Global Oil And Gas Infrastructure Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

561.30 Million

USD

987.20 Million

2025

2033

USD

561.30 Million

USD

987.20 Million

2025

2033

| 2026 –2033 | |

| USD 561.30 Million | |

| USD 987.20 Million | |

| % | |

|

Global Oil & Gas Infrastructure Market Segmentation, By Category (Surface and Lease Equipment, Gathering and Processing, Gas and NGL Pipelines, Oil and Gas Storage, Refining and Oil Products Transport, and Export Terminals), Operation (Transmission and Distribution) - Industry Trends and Forecast to 2033

¿Qué es la infraestructura mundial de petróleo y gasTamaño del mercado y tasa de crecimiento?

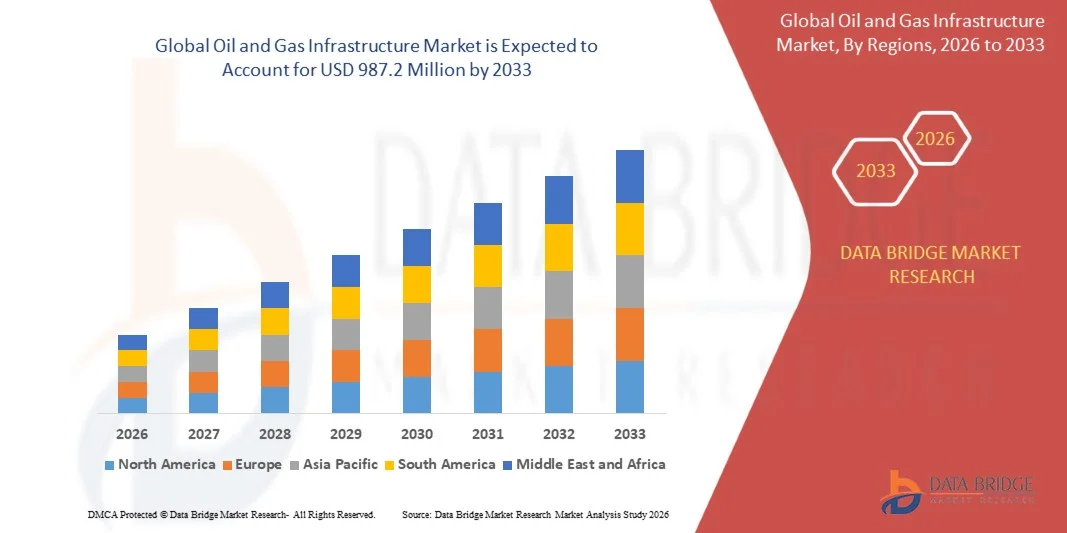

- Se valoró el tamaño del mercado mundial de la infraestructura de petróleo y gasUSD 561,3 millones en 2025y se espera que alcanceUSD 987,2 millones en 2033, aCAGR of5.20%durante el período previsto

- El crecimiento del mercado está respaldado por la creciente demanda de sistemas electrónicos eficientes y de alto rendimiento, la creciente aplicación de analizadores lógicos en circuitos integrados, computadoras personales y dispositivos de memoria, y la creciente necesidad de detección de errores, depuración lógica compleja y pruebas de circuito digital

- Además, se espera que la rápida adopción de dispositivos habilitados para IoT, los avances tecnológicos en los analizadores de lógica digital y las capacidades de activación y análisis mejoradas aceleren aún más la expansión del mercado.

¿Cuáles son los principales Takeaways of Oil & Gas Infrastructure Market?

