Asia Pacific Slimming Devices Market

Taille du marché en milliards USD

TCAC :

%

USD

1.31 Billion

USD

2.15 Billion

2025

2033

USD

1.31 Billion

USD

2.15 Billion

2025

2033

| 2026 –2033 | |

| USD 1.31 Billion | |

| USD 2.15 Billion | |

| % | |

|

Asia-Pacific Slimming Devices Market Segmentation, By Product (Electric Pulse Type, Vibration Type, Pneumatic Extrusion, and Others), Technology (Cryolipolysis, Low Level Laser Therapy, Focused Ultrasound, and Radiofrequency), Portability (Standalone and Portability), Body Area (Abdominal, Hip, Thighs, and Others), End User (Gyms and Fitness Centers, Wellness Centers, Home, and Others), Distribution Channel (Direct Tenders, and Over the Counter, Retail) - Industry Trends and Forecast to 2033

Quelle est la taille du marché et le taux de croissance des appareils de l'Asie-Pacifique

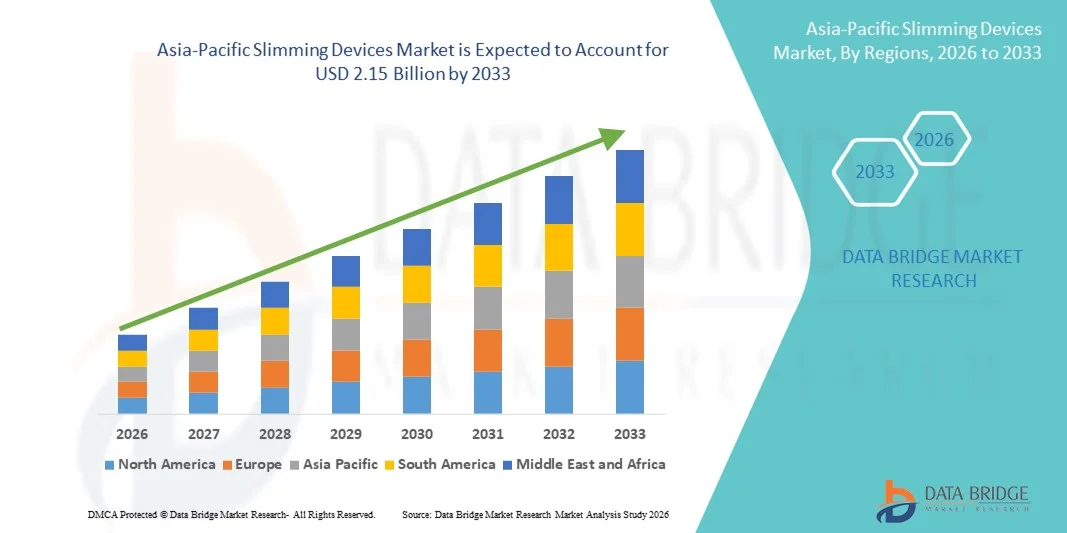

- Selon Data Bridge études de marché Analyse La taille du marché des dispositifs d'amincissement Asie-Pacifique a été évaluée à1,31 milliard de dollars en 2025et devrait atteindre2,15 milliards de dollars en 2033, à unTCAC de 6,40 %pendant la période de prévision

- La croissance du marché est largement alimentée par la prévalence croissante de l'obésité et des troubles liés au mode de vie, associée à une prise de conscience accrue de l'apparence physique et de la gestion de la santé. L'urbanisation croissante, les modes de vie sédentaires et les habitudes alimentaires malsaines contribuent de façon significative à accroître la demande de dispositifs minceurs non invasifs et peu invasifs dans les milieux cliniques et à domicile

- En outre, la préférence croissante pour les procédures esthétiques avec un temps d'arrêt minimal, ainsi que les progrès technologiques continus tels quelaserlipolyse, cryolipolyse,radiofréquence, et à base d'ultrasonsSystèmes de réduction des graisses, renforce l'adoption des produits. Ces facteurs convergents accélèrent l'adoption des solutions Slimming Devices, ce qui stimule considérablement l'expansion globale du marché

