Global Herbal Products Market

Taille du marché en milliards USD

TCAC :

%

USD

54.01 Billion

USD

91.76 Billion

2025

2033

USD

54.01 Billion

USD

91.76 Billion

2025

2033

| 2026 –2033 | |

| USD 54.01 Billion | |

| USD 91.76 Billion | |

| % | |

|

Global Herbal Products Market Segmentation, By Product (Moringa, Echinacea, Flaxseeds, Turmeric, Ginger and Ginseng), Formulation (Tablets, Capsules, Liquid, Powder and Granules, Soft Gels and Others), Consumer (Pregnant Women, Adult, Paediatric and Geriatric), Source (Leaves, Fruits and Vegetable, Barks, Roots and Others), Function (Medicinal, Aroma and Others), Application (Pharmaceutical, Personal Care, Food and Beverages and Others), Distribution Channel (Offline Stores and Online Stores)- Industry Trends and Forecast to 2033

Herbal Products Market Size

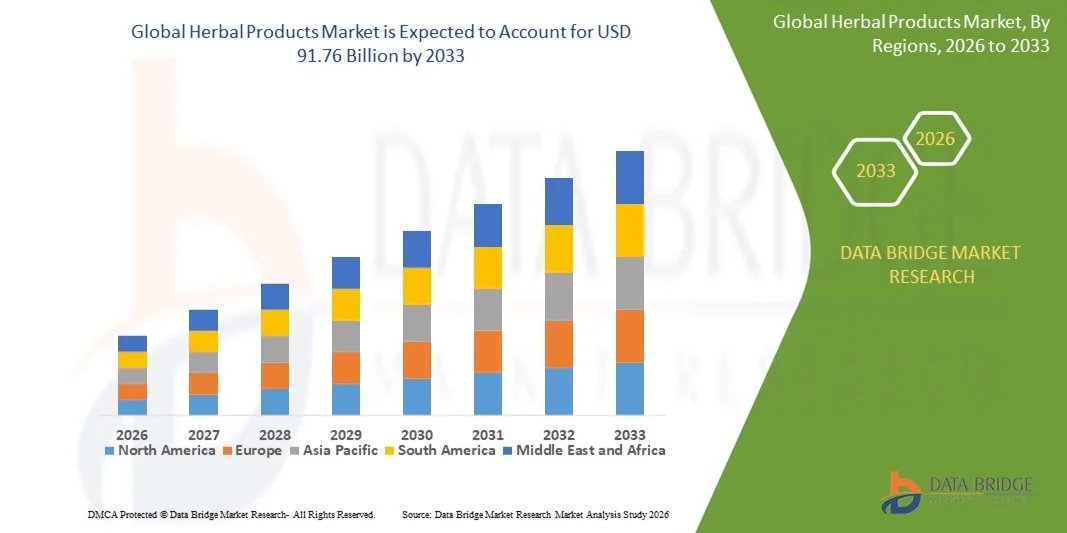

- The global herbal products market size was valued at USD 54.01 billion in 2025 and is expected to reach USD 91.76 billion by 2033, at a CAGR of 6.85% during the forecast period

- The market growth is largely fuelled by the increasing consumer preference for natural and plant-based remedies, rising health consciousness, and growing awareness of the benefits of herbal supplements and cosmetics

- Expansion of herbal-based personal care products, nutraceuticals, and traditional medicines is further driving market demand

Herbal Products Market Analysis

- Consumers are increasingly seeking natural and safe alternatives to synthetic drugs and chemical-based personal care products, promoting adoption of herbal products

- Continuous product innovations, research in herbal formulations, and supportive regulatory frameworks are encouraging the growth of the herbal products market

- North America dominated the global herbal products market in 2025 with the largest revenue share, supported by strong consumer interest in plant‑based wellness and natural supplements, along with well‑established retail and e‑commerce channels driving widespread adoption of herbal formulations and remedies

- Asia-Pacific region is expected to witness the highest growth rate in the global herbal products market, driven by increasing disposable incomes, expanding urban population, growing awareness of preventive healthcare, and strong demand for natural and herbal products in countries such as China and India

