Global Tank Insulation Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

Segmento del mercado de aislamiento de tanques, por tipo (toraje y transporte), tipo de material (poliestireno superior (EPS), rocoso, vidrio celular, fibra de vidrio, espuma elastómerica, poliuretano (PU), y otros), tipo de temperatura (aislamiento de techo y aislamiento frío), tipo de tanque (tanque vertical, cisterna horizontal)

Tank Insulation Market Size

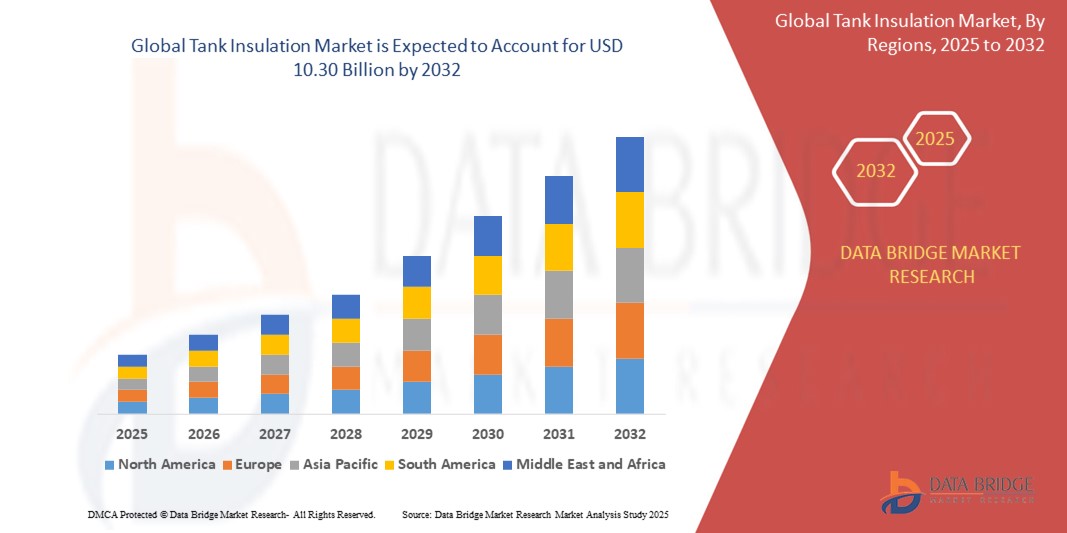

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Tabla de contenido

CUADRO DE INGRESOS GLOBALES

1 INTRODUCCIÓN

1.1 OBJETIVOS DEL ESTUDIO 1.2 DEFINICIÓN DEL MERCADO 1.3 EXAMEN GENERAL DEL MERCADO DE INSULACIÓN DE TANK GLOBAL 1.4 CURRENCÍA Y PRECUPACIÓN 1.5 LIMITACIONES 1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED 2.2 GEOGRAPHICAL SCOPE 2.3 YEARS CONSIDEED FOR THE STUDY 2.4 CURRENCY AND PRICING 2.5 DBMR TRIPOD DATA VALIDATION MODEL 2.6 TECHNOLOGY LIFE LINE CURVE 2.7 MULTIVARIATE MODELLING 2.8 PRIMARY INTERVIEWS with KEY OPINION LEAD

3 MARKET OVERVIEW

3.1 DRIVERS

3.1.1 INCREASING DEMAND from OIL & GAS INDUSTRY 3.1.2 GROWING DEMAND FOR CRYOGENICS INSULATION IN LNG STORAGE and TRANSPORTATION 3.1.3 GROWING DEMAND OF TEMPERATURE CONTROLLED PACKAGING FOR PHARMACEUTICALS 3.1.4 GROWING DEMAND OF MICA SHEETS IN TANKS TO PROVAL

3.2 RESTRAINTS

3.2.1 PRINCIPALES PRINCIPALES DE ARREGLO 3.2.2 CAMBIA DE LA ESTRUCTURA CHEMICA PARA LA ADULTERACIÓN DE LA INSULTACIÓN MATERIAL 3.2.3 UNAVAILABILIDAD DE MATERIALES PROFICIENTES PARA LA IRONA Y LA INDUSTRIA DE TELEMAS PARA HOLDAR EL METAL MÁSICO EN TANKOS 3.2.4

