Global Photodiode Sensors Market

Taille du marché en milliards USD

TCAC :

%

USD

1.45 Billion

USD

2.54 Billion

2025

2033

USD

1.45 Billion

USD

2.54 Billion

2025

2033

| 2026 –2033 | |

| USD 1.45 Billion | |

| USD 2.54 Billion | |

| % | |

|

Segmentation du marché mondial des capteurs à photodiodes, par type de photodiode (photodiode PN, photodiode PIN, photodiode à avalanche et photodiode Schottky), longueur d'onde (spectre ultraviolet (UV), spectre visible, spectre proche infrarouge (NIR) et spectre infrarouge (IR)), secteur d'utilisation finale (télécommunications, santé, électronique grand public, aérospatiale et défense, et autres) - Tendances et prévisions du marché jusqu'en 2033

Taille du marché

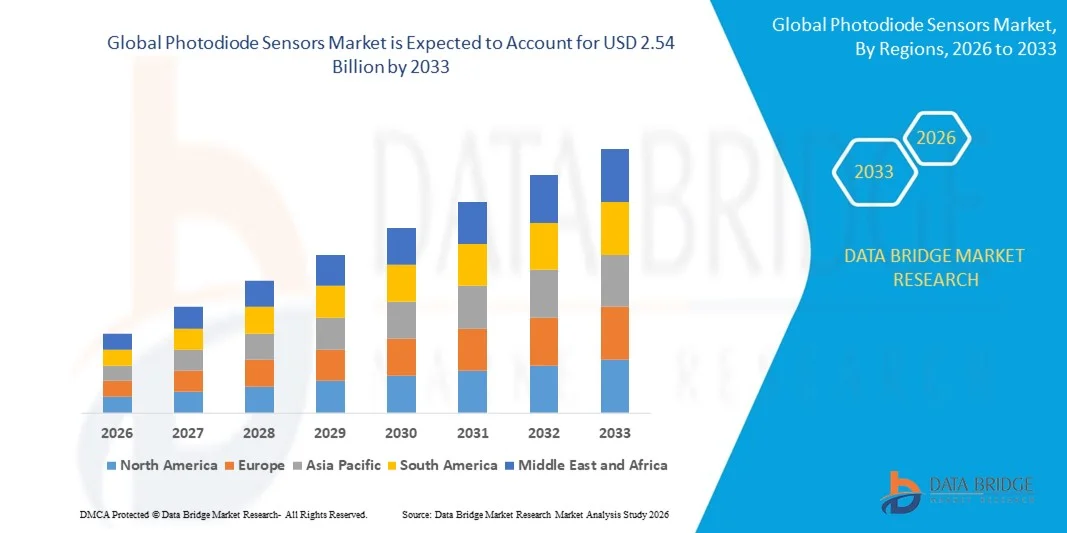

- Selon l'analyse de marché de Data Bridge, la taille du marché des capteurs de photodiode globale a été évaluée à1,45 milliard de dollars en 2025et devrait atteindre2,54 milliards de dollars en 2033, à unTCAC de 7,20 %pendant la période de prévision

- La croissance du marché est largement alimentée par l'expansion rapide des réseaux de communication à fibre optique, le déploiement croissant de systèmes de transmission de données à grande vitesse et les progrès continus dans les technologies optoélectroniques, conduisant à une meilleure intégration des capteurs photodiodes dans les télécommunications, l'automatisation industrielle et les applications de soins de santé

- En outre, la demande croissante de détection de lumière à haute sensibilité dans des applications telles queLIDAR, imagerie médicale, la surveillance de l'environnement et l'électronique grand public placent les capteurs photodiodes comme composants essentiels dans les systèmes de détection de la prochaine génération. Ces facteurs convergents accélèrent l'innovation technologique et le déploiement à grande échelle, ce qui stimule considérablement la croissance du marché des capteurs photodiodes