Taille du marché et prévisions

- Valeur marchande Asie-Pacifique (2025):1,31 milliard de dollars

- Valeur marchande prévue (2033) :2,15 milliards de dollars

- Prévisions CAGR (2026-2033):6.40%

Analyse du marché des dispositifs de limace Asie-Pacifique

- Les dispositifs de réduction des graisses non invasifs et peu invasifs et les solutions de contour du corps font de plus en plus partie intégrante des pratiques esthétiques et de bien-être modernes dans les milieux cliniques et à domicile en raison de leur commodité, de leur temps de récupération réduit et de leur préférence croissante pour les procédés cosmétiques non chirurgicaux

- L'augmentation de la demande de dispositifs d'amincissement est principalement alimentée par la prévalence croissante de l'obésité, une sensibilisation accrue à l'aspect physique et à la condition physique, et une forte évolution des consommateurs vers des traitements de contour du corps technologiquement avancés et sans douleur

- La Chine a dominé le marché des appareils minceur avec la plus grande part des revenus de 32,6 % en 2025, en raison de la sensibilisation croissante aux procédures cosmétiques non invasives, de la croissance rapide des cliniques esthétiques, de l'augmentation des revenus disponibles et de l'adoption généralisée de systèmes de contournage du corps à base de laser et d'énergie. Les initiatives gouvernementales visant à promouvoir les secteurs de la beauté et du bien-être, ainsi que la forte fabrication nationale d'appareils minceurs, renforcent encore la position de leader de la Chine sur le marché

- On s'attend à ce que l'Inde soit la région qui connaît la croissance la plus rapide du marché des dispositifs d'amincissement au cours de la période de prévision, avec une augmentation de 11,3 % du TCAC de 2026 à 2033, alimentée par l'intérêt croissant des consommateurs pour les traitements cosmétiques non invasifs, l'augmentation du revenu disponible, l'expansion du tourisme médical et l'accessibilité accrue des technologies d'amincissement modernes dans les zones urbaines et semi-urbaines. La prolifération des cliniques esthétiques et des campagnes de sensibilisation stimulent l'adoption rapide de dispositifs de réduction des graisses et de contours du corps partout au pays

- Le segment autonome a représenté la plus grande part du marché en 2025, soit 57,8 %, en raison de son utilisation généralisée dans les cliniques professionnelles et les centres de bien-être.

Étendue du rapport et segmentation du marché des dispositifs de réduction

|

Attributs |

Dispositifs de limace Aperçus clés du marché |

|

Segments couverts |

|

|

Pays couverts |

Asie-Pacifique

|

|

Principaux acteurs du marché |

|

|

Possibilités de marché |

|

|

Infos sur la valeur ajoutée |

|

Quelle est la tendance clé sur le marché des dispositifs de limace en Asie-Pacifique

Progrès technologiques dans les solutions de contournage non invasives

- Une tendance significative et accélérée sur le marché des dispositifs amincissants est l'adoption croissante de technologies de contour du corps non invasives et peu invasives, conçues pour réduire les graisses, resserrer la peau et améliorer l'esthétique du corps sans intervention chirurgicale

- Cette évolution technologique améliore considérablement l'efficacité du traitement, la sécurité et le confort des patients.

- Par exemple, en mars 2023, l'Allergan Aesthetics (AbbVie) a élargi la disponibilité de son système CoolSculpting Elite sur les marchés européens clés, offrant des applicateurs améliorés et une technologie de refroidissement optimisée pour améliorer la réduction des graisses. De même, Cynosure a mis en place en Asie-Pacifique des plates-formes de contournage du corps à base de radiofréquences afin d'améliorer la précision du serrage cutané et du traitement

- Les progrès dans les technologies telles que la cryolipolyse, la lipolyse laser, la cavitation par ultrasons et l'énergie radiofréquence permettent une réduction ciblée des graisses avec un temps d'arrêt minimal. Ces innovations permettent aux cliniques de fournir des plans de traitement personnalisés basés sur la composition corporelle individuelle et des objectifs esthétiques

- La préférence croissante pour les procédures cosmétiques ambulatoires et le passage à la réduction des graisses non chirurgicales favorisent l'adoption généralisée chez les professionnels du travail et les jeunes.

