Global Tank Insulation Market

Taille du marché en milliards USD

TCAC :

%

USD

3.84 Billion

USD

10.30 Billion

2024

2032

USD

3.84 Billion

USD

10.30 Billion

2024

2032

| 2025 –2032 | |

| USD 3.84 Billion | |

| USD 10.30 Billion | |

| % | |

|

Segmentation du marché mondial de l'isolation des réservoirs, par type (stockage et transport), type de matériau (polystyrène expansé (EPS), Rockwool, verre cellulaire, fibre de verre, mousse élastomérique, polyuréthane (PU), etc.), type de température (isolation par les puits et isolement par le froid), type de réservoir (citerne vertical, réservoir horizontal, réservoir fixe et réservoir monté), extrémités des réservoirs (réservoir parabolique et plat), utilisateur final (huile et gaz, énergie et énergie, produits chimiques, aliments et boissons, purification de l'eau, purification des eaux usées, etc.) - Tendances de l'industrie et prévisions jusqu'en 2032

Tank Insulation Market Size

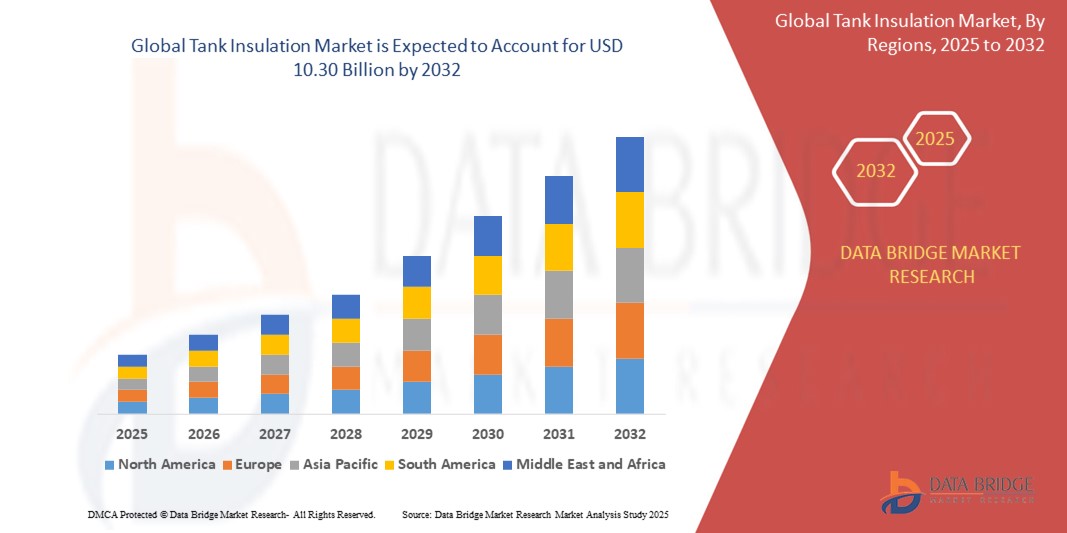

- The global tank insulation market size was valued atUSD 3.84 billion in 2024and is expected to reachUSD 10.30 billion by 2032, at aCAGR of 5.25%during the forecast period

- This growth is driven by factors such as the increasing demand for energy-efficient insulation solutions in industries such as oil & gas, energy, and chemicals

Tank Insulation Market Analysis

- Tank insulation is defined as the process in which different chemicals and materials are applied to the inside of tank and also to the surface, to maintain the temperature throughout its usage period

- Tank insulation is done to preserve the temperature inside the tank in order to minimize the heat loss

- North America is expected to dominate the tank insulations market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials

- Asia-Pacific is expected to be the fastest growing region in the tank insulation market during the forecast period due to rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions

- Rockwool and polyurethane (PU) segment is expected to dominate the market with a market share of 31.5% due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency

Report Scope and Tank Insulation Market Segmentation

|

Attributes |

Tank Insulation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tank Insulation Market Trends

“Advancements in Sustainable Insulation Materials”

- In recent years, there has been a significant trend towards the use of sustainable and eco-friendly insulation materials in tank insulation. Industries are increasingly focused on minimizing their environmental footprint and improving energy efficiency. Manufacturers are developing insulation solutions that are not only thermally efficient but also made from renewable or recyclable materials