Taille du marché et prévisions

- Valeur marchande mondiale (2025):1,45 milliard de dollars

- Valeur marchande prévue (2033) :2,54 milliards de dollars

- Prévisions CAGR (2026-2033):7.20%

Analyse du marché des capteurs photodiodes

- Les capteurs photodiodes, qui convertissent la lumière en signaux électriques pour une détection optique précise, sont des composants de plus en plus essentiels dans les systèmes de communication modernes, les dispositifs de diagnostic médical, les technologies de sécurité automobile et l'automatisation industrielle en raison de leur grande sensibilité, leur temps de réponse rapide, leur taille compacte et leur efficacité énergétique

- La demande croissante de capteurs photodiode est principalement alimentée par l'expansion de l'infrastructure 5G, l'adoption croissante de systèmes avancés d'assistance au conducteur et de technologies LiDAR, l'utilisation croissante d'équipements de surveillance médicale non invasifs et l'intégration croissante de solutions de détection optique dans les systèmes de détection de l'ozone.fabrication intelligenteet électronique grand public

- L'Amérique du Nord a dominé le marché des capteurs de photodiodes avec une part de46,01 % en 2025, en raison de la forte demande dans les secteurs de la communication optique, de l'aérospatiale et de la défense, et du diagnostic avancé des soins de santé

- L'Asie-Pacifique devrait être la région qui connaît la croissance la plus rapide du marché des capteurs de photodiodes au cours de la période de prévision en raison de l'urbanisation rapide, de l'expansion de l'infrastructure des télécommunications et de la forte capacité de fabrication de semi-conducteurs dans des pays comme la Chine, le Japon et la Corée du Sud.

- Le segment photodiode PIN a dominé le marché avec une part de marché de 41,92 % en 2025, en raison de sa sensibilité supérieure, de son temps de réponse rapide et de sa faible performance sonore par rapport aux photodiodes PN standard. Sa vaste région d'épuisement améliore l'efficacité d'absorption de la lumière, la rendant très adaptée aux systèmes de communication optique, aux instruments médicaux et aux applications de détection industrielle. La forte adoption de réseaux à fibre optique et de systèmes de transmission de données à grande vitesse soutient la demande de photodiodes PIN

Report Scope and Photodiode Sensors Market Segmentation

|

Attributs |

Capteurs de photodiodes Principales perspectives du marché |

|

Segments couverts |

|

|

Pays couverts |

Amérique du Nord

Europe

Asie-Pacifique

Moyen-Orient et Afrique

Amérique du Sud

|

|

Principaux acteurs du marché |

|

|

Possibilités de marché |

|

|

Infos sur la valeur ajoutée |

Outre les informations sur les scénarios du marché, tels que la valeur du marché, le taux de croissance, la segmentation, la couverture géographique et les principaux acteurs, les rapports de marché établis par Data Bridge Market Research comprennent également une analyse approfondie des experts, une production et une capacité géographiquement représentées par l'entreprise, des schémas de réseau des distributeurs et des partenaires, une analyse détaillée et actualisée des tendances des prix et une analyse du déficit de la chaîne d'approvisionnement et de la demande. |

Tendances du marché des capteurs de photodiode

Intégration accrue des capteurs photodiode dans les applications de détection LiDAR et 3D

- Une tendance significative sur le marché des capteurs photodiode est l'intégration croissante des technologies photodiode dans le LiDAR et les systèmes de détection 3D avancés, stimulés par une demande croissante de détection précise de profondeur et de cartographie en temps réel de l'environnement dans les secteurs automobile et industriel. Cette intégration renforce le rôle des photodiodes en tant que composants essentiels des architectures de détection de la prochaine génération

- Par exemple, Sony Semiconductor Solutions a introduit son capteur de profondeur SPAD empilé IMX479 pour les applications LiDAR automobiles, permettant une détection à longue portée et une efficacité photonique accrue. Ces développements améliorent la précision de la reconnaissance des objets et soutiennent des capacités de conduite autonomes plus sûres

