Global Fiberglass Tanks Market

Taille du marché en milliards USD

TCAC :

%

USD

2.26 Billion

USD

3.94 Billion

2025

2033

USD

2.26 Billion

USD

3.94 Billion

2025

2033

| 2026 –2033 | |

| USD 2.26 Billion | |

| USD 3.94 Billion | |

| % | |

|

Global Fiberglass Tanks Market Segmentation, By Type (E-Glass, A-Glass, S-Glass, AR-Glass, C-Glass, R-Glass, and Others), Resin Type (Polyester, Vinyl Ester, and Others), Usage (Water, Oil and Gas, Chemicals, and Wastewater), Sales and Service (Tank Sales and Service), Application (Composite and Insulation), End Users (Commercial, Residential, Municipal, and Industrial) - Industry Trends and Forecast to 2033

Fiberglass Tanks Market Size

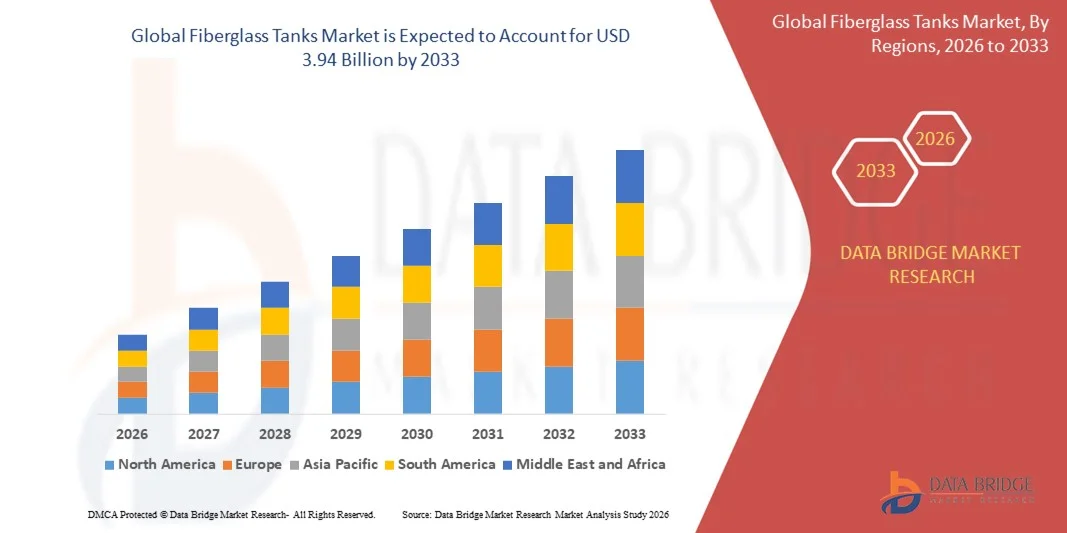

- The global fiberglass tanks market size was valued at USD 2.26 billion in 2025 and is expected to reach USD 3.94 billion by 2033, at a CAGR of 7.2% during the forecast period

- The market growth is largely driven by the increasing adoption of corrosion-resistant and long-lasting storage solutions across water, wastewater, chemical, and industrial applications, as fiberglass tanks offer superior durability compared to traditional metal alternatives

- Furthermore, rising investments in municipal infrastructure, industrial expansion, and stricter environmental regulations related to leakage prevention and material safety are accelerating the shift toward fiberglass tanks, thereby supporting sustained market growth

Fiberglass Tanks Market Analysis

- Fiberglass tanks, designed for the storage of water, chemicals, oil and gas, and wastewater, are becoming essential components of modern storage infrastructure due to their high strength-to-weight ratio, resistance to corrosion, and low maintenance requirements across diverse end-use sectors

- The growing demand for fiberglass tanks is primarily fueled by rapid urbanization, increasing industrial activity, and the need for cost-effective, long-life storage systems that comply with environmental and safety standards in municipal, commercial, and industrial settings

- North America dominated the fiberglass tanks market with a share of over 45% in 2025, due to strong investments in water infrastructure, replacement of aging metal tanks, and rising adoption of corrosion-resistant storage solutions

- Asia-Pacific is expected to be the fastest growing region in the fiberglass tanks market during the forecast period due to rapid urbanization, expanding industrialization, and increasing investments in water and wastewater infrastructure

- E-Glass segment dominated the market with a market share of 42.6% in 2025, due to its cost-effectiveness, strong mechanical strength, and wide availability across regions. E-Glass fibers are extensively used in tank manufacturing due to their excellent corrosion resistance and suitability for large-scale water and chemical storage applications. Manufacturers prefer E-Glass as it balances performance and affordability, supporting high-volume production across municipal and industrial projects

Report Scope and Fiberglass Tanks Market Segmentation

|

Attributes |

Fiberglass Tanks Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Fiberglass Tanks Market Trends