- Cette tendance vers des solutions de contournement du corps plus sûres, plus rapides et cliniquement éprouvées remodele les attentes des consommateurs dans les traitements esthétiques. Par conséquent, les entreprises se concentrent sur la portabilité des appareils, l'amélioration des systèmes de distribution d'énergie et l'amélioration des caractéristiques de confort des patients pour renforcer leur présence sur le marché.

- La demande de dispositifs d'amincissement perfectionnés augmente rapidement dans les cliniques esthétiques, les centres de dermatologie et les spas médicaux, les consommateurs privilégiant de plus en plus les procédures d'amélioration cosmétique minimalement invasives

Dynamique du marché des dispositifs d'escalade Asie-Pacifique

Chauffeur

Augmentation des taux d'obésité et augmentation de la demande de procédures esthétiques

- La prévalence croissante de l'obésité et de la prise de poids liée au mode de vie, associée à une prise de conscience accrue des procédures esthétiques de contour du corps, est un facteur important pour la demande accrue de dispositifs minceur dans toute l'Europe

- Par exemple, en mai 2024, les données publiées par l'Organisation mondiale de la santé (OMS) Asie-Pacifique indiquent que près de 60 % des adultes de la région européenne sont en surpoids ou obèses, ce qui entraîne une augmentation de la demande de technologies de réduction des graisses non invasives en milieu clinique. Ces préoccupations croissantes en matière de santé et de cosmétiques devraient stimuler la croissance de l'industrie des dispositifs de réduction au cours de la période de prévision.

- Comme les individus deviennent plus conscients de l'apparence physique et du bien-être, les traitements non chirurgicaux de contour du corps apparaissent comme des alternatives préférées aux procédures traditionnelles de liposuccion

- De plus, l'augmentation du revenu disponible et l'influence croissante des tendances des médias sociaux favorisant l'esthétique corporelle encouragent les consommateurs à rechercher des traitements amaigrissants professionnels

- La commodité des procédures ambulatoires, la réduction du temps de récupération et les résultats visibles sur une courte durée sont des facteurs clés qui propulsent l'adoption de dispositifs minceur dans les cliniques privées et les services esthétiques hospitaliers. L'expansion de centres esthétiques spécialisés et la disponibilité d'options de financement flexibles contribuent davantage à la croissance du marché.

Restriction/Défi

Coûts de traitement élevés et exigences réglementaires en matière de conformité

- Le coût relativement élevé des traitements d'amincissement perfectionnés, ainsi que les exigences réglementaires rigoureuses pour les appareils d'esthétique médicale, posent un défi important à une plus grande pénétration du marché. Étant donné que ces dispositifs font appel à des technologies basées sur l'énergie, ils nécessitent une validation et une certification cliniques strictes, ce qui augmente les coûts opérationnels des fabricants et des fournisseurs.

- Par exemple, en vertu du règlement de l'Union européenne sur les dispositifs médicaux (RDM) mis en œuvre en 2021, les fabricants de dispositifs esthétiques à base d'énergie doivent satisfaire à des exigences accrues en matière de sécurité et de preuves cliniques, ce qui entraîne des délais d'approbation et des dépenses de certification accrus.

