Europe Non Small Cell Lung Cancer Diagnostics Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

850.07 Billion

USD

2,181.09 Billion

2025

2033

USD

850.07 Billion

USD

2,181.09 Billion

2025

2033

| 2026 –2033 | |

| USD 850.07 Billion | |

| USD 2,181.09 Billion | |

| % | |

|

Europe Non-Small Cell Lung Cancer Market Segmentation, By Cancer Type (Lung Adenocarcinoma (LUAD), Lung Squamous Cell Carcinoma (LUSC), Large Cell Carcinoma And Others), Product (Reagents and Kits, Instruments, And Services And Softwares), Test (Imaging Test, Molecular Test, Biopsy, Sputum Cytology, Thoracentesis, Immunohistochemistry, And Others), End-User (Hospital, Clinical Laboratories, Academics And Others) - Industry Trends and Forecast to 2033

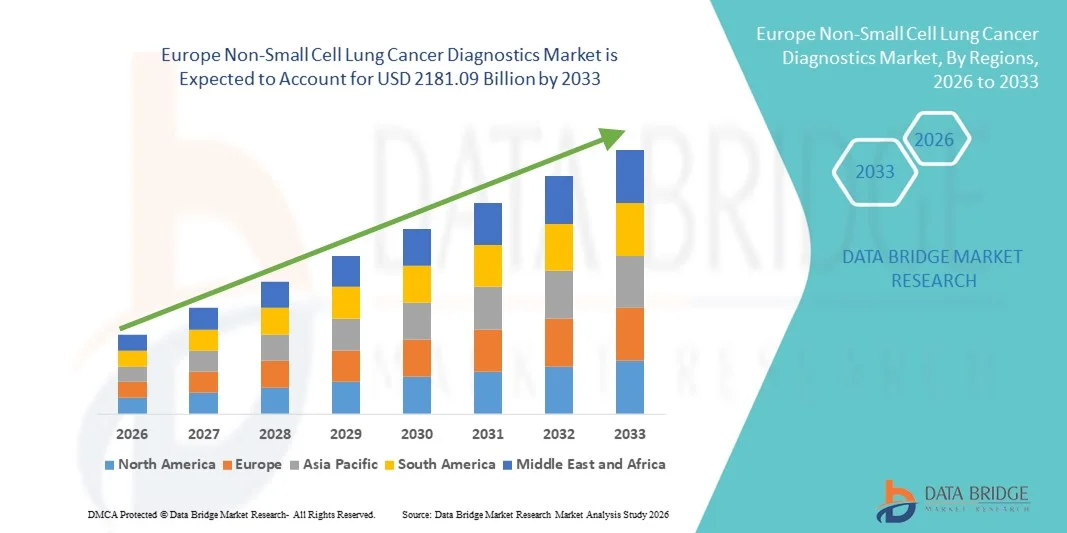

Europe Non-Small Cell Lung Cancer Diagnostics Market Size

- The Europe non-small cell lung cancer diagnostics market size was valued at USD 850.07 billion in 2025 and is expected to reach USD 2181.09 billion by 2033, at a CAGR of 12.50% during the forecast period

- The market growth is largely fueled by increasing prevalence of lung cancer globally, advancements in molecular diagnostics, and growing awareness for early detection and personalized treatment approaches

- Furthermore, rising demand for rapid, accurate, and non-invasive diagnostic solutions in clinical settings is establishing Non-Small Cell Lung Cancer (NSCLC) Diagnostics as a critical component in oncology care. These converging factors are accelerating the uptake of NSCLC Diagnostics solutions, thereby significantly boosting the industry's growth

Europe Non-Small Cell Lung Cancer Diagnostics Market Analysis

- Non-Small Cell Lung Cancer (NSCLC), are increasingly vital in oncology care due to their ability to enable early detection, guide targeted therapies, and improve patient outcomes