- For Instance, Rockwool International A/S, which has been at the forefront of developing insulation products made from sustainable materials. Their mineral wool insulation solutions are designed to be highly energy-efficient while being recyclable, aligning with growing global sustainability goals

- The transition to a circular economy is influencing the tank insulation market. Companies are investing in materials that can be reused or recycled, reducing waste and fostering sustainability in the supply chain

- Many governments around the world are implementing stricter regulations related to energy efficiency in industrial sectors. This is pushing companies to adopt more advanced and sustainable insulation solutions that reduce energy consumption and improve temperature control for storage tanks

- Manufacturers of tank insulation are increasingly obtaining environmental certifications for their products, ensuring compliance with international standards such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method)

Tank Insulation Market Dynamics

Driver

“Increasing Energy Efficiency Demands”

- The primary driver of growth in the global tank insulation market is the increasing demand for energy efficiency. Insulated tanks help reduce energy loss during the storage and transportation of liquids, gases, and chemicals by maintaining temperature control. This is especially critical in sectors such as oil and gas, chemicals, and food processing, where temperature-sensitive materials are involved

- As the global energy crisis intensifies, industries are under pressure to optimize their energy consumption. Tank insulation solutions help minimize energy waste by maintaining the desired temperature, leading to significant energy savings

- Governments are implementing stricter regulations regarding energy use, particularly in high-consumption industries.

- For instance, the European Union's Energy Efficiency Directive mandates the reduction of energy use across industries, pushing companies to adopt solutions such as tank insulation to comply with these regulations

- Tank insulation reduces the need for additional energy resources by preventing heat loss or gain. This directly results in lower energy bills for companies that adopt these solutions, making it a cost-effective measure

- The oil and gas industry is one of the largest consumers of insulated tanks. With the growing focus on reducing operational costs, the demand for advanced insulation solutions is surging to ensure that thermal energy is not wasted during storage and transportation processes

Opportunity

“Growth in Emerging Markets”

- Emerging markets, particularly in regions such as Asia-Pacific, Latin America, and the Middle East, offer significant growth opportunities for the global tank insulation market. As these regions industrialize at a rapid pace, there is an increasing demand for tank insulation solutions across various sectors, including chemicals, oil and gas, and pharmaceuticals

- Countries in the Middle East and Asia are investing heavily in infrastructure development, including energy production and petrochemical plants. This creates opportunities for the tank insulation market, as these facilities require highly efficient thermal insulation for storage tanks to optimize energy use

- Governments in emerging markets are encouraging foreign investments and providing incentives for companies to adopt energy-efficient technologies. These incentives are a key opportunity for manufacturers of tank insulation solutions to expand their reach in these regions

- As renewable energy projects such as wind, solar, and bioenergy grow in emerging markets, there is an increasing need for efficient storage solutions. Insulated tanks are crucial in ensuring that energy storage systems function optimally, which presents an opportunity for insulation companies to cater to the renewable energy sector

- The growing food processing and pharmaceutical industries in emerging markets create new opportunities for tank insulation providers, as these industries require insulated storage tanks for temperature-sensitive materials

Restraint/Challenge

“High Initial Investment Costs”

- The installation of advanced tank insulation systems, particularly those made from high-performance materials, involves significant upfront capital investment. For many small and medium-sized enterprises (SMEs), this high initial cost can be a major barrier to adopting tank insulation solutions

- The return on investment (ROI) for insulated tanks, although positive in terms of energy savings, can take several years to materialize. This long payback period discourages many companies from making the initial investment, especially in industries with tighter profit margins

- Retrofitting existing tanks with new insulation systems can be complex and costly. Many companies face challenges when integrating insulation into their pre-existing infrastructure, leading to higher operational costs during the installation process

- The prices of raw materials used in insulation, such as fiberglass, mineral wool, and polyurethane, can fluctuate significantly. This price volatility can increase the overall cost of insulation systems and create uncertainty in the market

- In some developing regions, the awareness of the benefits of tank insulation is still low. Companies may not fully realize the long-term energy savings and operational efficiency gains that can be achieved through proper insulation, which limits market growth in these areas

Tank Insulation Market Scope

The market is segmented on the basis type, material type, temperature type, tank type, tank ends, and end-user.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Material Type |

|

|

By Temperature Type |

|

|

By Tank Type |

|

|

By Tank Ends |

|

|

By End-User |

|

In 2025, the rockwool and polyurethane (PU) is projected to dominate the market with a largest share in material type segment

The rockwool and polyurethane (PU) segment is expected to dominate the tank insulation market with the largest share of 31.5% in 2025 due to their high thermal insulation properties and versatility. These materials are widely used in industries such as oil and gas, chemicals, and energy due to their excellent ability to maintain the required temperature levels while ensuring energy efficiency.