Growing Adoption of Corrosion-Resistant and Lightweight Storage Solutions

- A major trend in the fiberglass tanks market is the growing adoption of corrosion-resistant and lightweight storage solutions across water treatment, chemical processing, and industrial storage applications, driven by the need for longer service life and reduced maintenance requirements. Fiberglass tanks offer superior resistance to chemicals, moisture, and harsh environmental conditions, making them suitable for both above-ground and underground installations

- For instance, Owens Corning supplies high-performance fiberglass reinforcements that are widely used in the manufacturing of durable storage tanks for water and industrial fluids. These materials enhance structural integrity while maintaining low weight, supporting easier transportation and installation

- Industries managing aggressive or corrosive substances are increasingly replacing traditional steel tanks with fiberglass alternatives to minimize corrosion-related failures. This shift is strengthening the role of fiberglass tanks in chemical storage and wastewater management where material durability is critical

- The lightweight nature of fiberglass tanks is supporting faster installation and reduced foundation requirements, which is particularly beneficial for remote or space-constrained sites. This trend is improving project timelines and lowering overall installation complexity for end users

- Municipal water utilities are adopting fiberglass tanks for potable water and wastewater storage due to their compliance with hygiene and safety standards. This is reinforcing their use in long-term infrastructure projects focused on reliability and operational efficiency

- The increasing preference for low-maintenance and long-lasting storage systems is accelerating the transition toward fiberglass tanks across multiple industries. This trend is contributing to sustained demand growth and reinforcing fiberglass tanks as a reliable alternative to conventional storage materials

Fiberglass Tanks Market Dynamics

Driver

Rising Investments in Water and Wastewater Infrastructure

- Rising investments in water and wastewater infrastructure are a key driver for the fiberglass tanks market as governments and municipalities focus on expanding and upgrading storage and treatment facilities. Fiberglass tanks are increasingly selected due to their resistance to corrosion and suitability for long-term water storage applications

- For instance, Containment Solutions supplies fiberglass reinforced plastic tanks for municipal wastewater and stormwater management projects. These tanks support infrastructure modernization initiatives by offering long service life and reduced maintenance needs

- The expansion of urban populations is increasing demand for reliable water storage and treatment systems, which is boosting the adoption of fiberglass tanks in municipal projects. Their ability to withstand continuous exposure to moisture and chemicals makes them suitable for large-scale infrastructure use

- Industrial wastewater treatment facilities are also driving demand as regulatory pressure increases for proper effluent management. Fiberglass tanks help operators meet compliance requirements while maintaining operational efficiency

- Continued infrastructure spending focused on water security and environmental protection is reinforcing this driver. These investments are positioning fiberglass tanks as essential components in modern water and wastewater systems

Restraint/Challenge

High Initial Installation and Manufacturing Costs

- The fiberglass tanks market faces challenges due to high initial installation and manufacturing costs associated with advanced composite materials and specialized fabrication processes. These cost factors can limit adoption among small-scale users and price-sensitive projects

- For instance, ZCL Composites employs filament winding and advanced molding techniques to produce large-capacity fiberglass tanks. While these processes ensure high strength and durability, they contribute to higher upfront production costs

- Manufacturing fiberglass tanks requires controlled production environments and skilled labor to maintain consistent quality standards. These requirements increase operational expenses for manufacturers and influence final product pricing

- Transportation and installation costs can also be higher for large fiberglass tanks due to size and handling requirements, particularly for underground applications. This adds to the overall project expenditure for end users

- The need to balance performance benefits with cost considerations remains a key challenge for the market. Addressing manufacturing efficiency and cost optimization is essential for broader adoption while maintaining the structural and durability advantages of fiberglass tanks

Fiberglass Tanks Market Scope

The market is segmented on the basis of type, resin type, usage, sales and service, application, and end users.

- By Type

On the basis of type, the fiberglass tanks market is segmented into E-Glass, A-Glass, S-Glass, AR-Glass, C-Glass, R-Glass, and Others. The E-Glass segment dominated the market with the largest revenue share of 42.6% in 2025, driven by its cost-effectiveness, strong mechanical strength, and wide availability across regions. E-Glass fibers are extensively used in tank manufacturing due to their excellent corrosion resistance and suitability for large-scale water and chemical storage applications. Manufacturers prefer E-Glass as it balances performance and affordability, supporting high-volume production across municipal and industrial projects.

The S-Glass segment is expected to witness the fastest growth during the forecast period, supported by rising demand for high-strength and high-performance fiberglass tanks. S-Glass offers superior tensile strength and durability, making it suitable for demanding industrial and oil and gas storage conditions. Growing investments in advanced infrastructure and specialized storage solutions are further accelerating adoption of S-Glass-based tanks.

