Global Intrusion Detection And Prevention Systems Idps Market

Taille du marché en milliards USD

TCAC :

%

USD

6.91 Billion

USD

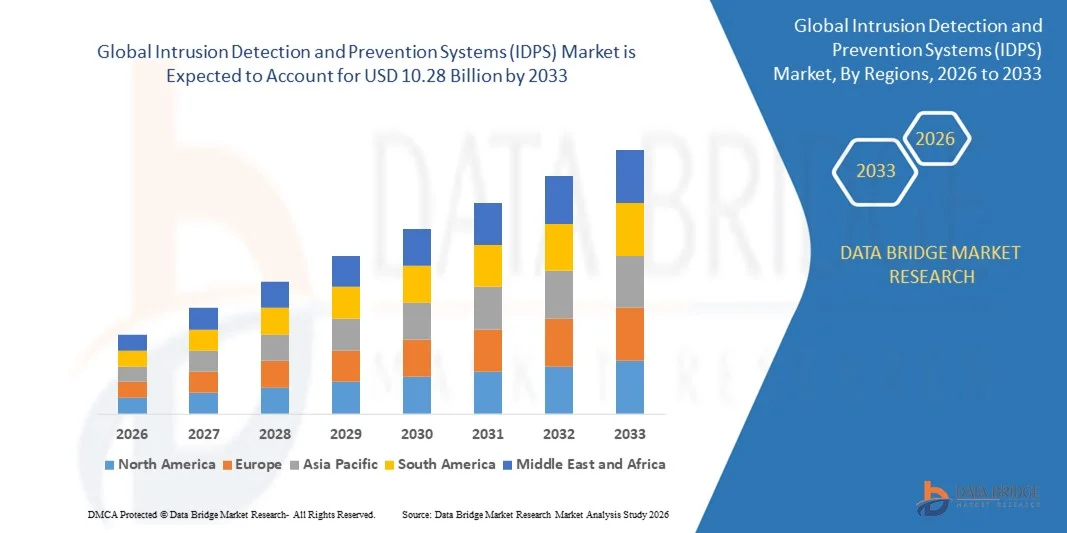

10.28 Billion

2025

2033

USD

6.91 Billion

USD

10.28 Billion

2025

2033

| 2026 –2033 | |

| USD 6.91 Billion | |

| USD 10.28 Billion | |

| % | |

|

Global Intrusion Detection and Prevention Systems (IDPS) Market Segmentation, By Component (Solutions and Services), Type (Network-based, Wireless-based, Network Behavior Analysis, and Host-based), Deployment Type (Cloud and On-Premises), Organization Size (SMEs and Large Enterprises), Vertical (Banking, Financial Services and Insurance (BFSI), Government and Defense, Healthcare, Information Technology (IT) and Telecom, Retail and eCommerce, Manufacturing, and Others) - Industry Trends and Forecast to 2033

Intrusion Detection and Prevention Systems (IDPS) Market Size

- The global Intrusion Detection and Prevention Systems (IDPS) market size was valued at USD 6.91 billion in 2025 and is expected to reach USD 10.28 billion by 2033, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital technologies, cloud computing, and hybrid IT infrastructures, which are driving organizations to implement advanced cybersecurity measures to protect critical data and networks

- Furthermore, rising cyber threats, regulatory compliance requirements, and the need for real-time monitoring and automated threat prevention are establishing Intrusion Detection and Prevention Systems (IDPS) as a vital component of enterprise security strategies. These converging factors are accelerating the deployment of Intrusion Detection and Prevention Systems (IDPS) solutions, thereby significantly boosting the industry’s growth

Intrusion Detection and Prevention Systems (IDPS) Market Analysis

- Intrusion Detection and Prevention Systems (IDPS) solutions, providing real-time detection and prevention of network intrusions, are becoming increasingly critical for organizations across BFSI, IT, healthcare, and government sectors due to their ability to safeguard sensitive data, maintain network integrity, and respond to cyberattacks proactively

- The escalating demand for Intrusion Detection and Prevention Systems (IDPS) is primarily fueled by the growing frequency and sophistication of cyberattacks, increased digital transformation initiatives, and the rising preference for automated, AI-enabled threat detection and response capabilities across enterprises