The hot insulation is expected to account for the largest share during the forecast period in temperature market

In 2025, the got insulation segment is expected to dominate the market with the largest market share of 51.31% due to preventing heat loss and protecting equipment, ensuring that industrial processes remain within safe temperature limits. Hot insulation solutions help companies save on heating costs and reduce energy consumption, making this a highly demanded segment across various industries.

Tank Insulation Market Regional Analysis

“North America Holds the Largest Share in the Tank Insulation Market”

- North America remains a dominant player in the global tank insulation market due to its advanced infrastructure and continuous focus on technological innovations in insulation materials. The region is home to a highly developed chemical, oil & gas, and energy sector, all of which rely heavily on insulated tanks for storage and transportation of liquids and gases

- Stringent regulations related to energy efficiency and safety standards have prompted companies in North America to adopt tank insulation solutions. These regulations not only ensure operational safety but also contribute to energy conservation and reduction of carbon footprints

- The oil & gas sector, especially in the U.S. and Canada, is a major consumer of tank insulation, where insulated tanks are essential to maintaining temperature control for both storage and transportation. The sector's growth, driven by the need for storage tanks for crude oil and natural gas, further bolsters market demand

- North America has well-established manufacturing capabilities for tank insulation materials such as polyurethane, polystyrene, and fiberglass, enabling a strong supply chain to meet local and international demand

- Increasing investments in energy efficiency across various industries, especially in power generation and industrial manufacturing, have further driven the demand for insulated tanks in this region, making North America a market leader

“Asia-Pacific is Projected to Register the Highest CAGR in the Tank Insulation Market”

- The Asia-Pacific region, particularly countries such as China, India, and South Korea, is experiencing rapid industrialization and urbanization, which is driving significant demand for tank insulation solutions. Industries such as chemicals, oil & gas, and food processing are growing rapidly, creating a high need for insulated tanks

- Several governments in APAC are focusing on enhancing industrial infrastructure, which includes the construction of storage facilities and refineries that require tank insulation solutions. Government incentives for energy-efficient solutions and compliance with environmental regulations are contributing to the region's growth in this market

- As energy consumption in the region rises, particularly in emerging economies such as India and China, there is a growing need to store and transport energy-efficient materials, requiring the installation of insulated tanks to maintain temperature stability and minimize energy losses

- APAC is seeing significant growth in its petrochemical industry, with major projects coming online, particularly in countries such as China and India. These industries are among the biggest consumers of tank insulation systems to store chemicals at safe temperatures

- The adoption of more affordable and locally manufactured insulation materials, such as fiberglass and mineral wool, is driving market growth in the APAC region. The lower costs of production and raw materials have made insulated tank solutions more accessible to a larger number of companies in this region

Tank Insulation Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Commercial Thermal Solutions, Inc. (U.S.)

- Dow(U.S.)

- GILSULATE INTERNATIONAL, INC. (U.S.)

- ITW INSULATION SYSTEMS(U.S.)

- J.H. Ziegler GmbH(Germany)

- Knauf Insulation (U.S.)

- PolarClad Tank Insulation (U.S.)

- ARMACELL LLC (U.S.)

- Kingspan Group (Ireland)

- Synavax (U.S.)

- Johns Manville (U.S.)

- Mayes Coatings & Insulation, Inc. (U.S.)

- Thermacon (U.S.)

- Gulf Cool Therm Factory LTD (UAE)

- ROCKWOOL International A/S (Denmark)

- Cabot Corporation (U.S.)

- SPX Transformer Solutions Inc. (U.S.)

- DUNMORE (U.S.)

- T.F. Warren Group (U.S.)