- En outre, le coût par séance de traitement peut être relativement élevé pour les patients, limitant l'accès parmi les consommateurs sensibles aux prix et limitant les procédures répétées

- La nécessité pour des professionnels formés d'utiliser des technologies d'amincissement de pointe ajoute aux coûts d'exploitation des cliniques, ce qui influe sur les structures de tarification des services

- Bien que la sensibilisation et la demande soient en hausse, la perception de prix élevés et la couverture limitée des remboursements pour les procédures cosmétiques peuvent encore entraver l'adoption généralisée

- Surmonter ces défis par la mise au point d'appareils rentables, l'élargissement des programmes de formation des praticiens et l'amélioration de l'éducation des consommateurs sur la sécurité et l'efficacité des traitements seront essentiels pour soutenir la croissance à long terme du marché.

Étendue du marché des dispositifs d'escalade Asie-Pacifique

Le marché est segmenté en fonction du produit, de la technologie, de la portabilité, de la surface corporelle, de l'utilisateur final et du canal de distribution.

- Par produit

Sur la base du produit, le marché des dispositifs de réduction est segmenté en type d'impulsion électrique, type de vibration, extrusion pneumatique, et autres. Le segment des impulsions électriques a dominé la plus grande part du marché de 38,6 % en 2025, en raison de son adoption croissante pour la stimulation musculaire et les traitements de réduction des graisses dans les milieux professionnels et à domicile. Ces dispositifs sont largement préférés en raison de leur nature non invasive et de leur capacité à améliorer la tonification musculaire ainsi que le métabolisme des graisses. Une prise de conscience croissante des consommateurs quant au contournage du corps et à la demande croissante de solutions esthétiques pratiques renforce la croissance du segment. Les dispositifs à impulsion électrique sont également soutenus par des progrès technologiques qui améliorent la sécurité et l'efficacité du traitement. Leur accessibilité économique par rapport aux interventions chirurgicales les rend accessibles à une population plus large. L'accroissement des partenariats entre les fabricants d'appareils et les cliniques de bien-être accroît encore la disponibilité. De plus, l'intégration avec les fonctions de surveillance numérique améliore l'engagement des utilisateurs. La forte commercialisation des solutions basées sur le SME et les tendances de la condition physique contribuent également à la domination. Le segment bénéficie de l'innovation continue et des mises à niveau de produits, assurant un leadership soutenu en 2025.

Le segment de type vibration devrait connaître le taux de croissance le plus rapide de 22,4% CAGR de 2026 à 2033, alimenté par l'augmentation de la préférence des consommateurs pour les équipements d'amincissement portables et faciles à utiliser. Les appareils de vibration sont de plus en plus adoptés dans les routines de fitness à domicile en raison de leur coût abordable et leur conception compacte. La sensibilisation croissante au drainage lymphatique et aux traitements de réduction de la cellulite favorise l'expansion du segment. La montée en puissance des influenceurs de fitness des médias sociaux qui promeuvent les outils de sculpture corporelle basés sur les vibrations accélère la demande. Ces appareils nécessitent une supervision technique minimale, ce qui les rend attrayants pour un usage personnel. Les fabricants se concentrent sur les conceptions ergonomiques et les réglages d'intensité multiples pour améliorer l'attrait client. L'expansion des plateformes de commerce électronique contribue également à l'accessibilité et à la visibilité. L'augmentation du revenu disponible et de l'intérêt pour les soins de santé préventifs stimulent encore la croissance. Comme les consommateurs recherchent des méthodes non chirurgicales de réduction des graisses, les appareils de type vibration sont positionnés pour une adoption rapide sur les marchés émergents.

- Par technologie

Sur la base de la technologie, le marché des dispositifs de réduction est segmenté en cryolipolyse, thérapie laser de faible niveau, échographie ciblée et radiofréquence. Le segment de la cryolipolyse détenait la plus grande part du marché en 2025, soit 41,3 %, en raison de son efficacité avérée dans la réduction ciblée des graisses sans chirurgie. Cette technologie est largement adoptée dans les cliniques de dermatologie et esthétique en raison de résultats cliniquement validés. L'augmentation de la demande de procédures non invasives de contour du corps appuie la domination. Les dispositifs de cryolipolyse offrent un temps d'arrêt minimal qui attire les professionnels. L'amélioration continue de la conception des applicateurs de refroidissement améliore la précision du traitement. La croissance du tourisme médical pour les procédures esthétiques renforce également le segment. Les taux élevés de satisfaction des patients et les traitements répétés entraînent davantage de revenus. De fortes approbations réglementaires et la reconnaissance de la marque parmi les principaux fabricants soutiennent la croissance. La technologie est capable de traiter efficacement les poches obstinées de graisse assure sa position de leader en 2025.