- The Turmeric segment held the largest market revenue share in 2025, driven by its extensive use in traditional medicine, dietary supplements, and functional foods. Turmeric’s bioactive compound, curcumin, is highly sought after for its antioxidant and anti-inflammatory properties, making it a popular choice among health-conscious consumers. Increasing consumer preference for natural remedies and preventive healthcare solutions further supports its dominance. In addition, Turmeric-based products are being increasingly incorporated into beverages, snacks, and skincare products

Report Scope and Herbal Products Market Segmentation

|

Attributes |

Herbal Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Herbal Products Market Trends

Rising Demand for Natural and Plant-Based Remedies

- The growing focus on natural, plant-derived, and minimally processed products is significantly shaping the herbal products market, as consumers increasingly prefer remedies and personal care solutions that are safe, chemical-free, and eco-friendly. Herbal products are gaining traction due to their perceived health benefits, supporting immunity, wellness, and holistic care, strengthening adoption across nutraceuticals, personal care, and traditional medicine segments

- Increasing awareness around health, wellness, and preventive care has accelerated demand for herbal products in dietary supplements, functional beverages, skincare, and haircare solutions. Health-conscious consumers and environmentally aware populations are actively seeking products formulated with natural ingredients, prompting manufacturers to emphasize sustainability and transparency in sourcing and production

- Clean-label, safety, and sustainability trends are influencing purchasing decisions, with manufacturers highlighting certifications, organic labeling, and eco-friendly practices. These factors help brands differentiate products in a competitive market and build consumer trust, while also driving adoption of natural certifications. Marketing campaigns increasingly reinforce these benefits to strengthen brand positioning and appeal to conscious consumers

- For instance, in 2024, Himalaya in India and Weleda in Germany expanded their product portfolios by launching new herbal supplements and personal care products. These introductions responded to rising consumer preference for natural remedies and clean-label formulations, with distribution across retail, specialty, and online channels. The products were marketed as health-conscious and environmentally responsible, enhancing brand loyalty and repeat purchases

- While demand for herbal products is growing, sustained market expansion depends on continuous R&D, standardization, and maintaining efficacy comparable to conventional products. Manufacturers are also focusing on improving scalability, supply chain reliability, and developing innovative solutions that balance cost, quality, and sustainability for broader adoption

Herbal Products Market Dynamics

Driver

Rising Preference For Natural, Plant-Based Remedies

- Increasing consumer demand for natural, plant-derived solutions is a major driver for the herbal products market. Manufacturers are actively replacing synthetic or chemical-based ingredients with herbal alternatives to meet clean-label and wellness-focused requirements, improve product appeal, and comply with regulatory standards. This trend is also pushing research into novel plant-based formulations, supporting product diversification

- Expanding applications in dietary supplements, personal care, functional foods, and traditional medicine are influencing market growth. Herbal products help enhance health, wellness, and overall consumer satisfaction, enabling manufacturers to meet expectations for high-quality, natural offerings. The growing adoption of preventive healthcare and holistic lifestyles globally further reinforces this trend

- Herbal product manufacturers are actively promoting herbal-based formulations through product innovation, marketing campaigns, and certifications. These efforts are supported by the increasing consumer preference for natural, safe, and sustainable products, and they encourage collaborations between ingredient suppliers and brands to improve product efficacy and reduce environmental impact

- For instance, in 2023, Dabur in India and Nature’s Bounty in the U.S. reported increased incorporation of herbal ingredients in dietary supplements and personal care products. This expansion followed higher consumer demand for natural, plant-based, and non-GMO products, driving repeat purchases and product differentiation. Both companies highlighted sustainability, traceability, and efficacy in marketing campaigns to strengthen consumer trust and brand loyalty

- Although rising natural and wellness-focused trends support growth, wider adoption depends on cost optimization, ingredient quality, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced formulation technology will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Cost And Limited Awareness Compared To Conventional Products

- The relatively higher cost of herbal products compared to conventional chemical-based alternatives remains a key challenge, limiting adoption among price-sensitive consumers. Higher raw material costs, complex extraction or processing methods, and seasonal availability contribute to elevated pricing

