North America Polyethylene Pipes Market

Tamaño del mercado en miles de millones de dólares

Tasa de crecimiento anual compuesta (CAGR) :

%

USD

8.22 Billion

USD

11.83 Billion

2025

2033

USD

8.22 Billion

USD

11.83 Billion

2025

2033

| 2026 –2033 | |

| USD 8.22 Billion | |

| USD 11.83 Billion | |

| % | |

|

North America Polyethylene Pipes Market Segmentation, By Type (HDPE (High Density Polyethylene), Cross Link Polyethylene, LDPE (Low Density Polyethylene), and LLDPE (Linear Low Density Polyethylene)), Application (Underwater and Municipal, Gas Extraction, Construction, Industrial, Agriculture, and Others) - Industry Trends and Forecast to 2033

North America Polyethylene Pipes Market Size

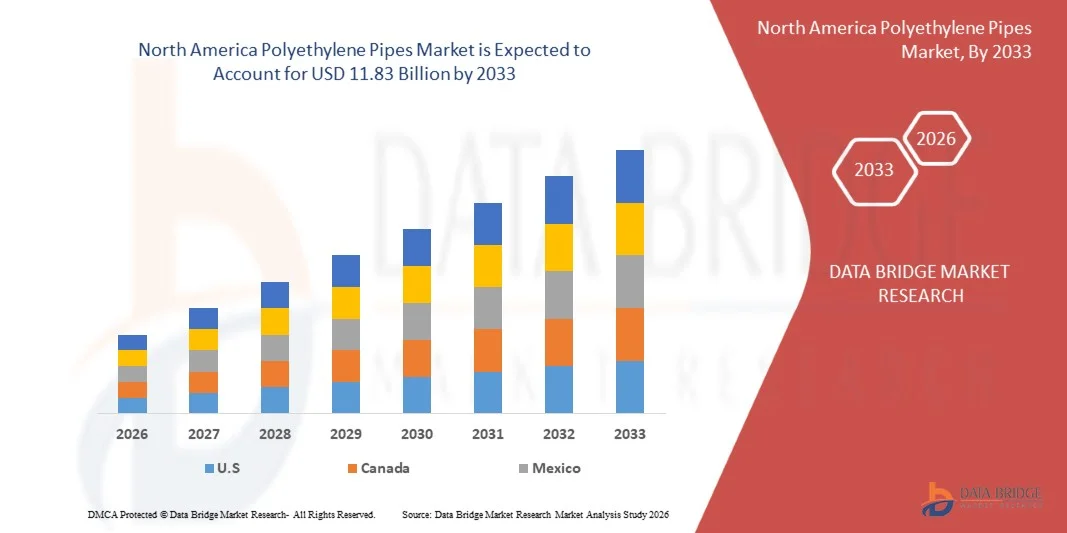

- The North America Polyethylene Pipes Market size was valued at USD 8.22 billion in 2025 and is expected to reach USD 11.83 billion by 2033, at a CAGR of 4.65% during the forecast period

- The market growth is largely fueled by the increasing demand for durable, corrosion-resistant, and flexible piping solutions across municipal, industrial, and agricultural applications. The superior performance of polyethylene pipes in water supply, sewage systems, and gas distribution is driving widespread adoption and reinforcing their preference over traditional materials such as steel or concrete

- Furthermore, rising infrastructure investments and urbanization are creating significant demand for high-quality piping systems. For instance, companies such as Advanced Drainage Systems are expanding production and distribution capacities to meet growing municipal and industrial needs. These converging factors are accelerating the uptake of polyethylene pipes, thereby significantly boosting the industry’s growth

North America Polyethylene Pipes Market Analysis

- Polyethylene pipes, offering high chemical resistance, lightweight handling, and long service life, are increasingly preferred in large-scale construction, irrigation, and industrial projects due to their cost-efficiency and reliability