- The escalating demand for NSCLC diagnostics is primarily fueled by rising lung cancer prevalence, growing awareness for personalized medicine, and increasing adoption of advanced molecular testing technologies in clinical setting

- U.K. dominated the non-small cell lung cancer diagnostics market with the largest revenue share of approximately 39.8% in 2025, supported by advanced healthcare infrastructure, strong oncology research programs, and the presence of leading diagnostic companies. Widespread adoption of cutting-edge diagnostic solutions—including liquid biopsy, NGS, and immunohistochemistry—along with continuous innovations, drives substantial market growth in the country

- Germany is expected to be the fastest-growing country in the non-small cell lung cancer diagnostics market during the forecast period, registering a CAGR of around 12.9%, fueled by rising lung cancer incidence, increasing healthcare expenditure, expanding oncology infrastructure, and growing awareness for early disease detection

- The Lung Adenocarcinoma (LUAD) segment dominated the largest market revenue share of 46.5% in 2025, owing to its higher prevalence among NSCLC patients globally, particularly in North America and Asia-Pacific

Report Scope and Non-Small Cell Lung Cancer Diagnostics Market Segmentation

|

Attributes |

Non-Small Cell Lung Cancer Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Non-Small Cell Lung Cancer Diagnostics Market Trends

Advancements in Targeted Diagnostics and Precision Medicine

- A key trend in the Europe NSCLC diagnostics market is the growing adoption of advanced molecular and genomic testing techniques to enable precision medicine

- Technologies such as next-generation sequencing (NGS), liquid biopsy, and multiplex PCR are increasingly being integrated into clinical workflows to allow early and accurate detection of genetic mutations, actionable biomarkers, and therapeutic targets

- For instance, in March 2023, Guardant Health launched its Guardant360® CDx liquid biopsy test in Europe, providing a minimally invasive, comprehensive genomic profiling solution for patients with advanced NSCLC. This development underscores the shift toward non-invasive diagnostics and personalized treatment strategies

- In addition, there is an increasing focus on integrating companion diagnostics with targeted therapies, enabling oncologists to tailor treatments based on specific biomarkers such as EGFR, ALK, KRAS, and ROS1 mutations. The trend toward multiplex testing and point-of-care diagnostic devices is accelerating early-stage detection, reducing turnaround times, and improving treatment outcomes

- Collaboration between diagnostic companies, hospitals, and research institutes is fostering the development of innovative tests and panels designed specifically for NSCLC patients, ensuring higher sensitivity and specificity in biomarker detection

Europe Non-Small Cell Lung Cancer Diagnostics Market Dynamics

Driver

Rising Incidence of Lung Cancer and Demand for Early Detection

- The escalating prevalence of lung cancer worldwide, particularly NSCLC, is a primary driver for market growth. Increasing awareness among healthcare professionals and patients about the benefits of early diagnosis and personalized treatment is prompting widespread adoption of advanced diagnostic tools

- For instance, in July 2022, Roche expanded its cobas EGFR Mutation Test v2 in Asia-Pacific, facilitating rapid and accurate detection of EGFR mutations in NSCLC patients. Such expansions by key players are expected to drive market adoption and growth

- The demand is further bolstered by increasing government initiatives and healthcare programs aimed at lung cancer screening and early detection. Health authorities in North America, Europe, and Asia-Pacific are implementing national screening programs, often incorporating low-dose CT scans combined with molecular testing for high-risk population

- Rising investments in R&D for biomarker identification, as well as the launch of innovative diagnostic kits and platforms, are enhancing the accuracy and efficiency of NSCLC detection. The growing integration of liquid biopsy and tissue biopsy methods provides clinicians with flexible, less invasive options for patient diagnosis and monitoring

Restraint/Challenge

High Costs of Advanced Diagnostic Tests and Limited Accessibility

- Despite technological advances, the high cost of molecular diagnostic tests remains a significant barrier to widespread adoption, especially in developing regions