- By Resin Type

On the basis of resin type, the fiberglass tanks market is segmented into polyester, vinyl ester, and others. The polyester segment accounted for the largest market revenue share in 2025, owing to its low cost, ease of processing, and good chemical resistance. Polyester resins are widely used in standard water and wastewater tanks where moderate performance requirements align with budget constraints. Their compatibility with mass production techniques further strengthens their dominance across municipal and residential applications.

The vinyl ester segment is projected to register the fastest growth rate over the forecast period, driven by increasing demand for tanks with superior corrosion and temperature resistance. Vinyl ester resins provide enhanced durability in aggressive chemical and industrial environments. Expanding chemical processing and oil and gas activities are driving preference for vinyl ester-based fiberglass tanks.

- By Usage

On the basis of usage, the fiberglass tanks market is segmented into water, oil and gas, chemicals, and wastewater. The water segment dominated the market in 2025, supported by rising investments in water storage infrastructure and municipal supply systems. Fiberglass tanks are widely adopted for potable and non-potable water storage due to their corrosion resistance and long service life. Increasing urbanization and water conservation initiatives continue to reinforce demand in this segment.

The chemicals segment is expected to grow at the fastest pace during the forecast period, driven by expanding chemical manufacturing and storage requirements. Fiberglass tanks are preferred for chemical usage due to their resistance to corrosion and ability to handle aggressive substances. Growing industrialization and stricter storage safety standards are further supporting rapid growth.

- By Sales and Service

On the basis of sales and service, the fiberglass tanks market is segmented into tank sales and service. The tank sales segment held the largest market revenue share in 2025, driven by ongoing demand for new installations across residential, commercial, and industrial sectors. Expansion of municipal infrastructure projects and industrial facilities continues to support steady tank procurement. The replacement of aging metal tanks with fiberglass alternatives is also contributing to sales growth.

The service segment is anticipated to witness the fastest growth over the forecast period, supported by increasing focus on maintenance, inspection, and refurbishment of installed tanks. Aging fiberglass infrastructure and regulatory requirements for periodic servicing are driving demand. Service offerings help extend tank lifespan, making them increasingly important for end users.

- By Application

On the basis of application, the fiberglass tanks market is segmented into composite and insulation. The composite segment dominated the market in 2025, driven by the extensive use of fiberglass tanks as structural composite solutions for storage and containment. Composite applications offer high strength-to-weight ratio and durability, making them suitable for large-scale industrial and municipal storage needs. Growing preference for lightweight and corrosion-resistant materials further supports dominance.

The insulation segment is expected to grow at the fastest rate during the forecast period, driven by increasing demand for temperature-controlled storage solutions. Fiberglass tanks with insulation properties are gaining traction in chemical and industrial applications where thermal stability is critical. Rising focus on energy efficiency and process safety is accelerating adoption.

- By End Users

On the basis of end users, the fiberglass tanks market is segmented into commercial, residential, municipal, and industrial. The municipal segment accounted for the largest revenue share in 2025, driven by extensive use of fiberglass tanks in water supply, sewage, and wastewater management systems. Long service life and low maintenance requirements make fiberglass tanks suitable for large-scale public infrastructure projects. Government investments in urban development continue to support demand.

The industrial segment is projected to witness the fastest growth over the forecast period, supported by expanding manufacturing, oil and gas, and chemical industries. Industrial facilities require durable and corrosion-resistant storage solutions for diverse fluids and chemicals. Increasing industrial output and safety compliance requirements are driving rapid adoption in this segment.

Fiberglass Tanks Market Regional Analysis

- North America dominated the fiberglass tanks market with the largest revenue share of over 45% in 2025, driven by strong investments in water infrastructure, replacement of aging metal tanks, and rising adoption of corrosion-resistant storage solutions

- End users across the region place high value on the durability, long service life, and low maintenance benefits offered by fiberglass tanks for water, wastewater, and industrial storage

- This widespread adoption is further supported by stringent environmental regulations, advanced manufacturing capabilities, and high awareness regarding sustainable storage systems, establishing fiberglass tanks as a preferred solution across municipal, commercial, and industrial applications

U.S. Fiberglass Tanks Market Insight

The U.S. fiberglass tanks market captured the largest revenue share within North America in 2025, fueled by extensive municipal water and wastewater projects and growing industrial storage requirements. Industries are increasingly prioritizing fiberglass tanks for chemical and oil and gas applications due to their superior corrosion resistance and safety performance. The strong focus on infrastructure modernization, coupled with increasing compliance with environmental and storage safety standards, continues to drive market expansion across the country.