- The escalating adoption of polyethylene pipes is primarily fueled by government initiatives to improve water supply networks, strict regulations on pipeline safety, and increasing awareness of sustainable and long-lasting piping solutions among contractors and end-users

- U.S. dominated the North America Polyethylene Pipes Market in 2025, due to strong adoption in municipal water supply, sewage, gas distribution, and industrial pipeline projects, well-established polymer manufacturing capabilities, and increasing preference for durable, corrosion-resistant piping solutions

- Canada is expected to be the fastest growing country in the North America Polyethylene Pipes Market during the forecast period due to increasing adoption in water distribution, sewage systems, and industrial pipelines

- HDPE (High Density Polyethylene) segment dominated the market with a market share of 46.3% in 2025, due to its high strength-to-density ratio, excellent chemical resistance, and long service life. HDPE pipes are extensively used in municipal water supply, gas distribution, and industrial applications due to their durability and ability to withstand high pressure and environmental stress. The segment also benefits from ease of installation, low maintenance requirements, and compatibility with modern piping systems, making it a preferred choice among contractors and municipalities

Report Scope and North America Polyethylene Pipes Market Segmentation

|

Attributes |

Polyethylene Pipes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

North America Polyethylene Pipes Market Trends

“Rising HDPE Pipe Adoption in Infrastructure”

- A significant trend in the North America Polyethylene Pipes Market is the growing adoption of high-density polyethylene (HDPE) pipes in urban and rural infrastructure projects, driven by their durability, corrosion resistance, and cost-efficiency compared to traditional materials. This adoption is enhancing pipeline longevity and reducing maintenance requirements across water supply, sewage, and gas distribution networks

- For instance, companies such as JM Eagle and Astral Pipes supply HDPE and polyethylene piping systems for large-scale municipal water projects and industrial installations. Their products are widely used in utility networks and construction projects requiring long-lasting and reliable pipeline solutions

- The use of HDPE pipes is increasing in irrigation and agricultural applications where leak-proof, flexible, and chemical-resistant piping is critical. This trend supports efficient water management practices and helps reduce resource wastage

- Industries focusing on oil, gas, and chemical transport are integrating polyethylene pipes due to their high chemical inertness and ability to withstand harsh environmental conditions. This integration is reinforcing polyethylene as a preferred material for safe and reliable fluid conveyance

- The construction sector is expanding the use of polyethylene pipes for underground and above-ground applications owing to their lightweight nature and ease of installation. This reduces labor costs and accelerates project timelines in both residential and commercial projects

- The market is witnessing steady growth in industrial and municipal infrastructure projects where long-lasting, corrosion-free, and environmentally resistant polyethylene pipes contribute to improved system reliability. This rising incorporation of polyethylene piping systems is reinforcing their strategic importance in modern infrastructure development

North America Polyethylene Pipes Market Dynamics

Driver

“Growing Demand for Durable and Corrosion‑Resistant Pipes”

- The growing need for long-lasting and low-maintenance pipeline solutions is driving the demand for polyethylene pipes, which offer superior durability, chemical resistance, and leak-proof performance. These features reduce operational downtime and enhance system efficiency across municipal, industrial, and agricultural applications

- For instance, Prince Pipes & Fittings has expanded its HDPE pipe portfolio to meet rising demand for potable water and sewage systems in India. Their durable products help utilities and contractors implement efficient water distribution networks with minimal maintenance

- The increasing replacement of aging metal pipes with corrosion-resistant polyethylene variants is supporting growth in urban and industrial infrastructure. This transition improves system longevity and reduces replacement cycles

- Growing investments in oil, gas, and chemical transport pipelines are accelerating the adoption of polyethylene pipes due to their high resistance to chemical attack and abrasion. These properties ensure safer and more efficient fluid transportation under demanding conditions

- The requirement for sustainable and leak-proof water management systems in smart cities and industrial parks is boosting the preference for polyethylene piping solutions. This driver continues to underpin market growth as infrastructure modernization advances

Restraint/Challenge

“High Initial Investment for Large Projects”