3.3 OPORTUNIDADES

3.3.1 Demanentes elevados para los quinques que se deben a la reducción de la capacidad de los pueblos indígenas en CHINA e INDIA 3.3.2 DEMANDA DE LAS MATERIALES INSULARES EN MANOS AGUAS PARA LOS RESIDENTIALES Y COMMERCIALES 3.3.3 INCREASING INDUSTRIALIZACIÓN EN LAS EMPRESAS

3.4

3.4.1 DERECHO Y EXPLOSIÓN A LA REACCIÓN CHEMICA CON EL MATERIAL INSULATIVO EN TANK 3.4.2 HAZARD DE SALUD DE MEDIAS INSULARES

RESUMEN EJECUTIVO 5 fotos INSIGHTS 6 INSIGHTS INDUSTRY 7 GLOBAL TANK INSULATION MARKET, BY TYPE

7.1 Examen general 7.2

8 MERCADO DE INSULACIÓN GLOBAL, POR MATERIAL TYPE

8.1 OVERVIEW 8.2 EXPANDED POLYSTYRENE (EPS) 8.3 ROCKWOOL 8.4 CELLULAR GLASS 8.5 FIBERGLASS 8.6 ELASTOMERIC FOAM 8.7 POLYURETHANE (PU) 8.8 OTHERS

9 MERCADO DE INSULACIÓN GLOBAL, POR TEMPERATURA

9.1 Examen general 9.2 HOT INSULATION 9.3 COLD INSULATION

10 GLOBAL TANK INSULATION MARKET, BY TANK TYPE

10.1 OVERVIEW 10.2 VERTICAL TANK 10.3 HORIZONTAL TANK 10.4 FIXED TANK 10.5 MOUNTED TANK

11 MERCADO DE INSULACIÓN GLOBAL, POR TANK ENDS

11.1 Examen general 11.2 DISH PARABOLIC 11.3

12 MERCADO DE INSULACIÓN GLOBAL, POR END-USER

12.1 Examen general 12.2 OIL Y GAS

12.2.1 OIL

12.2.1.1.1 CRUDE OIL 12.2.1.2 PETROCHEMICAL 12.2.1.3 OTHER CRUDE OIL DERIVATIVES

12.2.2 GAS

12.2.2.1 GAS NATURAL

12,3 ENERGÍA Y PODER 12,4 CAÍSTICA 12,5 FOOD Y BEVERAGES

12.5.1 FOOD 12.5.2 VIDAS

12.5.2.1 VENTAS ALCOHOLIC 12.5.2.2.2 DE FEBRERO 12.5.2.3 DROGAS AERATEDES 12.5.2.4 JUICES AND FLAVORED WATER 12.5.2.5 OTROS

12.6 PURIFICACIÓN DE AGUA

12.6.1 UBILDINGS COMMERCIALES 12.6.2 MUNICIPALITY 12.6.3 RESIDENTIAL BUILDINGS

12.7 WASTEWATER PURIFICATION

12.7.1 UBILDINGS COMMERCIALES 12.7.2 MUNICIPALITY 12.7.3 RESIDENTIAL BUILDINGS

12.8 OTROS

13 MERCADO DE INSULACIÓN GLOBAL, POR GEOGRAFÍA

13.1 PANORAMA GENERAL 13.2

13.2.1 U.S. 13.2.2 CANADA 13.2.3 MÉXICO

13.3 EUROPA

13.3.1 GERMANY 13.3.2 U.K 13.3.3 ITALIA 13.3.4 FRANCIA 13.3.5 ESPAÑA 13.3.6 SUIZA 13.3.7 RUSSIA 13.3.8 TURQUÍA 13.3.9 BELGIUM 13.3.10 13.3.11 Prueba de EUROPA

13.4 ASIA-PACIFIC

13.4.1 CHINA 13.4.2 INDIA 13.4.3 SOUTH KOREA 13.4.4 JAPÓN 13.4.5 AUSTRALIA 13.4.6 SINGAPORE 13.4.7 THAILAND 13.4.8 INDONESIA 13.4.9 MALAYSIA 13.4.10 PHILIPPINES 13.4.11 REST OF ASIA-PACIFIC

