Global Flexible Pipe Market

Taille du marché en milliards USD

TCAC :

%

USD

10.21 Billion

USD

32.30 Billion

2024

2032

USD

10.21 Billion

USD

32.30 Billion

2024

2032

| 2025 –2032 | |

| USD 10.21 Billion | |

| USD 32.30 Billion | |

| % | |

|

Segmentation du marché mondial des tubes flexibles, par matières premières (polyéthylène de haute densité, polyamide, fluorure de polyvinylidène, etc.), application (sur terre et en mer), verticale (huile et gaz, énergie renouvelable, bâtiment et construction, industrie, agriculture, etc.) – Tendances et prévisions de l'industrie jusqu'en 2032

Flexible Pipe Market Size

-

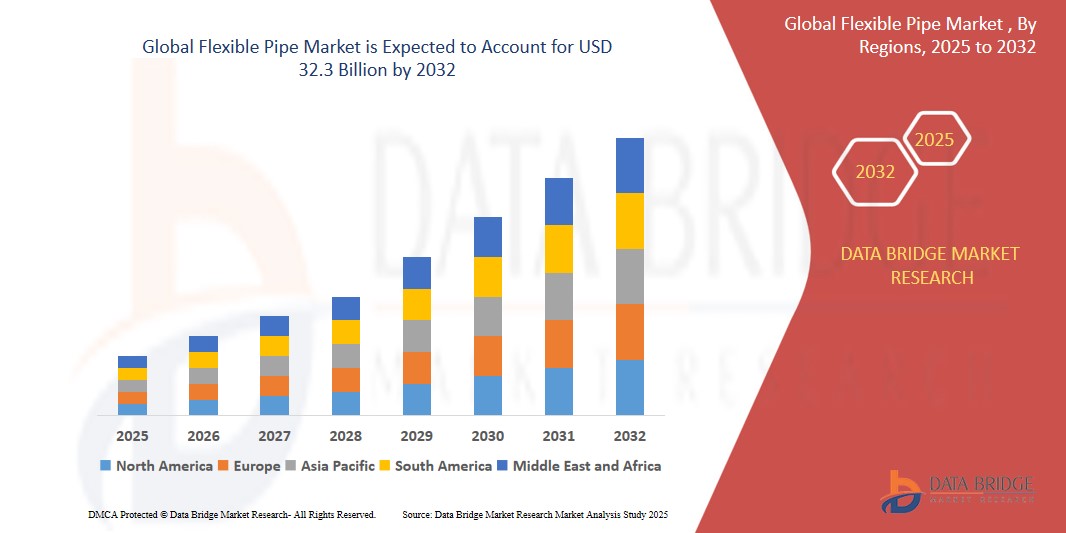

The Global Flexible Pipe Market was valued atUSD 10.21 Billion in 2024 and is expected to reachUSD 32.3 billion by 2032

- During the forecast period of 2025 to 2032 the Market is likely to grow at aCAGR of 4.4%, primarily driven by the increasing offshore oil & gas exploration spending on a global level

- This growth is driven by factors such as Increasing offshore oil & gas exploration activities and technological advancements in materials and pipe design.

Flexible Pipe Market Analysis

- The global flexible pipe market is expanding due to increased offshore oil and gas exploration. Flexible pipes are preferred in deepwater projects for their durability, corrosion resistance, and ease of installation. Demand is particularly high in regions such as the Gulf of Mexico, Brazil, and West Africa as a result of increased spending on offshore exploration and production spending

- Technological advancements in pipe materials, such as thermoplastics and composite reinforcements, have improved performance in high-pressure and corrosive environments. These innovations are driving adoption across energy and industrial sectors.

- However, high initial costs and complex installation processes act as restraints. Smaller companies face financial barriers, while regulatory compliance also adds pressure on manufacturers, slowing market penetration.

- Emerging opportunities lie in renewable energy and infrastructure projects in Asia-Pacific and Latin America. As these regions industrialize rapidly, flexible pipes are gaining traction in water management, energy transmission, and industrial applications.

- High-density polyethylene dominated the market with a revenue share of more than 45% in 2024 and is further expected to grow at a significant rate over the forecast period. This domination is attributed to the to its excellent strength-to-density ratio, resistance to corrosion, and cost-effectiveness. It is widely utilized in various applications, particularly in the oil and gas sector, where it can withstand high pressures and harsh environmental conditions.