- The North America Polyethylene Pipes Market faces challenges due to the substantial upfront costs associated with large-scale pipeline projects, including procurement, installation, and integration expenses. These initial investments can limit adoption, especially for smaller municipalities or cost-sensitive projects

- For instance, municipal projects deploying HDPE pipelines supplied by JM Eagle often require significant capital outlay for trenching, welding, and network integration, creating financial barriers for budget-constrained authorities

- The cost of high-quality raw materials and compliance with international standards for potable water and industrial applications further increases project expenses. This can slow down procurement cycles and affect project planning

- Large infrastructure projects demand skilled labor for proper installation and fusion welding of polyethylene pipes, adding to labor costs and project complexity. These operational requirements can deter some stakeholders from immediate adoption

- The challenge of balancing project budgets with the long-term benefits of durable, corrosion-resistant piping continues to influence procurement decisions. This constraint underscores the need for financial planning and phased implementation strategies in expansive infrastructure projects

North America Polyethylene Pipes Market Scope

The market is segmented on the basis of type and application.

• By Type

On the basis of type, the North America Polyethylene Pipes Market is segmented into HDPE (High Density Polyethylene), Cross Link Polyethylene, LDPE (Low Density Polyethylene), and LLDPE (Linear Low Density Polyethylene). The HDPE segment dominated the market with the largest revenue share of 46.3% in 2025, driven by its high strength-to-density ratio, excellent chemical resistance, and long service life. HDPE pipes are extensively used in municipal water supply, gas distribution, and industrial applications due to their durability and ability to withstand high pressure and environmental stress. The segment also benefits from ease of installation, low maintenance requirements, and compatibility with modern piping systems, making it a preferred choice among contractors and municipalities. Growing infrastructure development and stringent government regulations on safe water distribution further reinforce the dominance of HDPE pipes in the regional and global markets.

The Cross Link Polyethylene segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by its superior thermal resistance and flexibility, making it suitable for hot water plumbing and underfloor heating systems. For instance, companies such as Uponor have been expanding production capacities to meet rising demand in residential and commercial construction projects. The ability of Cross Link Polyethylene pipes to maintain structural integrity under temperature fluctuations and its long operational life contribute to its growing adoption. The segment’s increasing use in energy-efficient and eco-friendly building projects further supports robust growth. In addition, advancements in manufacturing processes are enhancing the cost-effectiveness and performance of these pipes, accelerating their uptake across multiple applications.

• By Application

On the basis of application, the North America Polyethylene Pipes Market is segmented into Underwater and Municipal, Gas Extraction, Construction, Industrial, Agriculture, and Others. The Underwater and Municipal segment dominated the market with the largest revenue share in 2025, driven by rising urbanization and the growing need for reliable water and sewage distribution systems. Polyethylene pipes are preferred in these applications due to their corrosion resistance, leak-proof performance, and ease of handling during large-scale water supply projects. Municipal authorities often prioritize polyethylene pipes for long-term infrastructure projects to reduce maintenance costs and ensure sustainability. The adoption of smart city initiatives and increasing investments in municipal water management further reinforce the leadership of this segment.

The Gas Extraction segment is expected to witness the fastest CAGR from 2026 to 2033, fueled by increasing demand for natural gas pipelines and expansion of energy infrastructure. For instance, companies such as JM Eagle are supplying polyethylene pipes for high-pressure gas transportation, ensuring safety and regulatory compliance. The inherent strength, flexibility, and chemical resistance of polyethylene pipes make them suitable for challenging oil and gas extraction environments. Rising energy demands and exploration of new gas fields are driving rapid adoption in this segment. In addition, ongoing technological advancements in pipe manufacturing are enhancing durability and performance, contributing to accelerated market growth.

