Global Osteoarthritic Pain Management Treatment Market

Taille du marché en milliards USD

TCAC :

%

USD

11.59 Billion

USD

20.28 Billion

2025

2033

USD

11.59 Billion

USD

20.28 Billion

2025

2033

| 2026 –2033 | |

| USD 11.59 Billion | |

| USD 20.28 Billion | |

| % | |

|

Global Osteoarthritic Pain Management Treatment Market Segmentation, By Type (Hip Osteoarthritis and Spinal Osteoarthritis), Drug (NSAIDs, Corticosteroids, Hyaluronic acid Injection, and Other Drugs), Diagnosis (Imaging and Joint Fluid Analysis), Treatment (Medication, Surgery, and Therapy), End Users (Hospitals and Medical Institutes)- Industry Trends and Forecast to 2033

Osteoarthritic Pain Management Treatment Market Size

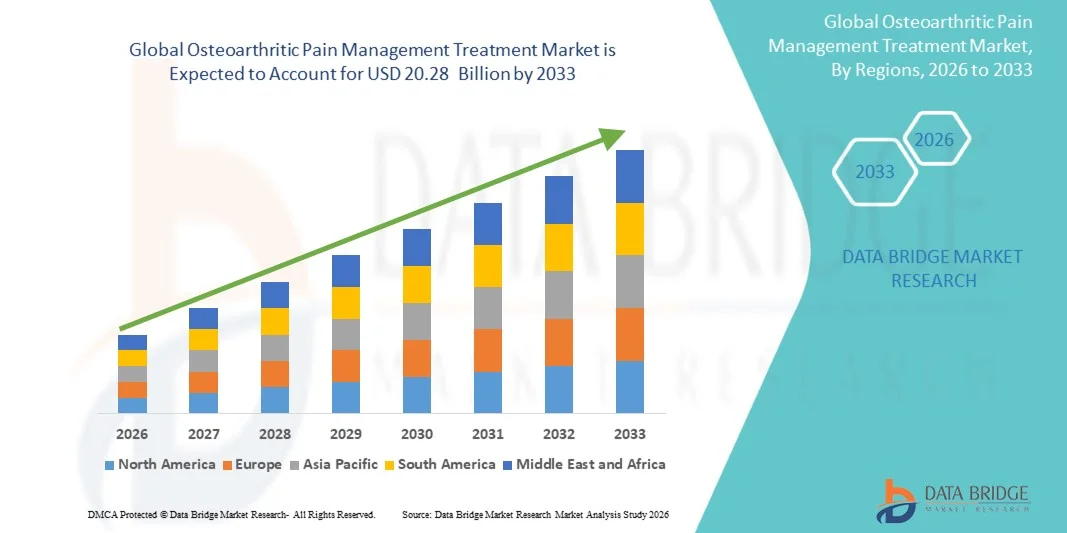

- The global osteoarthritic pain management treatment market size was valued at USD 11.59 billion in 2025 and is expected to reach USD 20.28 billion by 2033, at a CAGR of 7.25% during the forecast period

- The market growth is largely fueled by the rising prevalence of osteoarthritis, driven by aging demographics, increasing obesity rates, and lifestyle factors, which are expanding the patient pool and boosting demand for effective pain management therapies

- Furthermore, advancements in pain management therapies, improved disease awareness and diagnosis, and rising patient demand for safe, long‑term, and effective pain relief solutions across both hospital and homecare settings are positioning osteoarthritic pain treatments as essential components of musculoskeletal care, thereby accelerating adoption and significantly propelling industry growth

Osteoarthritic Pain Management Treatment Market Analysis

- Osteoarthritic pain management treatments, encompassing medications, surgeries, and therapy, are increasingly essential for improving mobility, reducing pain, and enhancing quality of life in patients suffering from osteoarthritis in both hospital and homecare settings due to their effectiveness, safety, and patient-centric approaches

- The escalating demand for osteoarthritic pain management solutions is primarily fueled by the rising prevalence of osteoarthritis, aging populations, increasing obesity rates, and growing awareness of advanced treatment options

- North America dominated the osteoarthritic pain management market with the largest revenue share of 40.5% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and strong presence of key market players, with the U.S. experiencing substantial adoption of pharmacological and minimally invasive therapies driven by innovation and patient-focused treatment programs