- Equipment, reagents, and specialized lab personnel contribute to elevated pricing, making access challenging for smaller healthcare facilities and low-income patients

- For instance, reports from 2023 highlighted that comprehensive NGS panels could cost over USD3,000 per test in the U.S., limiting adoption among outpatient clinics and community hospitals. Such cost considerations may hinder rapid market penetration in price-sensitive regions

- In addition, regulatory approvals and reimbursement challenges in different countries can slow the adoption of novel diagnostics. Variability in insurance coverage, lack of standardized guidelines, and limited reimbursement policies for advanced molecular tests may discourage hospitals from implementing high-end diagnostic platforms

- Addressing these barriers through strategic partnerships, pricing models, regional distribution expansion, and government initiatives for subsidized testing will be crucial to ensure broader adoption and sustained market growth

Europe Non-Small Cell Lung Cancer Diagnostics Market Scope

The market is segmented on the basis of cancer type, product, test, and end-user.

- By Cancer Type

On the basis of cancer type, the Non-Small Cell Lung Cancer market is segmented into Lung Adenocarcinoma (LUAD), Lung Squamous Cell Carcinoma (LUSC), Large Cell Carcinoma, and Others. The Lung Adenocarcinoma (LUAD) segment dominated the largest market revenue share of 46.5% in 2025, owing to its higher prevalence among NSCLC patients globally, particularly in North America and Asia-Pacific. The dominance is further supported by extensive research and clinical focus on LUAD due to the availability of targeted therapies like EGFR and ALK inhibitors. Rising awareness of early diagnosis, supported by government screening programs and insurance coverage, has increased the adoption of LUAD-specific molecular testing kits. Hospitals and clinical laboratories are investing in advanced diagnostic solutions, such as next-generation sequencing (NGS) and PCR-based assays, to detect LUAD at early stages. Increasing incidence in non-smokers has also expanded the need for routine diagnostic monitoring. Moreover, LUAD’s higher prevalence among females and its association with personalized therapies contribute to robust demand. The availability of validated biomarkers, coupled with the adoption of liquid biopsies, further strengthens revenue growth.

The Large Cell Carcinoma segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, driven by rising identification of rare and aggressive NSCLC subtypes. Advanced molecular profiling techniques, including NGS and immunohistochemistry, are enabling accurate detection of Large Cell Carcinoma, leading to increased adoption in research and clinical settings. Pharmaceutical companies are collaborating with diagnostic laboratories to develop targeted therapies specifically for Large Cell Carcinoma patients. The segment’s growth is fueled by expanding awareness of rare NSCLC subtypes, increasing funding for oncology research, and rising use of personalized medicine. Early detection, coupled with improved patient outcomes, is encouraging healthcare providers to invest in diagnostic infrastructure. Emerging markets are witnessing higher uptake due to rising prevalence and government healthcare initiatives.

- By Product

On the basis of product, the Non-Small Cell Lung Cancer market is segmented into Reagents and Kits, Instruments, and Services & Softwares. The Reagents and Kits segment held the largest market revenue share of 48.7% in 2025, driven by widespread adoption of molecular diagnostic panels, PCR kits, and immunohistochemistry reagents for NSCLC testing. High recurring demand for these consumables ensures steady revenue, particularly in hospitals and clinical laboratories. The segment benefits from standardized workflows and automation compatibility, which improve throughput and reduce manual errors. The growing focus on targeted therapy selection for NSCLC patients, coupled with increasing prevalence of early-stage lung cancer, further boosts demand. Market growth is supported by expanding reimbursement coverage, rising awareness of biomarker-based treatment, and integration with automated diagnostic platforms. The segment also benefits from the availability of multiplex testing solutions that allow simultaneous detection of multiple mutations, enhancing diagnostic efficiency and accuracy.