Le segment des radiofréquences devrait connaître le TCAC le plus rapide de 23,1% entre 2026 et 2033, en raison de ses deux avantages de la réduction des graisses et du resserrement de la peau. La demande croissante des consommateurs pour des traitements combinés qui s'attaquent au rétrécissement de la peau et aux contours entraîne une adoption rapide. Les appareils radiofréquences gagnent en popularité dans les centres de bien-être et les cliniques cosmétiques pour leur polyvalence. Les progrès technologiques permettant une distribution contrôlée de la chaleur améliorent les profils de sécurité. La sensibilisation aux traitements anti-âge accélère encore la croissance. Les fabricants introduisent des appareils RF portables pour usage domestique, élargissant la clientèle. Les investissements croissants dans les infrastructures esthétiques dans les pays en développement appuient l'expansion. L'acceptation sociale des procédés cosmétiques encourage également l'adoption. À mesure que la demande de traitements non invasifs augmente, la technologie des radiofréquences devrait croître au rythme le plus rapide au cours de la période de prévision.

- Par transférabilité

Sur la base de la portabilité, le marché des dispositifs de limage est segmenté en autonome et portable. Le segment autonome a représenté la plus grande part du marché en 2025, soit 57,8 %, en raison de son utilisation généralisée dans les cliniques professionnelles et les centres de bien-être. Les systèmes autonomes offrent généralement une puissance de sortie supérieure et des fonctionnalités avancées, offrant des résultats plus efficaces. Ces dispositifs sont préférés pour les procédures de niveau clinique nécessitant précision et performance constante. Une capacité d'investissement élevée des cliniques esthétiques favorise l'acquisition de systèmes avancés. Le nombre croissant de centres d'amincissement professionnels contribue globalement à la domination du segment. Les appareils autonomes intègrent souvent plusieurs technologies dans une seule unité, ce qui améliore la polyvalence. Un soutien solide des fabricants au service après-vente favorise l'adoption. L'accroissement de la confiance des patients dans les traitements à base de cliniques maintient une part de marché. Le segment continue de diriger en raison des résultats de traitement supérieurs et de la crédibilité professionnelle.

On prévoit que le segment mobile augmentera au TCAC le plus rapide de 24,5 %, de 2026 à 2033, en raison de l'augmentation des tendances du traitement à domicile. Les consommateurs préfèrent de plus en plus les appareils compacts qui offrent souplesse et commodité. L'essor des solutions de bien-être à distance et des pratiques d'autogestion stimule la demande. Les appareils portables sont généralement plus abordables et accessibles par les canaux en ligne. La miniaturisation technologique a amélioré les performances des appareils tout en maintenant la sécurité. Les modes de vie occupés et la demande de traitements efficaces dans le temps soutiennent davantage la croissance. Les fabricants lancent des modèles rechargeables et conviviaux pour attirer les jeunes. La pénétration croissante des marchés émergents accélère l'adoption. À mesure que l'esthétique domestique gagne en popularité, le segment portable devrait s'étendre rapidement pendant la période de prévision.