- Consumer and manufacturer awareness remains uneven, particularly in developing markets where natural or herbal product demand is still emerging. Limited understanding of functional benefits restricts adoption across certain product categories, and slower innovation uptake occurs in regions with minimal educational initiatives on herbal products

- Supply chain and distribution challenges also impact market growth, as herbal products require sourcing from certified suppliers and adherence to stringent quality standards. Logistical complexities, shelf-life limitations, and proper storage requirements increase operational costs

- For instance, in 2024, distributors in Southeast Asia supplying herbal dietary supplements and personal care brands such as Himalaya and Swisse reported slower uptake due to higher prices and limited awareness of functional advantages compared to conventional products. Storage requirements and certification compliance were additional barriers, prompting some retailers to limit shelf space for premium herbal products

- Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and consumers. Collaboration with retailers, healthcare operators, and certification bodies can help unlock the long-term growth potential of the global herbal products market. Developing cost-competitive formulations and strengthening marketing strategies around efficacy, natural benefits, and sustainability will be essential for widespread adoption

Herbal Products Market Scope

The market is segmented on the basis of product, formulation, consumer, source, function, application, and distribution channel.

- By Product

On the basis of product, the herbal products market is segmented into Moringa, Echinacea, Flaxseeds, Turmeric, Ginger, and Ginseng. The Turmeric segment held the largest market revenue share in 2025, driven by its extensive use in traditional medicine, dietary supplements, and functional foods. Turmeric’s bioactive compound, curcumin, is highly sought after for its antioxidant and anti-inflammatory properties, making it a popular choice among health-conscious consumers. Increasing consumer preference for natural remedies and preventive healthcare solutions further supports its dominance. In addition, Turmeric-based products are being increasingly incorporated into beverages, snacks, and skincare products.

The Moringa segment is expected to witness the fastest growth rate from 2026 to 2033, owing to its rich nutritional profile, versatility in food and beverage applications, and increasing awareness of its health benefits. Moringa leaves and powder are recognized for high protein, vitamins, and mineral content, driving consumer adoption. Rising demand for plant-based nutritional supplements and superfood powders is expected to propel market growth. Manufacturers are introducing innovative Moringa products in smoothies, teas, and dietary supplements to cater to a wider audience.

- By Formulation

On the basis of formulation, the market is segmented into Tablets, Capsules, Liquid, Powder and Granules, Soft Gels, and Others. The Capsules segment held the largest market revenue share in 2025 due to convenience in consumption and consistent dosage delivery, appealing to a broad consumer base. Capsules are preferred for their ease of use, portability, and ability to mask strong herbal flavors. Health-conscious consumers increasingly opt for capsules as part of daily wellness routines. In addition, advancements in encapsulation technology are enhancing the bioavailability of herbal extracts in this form.

The Powder and Granules segment is projected to grow at the fastest rate during 2026–2033, driven by rising adoption in beverages, smoothies, and cooking ingredients. Powders provide flexibility in dosage and are easy to incorporate into functional foods and drinks. Growing consumer awareness of natural ingredients in daily nutrition supports demand for herbal powders. Manufacturers are innovating by blending multiple herbal powders to create nutrient-rich supplements. E-commerce platforms also facilitate convenient purchase and delivery of herbal powders.

- By Consumer

On the basis of consumer, the market is segmented into Pregnant Women, Adult, Paediatric, and Geriatric. The Adult segment held the largest market share in 2025, driven by increasing awareness of preventive healthcare and the rising adoption of herbal supplements for wellness and immunity. Adults are more likely to integrate herbal products into daily routines for stress management, energy boosting, and chronic disease prevention. Marketing campaigns highlighting natural ingredients and health benefits have further boosted adoption. The segment continues to benefit from the rising trend of functional foods and herbal beverages.

The Geriatric segment is projected to grow at the fastest rate during 2026–2033, fueled by the growing aging population seeking natural remedies for chronic ailments and age-related health conditions. Herbal products such as Ginseng and Turmeric are preferred for joint health, cardiovascular support, and cognitive wellness. Increasing disposable income among older adults enables investment in high-quality herbal supplements. Health practitioners are also recommending herbal interventions for age-related wellness. Growing geriatric-focused product lines by manufacturers is supporting market expansion.