- L'adoption de photodiodes d'avalanche et de tableaux SPAD dans les systèmes avancés d'assistance au conducteur se développe car ces capteurs fournissent une sensibilité élevée et un temps de réponse rapide dans des conditions de faible luminosité. Il s'agit de positionner les capteurs photodiodes comme des moteurs critiques de systèmes de perception fiables sur des plateformes de mobilité intelligentes

- L'automatisation industrielle utilise de plus en plus les capteurs de temps de vol basés sur la photodiode pour permettre une cartographie 3D précise et la navigation robotique dans les environnements de fabrication. Cette tendance soutient le passage à des usines intelligentes qui dépendent de systèmes de détection optique stables et à grande vitesse

- Les appareils d'imagerie et de diagnostic des soins de santé intègrent des réseaux compacts de photodiodes pour améliorer la détection des signaux optiques et améliorer la précision de l'imagerie. Cette intégration accélère les progrès dans les systèmes de diagnostic non invasifs qui nécessitent des composants de détection de lumière de haute performance

- Le marché connaît une innovation soutenue dans les modules LiDAR à l'état solide et de détection de profondeur où les photodiodes forment la base de la réception et de la conversion des signaux. Cette intégration croissante dans les applications de l'automobile, de la robotique et de l'imagerie renforce la transition vers des écosystèmes de détection intelligents fondés sur des technologies photodiode à haute efficacité

Dynamique du marché des capteurs photodiodes

Chauffeur

Extension rapide de l'infrastructure de communication Fibre Optic

- L'expansion rapide des réseaux de communication à fibre optique dans l'ensemble de l'infrastructure mondiale de télécommunications entraîne une forte demande de capteurs photodiodes qui convertissent les signaux optiques en signaux électriques avec une grande précision et vitesse. Ces composants sont essentiels au maintien de l'intégrité du signal et à la transmission de données à large bande

- Par exemple, Hamamatsu Photonics fournit des photodiodes PIN à haute vitesse largement utilisées dans les récepteurs optiques pour les systèmes de communication à fibre optique. Ces dispositifs permettent une détection précise de la lumière et des performances stables sur les réseaux de transmission de données à longue distance

- Le déploiement de réseaux 5G et de centres de données hyperscales accroît le besoin de photodiodes à haute sensibilité capables de traiter des taux de données plus rapides et des exigences de latence plus faibles. Cela renforce le rôle des capteurs photodiode dans le soutien des infrastructures de communication de la prochaine génération

- Les opérateurs de télécommunications investissent massivement dans les émetteurs-récepteurs et les modules récepteurs qui dépendent de composants photodiodes fiables pour la conversion du signal. Cet investissement accélère les volumes de production et le raffinement technologique sur le marché de la photodiode

- L'expansion mondiale continue de l'accès à large bande et des services basés sur le cloud renforce ce moteur de croissance. La nécessité de récepteurs optiques plus rapides, plus économes en énergie et à haute précision continue d'influer sur le progrès technologique et l'expansion à long terme du marché

Restriction/Défi

Complexité manufacturière élevée et coût des technologies avancées de photodiode

- Le marché des capteurs de photodiodes est confronté à des défis en raison des processus de fabrication complexes nécessaires pour produire des photodiodes haute performance, en particulier des photodiodes d'avalanche et des tableaux SPAD qui exigent une ingénierie de semi-conducteurs de précision. Ces processus comportent des matériaux spécialisés, un traitement avancé des déchets et des contrôles environnementaux stricts, ce qui augmente les coûts de production globaux

- Par exemple, OSRAM Opto Semiconductors GmbH utilise des techniques avancées de fabrication de semi-conducteurs composés pour fabriquer des photodiodes à haute sensibilité pour l'automobile et l'industrie. Des exigences de production aussi complexes augmentent les investissements et les dépenses de fonctionnement des fabricants

- La fabrication de photodiodes avancées nécessite des normes de contrôle de qualité rigoureuses pour assurer un faible bruit, une efficacité quantique élevée et une stabilité à long terme dans des conditions d'exploitation exigeantes. Ces exigences prolongent les cycles de développement et augmentent les coûts d'essai et de validation

