Global Endocrinology Biosimilars Market

Taille du marché en milliards USD

TCAC :

%

USD

297.00 Million

USD

632.10 Million

2025

2033

USD

297.00 Million

USD

632.10 Million

2025

2033

| 2026 –2033 | |

| USD 297.00 Million | |

| USD 632.10 Million | |

| % | |

|

Global Endocrinology Biosimilars Segmentation du marché, par type de produit (Insulin Biosimilars et Growth Hormone Biosimilars), Indication ( Gestion du diabète et déficit en hormones de croissance )- Tendances de l'industrie et prévisions à 2033

Qu'est-ce que l'endocrinologie Biosimilaires Taille du marché et taux de croissance

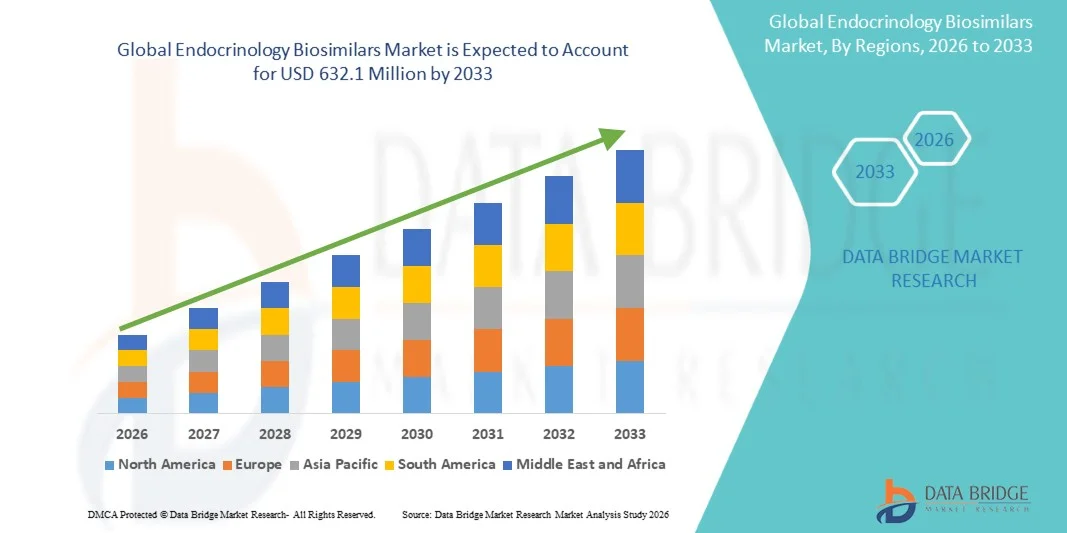

- Selon l'analyse de marché de Data Bridge, la taille du marché des biosimilaires endocrinologiques mondiaux a été évaluée à297 millions de dollars en 2025et devrait atteindre632,1 millions de dollars en 2033, à unTCAC de 9,90 %pendant la période de prévision

- La croissance du marché est largement alimentée par l'augmentation de la prévalence des troubles endocriniens, la demande croissante de thérapies biologiques abordables et les expiries brevetées de plusieurs produits biologiques d'origine, ce qui conduit à une plus grande adoption de biosimilaires dans le diabète, l'hormone de croissance et d'autres traitements endocriniens.

- En outre, une prise de conscience croissante des fournisseurs de soins de santé et des patients, des politiques de remboursement favorables et des réglementations gouvernementales favorables accélèrent l'adoption de solutions biosimilaires endocrinologiques, ce qui stimule considérablement la croissance de l'industrie.

Taille du marché et prévisions

- Valeur marchande mondiale (2025): 297 millions de dollars

- Valeur marchande prévue (2033): 632,1 millions de dollars

- Prévisions CAGR (2026-2033): 9.90%

Endocrinologie Biosimilaires Analyse du marché

- Les biosimilaires endocrinologiques, y compris les traitements du diabète, les carences en hormones de croissance et d'autres troubles endocriniens, sont des composantes de plus en plus vitales des soins de santé modernes en raison de leur rentabilité, de leur efficacité comparable aux produits biologiques d'origine et de leur adoption croissante chez les médecins et les patients.