- North America dominated the Intrusion Detection and Prevention Systems (IDPS) market with a share of 38.8% in 2025, due to increasing cybersecurity concerns, widespread digital transformation, and high adoption of cloud and enterprise IT infrastructure

- Asia-Pacific is expected to be the fastest growing region in the Intrusion Detection and Prevention Systems (IDPS) market during the forecast period due to rapid digitalization, urbanization, and increasing cybersecurity investments in countries such as China, Japan, and India

- Cloud segment dominated the market with a market share of 58.3% in 2025, due to its scalability, flexibility, and ability to provide real-time monitoring and centralized threat management across distributed networks. Organizations preferred cloud-based Intrusion Detection and Prevention Systems (IDPS) for seamless updates, reduced infrastructure costs, and ease of integration with existing IT ecosystems

Report Scope and Intrusion Detection and Prevention Systems (IDPS) Market Segmentation

|

Attributes |

Intrusion Detection and Prevention Systems (IDPS) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Intrusion Detection and Prevention Systems (IDPS) Market Trends

Growing Adoption of AI-Driven and Cloud-Based IDPS Solutions

- A significant trend in the Intrusion Detection and Prevention Systems (IDPS) market is the rising adoption of artificial intelligence (AI) and cloud-based solutions to enhance threat detection, response, and overall cybersecurity posture. These technologies allow organizations to automatically identify patterns of malicious activity and respond faster to evolving cyber threats

- For instance, Palo Alto Networks and Cisco offer AI-powered Intrusion Detection and Prevention Systems (IDPS) solutions integrated with cloud platforms that enable real-time monitoring and automated threat mitigation. Such solutions improve operational efficiency while reducing the burden on security teams by providing centralized threat intelligence and dynamic protection

- The deployment of machine learning algorithms in Intrusion Detection and Prevention Systems (IDPS) is gaining momentum as these systems can analyze massive volumes of network traffic and detect anomalies indicative of cyberattacks. This trend is positioning AI-driven Intrusion Detection and Prevention Systems (IDPS) as a crucial component for proactive cybersecurity frameworks in enterprises and critical infrastructures

- Cloud-based Intrusion Detection and Prevention Systems (IDPS) adoption is expanding across industries that require scalable and remote security management, enabling organizations to protect distributed networks without heavy on-premises infrastructure investments. The flexibility and rapid deployment of cloud solutions are driving accelerated integration in finance, healthcare, and government sectors

- Organizations are increasingly combining signature-based detection with behavioral analytics to improve the accuracy of intrusion prevention. This integrated approach helps reduce false positives, optimize security operations, and ensures that both known and unknown threats are addressed efficiently

- The market is witnessing growing interest in managed Intrusion Detection and Prevention Systems (IDPS) services where providers handle monitoring, threat analysis, and compliance, allowing enterprises to focus on core business operations. This trend highlights the evolving preference for comprehensive, outsourced cybersecurity solutions that deliver agility, scalability, and consistent threat protection

Intrusion Detection and Prevention Systems (IDPS) Market Dynamics

Driver

Rising Frequency and Sophistication of Cyberattacks

- The escalating number and complexity of cyberattacks are driving demand for advanced Intrusion Detection and Prevention Systems (IDPS) solutions capable of detecting and mitigating threats in real time. Organizations are seeking systems that can address both external attacks and insider threats to protect sensitive data and critical infrastructure

- For instance, IBM Security leverages its QRadar Intrusion Detection and Prevention Systems (IDPS) to detect sophisticated attack patterns and provide actionable insights for rapid response. Such deployments demonstrate how enterprises prioritize intelligent detection to counter increasingly sophisticated cyber adversaries

- The expansion of digital transformation initiatives and remote work has increased the attack surface, requiring more robust intrusion detection mechanisms. Intrusion Detection and Prevention Systems (IDPS) solutions are critical for ensuring secure connectivity, protecting cloud environments, and maintaining regulatory compliance across diverse IT landscapes

- High-profile ransomware, phishing, and zero-day attacks are compelling enterprises to adopt multi-layered defense strategies with Intrusion Detection and Prevention Systems (IDPS) at the core. These solutions help in early threat identification, reducing potential operational downtime and financial losses

- The rise in industrial IoT and connected systems is also driving the need for specialized Intrusion Detection and Prevention Systems (IDPS) that can monitor operational technology networks. Protecting these environments from cyberattacks ensures safety, continuity, and regulatory adherence, reinforcing the importance of advanced intrusion prevention technologies