- Par zone corporelle

Sur la base de la surface du corps, le marché des dispositifs de réduction est segmenté en abdominaux, hanches, cuisses et autres. Le segment abdominal a dominé le marché avec une part de revenus de 46,9 % en 2025, sous l'impulsion d'une forte concentration des consommateurs sur la réduction de la graisse du ventre. La graisse abdominale est généralement associée à des maladies du mode de vie, ce qui incite à la demande de traitements ciblés. Les préoccupations esthétiques et les tendances de fitness mettant l'accent sur la tonification de base renforcent encore la domination. Les cliniques offrent souvent des forfaits de contournement abdominal, supportant les revenus du segment. La prévalence croissante de l'obésité alimente la demande mondiale. Les progrès technologiques permettant un ciblage précis de la graisse abdominale améliorent l'efficacité. Les campagnes de marketing soulignant les résultats abdominaux visibles stimulent également l'absorption. Répéter les procédures pour la graisse du ventre obstinée contribue à la stabilité des revenus. Le segment demeure dominant en raison de la forte demande de traitement et des résultats prouvés.

Le segment des cuisses devrait connaître le TCAC le plus rapide de 21,9 % entre 2026 et 2033, en raison de la demande croissante de contours inférieurs. Les consommateurs cherchent de plus en plus des solutions pour la réduction de la cellulite et la tonification des cuisses. La popularité croissante de la sculpture corporelle chez les plus jeunes favorise l'expansion. Fitness et tendances de mode mettant l'accent sur l'esthétique corporelle inférieure stimulent l'intérêt. Les progrès dans les modèles d'applicateurs adaptés aux zones de cuisse améliorent la précision du traitement. Les centres de bien-être encouragent les traitements à base de paquets, y compris le contour des cuisses. La hausse des revenus disponibles dans les populations urbaines stimule encore la croissance. Une sensibilisation accrue aux options non envahissantes encourage l'adoption. À mesure que la demande de remodelage complet du corps augmente, les traitements axés sur les cuisses devraient croître rapidement.

- Par Utilisateur final

Sur la base de l'utilisateur final, le marché des appareils de slimming est segmenté en gymnases et centres de fitness, centres de bien-être, maison, et autres. Le segment des centres de bien-être détenait la plus grande part du marché de 39,4% en 2025, grâce à l'expertise professionnelle et à la disponibilité d'équipements avancés. Les consommateurs préfèrent souvent des procédures supervisées pour la sécurité et de meilleurs résultats. Les centres de bien-être offrent des programmes d'amincissement intégrés combinant des appareils et des conseils alimentaires. De plus en plus de cliniques esthétiques soutiennent la domination mondiale. Une grande confiance des consommateurs envers les praticiens certifiés entraîne davantage de revenus. Les améliorations technologiques dans les cliniques améliorent l'efficacité du traitement. L'urbanisation croissante et les changements de mode de vie favorisent la demande de solutions structurées d'atténuation. Le segment continue de jouer un rôle de premier plan en raison de sa crédibilité professionnelle et de ses services complets.

Le segment résidentiel devrait enregistrer le TCAC le plus rapide de 25,2 % entre 2026 et 2033, alimenté par une demande croissante de traitements pratiques et rentables. Les consommateurs préfèrent la protection de la vie privée et la souplesse associées aux appareils à domicile. La pénétration croissante du commerce électronique améliore l'accessibilité des produits. Le marketing des médias sociaux et l'appui des influenceurs accélèrent l'adoption. Les innovations technologiques ont amélioré les caractéristiques de sécurité des appareils domestiques. Les modes de vie occupés entraînent la demande de solutions d'économie de temps. Une prise de conscience accrue des tendances de l'autosoin favorise la croissance. Les stratégies de prix abordables des fabricants attirent une clientèle plus large. Au fur et à mesure que le bien-être personnalisé devient courant, le segment à domicile devrait s'étendre au taux de croissance le plus élevé.