- La demande croissante de biosimilaires endocrinologiques est principalement alimentée par l'augmentation de la prévalence des troubles endocriniens, les expirations patentes de plusieurs produits biologiques d'origine, la sensibilisation accrue des fournisseurs de soins de santé et les politiques d'appui du gouvernement et du payeur encourageant l'adoption de biosimilaires

- L'Amérique du Nord a dominé le marché des biosimilaires endocrinologiques avec la plus grande part des revenus d'environ 38,6 % en 2025, tirée par une infrastructure de soins de santé solide, des taux d'adoption élevés de biosimilaires, des politiques de remboursement bien établies et une forte présence d'acteurs clés de l'industrie, en particulier aux États-Unis, où l'adoption et la sensibilisation précoces alimentent la croissance du marché

- L'Asie-Pacifique devrait être la région qui connaîtra la croissance la plus rapide du marché des biosimilaires endocrinologiques au cours de la période de prévision, enregistrant un TCAC robuste d'environ 10,2 %, appuyé par l'augmentation de la prévalence des troubles endocriniens, l'augmentation de l'accès aux soins de santé, l'amélioration des politiques de remboursement et l'expansion des capacités de fabrication de produits pharmaceutiques dans des pays comme l'Inde, la Chine et le Japon.

- Le segment de la gestion du diabète a dominé la plus grande part des revenus du marché en 2025, soit 65 %, en raison de la prévalence élevée du diabète de type 1 et de type 2 dans le monde, de l'augmentation de la population gériatrique et de l'augmentation des initiatives gouvernementales visant à améliorer l'accès aux insulinothérapies rentables.

Portée du rapport et biosimilaires endocrinologiques Segmentation du marché

|

Attributs |

Biosimilaires endocrinologiques Principales perspectives du marché |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Principaux acteurs du marché |

|

|

Possibilités de marché |

|

|

Infos sur la valeur ajoutée |

En plus des renseignements sur les scénarios de marché comme la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent également une analyse approfondie des experts, l'épidémiologie des patients, l'analyse des pipelines, l'analyse des prix et le cadre réglementaire. |

Quelle est la tendance clé du marché des biosimilaires endocrinologiques

(en milliers de dollars)Progrès technologiques et thérapeutiques en endocrinologie(en milliers de dollars)

- Une tendance significative et accélérée sur le marché mondial des biosimilaires endocrinologiques est le développement et l'adoption de thérapies biosimilaires de nouvelle génération pour les troubles endocriniens chroniques tels que le diabète, les carences en hormones de croissance et les troubles thyroïdiens. Les innovations dans les techniques de fabrication, la stabilité de la formulation et les approbations réglementaires améliorent l'accessibilité et l'accessibilité, rendant ces traitements de plus en plus attrayants pour les fournisseurs de soins de santé et les patients.

- Par exemple, des sociétés pharmaceutiques comme Sandoz et Biocon ont activement développé des versions biosimilaires d'analogues d'insuline établis et d'hormones de croissance recombinantes avec une stabilité améliorée et des caractéristiques de conformité des patients. Ces progrès facilitent une adoption plus large sur les marchés développés et émergents, en particulier en Amérique du Nord, en Europe et en Asie-Pacifique, où la demande de thérapies endocriniennes rentables augmente

- Les progrès de la technologie de formulation, y compris les analogues d'insuline à longue durée d'action et les dispositifs d'injection prêts à l'emploi, permettent d'améliorer la précision du dosage, la fréquence d'administration et l'adhésion des patients. Par exemple, plusieurs produits d'insuline biosimilaire récents offrent maintenant des systèmes d'administration à base de stylos qui simplifient l'administration à domicile et réduisent l'anxiété liée à l'injection chez les patients, en particulier dans les populations pédiatriques et gériatriques.