- By Source

On the basis of source, the market is segmented into Leaves, Fruits and Vegetables, Barks, Roots, and Others. The Leaves segment dominated in 2025 due to their high concentration of bioactive compounds and ease of processing for diverse product formulations. Leaves such as Moringa, Eucalyptus, and Mint are widely used in teas, capsules, and extracts. The convenience of cultivation and sustainable harvesting makes leaves a cost-effective source. Rising demand for plant-based diets and herbal remedies further reinforces market share. Leaves also offer versatility for cosmetic and personal care applications.

The Roots segment is expected to grow the fastest from 2026 to 2033, driven by increasing demand for traditional herbal remedies and extracts with medicinal properties. Roots such as Ginger, Ginseng, and Turmeric are valued for their potent therapeutic effects. Growing preference for Ayurvedic and traditional medicine globally supports this growth. Innovative root extracts and blends are being launched in functional foods, beverages, and supplements. Consumer education on root-based benefits is increasing adoption across regions.

- By Function

On the basis of function, the market is segmented into Medicinal, Aroma, and Others. The Medicinal segment held the largest market revenue share in 2025 due to extensive use of herbal products in therapeutic treatments, immunity boosters, and preventive healthcare. Medicinal herbs are incorporated into dietary supplements, herbal teas, and pharmaceutical formulations. Rising health consciousness and the prevalence of lifestyle diseases are driving demand. Research and clinical validation of herbal benefits enhance consumer trust. Manufacturers are increasingly positioning medicinal herbs as alternatives to synthetic drugs.

The Aroma segment is projected to grow at the fastest rate during 2026–2033, supported by the rising popularity of essential oils, aromatherapy, and personal care products incorporating natural fragrances. Consumers are seeking herbal-based wellness solutions for relaxation, stress relief, and mental wellness. Increasing use in candles, diffusers, and skincare products is expanding market opportunities. The growth of home-based self-care routines is boosting adoption. Companies are innovating with blends of aromatic herbs to create multifunctional products.

- By Application

On the basis of application, the market is segmented into Pharmaceutical, Personal Care, Food and Beverages, and Others. The Food and Beverages segment held the largest share in 2025, driven by the incorporation of herbal ingredients in functional foods, beverages, and dietary supplements. Herbal teas, juices, and snacks with health-promoting properties are increasingly popular. Consumers prefer natural ingredients in their diet for preventive health. Product innovation with blends of multiple herbs is enhancing nutritional profiles. Rising global focus on wellness foods supports continued growth.

The Personal Care segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for natural skincare, haircare, and cosmetic products free from synthetic chemicals. Herbal extracts such as Aloe Vera, Turmeric, and Ginseng are widely used for skin and hair wellness. Increasing consumer preference for clean-label and sustainable personal care products is driving growth. Companies are leveraging herbal properties for anti-aging, moisturizing, and therapeutic benefits. Online marketing and influencer campaigns are enhancing consumer awareness.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Offline Stores and Online Stores. The Offline Stores segment held the largest market share in 2025 due to established retail networks, consumer trust, and direct product accessibility. Pharmacies, health stores, and supermarkets serve as key purchase points for herbal products. Brand loyalty and product trials in physical stores continue to support sales. In addition, offline presence allows consumers to access detailed product information and expert advice.

The Online Stores segment is expected to grow at the fastest rate during 2026–2033, supported by the increasing adoption of e-commerce platforms, convenience of home delivery, and expanding awareness of herbal product availability through digital channels. Online platforms offer access to a wide variety of products and competitive pricing. Rising smartphone penetration and digital literacy facilitate online purchases. Subscription-based herbal products and targeted promotions drive repeated sales. Social media marketing is further enhancing online adoption.