- Asia-Pacific is expected to be the fastest-growing region in the osteoarthritic pain management market during the forecast period due to increasing geriatric population, rising healthcare awareness, and improving access to advanced diagnostics and treatment solutions

- NSAIDs segment dominated the market with a share of 42.9% in 2025, driven by their proven efficacy in pain relief, wide availability, and strong physician preference, while other drugs such as corticosteroids and hyaluronic acid injections are witnessing rising adoption due to targeted therapeutic effects

Report Scope and Osteoarthritic Pain Management Treatment Market Segmentation

|

Attributes |

Osteoarthritic Pain Management Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Osteoarthritic Pain Management Treatment Market Trends

“Emergence of Targeted and Minimally Invasive Therapies”

- A significant and accelerating trend in the global osteoarthritic pain management market is the growing adoption of targeted drug therapies and minimally invasive procedures, which improve patient outcomes while reducing recovery times

- For instance, hyaluronic acid injections and corticosteroid-based localized therapies are increasingly being used to provide targeted pain relief and enhance joint function in hip and spinal osteoarthritis patients

- Advanced therapeutic approaches enable personalized treatment plans based on disease severity, patient comorbidities, and joint type, allowing physicians to optimize therapy effectiveness and reduce side effects

- Integration of wearable devices and remote monitoring tools supports real-time assessment of treatment efficacy, medication adherence, and mobility improvements, facilitating proactive patient care

- The trend of combining pharmacological treatments with physiotherapy and rehabilitation programs is gaining traction, offering holistic pain management and improved long-term outcomes

- This trend towards personalized, precise, and technology-assisted therapies is fundamentally reshaping clinical expectations and patient satisfaction, driving innovation in both pharmaceutical and device-based osteoarthritis treatments

- The demand for advanced, targeted, and minimally invasive osteoarthritic pain management solutions is growing rapidly across both hospital and homecare settings, as patients increasingly prioritize effectiveness, safety, and convenience

Osteoarthritic Pain Management Treatment Market Dynamics

Driver

“Rising Prevalence of Osteoarthritis and Aging Population”

- The increasing incidence of osteoarthritis, coupled with a growing elderly population, is a major driver for the heightened demand for pain management treatments

- For instance, the rising number of hip and spinal osteoarthritis cases globally has prompted healthcare providers to adopt advanced pharmacological and minimally invasive treatment protocols

- As patients experience chronic joint pain and mobility limitations, demand for effective and safe pain relief therapies continues to increase, boosting market growth

- In addition, growing awareness about osteoarthritis and early diagnosis through imaging and joint fluid analysis is expanding the patient pool and accelerating therapy adoption

- The availability of patient-centric treatment options, including NSAIDs, corticosteroids, and hyaluronic acid injections, along with therapy and surgical interventions, is further propelling market expansion

- Healthcare systems are increasingly investing in training, infrastructure, and telemedicine solutions to facilitate comprehensive osteoarthritic pain management across outpatient and homecare settings

- Rising research and development efforts by pharmaceutical companies to introduce safer, longer-acting, and targeted therapies are creating new growth avenues in the market

- Public and private initiatives promoting awareness about lifestyle modifications, physiotherapy, and preventive care are further driving adoption of osteoarthritic pain management strategies

Restraint/Challenge

“Side Effects, High Costs, and Regulatory Hurdles”

- Concerns regarding drug-related side effects and complications from surgical or invasive procedures pose significant challenges to wider market adoption

- For instance, long-term use of NSAIDs may lead to gastrointestinal issues, while corticosteroid injections require careful monitoring to avoid joint damage or systemic effects

- High costs of advanced biologics, minimally invasive surgeries, and therapy programs can limit access, particularly in developing regions or among price-sensitive patients

- In addition, regulatory approvals for new drugs and devices, along with stringent safety standards, can delay market entry and increase development timelines for innovative therapies

- Perceived risks and costs may hinder patients from adopting certain advanced treatments despite clinical efficacy, affecting overall market penetration

- Overcoming these challenges through patient education, safer drug formulations, cost-effective therapies, and streamlined regulatory compliance will be crucial for sustained growth in the osteoarthritic pain management market

- Limited availability of specialized healthcare professionals and rehabilitation centers in certain regions can constrain patient access to comprehensive pain management solutions

- Patient reluctance toward invasive procedures or frequent injections may further restrict market growth, emphasizing the need for less invasive and more convenient treatment options

Osteoarthritic Pain Management Treatment Market Scope

The market is segmented on the basis of type, drug, diagnosis, treatment, and end users.