Restraint/Challenge

High Implementation Costs and Integration Complexity

- The Intrusion Detection and Prevention Systems (IDPS) market faces challenges due to significant initial investment requirements for advanced hardware, software, and AI-driven components. Integrating these systems into existing IT infrastructures often demands specialized expertise and extensive configuration efforts

- For instance, implementing Fortinet’s FortiGate Intrusion Detection and Prevention Systems (IDPS) requires careful network mapping and integration with endpoint and cloud security tools to ensure comprehensive threat coverage. These complex setups increase deployment time and raise operational expenses for enterprises

- Organizations also encounter difficulties in managing large volumes of security alerts, requiring skilled personnel and sophisticated analytics platforms. The need to balance detection accuracy with operational efficiency adds to overall complexity

- Maintaining continuous updates and tuning to adapt to evolving threat landscapes increases the management burden on IT teams. Without proper maintenance, Intrusion Detection and Prevention Systems (IDPS) effectiveness can decline, reducing protection against new or sophisticated attack vectors

- The market continues to face constraints in ensuring interoperability with diverse network architectures, legacy systems, and third-party security solutions. These challenges collectively necessitate careful planning, significant investment, and ongoing management to maximize the value of Intrusion Detection and Prevention Systems (IDPS) deployments

Intrusion Detection and Prevention Systems (IDPS) Market Scope

The market is segmented on the basis of component, type, deployment type, organization size, and vertical.

- By Component

On the basis of component, the Intrusion Detection and Prevention Systems (IDPS) market is segmented into solutions and services. The solutions segment dominated the market with the largest revenue share in 2025, driven by the increasing need for advanced threat detection, real-time monitoring, and automated prevention capabilities. Organizations prioritize Intrusion Detection and Prevention Systems (IDPS) solutions to protect critical infrastructure and sensitive data against sophisticated cyberattacks and unauthorized intrusions. The demand is further fueled by the integration of AI and machine learning in solutions, enabling predictive threat analysis and faster response times. Comprehensive Intrusion Detection and Prevention Systems (IDPS) solutions also support compliance with stringent data security regulations across multiple industries, enhancing their adoption among enterprises.

The services segment is expected to witness the fastest growth from 2026 to 2033, propelled by rising demand for managed security services, consultancy, and deployment support. For instance, companies such as IBM provide IDPS-as-a-service, offering continuous monitoring, threat intelligence, and incident response support for organizations that lack in-house expertise. Organizations increasingly prefer outsourced services to reduce operational complexity and optimize cybersecurity budgets, driving the growth of the services segment.

- By Type

On the basis of type, the Intrusion Detection and Prevention Systems (IDPS) market is segmented into network-based, wireless-based, network behavior analysis (NBA), and host-based systems. The network-based segment dominated the market in 2025 due to its capability to monitor and secure entire networks in real-time, providing robust protection against external and internal attacks. Enterprises often deploy network-based Intrusion Detection and Prevention Systems (IDPS) to safeguard critical applications, data centers, and enterprise networks from malware, DDoS attacks, and unauthorized access. Its scalability, integration with firewalls, and compatibility with security information and event management (SIEM) systems further enhance adoption.

The NBA segment is anticipated to witness the fastest CAGR from 2026 to 2033, driven by advanced anomaly detection and behavioral analysis features that identify sophisticated, previously unknown threats. For instance, Cisco’s Stealthwatch uses network behavior analytics to detect suspicious patterns and mitigate threats proactively. Increasing cyberattack sophistication has prompted enterprises to adopt NBA Intrusion Detection and Prevention Systems (IDPS) solutions for predictive security measures, boosting market growth.

- By Deployment Type

On the basis of deployment type, the Intrusion Detection and Prevention Systems (IDPS) market is segmented into cloud and on-premises. The cloud segment dominated the market with the largest share of 58.3% in 2025 due to its scalability, flexibility, and ability to provide real-time monitoring and centralized threat management across distributed networks. Organizations preferred cloud-based Intrusion Detection and Prevention Systems (IDPS) for seamless updates, reduced infrastructure costs, and ease of integration with existing IT ecosystems.