- La dépendance à l'égard des matériaux semi-conducteurs composés et des technologies d'emballage spécialisées introduit la complexité de la chaîne d'approvisionnement et la variabilité des coûts. Maintenir un rendement uniforme tout en gérant les dépenses matérielles pose des défis permanents aux producteurs

- Ces facteurs combinés exercent une pression sur les participants de l'industrie pour qu'ils optimisent l'efficacité de la fabrication et réduisent les structures de coûts tout en maintenant des normes de performance élevées. La nécessité d'équilibrer l'innovation et la faisabilité économique continue de façonner la dynamique concurrentielle au sein du marché des capteurs photodiode

Portée du marché des capteurs de photodiode

Le marché est segmenté en fonction du type de photodiode, de la longueur d'onde et de l'utilisation finale.

- Par type de photodiode

Sur la base du type photodiode, le marché des capteurs de photodiode est segmenté en photodiode PN, photodiode PIN, photodiode avalanche et photodiode Schottky. Le segment photodiode PIN a dominé le marché avec la plus grande part de chiffre d'affaires de 41,92 % en 2025, grâce à sa sensibilité supérieure, son temps de réponse rapide et sa faible performance sonore par rapport aux photodiodes PN standard. Sa vaste région d'épuisement améliore l'efficacité d'absorption de la lumière, la rendant très adaptée aux systèmes de communication optique, aux instruments médicaux et aux applications de détection industrielle. La forte adoption de réseaux à fibre optique et de systèmes de transmission de données à grande vitesse soutient la demande de photodiodes PIN. En outre, leur rentabilité et leur stabilité opérationnelle dans diverses conditions environnementales renforcent leur position dans les déploiements commerciaux et industriels.

Le segment de photodiode d'avalanche devrait connaître le taux de croissance le plus rapide de 2026 à 2033, alimenté par l'augmentation de la demande de détection à haut gain et à haut niveau de sensibilité dans les environnements à faible luminosité. Les photodiodes d'avalanche fournissent une amplification du signal interne par ionisation d'impact, permettant une détection précise dans la communication optique longue distance, les systèmes LiDAR et les applications de défense avancées. Le déploiement croissant de systèmes autonomes et de technologies avancées d'assistance au conducteur accélère leur intégration dans les modules de détection. Leur capacité à détecter des signaux optiques faibles avec un meilleur rapport signal-bruit les rend très attrayants pour les solutions photoniques et d'imagerie de nouvelle génération.

- Par longueur d'onde

Sur la base de la longueur d'onde, le marché des capteurs photodiodes est segmenté en spectre ultraviolet (UV), spectre visible, spectre proche infrarouge (NIR) et spectre infrarouge (IR). Le segment du spectre proche infrarouge (NIR) a dominé le marché en 2025, en raison de son utilisation étendue dans les systèmes de communication à fibre optique, de surveillance biomédicale et d'automatisation industrielle. Les photodiodes NIR offrent une pénétration des matériaux plus profonde et des performances stables, ce qui les rend adaptées aux diagnostics médicaux non invasifs et aux applications de détection de proximité. L'expansion de l'infrastructure Internet à haut débit et des centres de données contribue de façon significative à la demande soutenue de capteurs photodiode basés sur le NIR. En outre, leur compatibilité avec les technologies de détecteurs à base de silicium améliore l'évolutivité de la fabrication et leur rentabilité.

On prévoit que le segment du spectre infrarouge (IR) connaîtra la croissance la plus rapide de 2026 à 2033, grâce à l'adoption croissante d'applications d'imagerie thermique, de détection des mouvements et de télédétection. Les photodiodes IR sont largement utilisées dans les systèmes de sécurité, la surveillance environnementale et les technologies aérospatiales en raison de leur capacité à détecter les signatures thermiques et à fonctionner dans des conditions de faible visibilité. Les investissements croissants dans les systèmes de surveillance intelligente et les solutions de sécurité industrielle propulsent la demande. Leur rôle croissant dans la détection automobile et les systèmes d'imagerie de défense renforce les perspectives de croissance à long terme.