- By Type

On the basis of type, the osteoarthritic pain management market is segmented into hip osteoarthritis and spinal osteoarthritis. The hip osteoarthritis segment dominated the market in 2025, owing to its higher prevalence among aging populations and the significant impact on mobility and quality of life. Patients with hip osteoarthritis often require a combination of pharmacological treatment, minimally invasive injections, and surgical interventions, contributing to higher market revenues. The segment also benefits from ongoing clinical research and the availability of advanced hip-specific therapies such as hip injections and joint replacement procedures. In addition, physicians prioritize early intervention in hip osteoarthritis to prevent severe degeneration, driving adoption of both medication and therapy-based management. Hip osteoarthritis management also sees substantial insurance coverage, particularly in developed regions, further supporting its dominance.

The spinal osteoarthritis segment is expected to witness the fastest growth rate from 2026 to 2033 due to increasing awareness and diagnosis of spinal joint degeneration, particularly among the elderly and sedentary populations. Spinal osteoarthritis often requires multidisciplinary treatment approaches including NSAIDs, corticosteroid injections, and physical therapy, which is expanding the treatment market. Advances in imaging technologies and minimally invasive spinal procedures are facilitating better outcomes and higher adoption rates. Rising prevalence of back pain and spinal degeneration in urban populations is creating significant growth opportunities. Moreover, the increasing focus on rehabilitation and non-surgical management is attracting patients seeking safe and effective spinal pain management solutions.

- By Drug

On the basis of drug, the market is segmented into NSAIDs, corticosteroids, hyaluronic acid injections, and other drugs. The NSAIDs segment dominated the market in 2025 with a market share of 42.9%, driven by their widespread availability, cost-effectiveness, and proven efficacy in managing pain and inflammation in osteoarthritis patients. Physicians often prescribe NSAIDs as the first-line treatment for both hip and spinal osteoarthritis due to their rapid symptomatic relief. The segment benefits from strong patient familiarity and trust, as NSAIDs have been used for decades to manage musculoskeletal pain. In addition, NSAIDs are available in oral, topical, and combination formulations, increasing patient compliance and treatment flexibility. Their dominance is further reinforced by strong inclusion in treatment guidelines by rheumatology and orthopedic associations.

The hyaluronic acid injection segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by its targeted mechanism for joint lubrication and cartilage support. Hyaluronic acid injections provide longer-lasting relief and are increasingly preferred among patients seeking alternatives to oral medications. Technological advancements in injection techniques and formulations have improved patient comfort and treatment efficacy. Growing awareness among orthopedic surgeons and patients about injectable therapies is driving adoption, particularly in developed markets. The segment is further supported by favorable reimbursement policies and the increasing trend toward minimally invasive interventions.

- By Diagnosis

On the basis of diagnosis, the market is segmented into imaging and joint fluid analysis. The imaging segment dominated the market in 2025, due to its critical role in accurately diagnosing osteoarthritis severity, monitoring disease progression, and guiding treatment decisions. Imaging techniques such as X-rays, MRI, and CT scans provide detailed information about cartilage degeneration, bone spurs, and joint space narrowing. Physicians rely on imaging to personalize treatment plans, select appropriate pharmacological or surgical interventions, and monitor therapy effectiveness. The segment’s dominance is supported by technological advancements in high-resolution imaging and the increasing availability of imaging equipment in hospitals and diagnostic centers.

The joint fluid analysis segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to provide precise biochemical insights into joint inflammation and cartilage degradation. Analysis of synovial fluid helps in early diagnosis and differentiation from other musculoskeletal conditions, enabling targeted treatment approaches. Rising adoption of minimally invasive sampling techniques and laboratory advancements are facilitating broader use of joint fluid diagnostics. Increasing awareness among clinicians regarding personalized therapy selection is also contributing to growth. In addition, joint fluid analysis supports the use of advanced injectable therapies such as corticosteroids and hyaluronic acid, creating a synergistic market opportunity.