- Par canal de distribution

Sur la base du canal de distribution, le marché des dispositifs de réduction des émissions est segmenté en appels d'offres directs et au-dessus du marché de détail. Le segment des appels d'offres directs a représenté la plus grande part du marché en 2025, soit 52,6 %, grâce à l'approvisionnement en gros des hôpitaux, des cliniques et des centres de bien-être. Les achats institutionnels assurent des revenus réguliers pour les fabricants. Les contrats à grande échelle comprennent souvent des contrats de maintenance et de service. Les investissements croissants dans les infrastructures esthétiques soutiennent la domination. L'approvisionnement direct assure l'accès aux appareils de qualité clinique avancés. Les fabricants bénéficient de partenariats à long terme avec les fournisseurs de soins de santé. La hausse de la demande de services d'amincissement professionnels renforce encore la part de segment. Le processus d'approvisionnement structuré renforce la présence du marché.

Le segment des ventes au détail devrait connaître le TCAC le plus rapide de 23,8 % entre 2026 et 2033, en raison de l'augmentation de l'inclination des consommateurs à l'égard des dispositifs d'amincissement à usage domestique. L'expansion des pharmacies de détail et des plateformes en ligne améliore l'accessibilité. Des prix concurrentiels et des offres promotionnelles attirent des acheteurs individuels. La sensibilisation accrue à la réduction des graisses non envahissantes soutient la demande au détail. Les fabricants se concentrent sur des campagnes d'emballage et de marketing attrayantes. L'augmentation des paiements numériques et des services de livraison à domicile stimule la croissance. Les consommateurs préfèrent de plus en plus les solutions autogérées. À mesure que l'esthétique à domicile continuera d'augmenter, le canal de distribution au détail devrait croître à un rythme significatif au cours de la période de prévision.

Analyse régionale du marché des dispositifs d'escalade Asie-Pacifique

- Le marché des appareils amaigrissants de l'Asie-Pacifique devrait s'étendre à un TCAC important tout au long de la période de prévision, principalement en raison de la prévalence croissante de l'obésité, de la sensibilisation accrue aux procédures esthétiques de contournage du corps et de la préférence croissante pour les traitements non invasifs de réduction des graisses

- L'augmentation de l'urbanisation, l'évolution des modes de vie et l'augmentation des niveaux de revenu disponible favorisent l'adoption de technologies d'atténuation avancées dans toute la région. Les consommateurs sont de plus en plus attirés par des solutions cosmétiques peu invasives qui offrent des temps d'arrêt réduits et des résultats visibles sans intervention chirurgicale

- La région connaît une croissance importante dans les cliniques esthétiques, les centres de dermatologie et les spas médicaux, avec des dispositifs d'amincissement qui sont intégrés à la fois dans des établissements cosmétiques spécialisés et dans des services esthétiques hospitaliers. Les progrès technologiques continus dans les systèmes laser, cryolipolyse, échographie et radiofréquence renforcent encore l'expansion du marché

China Slimming Devices Market Insight

Le marché chinois des appareils amaigrissants a dominé le marché des appareils amaigrissants avec la plus grande part de revenus de 32,6 % en 2025, sous l'effet de la sensibilisation accrue aux procédures cosmétiques non invasives, de la croissance rapide des cliniques esthétiques, de l'augmentation des revenus disponibles et de l'adoption généralisée de systèmes perfectionnés de contournage du corps à base de laser et d'énergie. Les initiatives gouvernementales visant à promouvoir les secteurs de la beauté et du bien-être, ainsi que la forte fabrication nationale d'appareils minceurs, renforcent encore la position de leader de la Chine sur le marché. L'expansion du réseau de cliniques esthétiques et de centres de dermatologie, couplée à la croissance du tourisme médical, renforce l'adoption soutenue.

India Slimming Devices Market Insight

Le marché indien des dispositifs d'amincissement devrait être la région qui connaîtra la croissance la plus rapide sur le marché des dispositifs d'amincissement au cours de la période de prévision, avec un TCAC de 11,3 %, passant de 2026 à 2033, alimenté par l'intérêt croissant des consommateurs pour les traitements cosmétiques non invasifs, l'augmentation du revenu disponible, l'expansion du tourisme médical et l'accessibilité accrue des technologies d'amincissement modernes dans les zones urbaines et semi-urbaines. La prolifération des cliniques esthétiques, des campagnes de sensibilisation et la disponibilité de dispositifs avancés de réduction des graisses sont à l'origine de l'adoption rapide de procédures de contournage dans tout le pays. Les innovations continues dans les systèmes laser, cryolipolyse et ultrasons soutiennent davantage la croissance du marché.