- Par industrie d'utilisation finale

Sur la base de l'industrie de l'utilisation finale, le marché des capteurs photodiodes est segmenté en télécommunications, soins de santé, électronique grand public, aérospatiale et défense, et autres. Le segment des télécommunications a dominé le marché avec la plus grande part des revenus en 2025, grâce à l'expansion rapide des réseaux de fibre optique et à l'augmentation du trafic de données. Les photodiodes jouent un rôle critique dans les récepteurs optiques, convertissant les signaux lumineux en signaux électriques avec une précision et une vitesse élevées. Le déploiement continu de l'infrastructure 5G et des solutions d'interconnexion de datacenter soutient considérablement la demande. En outre, la nécessité de systèmes de communication à large bande fiables renforce la domination de ce segment.

Le secteur des soins de santé devrait connaître le taux de croissance le plus rapide de 2026 à 2033, alimenté par l'adoption croissante de capteurs à base de photodiodes dans l'imagerie médicale, l'oxymétrie des impulsions et l'équipement de diagnostic. Les photodiodes permettent une détection précise de la lumière dans les dispositifs de surveillance non invasifs, ce qui favorise l'analyse en temps réel des données du patient. La demande croissante de dispositifs médicaux portables accélère l'intégration de capteurs photodiode compacts et économes en énergie. Les progrès technologiques de l'optique biomédicale et l'accent croissant mis sur les soins de santé préventifs favorisent l'expansion du segment.

Analyse régionale du marché des capteurs photodiodes

- L'Amérique du Nord a dominé le marché des détecteurs de photodiodes avec la plus grande part de revenus de 46,01 % en 2025, sous l'impulsion d'une forte demande dans les secteurs de la communication optique, de l'aérospatiale et de la défense, et des diagnostics de santé avancés

- La région bénéficie du déploiement rapide de réseaux de fibre optique, d'un investissement important dans les activités de R-D et de l'adoption rapide de technologies de détection avancées pour les applications industrielles et commerciales

- Cette adoption généralisée est soutenue par la présence de fabricants de semi-conducteurs de premier plan, d'une infrastructure de data center robuste et d'une innovation continue dans les systèmes LiDAR, d'imagerie médicale et d'automatisation, en établissant des capteurs photodiodes comme composants essentiels dans les systèmes électroniques à haute performance.

Senseurs de photodiodes américains

En 2025, le marché américain des capteurs photodiode a enregistré la plus grande part de revenus en Amérique du Nord, alimentée par l'expansion des réseaux de communication à grande vitesse et de solides programmes de modernisation de la défense. L'augmentation des investissements dans l'infrastructure 5G et les centres de données accélère la demande de détecteurs optiques à haute sensibilité. L'intégration croissante des photodiodes dans les dispositifs médicaux, les véhicules autonomes et les systèmes d'automatisation industrielle favorise la croissance du marché. En outre, les progrès technologiques dans la fabrication de semi-conducteurs et l'optoélectronique renforcent les capacités de production nationales et le leadership de l'innovation.

Europe Photodiode Senseurs Aperçu du marché

Le marché européen des capteurs photodiode devrait s'étendre à un important TCAC tout au long de la période de prévision, principalement en raison de l'accent accru mis sur l'automatisation industrielle, les systèmes d'énergie renouvelable et les technologies automobiles de pointe. L'adoption croissante de la détection optique dans les solutions de fabrication et de mobilité intelligente favorise la croissance régionale. Les industries européennes mettent l'accent sur la précision, l'efficacité énergétique et la conformité à la réglementation, qui soutient le déploiement de systèmes de détection fiables basés sur la photodiode. La croissance est évidente dans les secteurs des télécommunications, de l'aérospatiale et de la fabrication d'appareils médicaux.