North America Polyethylene Pipes Market Regional Analysis

- U.S. dominated the North America Polyethylene Pipes Market with the largest revenue share in 2025, driven by strong adoption in municipal water supply, sewage, gas distribution, and industrial pipeline projects, well-established polymer manufacturing capabilities, and increasing preference for durable, corrosion-resistant piping solutions

- The demand for advanced polyethylene pipes is supported by large-scale production and infrastructure initiatives by companies such as JM Eagle and Pipelife, enabling consistent supply for applications including potable water networks, irrigation systems, and industrial fluid transport

- The presence of major pipe and polymer manufacturers, continuous advancements in HDPE and PE material technology, and integration of polyethylene piping into multiple large-scale infrastructure projects reinforce the U.S. leadership position in the North America market

Canada North America Polyethylene Pipes Market Insight

Canada is projected to register the fastest CAGR in the North America Polyethylene Pipes Market from 2026 to 2033, supported by increasing adoption in water distribution, sewage systems, and industrial pipelines. Rising use of HDPE and PE pipes in municipal water projects, irrigation networks, and gas transport is accelerating market growth. The development of advanced polymer processing facilities and collaborations with companies such as Prince Pipes & Fittings are strengthening production capabilities across the country. Growing emphasis on leak-proof, corrosion-resistant, and sustainable piping solutions positions Canada as the fastest-growing country in the region during the forecast period.

Mexico North America Polyethylene Pipes Market Insight

Mexico is expected to grow steadily from 2026 to 2033, driven by expanding municipal and industrial infrastructure projects and increasing demand for polyethylene pipes in water management, gas distribution, and chemical transport applications. The country’s role as a growing manufacturing hub is supporting adoption in large-scale fluid conveyance networks. Collaborations with global pipe manufacturers and expansion of production facilities are improving supply availability. Major companies such as Astral Pipes and JM Eagle are strengthening distribution networks in the region. These developments contribute to sustained growth of the North America Polyethylene Pipes Market throughout the forecast period.

North America Polyethylene Pipes Market Share

The polyethylene pipes industry is primarily led by well-established companies, including:

- Dow (U.S.)

- Exxon Mobil Corporation (U.S.)

- SABIC (Saudi Arabia)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- ISCO Industries (U.S.)

- Advanced Drainage Systems, Inc. (U.S.)

- Dura‑Line (U.S.)

- Arkema (France)

- JM Eagle (U.S.)

- Aliaxis Group (Belgium)

- WL Plastics (U.S.)

- Chevron Phillips Chemical Company LLC (U.S.)

- China Lesso Group Holdings Ltd. (China)

- Pipelife International GmbH (Austria)

Latest Developments in North America Polyethylene Pipes Market

- In August 2025, Supreme Industries completed the acquisition of Wavin India’s pipes and fittings business, significantly enhancing its production footprint and technological capabilities in the Indian and regional markets. This acquisition allowed Supreme to integrate Wavin’s advanced piping technologies and expand its product portfolio, enabling the company to cater to a wider range of municipal, residential, and industrial projects. The move strengthened Supreme’s competitive position in the polyethylene pipes segment by increasing market penetration and improving supply chain efficiency, meeting the rising demand for high-quality and durable piping solutions across the region

- In May 2025, Advanced Drainage Systems (ADS) acquired River Valley Pipe, broadening its manufacturing capacity and distribution network in the U.S. Midwest. The acquisition enabled ADS to address increasing demand for HDPE drainage and pipe products in municipal, agricultural, and commercial infrastructure projects. By combining production capabilities and operational expertise, ADS enhanced its ability to supply large-scale infrastructure developments efficiently, reinforcing its market leadership and positioning itself as a preferred supplier for high-performance polyethylene piping solutions

- In November 2024, Fortress Investment Group acquired Infra Pipe Solutions, one of North America’s largest HDPE pipe manufacturers, strengthening its strategic presence in the infrastructure sector. This acquisition allowed Fortress to offer a more diversified product portfolio, including specialized HDPE pipes for water, gas, and industrial applications. By leveraging Infra Pipe Solutions’ technical expertise and established customer base, Fortress improved its capability to serve large-scale projects, support long-term infrastructure development, and capture higher market share in the competitive North American North America Polyethylene Pipes Market