- L'intégration croissante des programmes de pharmacovigilance et de surveillance post-commercialisation améliore la surveillance de l'innocuité des biosimilaires endocrinologiques, ce qui fournit aux cliniciens des données réelles sur l'efficacité et les événements indésirables. Cela facilite la prise de décisions éclairées en matière de traitement, favorise la confiance parmi les professionnels de la santé et encourage l'adoption plus large de thérapies biosimilaires

- Ces développements transforment les paradigmes de traitement en endocrinologie en offrant des solutions de rechange abordables, efficaces et cliniquement comparables aux produits biologiques d'origine, en élargissant finalement l'accès à des thérapies vitales pour une population de patients plus importante sur les marchés mondiaux.

- La demande de biosimilaires endocrinologiques continue d'augmenter, en raison de la prévalence croissante des troubles endocriniens chroniques, de l'augmentation des dépenses de soins de santé et des politiques gouvernementales d'appui visant à réduire les coûts de traitement et à améliorer l'accès des patients

Endocrinologie Biosimilaires Dynamique du marché

Chauffeur

Incidence croissante des troubles endocriniens et de la croissance du groupe de patients

- L'augmentation mondiale du diabète, de la carence en hormones de croissance et des troubles liés à la thyroïde est à l'origine de la demande d'options de traitement rentables, faisant de biosimilaires endocrinologiques une solution de rechange préférée aux produits biologiques d'origine coûteux.

- Par exemple, la Fédération internationale du diabète (FDI) a signalé une augmentation significative de la prévalence du diabète de type 2, en particulier en Asie-Pacifique et en Amérique du Nord, encourageant les systèmes de santé à adopter des insulines biosimilaires pour améliorer l'accessibilité et la couverture des patients.

- De plus, le vieillissement de la population et l'augmentation des taux d'obésité contribuent à la création d'un plus grand bassin de patients nécessitant des interventions endocriniennes, ce qui favorise la croissance du marché.

- En outre, l'introduction de dispositifs d'administration adaptés aux patients, tels que stylos préremplis, auto-injecteurs et pompes à insuline portables compatibles avec les biosimilaires, augmente l'adhésion et la satisfaction au traitement, en particulier chez les patients pédiatriques, adolescents et gériatriques.

- Les initiatives de soins de santé et les politiques d'assurance qui favorisent des solutions de rechange biologiques rentables encouragent également les médecins et les hôpitaux à intégrer les biosimilaires dans les protocoles de traitement standard, ce qui favorise la pénétration du marché.

Restriction/Défi

(en milliers de dollars)Complexité réglementaire et coûts de développement élevés(en milliers de dollars)

- Les exigences réglementaires relativement complexes et rigoureuses pour l'approbation des biosimilaires endocrinologiques posent un défi important à l'entrée sur le marché. Les fabricants doivent démontrer une biosimilarité en termes d'efficacité, d'innocuité et d'immunogénicité par rapport aux produits biologiques de référence, ce qui nécessite des essais cliniques approfondis et de la documentation

- Par exemple, les voies d'approbation biosimilaires établies par la FDA américaine et l'EMA exigent des études cliniques pharmacocinétiques, pharmacodynamiques et comparatives rigoureuses, ce qui entraîne des coûts de développement élevés et des délais plus longs pour la commercialisation de nouveaux produits.

- De plus, l'hésitation des médecins et les inquiétudes des patients au sujet de l'interchangeabilité et de la sécurité à long terme des biosimilaires peuvent limiter l'adoption, en particulier sur les marchés où les produits biologiques d'origine ont établi la confiance

- Le coût élevé de production de certaines molécules biosimilaires, combiné à des défis dans la logistique, le stockage et la distribution de la chaîne du froid, peut limiter la disponibilité dans les économies émergentes, ralentissant la pénétration du marché.

- Surmonter ces défis grâce à l'harmonisation réglementaire, à des programmes de sensibilisation améliorés, à des techniques de fabrication rentables et à des partenariats de collaboration entre les fabricants innovateurs et les fabricants de produits biosimilaires sera essentiel à une croissance soutenue du marché dans le secteur des biosimilaires endocrinologiques

Endocrinologie Biosimilaires Portée du marché

Le marché est segmenté en fonction du type de produit et de l'indication.