- Ampliar la demanda de tabletas, PC y sistemas electrónicos avanzados en las economías en desarrollo, junto con un número creciente de iniciativas de investigación y desarrollo, está creando importantes oportunidades de crecimiento y fortaleciendo las perspectivas a largo plazo del mercado de la infraestructura de gas y petróleo

- Sin embargo, se espera que desafíos como la escasez de profesionales cualificados, el aumento de las complejidades de diseño e integración y las cuestiones de interacción de los sistemas actúen como limitaciones clave, lo que podría limitar el crecimiento del mercado durante el período previsto

- América del Norte dominaba el mercado de infraestructura de gas y petróleo con una cuota de ingresos estimada del 34,26% en 2025, impulsada por inversiones a gran escala en redes de oleoductos, terminales de GNL, instalaciones de almacenamiento de petróleo y refinación de infraestructura en Estados Unidos y Canadá

- Se prevé que Asia-Pacífico registrará el CAGR más rápido del 5,9% entre 2026 y 2033, impulsado por el aumento de la demanda energética, la rápida industrialización, la urbanización y la expansión del consumo de gas de petróleo en China, India, Japón, Corea del Sur y Asia sudoriental

- El segmento Gas y NGL Pipelines dominaron el mercado con una cuota estimada del 38,6% en 2025, debido a las extensas inversiones en tuberías de transmisión cruzadas, el aumento de la demanda de gas natural y la expansión de redes de transporte de GNL y NGL

Ámbito de presentación de informesSegmentación del mercado de la infraestructura de petróleo

| Atributos | Clave de infraestructura de gasMarket Insights |

| Segmentos cubiertos |

|

| Países cubiertos | América del Norte

Europa

Asia y el Pacífico

Oriente Medio y África

América del Sur

|

| Principales jugadores del mercado |

|

| Oportunidades de mercado |

|

| Valor añadido Data Infosets | Además de las ideas sobre escenarios de mercado como el valor de mercado, la tasa de crecimiento, la segmentación, la cobertura geográfica y los principales actores, los informes de mercado comisariados por el Data Bridge Market Research también incluyen análisis profundos de expertos, análisis de precios, análisis de acciones de la marca, análisis de la demografía, análisis de la cadena de suministro, análisis de la cadena de valor, visión general de materias primas/consumibles, criterios de selección de proveedores, análisis de PESTLE Analysis, análisis de PESTLE, análisis, análisis de Porter, análisis de Porter y marco regulador. |

¿Cuál es la tendencia clave en el mercado de infraestructura de petróleo y gas?

“Aumentar el cambio hacia sistemas de infraestructura de petróleo, inteligentes e integrados”

- El mercado de la infraestructura del petróleo y el gas es testigo de la creciente adopción de sistemas de vigilancia digital, sensores inteligentes y control integrados para aumentar la eficiencia operacional, la seguridad y la fiabilidad de los activos en las instalaciones de corriente superior, de corriente media y aguas abajo

- Los desarrolladores de infraestructura están implementando plataformas de automatización, sistemas SCADA, gemelos digitales y analíticas habilitadas para IA para optimizar operaciones de tuberías, gestión de almacenamiento y procesos de refinación

- La creciente demanda de infraestructuras rentables, supervisadas remotamente y predecibles para el mantenimiento está impulsando la adopción a través de tuberías, terminales, refinerías e instalaciones offshore

- Por ejemplo, empresas como Shell, BP, Exxon Mobil y Baker Hughes están integrando tecnologías digitales de campo de petróleo, monitoreo de activos en tiempo real y plataformas de decisión basadas en datos en proyectos de infraestructura global

- El aumento de la atención en la transparencia operacional, la vigilancia de las emisiones y el cumplimiento reglamentario está acelerando el cambio hacia la infraestructura inteligente y conectada del gas

- A medida que los sistemas energéticos se vuelvan más complejos y impulsados por la sostenibilidad, la infraestructura de petróleo y gas digital seguirá siendo crítica para el transporte y procesamiento energético resistentes, seguros y eficientes

¿Cuáles son los principales impulsores del mercado de infraestructura de petróleo y gas?