Herbal Products Market Regional Analysis

- North America dominated the global herbal products market in 2025 with the largest revenue share, supported by strong consumer interest in plant‑based wellness and natural supplements, along with well‑established retail and e‑commerce channels driving widespread adoption of herbal formulations and remedies

- Consumers in the region appreciate the health benefits, traditional roots, and perceived safety of herbal products, and this preference is reinforced by high disposable incomes, growth in preventive health spending, and regulatory frameworks that support natural health alternatives

- This broad adoption is further bolstered by a growing focus on integrative medicine, increased awareness of lifestyle‑related health conditions, and strategic innovation by key manufacturers, making herbal products increasingly commonplace in both personal care and dietary applications

U.S. Herbal Products Market Insight

The U.S. herbal products market accounted for a significant portion of the North American share in 2025, driven by rising acceptance of botanical supplements, natural remedies, and plant‑derived cosmetic ingredients. Consumers are increasingly choosing herbal options for fitness, immunity boosting, and overall wellness, with e‑commerce platforms expanding access and convenience. The integration of herbal products into mainstream health and beauty routines, combined with robust marketing and product innovation, continues to propel market expansion.

Europe Herbal Products Market Insight

The Europe herbal products market is expected to achieve consistent growth from 2026 to 2033, motivated by favorable regulatory environments for traditional herbal medicinal products, and a strong cultural preference for natural health solutions. Urban populations across European countries are increasingly prioritizing clean‑label and plant‑based products, and demand is rising across dietary supplements, personal care, and herbal remedies. The region’s aging population and expanding wellness tourism further reinforce market dynamics.

U.K. Herbal Products Market Insight

The U.K. herbal products market is poised for accelerated growth from 2026 to 2033, boosted by heightened consumer interest in botanical wellness and preventive health solutions. Increased online sales penetration and strong retail presence of herbal supplements, combined with growing awareness of natural alternatives, encourage both individual and family purchases. The country’s extensive retail infrastructure and wellness culture are expected to sustain solid market growth.

Germany Herbal Products Market Insight

The Germany herbal products market is anticipated to grow significantly from 2026 to 2033, propelled by well‑established herbal traditions, strong pharmaceutical and natural health sectors, and keen consumer interest in scientifically validated botanical products. Consumers in Germany tend to favor natural health and beauty formulations, and integration of herbal ingredients into daily routines is becoming more prevalent, supporting steady market expansion.

Asia‑Pacific Herbal Products Market Insight

The Asia‑Pacific herbal products market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and enduring cultural traditions of herbal medicine in countries such as China, India, and Japan. Deep‑rooted practices like Traditional Chinese Medicine and Ayurveda contribute to widespread adoption, while strong domestic manufacturing capabilities and export growth enhance global competitiveness. Consumers in the region are embracing herbal products across healthcare, beauty, and wellness categories, reinforcing the region’s leadership in the global market.

Japan Herbal Products Market Insight

The Japan herbal products market is projected to expand rapidly from 2026 to 2033, supported by the country’s advanced wellness culture and demand for high‑quality natural products. Herbal formulations that integrate with holistic health routines, particularly among health‑conscious and aging populations, are gaining prominence. The blend of traditional herbal practices with modern product innovation and high consumer spending power sustains strong market momentum.

China Herbal Products Market Insight

The China herbal products market held a dominant share in Asia‑Pacific in 2025, fueled by the long history of traditional herbal medicine, robust domestic production, and a growing middle class with rising health awareness. Extensive use of herbal products in preventive healthcare, strong export activity, and supportive policy initiatives for traditional medicine systems are key factors driving the market. China continues to be a central hub for herbal raw materials and finished products, contributing significantly to global herbal market growth.

Herbal Products Market Share

The Herbal Products industry is primarily led by well-established companies, including:

- Jarrow Formulas, Inc. (U.S.)

- Gaia Herbs (U.S.)

- NOW Foods (U.S.)

- Bio Botanica, Inc. (U.S.)

- Nature’s Bounty (U.S.)

- Solgar Inc. (U.S.)

- Ancient Greenfields PVT LTD (India)

- Bactolac Pharmaceutical, Inc. (U.S.)

- Bionova (U.S.)

- Sunfood (U.S.)

- Supplement Manufacturing Partner (U.S.)

- Cedar Bear Naturales (U.S.)

- Biolife Technologies (U.S.)

- ABH nature's products (U.S.)

- Atlantic Essentials Products, INC. (U.S.)

- TVS Biotech (India)

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.