The Services & Softwares segment is anticipated to witness the fastest CAGR of 23.5% from 2026 to 2033, driven by increasing adoption of AI-enabled diagnostic solutions, cloud-based platforms, and telepathology services. Hospitals and laboratories are leveraging digital pathology software for faster interpretation of molecular data and automated reporting. Collaborations between IT companies and diagnostic laboratories for bioinformatics support and real-time monitoring of patient data are boosting segment growth. Rising demand for remote diagnostics and virtual consultation platforms in oncology also fuels adoption. Additionally, regulatory approvals and increasing investments in precision medicine initiatives enhance the uptake of advanced software solutions. The segment is gaining traction in both developed and emerging markets, supported by rising focus on data analytics, personalized treatment planning, and improved patient outcomes.

- By Test

On the basis of test, the Non-Small Cell Lung Cancer market is segmented into Imaging Test, Molecular Test, Biopsy, Sputum Cytology, Thoracentesis, Immunohistochemistry, and Others. The Molecular Test segment dominated the largest market revenue share of 45.3% in 2025, due to increasing adoption of NGS, PCR-based diagnostics, and liquid biopsy technologies. Molecular tests are critical for identifying EGFR, ALK, KRAS, and ROS1 mutations, which guide targeted therapy decisions. Hospitals and clinical laboratories are increasingly implementing molecular testing as standard practice for NSCLC diagnosis. The growth is further supported by personalized medicine initiatives, insurance reimbursement, and regulatory encouragement for companion diagnostics. Molecular tests also offer high sensitivity and specificity, facilitating early detection and monitoring of treatment response.

The Liquid Biopsy & Thoracentesis sub-segment is expected to witness the fastest CAGR of 24.1% from 2026 to 2033, driven by the non-invasive nature of these procedures, enabling real-time monitoring and minimal patient discomfort. Adoption is supported by advances in circulating tumor DNA (ctDNA) analysis, AI-assisted interpretation, and integration with personalized treatment programs. Pharmaceutical and diagnostic companies are investing heavily in liquid biopsy development, particularly for NSCLC patients with difficult-to-biopsy tumors. The segment is expanding rapidly in clinical trials and oncology centers, especially in regions focusing on precision medicine and early cancer detection.

- By End-User

On the basis of end-user, the Non-Small Cell Lung Cancer market is segmented into Hospitals, Clinical Laboratories, Academic Institutes, and Others. The Hospitals segment accounted for the largest market revenue share of 50.2% in 2025, due to comprehensive diagnostic services, integration of advanced imaging, biopsy, and molecular testing facilities, and availability of skilled oncologists and pathologists. Hospitals are the preferred choice for patients seeking timely and accurate NSCLC diagnosis, as well as for early-stage screening programs. The presence of advanced diagnostic equipment and in-house labs enables rapid testing and treatment planning, enhancing patient outcomes. Increasing government initiatives and healthcare infrastructure investments further boost hospital adoption.

The Academic Institutes segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by growing research initiatives in NSCLC diagnostics, clinical trials, and development of innovative testing solutions. Academic centers are increasingly collaborating with biotech and pharmaceutical companies for translational research, biomarker discovery, and precision oncology programs. Rising funding for lung cancer research, coupled with government grants, has significantly accelerated academic adoption of molecular diagnostic platforms. Academic institutes also play a crucial role in developing novel diagnostic kits and supporting training programs for healthcare professionals.

Europe Non-Small Cell Lung Cancer Diagnostics Market Regional Analysis

- The Europe non-small cell lung cancer diagnostics market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing lung cancer incidence, rising awareness for early diagnosis, and supportive government healthcare policies

- Countries such as the U.K. and Germany are witnessing strong adoption of molecular testing, biomarker profiling

- Precision oncology solutions across clinical laboratories, hospitals, and research centers, enhancing the overall demand for NSCLC diagnostic technologies

U.K. Non-Small Cell Lung Cancer Diagnostics Market Insight

The U.K. non-small cell lung cancer diagnostics market dominated Europe with the largest revenue share of approximately 39.8% in 2025, supported by advanced healthcare infrastructure, strong oncology research programs, and the presence of leading diagnostic companies. Widespread adoption of cutting-edge diagnostic solutions—including liquid biopsy, next-generation sequencing (NGS), and immunohistochemistry—along with continuous innovations, drives substantial market growth in the country. National cancer screening programs and the increasing implementation of biomarker-driven treatment approaches further encourage both public and private healthcare providers to adopt state-of-the-art NSCLC diagnostic solutions.

