust them post-implantation via wireless technologies. This model enhances patient convenience and reduces the need for frequent follow-up visits.

For instance,

- In January 2024, Abbott Laboratories introduced an enhanced version of its Proclaim™ XR spinal cord stimulation system in Europe, enabling remote therapy adjustments and tailored stimulation in ambulatory care settings, significantly improving access for patients with chronic pain and mobility limitations

- This opportunity is further supported by Europe's growing investment in digital health infrastructure, the proliferation of ambulatory surgical centers, and the increasing need to optimize clinical capacity by reducing inpatient volumes—fostering demand for flexible, technology-driven neuromodulation solutions.

Restraint/Challenge

“High Procedure Costs and Stringent EU MDR Compliance Hindering Accessibility and Innovation”

- The high cost associated with internal neuromodulation devices—including implantable pulse generators, leads, and advanced stimulation systems—poses a significant barrier to widespread adoption, particularly in publicly funded healthcare systems and low-resource settings across Europe.

- Compliance with the European Union Medical Device Regulation (EU MDR) presents a major challenge for neuromodulation manufacturers. The regulation requires extensive clinical evidence, post-market surveillance, and meticulous documentation, substantially increasing the cost and duration of product development and approval.

- Small and medium-sized enterprises (SMEs) in the neuromodulation sector are disproportionately affected, as limited financial and operational resources hinder their ability to adapt to these regulatory demands. This leads to delayed product rollouts, reduced innovation, or complete market exit—ultimately limiting treatment options and technological advancement in several European markets.

For instance,

- According to a 2024 MedTech Europe report, more than 50% of neuromodulation SMEs indicated that MDR-related costs had forced them to delay new product introductions or halt clinical development pipelines altogether, significantly impacting their market participation in Europe.

- These barriers are further intensified in decentralized or rural healthcare systems, where access to specialized surgical teams and infrastructure for neuromodulation therapy remains limited. As a result, patients in these regions face restricted access to cutting-edge treatments, constraining overall market growth and equity in neurological care

Internal Neuromodulation Devices Market Scope

The market is segmented on the basis, product, type, application, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Product Type |

|

|

By Lead Type |

|

|

By Biomaterial |

|

|

By Application |

|

|

ByDistribution Channel |

|

In 2025, Spinal Cord Stimulation (SCS) Devices is projected to dominate the market with a largest share in product type segment

The Spinal Cord Stimulator segment is expected to dominate the Internal Neuromodulation Devices Market with the largest share of 56.22% in 2025 due to its high prevalence of chronic pain conditions, such as back pain, neuropathic pain, and failed back surgery syndrome, which often require long-term pain management solutions. SCS devices are crucial for providing sustained relief by delivering targeted electrical pulses to the spinal cord, thereby blocking pain signals. The growing preference for non-invasive, drug-free treatments, coupled with advancements in SCS technology such as MRI compatibility, wireless programming, and rechargeability, is propelling the adoption of these devices. Additionally, the shift toward personalized treatment options, including adaptive and responsive neurostimulation, is enhancing the efficacy of SCS systems and improving patient outcomes. As the demand for chronic pain management solutions increases, the SCS devices segment is projected to maintain a dominant share in the European market.

The Parkinson’s Disease is expected to account for the largest share during the forecast period in Application market

In 2025, the Parkinson’s disease treatment segment is expected to dominate the market with the largest market share of 43.31% due to its high prevalence of Parkinson’s disease, a progressive neurodegenerative disorder that affects motor function, with a notable increase in cases due to the aging population in Europe. Internal neuromodulation devices, such as deep brain stimulation (DBS), are proving to be effective solutions for managing the motor symptoms of Parkinson’s disease, including tremors, rigidity, and bradykinesia. Advancements in DBS technology, such as MRI-compatible devices, rechargeable batteries, and closed-loop systems that adjust stimulation in real-time based on brain signals, are enhancing the effectiveness of treatment. Additionally, the integration of personalized stimulation settings and the ability to remotely monitor and adjust therapy are improving patient outcomes and quality of life. As Parkinson's disease continues to have a significant impact on European healthcare systems, demand for non-pharmacological therapies like DBS is expected to grow, making it a dominant segment in the market.

Internal Neuromodulation Devices Market Regional Analysis

“Germany is the Dominant Country in the Internal Neuromodulation Devices Market”

- Germany is a leader in the Europe Internal Neuromodulation Devices Market, holding the largest share due to its advanced healthcare infrastructure, highly developed neurology and pain management sectors, and substantial investments in medical technologies.

- The country’s well-established healthcare system, strong research and development environment, and emphasis on chronic pain management and neurological disorders, including Parkinson’s disease and epilepsy, drive the adoption of internal neuromodulation devices such as spinal cord stimulators (SCS) and deep brain stimulation (DBS).

- Germany’s integration of cutting-edge technologies, including MRI-compatible devices, rechargeable batteries, and real-time monitoring systems, further strengthens its position as a leader in the neuromodulation market.

- The presence of leading medical device manufacturers, such as Medtronic and Boston Scientific, along with favorable reimbursement policies, fosters a conducive environment for the growth of the internal neuromodulation devices market.

- Germany’s strong academic and clinical research network, along with collaborations between healthcare providers and medical device companies, drives innovation and enhances the availability of state-of-the-art neuromodulation solutions for patients.

“U.K. is Projected to Register the Highest Growth Rate”

- The U.K. is projected to experience the fastest growth in the Europe Internal Neuromodulation Devices Market due to a rising prevalence of neurological disorders, including chronic pain conditions, Parkinson’s disease, and epilepsy, alongside an increasing demand for non-invasive and personalized treatment options.

- The U.K. government’s focus on enhancing healthcare access, integrating digital health solutions, and expanding telemedicine services is accelerating the adoption of neuromodulation devices, such as DBS for Parkinson's disease and spinal cord stimulators for chronic pain.

- Additionally, the country’s growing elderly population, increased awareness about the benefits of neuromodulation therapies, and investments in specialized neurological care across urban and rural regions are fueling the demand for these devices.

- The U.K. is home to prominent healthcare institutions and academic research centers collaborating with medical device manufacturers, further accelerating innovation and the development of advanced neuromodulation solutions tailored to the needs of patients.

- The strong emphasis on minimally invasive procedures, patient-centered care, and cost-effective treatment options is driving the expansion of the internal neuromodulation devices market in the U.K., positioning it as a key player in the European market.

Internal Neuromodulation Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Medtronic plc (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- LivaNova PLC (U.K.)

- Aleva Neurotherapeutics SA (Switzerland)

- NeuroPace, Inc. (U.S.)

- BioControl Medical (Israel)

Latest Developments in Global Internal Neuromodulation Devices Market

- In September 2023, Boston Scientific announced the acquisition of Relievant Medsystems for usd 850 million, enhancing its portfolio with the Intracept Intraosseous Nerve Ablation System, designed to treat vertebrogenic pain. The system offers a minimally invasive procedure for chronic low back pain. The deal is expected to close in the first half of 2024.

- In April 2024, Medtronic announced FDA approval for its Inceptiv closed-loop rechargeable spinal cord stimulator (SCS) for chronic pain treatment. Inceptiv is the first SCS to automatically adjust stimulation based on real-time biological signals, ensuring optimal therapy. The device also offers 1.5T and 3T MRI access, enhancing patient comfort and outcomes.

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.