- Aumento de la demanda mundial de transporte energético, capacidad de almacenamiento y refinación de infraestructura para apoyar el aumento del consumo de petróleo y gas

- Por ejemplo, durante 2024–2025, los principales operadores como TotalEnergies, Chevron y SLB ampliaron las inversiones en modernización de tuberías, terminales de GNL y mejoras de infraestructura digital

- El creciente desarrollo de instalaciones de GNL, oleoductos transfronterizos y terminales de exportación en América del Norte, Asia y el Pacífico y Oriente Medio está impulsando el gasto en infraestructura

- Los avances en la automatización, la ingeniería de materiales, la vigilancia de la corrosión y la gestión de activos digitales están fortaleciendo el rendimiento de la infraestructura y la eficiencia del ciclo de vida

- Aumentar las inversiones en la infraestructura de gas natural como combustible de transición, junto con activos compatibles con hidrógeno y bajo carbono, están apoyando el crecimiento a largo plazo

- Respaldado por los gastos de capital sostenidos, las iniciativas de seguridad energética y los programas de modernización de infraestructuras, se espera que el mercado de infraestructura de petróleo y gas sea testigo de una expansión constante a largo plazo

¿Qué factor está afectando el crecimiento del mercado de infraestructura de petróleo y gas?

- Los altos costos de capital asociados con la construcción de oleoductos, infraestructura offshore, instalaciones de almacenamiento y mejoras de refinería limitan el despliegue rápido

- Por ejemplo, durante 2024–2025, la volatilidad de los precios materiales, las perturbaciones de la cadena de suministro y la escasez de mano de obra calificada aumentaron los costos de los proyectos y aumentaron los plazos

- Los marcos reglamentarios complejos, las aprobaciones ambientales y los problemas de adquisición de tierras retrasan el desarrollo de la infraestructura

- La creciente presión de las políticas de transición energética, los objetivos de descarbonización y la oposición pública crea incertidumbre para las inversiones a largo plazo en infraestructura de combustibles fósiles

- La competencia por la infraestructura de energía renovable y los combustibles alternativos afecta a la asignación de capital y la priorización de proyectos

- Para mitigar estos desafíos, las empresas se centran en la optimización digital, la construcción modular, las tecnologías de reducción de emisiones y la infraestructura que se reactiva para mantener el crecimiento en el mercado de la infraestructura de petróleo

¿Cómo se aumenta el mercado de infraestructura de petróleo y gas?

El mercado se segmenta sobre la base decategoría y funcionamiento.

• Por categoría

Sobre la base de la categoría, el mercado de infraestructura de petróleo y gas se segmenta en equipos de superficie y plomo, recolección y procesamiento, tuberías de gas y NGL, almacenamiento de petróleo y gas, transporte de productos derivados y petróleo y terminales de exportación. El segmento Gas y NGL Pipelines dominaron el mercado con una cuota estimada del 38,6% en 2025, debido a las extensas inversiones en tuberías de transmisión cruzadas, el aumento de la demanda de gas natural y la expansión de redes de transporte de GNL y NGL. Las tuberías siguen siendo la columna vertebral de la infraestructura de petróleo y gas, ofreciendo un transporte rentable, de alta capacidad y continuo a través de operaciones de corriente, corriente media y aguas abajo. Aumentar el enfoque en la seguridad energética, la conectividad interregional y la sustitución de las redes de tuberías de envejecimiento apoya aún más el dominio.

Se espera que el segmento Export Terminals crezca en el CAGR más rápido de 2026 a 2033, impulsado por el rápido crecimiento de las exportaciones de GNL, el aumento del comercio de petróleo crudo y la expansión de la infraestructura portuaria en América del Norte, Oriente Medio y Asia-Pacífico. El aumento del comercio mundial de energía y las inversiones en las instalaciones de almacenamiento y carga están acelerando el crecimiento de los segmentos.

• Por operación

Sobre la base de la operación, el mercado de infraestructura de gas y petróleo se segmenta en Transmisión y Distribución. El segmento Transmission dominó el mercado con una cuota de ingresos de alrededor del 61,4% en 2025, respaldada por inversiones a gran escala en tuberías de larga distancia, redes de transmisión de alta capacidad y corredores de energía transfronterizos. La infraestructura de transmisión desempeña un papel fundamental en el transporte de petróleo crudo, gas natural y productos refinados de los lugares de producción y procesamiento a los centros de consumo y exportación. Aumentar el desarrollo de tuberías de transmisión de gas natural, líneas de alimentación de GNL y redes interestatales fortalece el liderazgo de este segmento.