• Par type de produit

Sur la base du type de produit, le marché des biosimilaires endocrinologiques est segmenté en biosimilaires à l'insuline et en biosimilaires à l'hormone de croissance. Le segment des biosimilaires d'insuline a dominé la plus grande part du marché de 61 % en 2025, en raison de la prévalence croissante du diabète à l'échelle mondiale, de l'adoption accrue d'insulinothérapies rentables et du soutien au remboursement dans les pays développés et les pays émergents. Le segment bénéficie d'une solide acceptation clinique, de pipelines de fabrication étendus et de la connaissance des régimes d'insuline par les patients. Les gouvernements et les payeurs de soins de santé encouragent l'adoption de produits biosimilaires pour réduire les coûts de traitement, tandis que les hôpitaux et les cliniques favorisent les biosimilaires d'insuline en raison de la facilité de stockage et d'administration. L'innovation en cours dans les formulations d'insuline à action prolongée et rapide renforce encore le leadership du marché, en particulier en Amérique du Nord et en Europe.

Le segment des biosimilaires de l'hormone de croissance devrait connaître le TCAC le plus rapide de 14,3 % entre 2026 et 2033, alimenté par la sensibilisation accrue aux traitements de la carence en hormones de croissance (GHD) chez les enfants et les adultes, l'augmentation des taux de diagnostic et l'amélioration de l'accès par les programmes de soins de santé publics et privés. Les entreprises pharmaceutiques lancent des biosimilaires de nouvelle génération avec une efficacité accrue, des profils d'innocuité et des dispositifs de livraison, ce qui accélère l'adoption. L'expansion des centres d'endocrinologie pédiatrique et l'administration à domicile d'hormones de croissance contribuent également à la croissance rapide du marché mondial. Les marchés émergents en Asie-Pacifique et en Amérique latine devraient être à l'origine d'une part importante de ce TCAC.

• Par indication

Sur la base de l'indication, le marché des biosimilaires endocrinologiques est segmenté en déficit en gestion du diabète et en hormones de croissance. Le segment de la gestion du diabète a dominé la plus grande part des revenus du marché en 2025, soit 65 %, en raison de la forte prévalence du diabète de type 1 et de type 2 dans le monde, de l'augmentation des populations de gériatrie et de l'augmentation des initiatives gouvernementales visant à améliorer l'accès aux insulinothérapies rentables. Ce segment comprend à la fois des biosimilaires d'insuline à action longue et rapide largement utilisés dans les hôpitaux, les cliniques et les soins à domicile, avec des politiques de remboursement favorables à l'adoption. La nécessité d'un contrôle glycémique fréquent et une prise de conscience croissante des complications du diabète soutiennent une forte demande mondiale de biosimilaires d'insuline.

Le segment de déficit en hormones de croissance devrait connaître le TCAC le plus rapide de 13,8 % entre 2026 et 2033, en raison de l'augmentation du diagnostic de DHD, de l'adoption plus large de thérapies biosimilaires et des progrès technologiques dans les systèmes de distribution de médicaments tels que les stylos préremplis et les auto-injecteurs. Les cliniques d'endocrinologie pédiatrique et adulte se développent à l'échelle mondiale, offrant un meilleur accès aux traitements. Le lancement de biosimilaires rentables par rapport aux hormones de croissance de l'initiateur favorise davantage l'adoption dans les économies émergentes. En outre, les campagnes de sensibilisation et les améliorations apportées à la couverture de l ' assurance maladie accélèrent l ' expansion du marché.

Endocrinologie Biosimilaires Marché Analyse régionale

- L'Amérique du Nord a dominé le marché des biosimilaires endocrinologiques avec la plus grande part des revenus d'environ 38,6 % en 2025.