Europe Fiberglass Tanks Market Insight

The Europe fiberglass tanks market is projected to expand at a steady CAGR during the forecast period, primarily driven by stringent environmental regulations and rising demand for efficient wastewater and chemical storage solutions. Increasing urbanization and infrastructure upgrades across residential and industrial sectors are supporting adoption. The region is witnessing growing use of fiberglass tanks in both new installations and refurbishment projects, particularly in municipal and industrial facilities.

U.K. Fiberglass Tanks Market Insight

The U.K. fiberglass tanks market is anticipated to grow at a notable CAGR during the forecast period, driven by rising investments in water management infrastructure and increasing focus on sustainable storage systems. Growing concerns regarding leakage, corrosion, and long-term maintenance are encouraging municipalities and industries to adopt fiberglass tanks. The U.K.’s emphasis on environmental compliance and efficient wastewater treatment is expected to continue supporting market growth.

Germany Fiberglass Tanks Market Insight

The Germany fiberglass tanks market is expected to expand at a considerable CAGR over the forecast period, supported by strong industrial activity and demand for high-performance storage solutions. Germany’s advanced manufacturing base and focus on chemical processing and wastewater treatment are driving adoption. The preference for durable, eco-efficient, and low-maintenance storage materials aligns well with fiberglass tank solutions across industrial and municipal applications.

Asia-Pacific Fiberglass Tanks Market Insight

The Asia-Pacific fiberglass tanks market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, expanding industrialization, and increasing investments in water and wastewater infrastructure. Governments across the region are emphasizing large-scale water storage and treatment projects, supporting market growth. In addition, the region’s role as a manufacturing hub is improving the affordability and availability of fiberglass tanks for a broad range of end users.

Japan Fiberglass Tanks Market Insight

The Japan fiberglass tanks market is gaining traction due to growing demand for reliable water storage and efficient wastewater management systems. The country’s focus on infrastructure resilience and disaster preparedness is supporting the adoption of durable fiberglass storage solutions. Increasing industrial activity and modernization of municipal facilities are further contributing to market growth.

China Fiberglass Tanks Market Insight

The China fiberglass tanks market accounted for the largest revenue share within Asia-Pacific in 2025, attributed to rapid urbanization, large-scale municipal projects, and strong growth in chemical and industrial sectors. China’s extensive investments in water supply, wastewater treatment, and industrial infrastructure are driving high demand for fiberglass tanks. The presence of strong domestic manufacturers and cost-effective production capabilities continues to reinforce the country’s leading position in the regional market.

Fiberglass Tanks Market Share

The fiberglass tanks industry is primarily led by well-established companies, including:

- PPG Industries, Inc. (U.S.)

- Design Tanks (U.S.)

- Denali Incorporated (U.S.)

- NOV Inc. (U.S.)

- Enduro Composites (U.S.)

- Russel Metals Inc. (Canada)

- EPP Composites Pvt Ltd (India)

- Amiblu Holding GmbH (Austria)

- Nationwide Tank and Pipe LLC (U.S.)

- ANDRONACO INDUSTRIES (U.S.)

- Gruppo Sarplast (Italy)

- FIBREX (Saudi Arabia)

- FCX Performance (U.S.)

- Hengrun Group Co., Ltd (China)

- Graphite India Limited (India)

- ADPF (U.A.E.)

- Balaji Fiber Reinforce Pvt. Ltd. (India)

- Zhongfu Lianzhong Group (China)

Latest Developments in Global Fiberglass Tanks Market

- In September 2025, CST Industries Inc introduced a new range of fiberglass tanks tailored for agricultural applications, using advanced composite materials to improve durability and lower long-term maintenance costs. This development strengthens CST Industries’ position in the agriculture segment by addressing sector-specific storage challenges and expanding its specialized product portfolio, supporting higher adoption among farming and agribusiness customers

- In August 2025, Snyder Industries Inc announced the opening of a new manufacturing facility in Texas to expand production capacity and improve service coverage across the southern U.S. This expansion is expected to enhance the company’s competitive position by reducing logistics costs, shortening delivery timelines, and enabling faster response to regional demand, thereby supporting market share growth

- In July 2025, ZCL Composites Inc entered into a strategic partnership with a major water treatment company to develop integrated fiberglass tank and water purification solutions. This collaboration reflects a broader market shift toward integrated systems, enabling ZCL Composites to extend its value proposition beyond storage and strengthen its presence in municipal and industrial water projects

- In May 2025, Containment Solutions Inc expanded its product portfolio with high-capacity fiberglass tanks designed for municipal wastewater applications. This move supports the company’s growth in public infrastructure projects by addressing increasing wastewater treatment requirements and reinforcing demand for corrosion-resistant, long-life storage solutions

- In March 2025, LF Manufacturing Inc invested in process automation upgrades across its fiberglass tank production facilities to improve manufacturing efficiency and product consistency. This investment is expected to enhance cost competitiveness, support higher production volumes, and enable the company to better meet rising demand from industrial and commercial end users

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.