13.5 SOUTH AMERICA

13.5.1 BRASIL 13.5.2 ARGENTINA 13.5.3 REST OF SOUTH AMERICA

13.6 MIDDLE EAST AND AFRICA

13.6.1 UAE 13.6.2 SAUDI ARABIA 13.6.3 ISRAEL 13.6.4 SOUTH AFRICA 13.6.5 EGIPTO 13.6.6.6 REST OF MIDDLE EAST AND AFRICA

14 GLOBAL TANK INSULATION MARKET, COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: GLOBAL 14.2 COMPANY SHARE ANALYSIS: NORTH AMERICA 14.3 COMPANY SHARE ANALYSIS: EUROPE 14.4 COMPANY SHARE ANALYSIS: ASIA- PACIFIC 14.5 MERGERS ' ACQUISITIONS 14.6 NEW PRODUCT DEVELOPMENT ' APPROVALS 14.7 EXPANSIONS O.

15 COMPANY PROFILES

15.1 BASF SE

15.1.1 COMPANY SNAPSHOT 15.1.2 SWOT ANALYSIS 15.1.3 REVENUE ANALYSIS 15.1.4 COMPANY SHARE ANALISIS 15.1.5 PRESENCIA GEOGRÁFICA 15.1.6 PRODUCTOS PORTFOLIO 15.1.7 ACONTECIMIENTOS RECIENTES 15.1.8 DATOS BRIDGE MARKET RESEARCH ANALISIS

15.2 LA EMPRESA CHEMICA

15.2.1 COMPANY SNAPSHOT 15.2.2.2 SWOT ANALYSIS 15.2.3 REVENUE ANALISIS 15.2.4 COMPANY SHARE ANALISIS 15.2.5 PRESENCIA GEOGRÁFICA 15.2.6 PRODUCTOS PORTFOLIO 15.2.7 ACONTECIMIENTOS RECIENTES 15.2.8 DE DATOS BRIDGE MARKET

15.3 SAINT-GOBAIN

15.3.1 COMPANY SNAPSHOT 15.3.2 SWOT ANALYSIS 15.3.3 REVENUE ANALYSIS 15.3.4 COMPANY SHARE ANALISIS 15.3.5 PRESENCIA GEOGRÁFICA 15.3.6 PRODUCTOS PORTFOLIO 15.3.7 ACONTECIMIENTOS RECIENTES 15.3.8 DATOS DE MARKET RESEARCH ANALISIS

15.4 HUNTSMAN INTERNATIONAL LLC

15.4.1 COMPANY SNAPSHOT 15.4.2 SWOT ANALYSIS 15.4.3 REVENUE ANALYSIS 15.4.4.4 COMPANY SHARE ANALISIS 15.4.5 PRESENCIA GEOGRÁFICA 15.4.6 PRODUCTOS PORTFOLIO 15.4.7 ACONTECIMIENTOS RECIENTES 15.4.8 DATOS DE MARKET RESEARCH ANALISIS

15,5 KINGSPAN GROUP

15.5.1 COMPANY SNAPSHOT 15.5.2 SWOT ANALYSIS 15.5.3 REVENUE ANALYSIS 15.5.4 COMPANY SHARE ANALISIS 15.5.5.5.5 PRESENCIA GEOGRÁFICA 15.5.6 PRODUCTOS PORTFOLIO 15.5.7 ACONTECIMIENTOS RECIENTES 15.5.8 DE DATOS BRIDGE MARKET RESEARCH ANALISIS

15.6 ARMACELL LLC

15.6.1 SNAPSHOT 15.6.2 ANÁLISIS REVENIDO 15.6.3 PRESENCIA GEOGRÁFICA 15.6.4 DE PRODUCTOS PORTFOLIO 15.6.5 ACONTECIMIENTOS RECIENTES

15.7 CABOT CORPORATION

15.7.1 SNAPSHOT 15.7.2 ANÁLISIS REVENIDO 15.7.3 PRESENCIA GEOGRÁFICA 15.7.4 DE PRODUCTOS PORTFOLIO 15.7.5 ACONTECIMIENTOS RECIENTES