The on-premises segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing demand for direct control over sensitive data, enhanced customization, and compliance with stringent regulatory requirements. Enterprises are adopting on-premises Intrusion Detection and Prevention Systems (IDPS) to ensure dedicated performance, advanced threat response, and secure handling of critical infrastructure.

- By Organization Size

On the basis of organization size, the Intrusion Detection and Prevention Systems (IDPS) market is segmented into SMEs and large enterprises. Large enterprises dominated the market in 2025 owing to their extensive IT infrastructure, high-value data assets, and need for advanced cybersecurity measures to prevent financial and reputational losses. Enterprises often deploy multi-layered Intrusion Detection and Prevention Systems (IDPS) solutions to secure multiple locations, cloud applications, and hybrid networks. Large-scale operations and compliance obligations drive continuous investment in sophisticated Intrusion Detection and Prevention Systems (IDPS) systems.

The SMEs segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing awareness of cybersecurity threats and the affordability of managed Intrusion Detection and Prevention Systems (IDPS) solutions. For instance, Fortinet provides SME-focused Intrusion Detection and Prevention Systems (IDPS) offerings that are easy to deploy and cost-effective while ensuring real-time threat detection. Rising cyberattacks targeting smaller businesses are prompting SMEs to adopt Intrusion Detection and Prevention Systems (IDPS) solutions rapidly.

- By Vertical

On the basis of vertical, the Intrusion Detection and Prevention Systems (IDPS) market is segmented into BFSI, government and defense, healthcare, IT and telecom, retail and eCommerce, manufacturing, and others. The BFSI vertical dominated the market in 2025 due to the critical need to protect sensitive financial data, prevent fraud, and comply with stringent financial regulations. Banks and financial institutions deploy Intrusion Detection and Prevention Systems (IDPS) to safeguard customer information, online transactions, and internal networks against increasingly sophisticated cyber threats. The sector also benefits from the integration of AI-driven threat intelligence and real-time monitoring for proactive defense.

The IT and telecom vertical is expected to witness the fastest growth from 2026 to 2033, fueled by the rapid expansion of digital services, cloud infrastructure, and data traffic. For instance, companies such as AT&T deploy advanced Intrusion Detection and Prevention Systems (IDPS) to secure networks, data centers, and communication channels from cyberattacks. Rising demand for secure connectivity, high-speed data protection, and remote access management accelerates adoption in this vertical.

Intrusion Detection and Prevention Systems (IDPS) Market Regional Analysis

- North America dominated the Intrusion Detection and Prevention Systems (IDPS) market with the largest revenue share of 38.8% in 2025, driven by increasing cybersecurity concerns, widespread digital transformation, and high adoption of cloud and enterprise IT infrastructure

- Organizations in the region highly prioritize real-time threat detection, automated prevention, and regulatory compliance, fostering the deployment of sophisticated Intrusion Detection and Prevention Systems (IDPS) solutions across industries

- This widespread adoption is supported by robust IT budgets, a technology-oriented workforce, and increasing cyberattack incidents, positioning Intrusion Detection and Prevention Systems (IDPS) as a critical component for both large enterprises and SMEs

U.S. Intrusion Detection and Prevention Systems (IDPS) Market Insight

The U.S. Intrusion Detection and Prevention Systems (IDPS) market captured the largest revenue share in 2025 within North America, fueled by the growing demand for advanced cybersecurity solutions across BFSI, healthcare, and IT sectors. Enterprises are increasingly investing in AI- and ML-powered Intrusion Detection and Prevention Systems (IDPS) for proactive threat detection and automated response. The rising frequency of ransomware and phishing attacks, combined with stringent data protection regulations such as HIPAA and CCPA, is accelerating market adoption. Moreover, the increasing integration of Intrusion Detection and Prevention Systems (IDPS) with cloud infrastructure and hybrid IT environments is further driving growth.

Europe Intrusion Detection and Prevention Systems (IDPS) Market Insight

Le marché européen des systèmes de détection et de prévention des intrusions (IDPS) devrait connaître une croissance annuelle composée (TCAC) importante au cours de la période de prévision, sous l'effet de la recrudescence des cybermenaces, du renforcement des réglementations en matière de protection des données telles que le RGPD et de l'augmentation des investissements dans les infrastructures informatiques. Les gouvernements et les entreprises déploient de plus en plus de systèmes IDPS pour protéger leurs données critiques et prévenir les violations de réseau. L'essor de la numérisation, des initiatives de villes intelligentes et de l'adoption du cloud dans des pays comme la France et l'Italie contribue à l'augmentation du déploiement des solutions IDPS. Les organisations de la région adoptent également des cadres de sécurité intégrés pour protéger leurs réseaux et se conformer aux normes de cybersécurité en constante évolution.