- Poussés par une infrastructure de soins de santé solide, des taux d'adoption élevés de biosimilaires, des politiques de remboursement bien établies et une forte présence d'acteurs clés de l'industrie, en particulier aux États-Unis, où l'adoption précoce et la sensibilisation alimentent la croissance du marché

- Le marché est témoin d'une absorption importante de biosimilaires dans les thérapies endocrinologiques telles que le diabète, les carences en hormones de croissance et les troubles de la thyroïde, appuyée par une acceptation clinique solide et une sensibilisation accrue des patients

Endocrinologie américaine Biosimilaires Aperçu du marché

Le marché américain des biosimilaires endocrinologiques a capté la majorité des revenus de l'Amérique du Nord, alimentés par l'adoption rapide de biosimilaires dans les hôpitaux et les cliniques externes. Des facteurs tels que l'éducation proactive des médecins, des campagnes de sensibilisation des patients et des politiques de remboursement favorables stimulent la croissance dans les segments du diabète, de l'hormone de croissance et de la thyroïde.

Europe Endocrinologie Biosimilaires Aperçu du marché

Le marché européen des biosimilaires endocrinologiques devrait s'étendre à un TCAC important au cours de la période de prévision, en raison de l'adoption croissante de biosimilaires dans les thérapies endocriniennes, de la réglementation gouvernementale favorable et de l'augmentation des dépenses de santé. Des pays comme l'Allemagne, le Royaume-Uni et la France connaissent une croissance en raison d'infrastructures de soins de santé bien établies et de la présence de grands fabricants biosimilaires.

Royaume-Uni Endocrinologie Biosimilaires Aperçu du marché

Le marché des biosimilaires endocrinologiques au Royaume-Uni devrait croître régulièrement au cours de la période de prévision, grâce à des cadres de remboursement favorables, à une sensibilisation accrue des médecins et à des initiatives gouvernementales favorisant des thérapies rentables. L'augmentation de la prévalence des troubles endocriniens et l'adoption croissante de biosimilaires dans les hôpitaux et les cliniques sont à l'origine de l'expansion du marché.

Allemagne Endocrinologie Biosimilaires Aperçu du marché

Le marché allemand des biosimilaires endocrinologiques devrait croître à un rythme considérable au cours de la période de prévision, alimenté par l'adoption croissante de biosimilaires, de systèmes de santé bien développés et d'initiatives visant à réduire les coûts de traitement. Les campagnes de sensibilisation et les collaborations entre les fournisseurs de soins de santé et les sociétés pharmaceutiques soutiennent davantage la pénétration du marché.

Endocrinologie Asie-Pacifique Biosimilaires Aperçu du marché

Le marché des biosimilaires endocrinologiques en Asie et dans le Pacifique devrait être la région ayant connu la croissance la plus rapide sur le marché des biosimilaires endocrinologiques au cours de la période de prévision, enregistrant un TCAC robuste d'environ 10,2 %, appuyé par l'augmentation de la prévalence des troubles endocriniens, l'augmentation de l'accès aux soins de santé, l'amélioration des politiques de remboursement et l'expansion des capacités nationales de fabrication de produits pharmaceutiques dans des pays comme l'Inde, la Chine et le Japon. La croissance rapide de l'infrastructure hospitalière et la sensibilisation aux biosimilaires chez les médecins et les patients sont également des facteurs clés de la demande régionale.

Japon Endocrinologie Biosimilaires Aperçu du marché

Le marché japonais des biosimilaires endocrinologiques gagne en traction en raison de l'adoption croissante de biosimilaires pour le diabète, les carences en hormones de croissance et les troubles thyroïdiens. Les politiques de soins de santé de soutien, la sensibilisation élevée des patients et les progrès technologiques dans la fabrication pharmaceutique alimentent la croissance du marché.

Chine Endocrinologie Biosimilaires Aperçu du marché

Le marché chinois des biosimilaires endocrinologiques a représenté la plus grande part des revenus en Asie-Pacifique en 2025, en raison de l'expansion de l'infrastructure de soins de santé, de l'augmentation de la prévalence des troubles endocriniens, de l'accent accru mis par le gouvernement sur les traitements rentables et de la forte capacité de fabrication de produits pharmaceutiques au pays. La Chine est de plus en plus consciente des biosimilaires et de l'augmentation des approbations pour les thérapies endocrinologiques sont les principaux facteurs propulsant le marché.