15.8 SOLUCIONES THERMALES COMMERCIALES, INC.

15.8.1 COMPANY SNAPSHOT 15.8.2 PRODUCT PORTFOLIO 15.8.3 RECENTIMIENTO

15.9 TECNOLOGÍAS REISTENTES DE CORROSIÓN, INC.

15.9.1 SNAPSHOT 15.9.2 PRODUCTO PORTFOLIO 15.9.3 DESARROLLO RECIENTE

15.10 DUNMORE

15.10.1 SNAPSHOT 15.10.2 PRESENCIA GEOGRÁFICA 15.10.3 PRODUCTOS PORTFOLIO 15.10.4 ACONTECIMIENTOS RECIENTES

15.11 GILSULATE INTERNATIONAL, INC.

15.11.1 SNAPSHOT 15.11.2 PRODUCTO PORTFOLIO 15.11.3 ACONTECIMIENTOS RECIENTES

15.12 LTD de la FACTORIA DE COOL

15.12.1 COMPANY SNAPSHOT 15.12.2 PRODUCTO PORTFOLIO 15.12.3

15.13 INSULATION SYSTEMS

15.13.1 SNAPSHOT 15.13.2 PRESENCIA GEOGRÁFICA 15.13.3 PRODUCTO PORTFOLIO 15.13.4 ACONTECIMIENTOS RECIENTES

15.14 JOHNS MANVILLE

15.14.1 SNAPSHOT 15.14.2 PRESENCIA GEOGRÁFICA 15.14.3 PRODUCTOS PORTFOLIO 15.14.4 ACONTECIMIENTOS RECIENTES

15.15 J.H. ZIEGLER GMBH

15.15.1 SNAPSHOT 15.15.2 PRESENCIA GEOGRÁFICA 15.15.3 PRODUCTO PORTFOLIO 15.15.4 DESARROLLO RECIENTE

15.16 KNAUF INSULATION

15.16.1 SNAPSHOT 15.16.2 PRESENCIA GEOGRÁFICA 15.16.3 PRODUCTO PORTFOLIO 15.16.4 ACONTECIMIENTOS RECIENTES

15.17 MAYES COATINGS ' INSULATION, INC.

15.17.1 SNAPSHOT 15.17.2 PRODUCTO PORTFOLIO 15.17.3 ACONTECIMIENTOS RECIENTES

15,18 OWENS CORNING

15.18.1 SNAPSHOT 15.18.2 ANÁLISIS REVENIDO 15.18.3 PRESENCIA GEOGRÁFICA 15.18.4 DE PRODUCTOS PORTFOLIO 15.18.5 ACONTECIMIENTOS RECIENTES

15.19 POLARCLAD TANK INSULATION

15.19.1 COMPANY SNAPSHOT 15.19.2 PRODUCTO PORTFOLIO 15.19.3

15.20 GRUPO DE ÖCHLING

15.20.1 SNAPSHOT 15.20.2 PRESENCIA GEOGRÁFICA 15.20.3 PRODUCTOS PORTFOLIO 15.20.4

15.21 ROCKWOOL INTERNATIONAL A/S

15.21.1 15.21.2 ANÁLISIS REVENIO 15.21.3 PRESENCIA GEOGRÁFICA 15.21.4 PRODUCTOS PORTFOLIO 15.21.5 ACONTECIMIENTOS RECIENTES

15.22 SPX TRANSFORMER SOLUTIONS INC.

15.22.1 COMPANY SNAPSHOT 15.22.2 PRODUCT PORTFOLIO 15.22.3 ACONTECIMIENTOS RECIENTES

15.23 SYNAVAX

15.23.1 SNAPSHOT 15.23.2 SOLUCIÓN PORTFOLIO 15.23.3 ACONTECIMIENTOS RECIENTES

15.24 THERMACON

15.24.1 SNAPSHOT 15.24.2 PRODUCTO PORTFOLIO 15.24.3 DESARROLLO RECIENTE

15.25 T.F.WARREN GROUP

15.25.1 SNAPSHOT 15.25.2 PRESENCIA GEOGRÁFICA 15.25.3 PRODUCTO PORTFOLIO 15.25.4 ACONTECIMIENTOS RECIENTES

16 CUESTIÓN 17 CONCLUSIÓN 18 INFORMES CONEXOS

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.