U.K. Capteurs photodiode Aperçu du marché

Le marché des capteurs photodiodes au Royaume-Uni devrait croître à un TCAC remarquable au cours de la période de prévision, en raison de l'augmentation des investissements dans les établissements de recherche, les technologies de santé et les systèmes de communication de la prochaine génération. Le pays encourage l'innovation dans les composants optoélectroniques. L'adoption croissante de capteurs optiques dans les applications biomédicales et la surveillance de l'environnement stimule la demande. L'accent de plus en plus mis sur l'infrastructure numérique et la connectivité à grande vitesse continue d'appuyer l'expansion du marché.

Allemagne Photodiode Sensors Market Insight

Le marché allemand des capteurs photodiodes devrait s'étendre à un TCAC considérable pendant la période de prévision, alimenté par la forte base industrielle du pays et le leadership dans l'ingénierie automobile. L'intégration de capteurs photodiodes dans les systèmes avancés d'assistance au conducteur, la robotique industrielle et les équipements de fabrication de précision contribue grandement à la demande. Allemagne L'accent mis sur l'industrie 4.0 et les initiatives d'usine intelligente accélère l'adoption de technologies de détection optique haute performance. L'innovation continue dans l'automobile LiDAR et les solutions d'automatisation renforcent encore les perspectives de croissance.

Aperçu du marché des capteurs de photodiode en Asie-Pacifique

Le marché des capteurs de photodiodes en Asie et dans le Pacifique est sur le point de croître au rythme le plus rapide du TCAC pendant la période de prévision de 2026 à 2033, sous l'impulsion d'une urbanisation rapide, d'une infrastructure de télécommunications en expansion et de solides capacités de fabrication de semi-conducteurs dans des pays comme la Chine, le Japon et la Corée du Sud. L'augmentation de la production d'électronique de consommation et le déploiement croissant de réseaux de fibre optique sont des catalyseurs de croissance majeurs. Les initiatives gouvernementales visant à promouvoir la numérisation et la fabrication nationale de puces renforcent encore la demande régionale. Le rôle croissant d'APAC en tant que centre mondial de fabrication d'électronique améliore l'adoption à grande échelle de capteurs photodiode.

Japan Photodiode Sensors Market Insight

Le marché japonais des capteurs photodiodes prend de l'ampleur grâce à l'industrie électronique avancée du pays et à l'accent mis sur l'ingénierie de précision. L'adoption élevée de photodiodes dans les systèmes d'imagerie, la robotique et les dispositifs médicaux favorise une croissance régulière. Japon Le leadership dans les technologies optiques et la miniaturisation des capteurs stimule l'innovation dans les systèmes de détection haute performance. Le développement croissant d'infrastructures intelligentes et de technologies automobiles de nouvelle génération accélère encore l'expansion du marché.

Chine Capteurs photodiode Aperçu du marché

En 2025, le marché chinois des détecteurs de photodiodes représentait la part de marché la plus importante en Asie-Pacifique, attribuable à l'expansion rapide des réseaux de télécommunications et à la fabrication d'électroniques à grande échelle. Chine Un solide écosystème de semi-conducteurs domestique soutient la production en volume de composants optoélectroniques. La demande croissante d'électronique de consommation, d'automatisation industrielle et de systèmes de surveillance propulse l'adoption. Les investissements du pays dans les villes intelligentes, les infrastructures 5G et les technologies de pointe continuent de renforcer sa position dominante au niveau régional.

Part de marché des capteurs de photodiode

L'industrie des capteurs photodiode est principalement dirigée par des entreprises bien établies, notamment :

- La société Everlight Electronics Co., Ltd (Taiwan)

- OSRAM Opto Semiconductors GmbH(Allemagne)

- ROHM CO., LTD.(Japon)

- Hamamatsu Photonics K.K.(Japon)

- Thorlabs, Inc. (États-Unis)

- TT électronique (Royaume-Uni)

- Premier capteur AG (Allemagne)

- Edmund Optics Inc. (États-Unis)

- Industries des composants semi-conducteurs, LLC (États-Unis)

- Global Communication Semiconductors, LLC (États-Unis)

- KYOTO SEMICONDUCTOR Co., Ltd. (Japon)

- Vishay Intertechnology, Inc. (États-Unis)