- By Treatment

On the basis of treatment, the market is segmented into medication, surgery, and therapy. The medication segment dominated the market in 2025, owing to its ease of administration, affordability, and rapid pain relief capabilities. Medication-based management, including NSAIDs, corticosteroids, and other drugs, forms the cornerstone of osteoarthritis treatment in both early and moderate stages. The segment benefits from patient familiarity, guideline recommendations, and strong physician preference. High adoption is seen across hospitals, outpatient clinics, and homecare settings due to convenience and minimal procedural requirements. Medication also allows combination therapy with physical therapy or rehabilitation programs, enhancing patient outcomes. The dominance is further supported by continuous development of new oral and topical formulations, including sustained-release options.

The therapy segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for non-invasive pain management and rehabilitation programs. Physical therapy, occupational therapy, and exercise-based interventions improve joint function, reduce pain, and complement pharmacological treatments. Rising awareness about holistic and preventive care, coupled with growing insurance coverage for therapy services, is boosting adoption. Technological integration such as tele-rehabilitation platforms and wearable motion tracking devices is expanding access and patient adherence. Furthermore, therapy-focused interventions are increasingly recommended for elderly patients and those contraindicated for surgery or aggressive pharmacological regimens.

- By End Users

On the basis of end users, the market is segmented into hospitals and medical institutes. The hospitals segment dominated the market in 2025, driven by the high patient inflow, access to advanced treatment facilities, and availability of multidisciplinary care teams. Hospitals provide comprehensive osteoarthritic pain management services including imaging, medication administration, minimally invasive procedures, therapy, and surgery. Their dominance is supported by strong insurance partnerships and established referral networks. Hospitals also lead in adoption of new technologies and advanced drug therapies, enhancing patient outcomes and market revenues.

The medical institutes segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increased emphasis on outpatient care, preventive programs, and research-driven therapies. Medical institutes often specialize in early diagnosis, advanced drug trials, and therapy-focused management, providing patients with innovative care options. Rising collaborations with pharmaceutical companies for clinical research and adoption of telemedicine solutions are further enhancing growth. Medical institutes also cater to patients seeking personalized and less invasive treatment approaches, which is driving adoption of minimally invasive injections and therapy programs. In addition, education and awareness programs run by medical institutes are expanding patient outreach and treatment engagement.

Osteoarthritic Pain Management Treatment Market Regional Analysis

- North America dominated the osteoarthritic pain management market with the largest revenue share of 40.5% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and strong presence of key market players

- Patients and healthcare providers in the region highly value advanced treatment options, including targeted drug therapies, minimally invasive injections, and comprehensive rehabilitation programs, which improve mobility and quality of life

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare spending, strong insurance coverage, and the presence of key pharmaceutical and medical device players, establishing osteoarthritic pain management solutions as a preferred choice for both hospital and outpatient care settings

U.S. Osteoarthritic Pain Management Treatment Market Insight

The U.S. osteoarthritic pain management market captured the largest revenue share of 40% in 2025 within North America, fueled by the rising prevalence of osteoarthritis and an aging population. Patients increasingly prioritize advanced therapies such as targeted drug treatments, minimally invasive injections, and rehabilitation programs to improve mobility and quality of life. The growing preference for outpatient care, telemedicine consultations, and personalized treatment plans further propels the market. Moreover, the increasing integration of advanced imaging, wearable monitoring devices, and therapy platforms is significantly contributing to the market's expansion.

Europe Osteoarthritic Pain Management Market Insight

The Europe osteoarthritic pain management market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by high awareness of musculoskeletal disorders and established healthcare infrastructure. Increasing urbanization, coupled with rising demand for early diagnosis and effective treatment, is fostering adoption of both pharmacological and non-pharmacological therapies. European patients are also drawn to integrated pain management solutions that combine medication, therapy, and minimally invasive interventions. The region is experiencing growth across hospital, outpatient, and rehabilitation settings, with treatments incorporated into both new and ongoing care programs.