Analyse du marché britannique des systèmes de détection et de prévention des intrusions (IDPS)

Le marché britannique des systèmes de détection et de prévention des intrusions (IDPS) devrait connaître une croissance annuelle composée (TCAC) remarquable au cours de la période de prévision, portée par une sensibilisation accrue aux cybermenaces, aux exigences de conformité réglementaire et à l'adoption de solutions informatiques avancées. Les secteurs de la banque, de la finance et de l'assurance (BFSI), de la santé et du gouvernement sont à la pointe de la mise en œuvre des systèmes IDPS afin de garantir la protection des données et la sécurité des réseaux. Le développement des services cloud et des solutions de sécurité gérées encourage également les entreprises à déployer des systèmes IDPS évolutifs. L'accent mis sur la transformation numérique au sein des entreprises, associé à une approche proactive en matière de cybersécurité, continue de stimuler la croissance du marché.

Analyse du marché allemand des systèmes de détection et de prévention des intrusions (IDPS)

Le marché allemand des systèmes de détection et de prévention des intrusions (IDPS) devrait connaître une croissance annuelle composée (TCAC) importante au cours de la période de prévision, portée par la recrudescence des cyberattaques, un tissu industriel solide et une modernisation informatique croissante dans tous les secteurs. Les entreprises privilégient les solutions IDPS pour protéger leurs infrastructures critiques et leurs données industrielles sensibles. L'accent mis par l'Allemagne sur l'Industrie 4.0, conjugué aux exigences réglementaires en matière de sécurité des données, favorise le déploiement de solutions IDPS sur site et dans le cloud. Les organisations intègrent également l'intelligence artificielle pour le renseignement sur les menaces et l'analyse comportementale afin de renforcer la sécurité de leurs réseaux et de garantir leur conformité aux normes locales de cybersécurité.

Analyse du marché des systèmes de détection et de prévention des intrusions (IDPS) en Asie-Pacifique

Le marché des systèmes de détection et de prévention des intrusions (IDPS) en Asie-Pacifique devrait connaître la croissance annuelle composée la plus rapide entre 2026 et 2033, portée par la digitalisation rapide, l'urbanisation et l'augmentation des investissements en cybersécurité dans des pays comme la Chine, le Japon et l'Inde. La recrudescence des cyberattaques, conjuguée à l'expansion des infrastructures informatiques et de télécommunications, favorise l'adoption des solutions IDPS. Les gouvernements et les entreprises mettent en œuvre des mesures proactives de cybersécurité pour sécuriser leurs données critiques et leurs infrastructures cloud. La préférence croissante pour les services de sécurité gérés et les solutions IDPS abordables contribue à leur adoption par les PME et les grandes entreprises de la région.

Analyse du marché japonais des systèmes de détection et de prévention des intrusions (IDPS)

Le marché japonais des systèmes de détection et de prévention des intrusions (IDPS) connaît une forte croissance grâce à son écosystème de haute technologie, à l'adoption croissante du cloud et des solutions informatiques hybrides, et à l'importance accrue accordée à la sécurité des réseaux. Les entreprises déploient des systèmes IDPS pour détecter et atténuer en temps réel les cybermenaces sophistiquées. L'intégration des systèmes IDPS avec d'autres technologies de sécurité, telles que les solutions SIEM et la protection des terminaux, favorise leur adoption dans les secteurs de la banque, de la finance et de l'assurance (BFSI), de l'industrie et des technologies de l'information. L'accent mis par le Japon sur la cyber-résilience et l'essor des infrastructures intelligentes connectées devraient stimuler davantage la demande de solutions IDPS.