Se prevé que el segmento de distribución crecerá en el CAGR más rápido de 2026 a 2033, impulsado por la creciente urbanización, la expansión de las redes de distribución de gas urbano y la creciente demanda de conectividad de última millas en sectores industriales, comerciales y residenciales. Las iniciativas gubernamentales para ampliar el acceso al gas y modernizar la infraestructura de distribución están apoyando aún más el rápido crecimiento.

¿Qué región posee la mayor parte del mercado de infraestructura de petróleo y gas?

- América del Norte dominaba el mercado de infraestructura de gas y petróleo con una cuota de ingresos estimada del 34,26% en 2025, impulsada por inversiones a gran escala en redes de oleoductos, terminales de GNL, instalaciones de almacenamiento de petróleo y refinación de infraestructura en Estados Unidos y Canadá. La fuerte producción de petróleo y gas de esquisto, la expansión de los activos de corriente media y la modernización de la infraestructura de envejecimiento siguen alimentando el crecimiento del mercado regional

- Las compañías líderes de petróleo y gas en América del Norte están invirtiendo fuertemente en expansiones de oleoductos, terminales de exportación de GNL, sistemas de monitoreo digital y actualizaciones de seguridad, fortaleciendo el liderazgo de infraestructura de la región. La asignación continua de capital hacia la seguridad energética y la capacidad de exportación apoya la expansión del mercado a largo plazo

- Los marcos regulatorios bien establecidos, las capacidades avanzadas de ingeniería y una fuerte presencia de operadores mundiales de gas y petróleo refuerzan aún más el dominio de América del Norte en el mercado de infraestructura de petróleo

Mercado de la Infraestructura de Gas

Estados Unidos es el mayor contribuyente de América del Norte, con el apoyo de una amplia producción de esquisto, una red de tuberías densa, una gran capacidad de refinación y una rápida expansión de los terminales de exportación de GNL. El aumento de las inversiones en los oleoductos de crudo, la transmisión de gas natural, las instalaciones de almacenamiento y la infraestructura portuaria impulsan una fuerte demanda. La presencia de las principales empresas de gas y petróleo, una fuerte disponibilidad de capital y mejoras continuas de infraestructura apoyan aún más el crecimiento del mercado.

Canadá Oil & Gas Infrastructure Market Insight

Canadá contribuye significativamente debido al desarrollo continuo de infraestructuras de arenas petrolíferas, tuberías transfronterizas, instalaciones de procesamiento de gas y proyectos de exportación de GNL. El apoyo del Gobierno a las exportaciones de energía, la modernización de la infraestructura y la diversificación de las rutas de exportación refuerza el crecimiento del mercado a largo plazo.

Mercado de infraestructura de petróleo y gas de Asia y el Pacífico

Se prevé que Asia-Pacífico registrará el CAGR más rápido del 5,9% entre 2026 y 2033, impulsado por el aumento de la demanda energética, la rápida industrialización, la urbanización y la expansión del consumo de gas de petróleo en China, India, Japón, Corea del Sur y Asia sudoriental. Las inversiones a gran escala en refinerías, oleoductos, terminales de importación de GNL y instalaciones de almacenamiento están acelerando el desarrollo de la infraestructura.

China Oil & Gas Infrastructure Market Insight

China es el mayor contribuyente de Asia-Pacífico, apoyado por inversiones masivas en oleoductos, terminales de GNL, reservas estratégicas de petróleo y capacidad de refinación. Las iniciativas de seguridad energética dirigidas por el Gobierno y el aumento del consumo de gas siguen aumentando la expansión de la infraestructura.