U.K. Osteoarthritic Pain Management Market Insight

The U.K. osteoarthritic pain management market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of osteoarthritis and a strong focus on preventive care. In addition, increasing prevalence of joint disorders and patient preference for minimally invasive procedures and therapy programs are encouraging healthcare providers to offer comprehensive pain management solutions. The U.K.’s adoption of digital health platforms and tele-rehabilitation, alongside robust healthcare infrastructure, is expected to continue stimulating market growth.

Germany Osteoarthritic Pain Management Market Insight

The Germany osteoarthritic pain management market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s strong focus on research, early diagnosis, and advanced treatment adoption. Germany’s well-developed healthcare system, coupled with high patient awareness and emphasis on innovative, technology-driven therapies, promotes the adoption of pharmacological and non-pharmacological treatments. The integration of therapies with homecare monitoring, wearable devices, and rehabilitation programs is also becoming increasingly prevalent, supporting sustained market growth.

Asia-Pacific Osteoarthritic Pain Management Market Insight

The Asia-Pacific osteoarthritic pain management market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing geriatric populations, rising prevalence of osteoarthritis, and improving healthcare infrastructure in countries such as China, Japan, and India. The region’s growing awareness of effective pain management treatments, combined with telemedicine services and physiotherapy adoption, is driving market growth. Furthermore, as APAC emerges as a hub for affordable pharmaceutical therapies and minimally invasive procedures, accessibility of osteoarthritis care is expanding to a wider patient base.

Japan Osteoarthritic Pain Management Market Insight

The Japan market is gaining momentum due to rapid aging, high healthcare standards, and increasing demand for minimally invasive therapies and rehabilitation programs. Japanese patients place a strong emphasis on treatment efficacy, safety, and improved mobility, leading to adoption of targeted drug therapies, hyaluronic acid injections, and therapy-based interventions. Integration with digital health platforms, wearable monitoring devices, and outpatient care solutions is fueling growth. The aging population is likely to further increase demand for easier-to-use, effective pain management solutions in both hospital and homecare settings.

India Osteoarthritic Pain Management Market Insight

The India osteoarthritic pain management market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rising osteoarthritis prevalence, rapid urbanization, and increasing awareness of advanced therapies. India represents one of the largest emerging markets for pain management, with growing adoption of medication, injections, and physiotherapy across hospital and outpatient settings. Initiatives promoting preventive care, telemedicine, and affordable treatment options are key factors propelling market growth. In addition, the presence of domestic pharmaceutical manufacturers and expanding healthcare infrastructure supports widespread accessibility and adoption.

Osteoarthritic Pain Management Treatment Market Share

The Osteoarthritic Pain Management Treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- GSK plc (U.K.)

- Sanofi (France)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Zimmer Biomet. (U.S.)

- Stryker (U.S.)

- Anika Therapeutics, Inc. (U.S.)

- Bioventus Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Fidia Farmaceutici S.p.A. (Italy)

- ABIOGEN PHARMA S.p.A (Italy)

- Ferring B.V. (Switzerland)

- Pacira BioSciences, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

What are the Recent Developments in Global Osteoarthritic Pain Management Treatment Market?

- In October 2025, low‑dose radiotherapy was reported at the American Society for Radiation Oncology meeting to safely ease pain and improve function in patients with mild‑to‑moderate osteoarthritis, suggesting a non‑drug, non‑surgical approach to managing symptomatic OA pain

- In September 2025, researchers developed an experimental neuron‑derived “pain sponge” therapy in preclinical models that absorbs inflammatory pain signals before reaching the brain, showing promise as a novel biological approach to chronic pain relief in osteoarthritis

- In July 2025, Genascence announced that the U.S. Food and Drug Administration (FDA) granted Regenerative Medicine Advanced Therapy (RMAT) designation to GNSC‑001, a novel gene therapy for knee osteoarthritis, potentially accelerating development and enabling earlier access for patients suffering long‑term joint pain and inflammation

- In May 2025, Genascence reported positive 12‑month Phase 1b clinical trial results for GNSC‑001, demonstrating sustained safety, tolerability, and IL‑1 receptor antagonist expression an important step toward a potential disease‑modifying therapy for osteoarthritis pain

- In April 2025, an international research collaboration involving scientists from Australia and Germany revealed over 500 previously unknown genetic links to osteoarthritis, significantly expanding potential therapeutic targets and laying groundwork for future drug development beyond symptom management

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.