Analyse du marché chinois des systèmes de détection et de prévention des intrusions (IDPS)

Le marché chinois des systèmes de détection et de prévention des intrusions (IDPS) a généré la plus grande part de revenus en Asie-Pacifique en 2025, grâce à une numérisation rapide, à l'expansion des réseaux d'entreprise et à un fort taux d'adoption de la cybersécurité. Le pays connaît un déploiement croissant de systèmes IDPS dans les secteurs public, financier et commercial afin de contrer la multiplication des cybermenaces. Les fournisseurs chinois de solutions de sécurité informatique proposent des solutions évolutives et économiques, contribuant ainsi à la croissance du marché. Les initiatives gouvernementales en faveur de la sensibilisation à la cybersécurité et des infrastructures intelligentes sont des facteurs clés de la croissance du marché des systèmes IDPS en Chine.

Part de marché des systèmes de détection et de prévention des intrusions (IDPS)

Le secteur des systèmes de détection et de prévention des intrusions (IDPS) est principalement dominé par des entreprises bien établies, notamment :

- Cisco Systems Inc. (États-Unis)

- IBM (États-Unis)

- McAfee, LLC (États-Unis)

- Trend Micro Incorporated (Japon)

- Palo Alto Research Center Incorporated (États-Unis)

- Propriété intellectuelle d'AT&T (États-Unis)

- Darktrace (Royaume-Uni)

- FireEye, Inc. (États-Unis)

- Alert Logic, Inc. (États-Unis)

- Fortinet, Inc. (États-Unis)

- WatchGuard Technologies, Inc. (États-Unis)

- Vectra AI, Inc. (États-Unis)

- NSFOCUS (Chine)

- Armor Defense Inc. (États-Unis)

- BluVector (États-Unis)

- ExtraHop Networks (États-Unis)

- Réseaux Hilstone (États-Unis)

- SecureWorks, Inc. (États-Unis)

- Huawei Technologies Co., Ltd. (Chine)

- Bricata (États-Unis)

Dernières évolutions du marché mondial des systèmes de détection et de prévention des intrusions (IDPS)

- En avril 2025, Palo Alto Networks a finalisé l'acquisition des actifs SaaS d'IBM QRadar, renforçant considérablement ses capacités de corrélation des menaces et ses fonctionnalités de réponse automatisée. Cette initiative stratégique consolide la position de Palo Alto sur le marché des systèmes de détection et de prévention des intrusions (IDPS) en offrant une visibilité accrue sur les schémas d'attaque complexes, en améliorant la précision de la détection des incidents et en fournissant aux entreprises une atténuation des menaces plus rapide et plus efficace.

- En mars 2025, Google Cloud et Palo Alto Networks ont lancé un service conjoint de pare-feu et de système de prévention des intrusions (IDPS) conçu pour les déploiements informatiques hybrides. Cette collaboration élargit l'offre du marché en permettant aux entreprises de sécuriser leurs environnements sur site et cloud grâce à une protection intégrée, de rationaliser la gestion de la sécurité et de favoriser l'adoption de solutions IDPS hybrides au sein des entreprises dotées d'infrastructures informatiques complexes.

- En février 2025, T-Mobile a lancé une solution SASE (Secure Access Service Edge) gérée intégrant des fonctions de systèmes de détection et de prévention des intrusions (IDPS). Cette innovation a un impact sur le marché en offrant aux entreprises, notamment aux PME, des services de sécurité accessibles et fournis dans le cloud, combinant détection des menaces, prévention et contrôle d'accès au réseau. Elle accélère ainsi l'adoption des systèmes IDPS gérés et des solutions SASE sur le marché.

- En janvier 2025, Fortinet a acquis Lacework pour 4,5 milliards de dollars, intégrant ainsi l'analyse comportementale du cloud à son portefeuille de sécurité. Cette acquisition renforce l'avantage concurrentiel de Fortinet sur le marché des systèmes de détection et de prévention des intrusions (IDPS) en permettant une meilleure détection des activités anormales dans les environnements cloud, en améliorant la prévention proactive des menaces et en stimulant la demande de solutions IDPS natives du cloud auprès des entreprises en pleine transformation numérique.

- En décembre 2024, CrowdStrike s'est associé à Fortinet pour fusionner la visibilité des terminaux et du réseau, renforçant ainsi l'écosystème global de détection et de réponse aux menaces. Cette collaboration a un impact sur le marché des systèmes de détection et de prévention des intrusions (IDPS) en permettant une surveillance intégrée des terminaux et des réseaux, en améliorant les temps de réponse aux attaques complexes et en favorisant une plus grande adoption des solutions de sécurité combinées terminaux-réseau dans les déploiements à grande échelle en entreprise.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.