- Centronic (Royaume-Uni)

- AIPC Corporation (Japon)

- Diodes Incorporated (États-Unis)

- Agilent Technologies, Inc. (États-Unis)

- New Japan Radio Co., Ltd. (Japon)

- Société LuxNet (Japon)

- Central Semiconductor Corp. (États-Unis)

Les derniers développements du marché mondial des capteurs de photodiode

- En décembre 2025, Imec a démontré l'intégration de photodiodes colloïdales quantiques-points sur des wafers CMOS de 300 mm, faisant progresser la technologie de détection infrarouge à ondes courtes évolutives (SWIR) pour la fabrication de semi-conducteurs à grand volume. Ce développement devrait réduire considérablement les coûts de production tout en améliorant la sensibilité et la résolution des capteurs de photodiode SWIR. L'innovation renforce la viabilité commerciale de l'automobile LiDAR, l'inspection industrielle, la surveillance environnementale et les applications agricoles intelligentes. En permettant la compatibilité avec les processus CMOS standard, il accélère l'adoption plus large de capteurs de photodiode infrarouge avancés dans l'électronique de masse

- En juin 2025, Sony Semiconductor Solutions a introduit le capteur de profondeur SPAD empilé IMX479 conçu pour les systèmes LiDAR automobiles, offrant une gamme de détection allant jusqu'à 300 mètres avec une efficacité de détection de photon améliorée. Cette avancée favorise la reconnaissance d'objets de précision et la cartographie de profondeur à longue portée dans les systèmes avancés d'assistance au conducteur et les véhicules autonomes. L'amélioration de l'efficacité améliore les performances dans les environnements de conduite à faible luminosité et à grande vitesse, renforçant ainsi la compétitivité des architectures photodiodes basées sur SPAD. Étant donné que les constructeurs automobiles privilégient de plus en plus la sécurité et l'automatisation, ces innovations créent des possibilités de croissance substantielles sur le marché des capteurs photodiode

- En mai 2025, Lawrence Livermore National Laboratory a dévoilé une méthode électrophorétique de dépôt quantique-point qui améliore la performance des détecteurs à infrarouge proche sur les substrats texturés et non planaires. Cette technique améliore l'efficacité et l'uniformité de l'absorption de la lumière, ce qui peut améliorer significativement la sensibilité dans les capteurs photodiodes infrarouges. La percée appuie les progrès dans les applications de télécommunications, d'imagerie biomédicale et de spectroscopie nécessitant une détection optique de haute précision. En permettant une meilleure fabrication des détecteurs sur des surfaces complexes, le développement étend la flexibilité de conception et les capacités de performance au sein de l'industrie des capteurs photodiodes

- En avril 2025, TDK a démontré le premier détecteur de photo Spin au monde capable d'obtenir des améliorations de taux de données décuplés par rapport aux photodétecteurs conventionnels. Cette innovation introduit une nouvelle approche de la conversion optique des données à haute vitesse, en particulier pour les interconnexions d'accélérateurs d'IA et les environnements informatiques à large bande. L'augmentation de la vitesse de transmission et de l'efficacité des signaux soutient la demande croissante de traitement plus rapide des données dans les centres de données et les systèmes informatiques avancés. Ces progrès renforcent le rôle croissant des technologies de photodiode de nouvelle génération dans les infrastructures de communication à haut rendement

- En mars 2025, onsemi a lancé le capteur de temps de vol indirect Hyperlux ID en temps réel, capable de détecter la profondeur jusqu'à 30 mètres pour les environnements industriels. Cette solution améliore les capacités de détection 3D de précision dans les systèmes d'automatisation d'usine, de robotique et de vision des machines. En améliorant la précision et la fiabilité de la profondeur dans des conditions d'éclairage difficiles, il renforce l'intégration des modules de détection à base de photodiodes dans les plates-formes d'automatisation industrielle. Le lancement contribue à la demande croissante de solutions de détection optique de pointe dans les initiatives de fabrication intelligente et de numérisation industrielle

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.