Quelles sont les meilleures entreprises du marché des appareils de limage en Asie-Pacifique

L'industrie des dispositifs d'escalade est principalement dirigée par des entreprises bien établies, notamment :

- Cynosure, LLC (États-Unis)

- Vénus Concept Ltd. (Canada)

- Cutera, Inc. (États-Unis)

- Alma Lasers (Israël)

- Lumenis Ltd. (Israël)

- BTL Industries (Royaume-Uni)

- Fotona d.o.o. (Slovénie)

- Syneron Candela (États-Unis)

- Sciton, Inc. (États-Unis)

- Allergan Esthétique (États-Unis)

- Solta Medical (États-Unis)

- Hologic, Inc. (États-Unis)

- Société Lutronic (Corée du Sud)

- Zimmer MedizinSysteme GmbH (Allemagne)

- Beijing KES Biology Technology Co., Ltd. (Chine)

Les derniers développements en Asie-Pacifique Marché des dispositifs de limage

- En janvier 2021, Allergan Aesthetics a introduit la procédure CoolSculpting Elite approuvée par la FDA, conçue pour cibler et éliminer les gonflements de graisse visibles dans neuf zones différentes du corps, y compris les cuisses, l'abdomen, les flancs, le dos, les fesses, les bras supérieurs, les régions submentales et submandibulaires. Cette gamme étendue d'applicateurs a amélioré la polyvalence et l'efficacité de la ligne CoolSculpting dans les traitements de réduction des graisses non invasives

- En mars 2023, iCRYO, une marque américaine de santé et de bien-être, s'est associée à BTL Industries pour intégrer des technologies de mise en forme du corps non invasives de pointe, dont Emsculpt NEO, dans ses offres de services. Cette collaboration a élargi les capacités de tonification musculaire, de réduction des graisses et de contour du corps, offrant une gamme plus large de solutions esthétiques innovantes

- En juin 2023, ShanDong EXFU Lasers Technology Co. Ltd., une société chinoise de produits de beauté et de bien-être, a lancé la FIND S EMS Slimming Machine, avec la technologie avancée de stimulation musculaire électrique (EMS) avec des niveaux d'intensité réglables et un design compact et portable pour permettre l'activation musculaire ciblée et la sculpture corporelle améliorée à la maison

- En août 2024, Zimmer MedizinSystems a lancé le dispositif de réduction des ondes de choc acoustiques Z Wave Q, doté d'une pièce à main refroidie à l'eau qui fonctionne avec un bruit considérablement réduit par rapport aux unités précédentes, offrant un confort et une commodité améliorés lors des sessions de contour du corps

- En septembre 2024, Venus Concept a reçu l'autorisation de l'Australie de la Therapeutic Goods Administration (TGA) pour son système Venus Bliss MAX, une solution de façonnage 3-en-1 qui intègre la technologie laser diode pour la réduction des graisses, la technologie (MP)2 pour le serrage de la peau et la stimulation musculaire électrique pour le tonification musculaire

- En décembre 2024, BTL Aesthetics a annoncé le lancement des applicateurs EMSCULPT NEO EDGE, conçus pour cibler plus efficacement l'ensemble de l'abdomen latéral en combinant les énergies électromagnétiques synchronisées (RF) et à haute intensité (HIFEM) pour la réduction simultanée des graisses et le renforcement musculaire

- En février 2025, Cutera a introduit le truSculpt flex+ de nouvelle génération, avec un mode de traitement rapide de 15 minutes capable de traiter jusqu'à huit zones simultanément en utilisant la technologie multidirectionnelle de stimulation (MDS) pour améliorer la tonification musculaire et renforcer les performances

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.