Quelle région détient la plus grande part de la Endocrinologie Biosimilaires Marché

L'industrie des biosimilaires endocrinologiques est principalement dirigée par des entreprises bien établies, notamment :

- Biocon (Inde)

- Pfizer (États-Unis)

- Amgen (États-Unis)

- Samsung Bioepis (Corée du Sud)

- Celltrion Healthcare (Corée du Sud)

- Teva Pharmaceuticals (Israël)

- Stada Arzneimittel (Allemagne)

- Fresenius Kabi (Allemagne)

- Hétero Biopharma (Inde)

- Laboratoires de Reddy (Inde)

- Coherus BioSciences (États-Unis)

- Glenmark Pharmaceuticals (Inde)

- Novartis (Suisse)

- Merck & Co. (États-Unis)

- AbbVie (États-Unis)

- Biopharma de Genor (Chine)

- Hansoh Pharmaceutical (Chine)

Derniers développements du marché mondial des biosimilaires endocrinologiques

- En juillet 2021, la Food and Drug Administration (FDA) des États-Unis a approuvé Semglee (insuline glargine-vfgn) comme biosimilaire interchangeable au produit d'insuline de référence Lantus, marquant l'un des premiers biosimilaires interchangeables d'insuline aux États-Unis. Cette approbation a considérablement élargi les options de traitement abordables pour la prise en charge du diabète et a créé un précédent pour les futurs biosimilaires interchangeables endocrinologiques, encourageant l'adoption plus large et la concurrence dans l'insulinothérapie

- En avril 2023, Eli Lilly and Company lance Rezvoglar (insuline glargine-aglr), son deuxième biosimilaire interchangeable d'insuline glargine aux États-Unis, renforçant encore la concurrence dans le segment de l'insuline basale. L'entrée sur le marché de Rezvoglar a fourni une option accessible supplémentaire pour l'insulinothérapie à longue durée d'action, aidant à éliminer les obstacles aux coûts et à l'accès pour les patients diabétiques

- En septembre 2024, Sandoz a annoncé le lancement d'un nouveau biosimilaire de l'insuline glargine dans certains pays d'Europe de l'Est, visant à renforcer son empreinte biosimilaire endocrinologique sur les marchés régionaux. En ciblant ces marchés émergents, Sandoz a élargi l'accès aux insulinothérapies rentables et contribué à une plus grande disponibilité biosimilaire au-delà des marchés occidentaux traditionnels.

- En novembre 2024, Biocon Biologics a reçu une autorisation réglementaire pour étendre son offre biosimilaire d'insuline à de multiples marchés européens à la suite d'audits de fabrication réussis, renforçant son rôle mondial dans les biosimilaires endocrinologiques et permettant un accès plus large aux analogues d'insuline de haute qualité en Europe.

- En février 2025, la FDA des États-Unis a approuvé Merilog (insuline-aspart-szjj) en tant que biosimilaire à Novolog (insuline-asparte), le premier produit biosimilaire d'insuline à action rapide approuvé aux États-Unis. Cette approbation a élargi les options de traitement pour les patients diabétiques adultes et pédiatriques en introduisant la concurrence dans le segment de l'insuline à action rapide, en répondant aux besoins clés non satisfaits dans le contrôle du glucose au repas

- En juillet 2025, la FDA a accordé l'approbation de Kirsty (Insulin Aspart‐xjhz) comme premier et seul biosimilaire interchangeable à NovoLog (insulin aspart) aux États-Unis. Cette étape a renforcé l'offre d'insuline biosimilaire en permettant une substitution automatique au niveau de la pharmacie, en améliorant l'accès des patients et en réduisant potentiellement les coûts de traitement.

- En mai 2025, Novo Nordisk a annoncé un partenariat de production avec Fujifilm Diosynth Biotechnologies pour développer la fabrication de biosimilaires d'insuline asparte ciblant la demande asiatique et européenne, soulignant les efforts stratégiques de l'industrie pour répondre aux besoins mondiaux de thérapies contre le diabète à un coût abordable grâce à une capacité de production accrue et à une portée géographique accrue.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.