- In October 2024, Lane Enterprises inaugurated a new plastic pipe production facility in Longview, Washington, expanding its capacity for corrugated HDPE pipes. This facility directly addresses the growing demand for stormwater management, drainage, and utility piping in infrastructure projects across the western U.S. The expansion improves supply reliability, reduces delivery lead times, and allows Lane Enterprises to meet increasing regulatory standards for sustainable and durable piping solutions, positioning the company to capitalize on urbanization and large-scale construction projects

- In February 2024, Chevron Phillips Chemical Company LLC and QatarEnergy initiated the construction of an integrated polymers complex at Ras Laffan, including substantial HDPE production units. This upstream investment strengthens the long-term availability of high-quality pipe-grade polyethylene resin, supporting the expansion of global pipe manufacturing capacities. By ensuring a stable and scalable supply of raw materials, the complex enables pipe manufacturers to innovate, produce higher-performance pipes, and meet rising global demand across water distribution, gas transportation, and industrial sectors, thereby influencing growth and resilience in the North America Polyethylene Pipes Market

SKU-

Obtenga acceso en línea al informe sobre la primera nube de inteligencia de mercado del mundo

- Panel de análisis de datos interactivo

- Panel de análisis de empresas para oportunidades con alto potencial de crecimiento

- Acceso de analista de investigación para personalización y consultas

- Análisis de la competencia con panel interactivo

- Últimas noticias, actualizaciones y análisis de tendencias

- Aproveche el poder del análisis de referencia para un seguimiento integral de la competencia

Metodología de investigación

La recopilación de datos y el análisis del año base se realizan utilizando módulos de recopilación de datos con muestras de gran tamaño. La etapa incluye la obtención de información de mercado o datos relacionados a través de varias fuentes y estrategias. Incluye el examen y la planificación de todos los datos adquiridos del pasado con antelación. Asimismo, abarca el examen de las inconsistencias de información observadas en diferentes fuentes de información. Los datos de mercado se analizan y estiman utilizando modelos estadísticos y coherentes de mercado. Además, el análisis de la participación de mercado y el análisis de tendencias clave son los principales factores de éxito en el informe de mercado. Para obtener más información, solicite una llamada de un analista o envíe su consulta.

La metodología de investigación clave utilizada por el equipo de investigación de DBMR es la triangulación de datos, que implica la extracción de datos, el análisis del impacto de las variables de datos en el mercado y la validación primaria (experto en la industria). Los modelos de datos incluyen cuadrícula de posicionamiento de proveedores, análisis de línea de tiempo de mercado, descripción general y guía del mercado, cuadrícula de posicionamiento de la empresa, análisis de patentes, análisis de precios, análisis de participación de mercado de la empresa, estándares de medición, análisis global versus regional y de participación de proveedores. Para obtener más información sobre la metodología de investigación, envíe una consulta para hablar con nuestros expertos de la industria.

Personalización disponible

Data Bridge Market Research es líder en investigación formativa avanzada. Nos enorgullecemos de brindar servicios a nuestros clientes existentes y nuevos con datos y análisis que coinciden y se adaptan a sus objetivos. El informe se puede personalizar para incluir análisis de tendencias de precios de marcas objetivo, comprensión del mercado de países adicionales (solicite la lista de países), datos de resultados de ensayos clínicos, revisión de literatura, análisis de mercado renovado y base de productos. El análisis de mercado de competidores objetivo se puede analizar desde análisis basados en tecnología hasta estrategias de cartera de mercado. Podemos agregar tantos competidores sobre los que necesite datos en el formato y estilo de datos que esté buscando. Nuestro equipo de analistas también puede proporcionarle datos en archivos de Excel sin procesar, tablas dinámicas (libro de datos) o puede ayudarlo a crear presentaciones a partir de los conjuntos de datos disponibles en el informe.