Report Scope and Flexible Pipe Market Segmentation

|

Attributes |

Flexible Pipe Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on Market scenarios such as Market value, growth rate, segmentation, geographical coverage, and major players, the Market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

In 2025, the high density polyethylene segment is projected to dominate the market with a largest share in the raw material segment

High-density polyethylene dominated the market with a revenue share of around 45% in 2025 and is further expected to grow at a significant rate over the forecast period. HDPE is the most dominant material in the market due to its excellent strength-to-density ratio, resistance to corrosion, and cost-effectiveness. It is widely utilized in various applications, particularly in the oil and gas sector, where it can withstand high pressures and harsh environmental conditions.

Offshore is expected to account for the largest share during the forecast period in technology market

In 2025, offshore led the flexible pipe market and accounted for a revenue share of more than 70%. The flexibility and adaptability of these pipes allow for easier installation and maintenance in complex terrains, making them a preferred choice among offshore oil and gas companies.

Flexible Pipe Market Trends

“Increasing investment in offshore projects”

- The flexible pipe market is witnessing a strong shift toward deepwater and ultra-deepwater oil exploration. Increasing investments in offshore projects, especially in Brazil and the Gulf of Mexico, are fueling demand for advanced flexible piping solutions.

- For instance, the flexible pipe market is evolving with increased offshore oil exploration and renewable energy integration. Innovations in composite materials enhance durability and flexibility, while smart sensors improve monitoring. Growing demand in emerging economies and sustainable infrastructure projects further accelerates adoption, positioning flexible pipes as essential in modern energy and industrial systems.

- Material innovation is a core trend, with manufacturers integrating high-performance polymers and composite reinforcements. These enhance flexibility, corrosion resistance, and pressure tolerance, aligning with harsh offshore and industrial applications.

- Digital transformation is gaining ground as smart flexible pipes embedded with sensors support real-time monitoring, predictive maintenance, and enhanced operational safety in critical environments like subsea installations.

- Sustainability and energy diversification are reshaping the market. Flexible pipes are increasingly used in renewable sectors like offshore wind and geothermal energy. This trend is further supported by government incentives and growing infrastructure investment in emerging markets.

Flexible Pipe Market Dynamics

Driver

“Increasing Offshore Oil & Gas Exploration Activities”

- The global demand for energy continues to rise, driving exploration and production efforts in offshore oil and gas fields. Deepwater and ultra-deepwater reserves have become more attractive due to advancements in subsea technologies. Flexible pipes are essential in these projects due to their ability to withstand high pressure, dynamic sea currents, and complex topography, making them critical components in subsea infrastructure. As oil companies expand into harsher offshore environments, demand for flexible pipes surges.

- Furthermore, flexible pipes offer advantages over rigid alternatives, including lower installation costs and better resistance to fatigue and corrosion. Their ability to bend under extreme conditions reduces the risk of leakage or failure, thereby improving operational safety and efficiency. These benefits significantly appeal to offshore developers who prioritize long-term performance and environmental security.

- The resurgence of offshore investments in regions such as West Africa, the Gulf of Mexico, and Southeast Asia contributes heavily to market growth. These regions are seeing large-scale capital expenditures on offshore rigs and pipeline infrastructure, with flexible pipes being a crucial enabler. National oil companies and private operators are increasingly relying on innovative pipe solutions to boost production without compromising on safety or cost.

- In addition, governments in oil-rich economies are offering incentives and regulatory support for offshore exploration to enhance energy security. This is reinforcing the deployment of advanced piping technologies, creating a ripple effect across the entire flexible pipe value chain. Overall, the offshore oil and gas boom stands out as a pivotal driver for market expansion globally.

Opportunity

“Expansion of Renewable Energy Infrastructure”

- As the world shifts toward cleaner energy, there's a growing need for flexible pipes in renewable infrastructure, particularly in offshore wind farms and geothermal energy. These installations require dynamic cable protection systems, fluid transport, and advanced piping for cooling and hydraulic systems—all potential applications for flexible pipes.

- Flexible pipes are suitable for floating wind platforms and subsea energy transmission, as they accommodate environmental movement and pressure variations. As offshore wind expands in regions like Europe, China, and the U.S., demand for advanced piping solutions will likely follow.

- Government incentives and green transition funding are creating a favorable investment climate. Companies entering or pivoting toward the renewables sector can capitalize on this trend by adapting flexible pipe solutions to clean energy needs, thereby diversifying revenue streams beyond fossil fuels.

- The growing integration of hybrid energy platforms—like offshore oil rigs co-located with wind farms—also presents new cross-industry applications. This broadens the market scope and provides a path for long-term sustainable growth for flexible pipe manufacturers.