Germany Non-Small Cell Lung Cancer Diagnostics Market Insight

The Germany non-small cell lung cancer diagnostics market is expected to be the fastest-growing country in Europe during the forecast period, registering a CAGR of around 12.9%. Growth is fueled by rising lung cancer incidence, increasing healthcare expenditure, expanding oncology infrastructure, and growing awareness for early disease detection. Adoption of advanced diagnostics such as NGS, liquid biopsy, and multiplex immunoassays in hospitals and research institutions is accelerating early detection and improving patient outcomes. Additionally, Germany’s strong emphasis on precision medicine and investment in oncology research supports the rapid uptake of NSCLC diagnostic technologies across the country.

Europe Non-Small Cell Lung Cancer Diagnostics Market Share

The Non-Small Cell Lung Cancer Diagnostics industry is primarily led by well-established companies, including:

- Roche Diagnostics (Switzerland)

- Thermo Fisher Scientific (U.S.)

- Abbott (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Qiagen (Netherlands)

- Illumina (U.S.)

- Agilent Technologies (U.S.)

- Hologic (U.S.)

- Bio-Rad Laboratories (U.S.)

- Siemens Healthineers (Germany)

- Becton Dickinson (U.S.)

- PerkinElmer (U.S.)

- Guardant Health (U.S.)

- Foundation Medicine (U.S.)

- Myriad Genetics (U.S.)

- Laboratory Corporation of America (U.S.)

- Genomic Health (U.S.)

- Epigenomics AG (Germany)

- Luminex Corporation (U.S.)

- Invitae Corporation (U.S.)

Latest Developments in Europe Non-Small Cell Lung Cancer Diagnostics Market

- In May 2025, the NHS in England became the first health service in the world to roll out a routine “liquid biopsy” blood test for lung cancer patients, enabling genomic testing of circulating tumour DNA (ctDNA) to guide personalised treatment decisions and accelerate access to targeted therapy compared with traditional biopsy workflows. The test detects tumour DNA fragments in blood and has been made available at NHS hospitals following pilot studies showing that it can deliver results significantly faster than tissue biopsies, helping up to 15,000 lung cancer patients annually receive timely, targeted treatment

- In June 2025, liquid biopsy for lung and breast cancer became available routinely across the National Health Service (NHS) in England, offering broad access to ctDNA testing as part of standard genomic diagnostics for NSCLC and other cancers. This “blood test first” approach enables clinicians to detect actionable mutations earlier, often reducing the need for invasive tissue biopsies and supporting faster treatment decisions for patients with suspected lung cancer

- In November 2025, the FDA cleared Thermo Fisher Scientific’s Oncomine Dx Target Test as a companion diagnostic for identifying patients with HER2 TKD‑mutant NSCLC eligible for sevabertinib (HYRNUO™), further reinforcing the critical role of NGS‑based tests in matching patients with specific targeted therapies in advanced lung cancer. This regulatory decision underscores the growing reliance on genomic sequencing platforms in routine NSCLC diagnostic workflows

- In November 2025, Thermo Fisher Scientific received FDA approval for its Oncomine Dx Target Test as a companion diagnostic to support the newly approved Bayer therapy HYRNUO (sevabertinib) for advanced NSCLC patients with HER2 mutations, enabling precise patient identification and personalised treatment plans based on tumour genetic profiles. This expanded use of the Oncomine Dx platform broadens access to targeted care for a subset of NSCLC patients

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.