Japón Petróleo & Mercado de Infraestructura de Gas

Japón muestra un crecimiento constante debido a la fuerte demanda de terminales de importación de GNL, instalaciones de almacenamiento y mejoras de refinación. Centrarse en la seguridad energética y las fuentes de suministro diversificadas apoya la inversión sostenida en infraestructura.

India Oil & Gas Infrastructure Market Insight

India está surgiendo como un mercado de alto crecimiento, impulsado por la rápida expansión de gasoductos, redes de distribución de gas, refinerías y terminales de GNL. Las iniciativas gubernamentales y el aumento de la demanda de energía aceleran el desarrollo de la infraestructura.

Sur Korea Oil & Gas Infrastructure Market Insight

Corea del Sur contribuye significativamente a través de inversiones en terminales de GNL, capacidad de refinación e infraestructura de almacenamiento. La fuerte demanda industrial y la dependencia de la importación de energía apoyan el crecimiento continuo del mercado.

¿Cuáles son las mejores empresas del mercado de infraestructura de petróleo y gas?

La industria de la infraestructura de petróleo y gas está dirigida principalmente por empresas bien establecidas, incluyendo:

- Exxon Mobil Corporation (Estados Unidos)

- Shell (Reino Unido)

- BP (U.K.)

- Chevron Corporation (Estados Unidos)

- TotalEnergias (Francia)

- Baker Hughes Company (Estados Unidos)

- Centrica (Reino Unido)

- ConocoPhillips (Estados Unidos)

- Energy Transfer (U.S.)

- Enterprise Products Partners (U.S.)

- Hatch (Canadá)

- Halliburton (Estados Unidos)

- Kinder Morgan (Estados Unidos)

- Marathon Oil Company (Estados Unidos)

- NGL Energy Partners (Estados Unidos)

- Occidental Petroleum Corporation (U.S.)

- ONEOK (U.S.)

- Royal Vopak (Países Bajos)

- SLB (Estados Unidos)

- WILLIAMS (Estados Unidos)

¿Cuáles son los avances recientes en el mercado mundial de infraestructura de petróleo y gas?

- En enero de 2025, Baker Hughes obtuvo un pedido importante de Tecnicas Reunidas para suministrar seis compresores de propano y seis trenes de compresión de gas para la tercera fase del campo de gas Jafurah de Saudi Aramco en Arabia Saudí, incluyendo soluciones de compresión a motor eléctrico, y el proyecto también complementará la colaboración a largo plazo de Baker Hughes con Aramco a través de múltiples instalaciones de gas, fortaleciendo la posición de la empresa a través de la infraestructura de gas natural

- En enero de 2025, BP inició con éxito el flujo de gas de pozos en el proyecto Greater Tortue Ahmeyim Phase 1 LNG, encauzando producción a su buque FPSO para la próxima etapa de puesta en marcha, y una vez completado el proyecto se espera que proporcione más de 2.3 millones de toneladas de GNL anualmente, marcando un hito clave que mejora la huella global de BP y perspectivas de crecimiento a largo plazo

- En septiembre de 2024, Exxon Mobil Corporation y Mitsubishi Corporation firmaron un acuerdo marco de proyecto que permite la participación de Mitsubishi en la avanzada instalación Baytown, Texas de Exxon Mobil, que producirá hidrógeno de bajo carbono con alrededor del 98% de eficiencia de captura de carbono y hasta mil millones de bcf por día de hidrógeno, junto con un millón de toneladas de amoníaco de bajo carbono anualmente, apoyando el impulso estratégico de ambas empresas hacia infraestructura energética de baja carbono

- En agosto de 2024, Chevron anunció una inversión de USD 1 mil millones para establecer un Centro de Excelencia de Ingeniería e Innovación en Bengaluru como su primer centro de ingeniería e innovación a gran escala en la India, centrado en las capacidades digitales y de ingeniería, reforzando el compromiso a largo plazo de Chevron con soluciones energéticas impulsadas por tecnología y expansión de la innovación mundial

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.