Restraint/Challenge

“High Initial Costs and Complex Installation”

- Despite the advantages flexible pipes offer, their high initial investment remains a key restraint. The materials used—such as thermoplastic composites and corrosion-resistant alloys—are significantly more expensive than those in conventional piping systems. In addition, the specialized manufacturing processes and stringent quality standards increase the cost of production.

- Installation of flexible pipes, especially in offshore settings, requires skilled labor, advanced equipment, and precise engineering. This results in higher deployment costs compared to rigid pipes. Small and medium enterprises (SMEs) often find it financially challenging to adopt these systems, limiting the market’s growth among cost-sensitive sectors.

- Furthermore, logistical challenges in transporting flexible pipes to remote or offshore locations can escalate project timelines and budgets. These practical difficulties discourage adoption, especially in emerging economies where infrastructure and capital availability may be limited.

- While long-term cost savings from reduced maintenance may offset these expenses, the upfront financial burden continues to hinder faster market penetration. The need for significant capital investment narrows the customer base to larger players with deeper financial resources.

Flexible Pipe Market Scope

The market is segmented on the basis of raw material and application

|

Segmentation |

Sub-Segmentation |

|

By Raw Material |

|

|

By Application |

|

|

By Vertical |

|

Flexible Pipe Market Regional Analysis

“North America is the Dominant Region in the Flexible Pipe Market”

- North America, is expected to dominate the market due to extensive offshore oil and gas operations, particularly in the Gulf of Mexico, alongside significant investments in shale gas exploration and production. The region's advanced infrastructure and stringent environmental regulations further bolster the demand for flexible piping solutions.

- U.S. is the dominant country in the global flexible pipe market. This leadership is attributed to significant offshore oil and gas operations, particularly in the Gulf of Mexico, and substantial investments in shale gas exploration. Government policies aimed at boosting energy production further bolster demand for flexible pipe solutions.

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- Asia-Pacific region is recognized as the fastest-growing market for flexible pipes, propelled by expanding industrial activities, particularly in offshore oil and gas exploration and production. Growing investments in infrastructure development and rising demand for energy resources contribute to the region's significant market growth.

Flexible Pipe Market Share

The Market competitive landscape provides details by competitors and market share. Details included are company overview, company financials, revenue generated, Market potential, investment in research and development, new Market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to Market.

The Major Market Leaders Operating in the Global Flexible Pipe Market Are:

- Chevron Phillips Chemical Company (U.S.)

- Evonik Industries (Germany)

- National Oilwell Varco, Inc. (U.S.)

- Technip Inc. (now Technip Energies) (France)

- Prysmian Group (Italy)

- Baker Hughes Company (U.S.)

- General Electric (U.S.)

- Shawcor Ltd. (Canada)

- Pipelife Nederland B.V. (Netherlands)

- Airborne Oil & Gas (Netherlands)

- Magma Global Ltd. (U.K.)

- ContiTech AG (Germany)

- FlexSteel Pipeline Technologies, Inc. (U.S.)

Latest Developments in Global Flexible Pipe Market

- In November 2023, Baker Hughes Company announced plans to launch of new pipe under the brand of PythonPipe. The pipe utilizes the reinforced thermoplastic pipe (RTP) technology that enables fast installation, reduced time to first production and low lifecycle emissions.

- In February 2017, Airborne Oil & Gas received a qualification program from Royal Dutch Shell plc (Netherlands) for a high-pressure, deepwater thermoplastic composite pipe (TCP) jumper spool. The first deployment is planned for the Gulf of Mexico. The lightweight and flexible design of these polymer pipes is expected to significantly lower operational costs in deepwater exploration. Additionally, the high-pressure jumper spool marks a critical advancement toward the future use of deepwater composite risers.

- In January 2017, National Oilwell Varco (NOV) introduced an innovation in oil and gas technology with the development of an automated casing monitoring system called cerT&D. This system has shown promising applications in multiple projects by enabling real-time monitoring. Its use by Three Rivers Operating Company (3ROC) helped avoid exceeding the tensile limits of rig site and pipe equipment, allowing operations to reach total depth (TD) safely and without causing damage to the equipment or casing.

- In February 2016, Technip secured a contract from Deep Gulf Energy III, LLC (DGE) for the development of the South Santa Cruz and Barataria fields. The agreement includes several deliverables, among them the fabrication and installation of approximately 23 kilometers of pipe-in-pipe flowlines.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.