- Saint-Gobain (France)

- Huntsman International LLC (U.S.)

- Corrosion Resistant Technologies, Inc. (U.S.)

- Röchling (Germany)

Latest Developments in Global Tank Insulation Market

- In May 2025, Rockwool International A/S Expands Product Line, the new products are designed with improved fire resistance and better thermal performance, catering to industries with stringent regulatory requirements

- In March 2025, Dow Launches New Polyurethane-Based Insulation, designed to enhance the performance and energy efficiency of tank insulation systems. The new product features improved thermal resistance properties and lower environmental impact due to the use of renewable materials

- In January 2025, Knauf Insulation Partners with Large Industrial Clients, to supply tank insulation materials for large-scale oil and gas refineries and chemical plants. The collaboration aims to enhance the energy efficiency of storage and transportation tanks used in these industries

- In December 2024, ITW Insulation Systems Launches Advanced Insulation Solutions for High-Temperature Applications, designed for hot tanks in the petrochemical industry. The products feature enhanced resistance to thermal stress and are designed to improve energy conservation in high-demand environments

- In September 2024, Johns Manville Introduces Recyclable Insulation Products, made from sustainable materials. These products are aimed at companies looking to reduce their environmental impact while maintaining high insulation performance

- In June 2024, Armacell LLC Expands Operations in Asia-Pacific, expanded its operations in the Asia-Pacific region by opening a new production facility in India. This facility will cater to the growing demand for tank insulation in industries such as oil & gas and chemicals

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

TABLE DES MATIÈRES MARCHÉ MONDIAL DE L'INSULATION

1 INTRODUCTION

1.1 OBJECTIFS DE L'ÉTUDE 1.2 DÉFINITION DU MARCHÉ 1.3 APERÇU DU MARCHÉ MONDIAL DE L'INSULATION DES TANQUES 1.4 MONNAIE ET PRINCIPE 1.5 LIMITES 1.6 MARCHÉS COUVERTS

2 SEGMENTATION DU MARCHÉ

2.1 MARCHÉS COUVERTS 2.2 CHAMP D'APPLICATION GÉOGRAPHIQUE 2.3 ANNÉES CONSIDÉRÉES POUR L'ÉTUDE 2.4 CURRENCE ET PRICTION 2.5 MODÈLE DE VALIDATION DES DONNÉES DU TRIPOD DBMR 2.6 MODÈLE DE LA TECHNOLOGIE 2.7 MODÈLE MULTIVARIATE 2.8 INTERVIEWS PRIMAIRES AVEC LES PRINCIPAUX D'AVIS 2.9 GRID DE POSITION DU MARCHÉ DBMR 2.10 GRID DE COUVERTURE DES APPLICATIONS DU MARCHÉ 2.11 MODÈLE DE DÉFIS DU MARCHÉ DBMR 2.12 DONNÉES SUR L'IMPORTATION ET L'EXPORTATION 2.13 ANALYSE DES PARTAGES DBMR 2.14 SOURCES SECONDAIRES 2.15

3 APERÇU DU MARCHÉ

3.1 Conducteurs

3.1.1 RENFORCEMENT DE LA DEMANDE DE L'INDUSTRIE DE L'HUILE ET DU GAZ 3.1.2 RENFORCEMENT DE LA DEMANDE D'ASSULATION DE CRYOGÉNIQUES DANS LE STOCKAGE DU GNL ET LE TRANSPORT 3.1.3 RENFORCEMENT DE LA DEMANDE D'EMBALLAGE CONTRÔLÉ DE TEMPÉRATURE POUR LES PHARMACEUTIQUES 3.1.4 RENFORCEMENT DE LA DEMANDE DE MICA FEUILLES DANS LES TANQUES POUR PROVIDER LE BARRIER THERMIQUE

3.2 RÉSULTATS

3.2.1 PRIX DES MATÉRIAUX FLUCTEURS 3.2.2 CHANGEMENT DE LA STRUCTURE CHIMIQUE DUE À L'ADULTERATION PAR LES MATÉRIAUX INSULATIFS 3.2.3 INDISPONIBILITÉ DES MATÉRIAUX INSULATIFS PROFESSIONNELS POUR L'INDUSTRIE DE L'IRON ET DE L'ACIER À L'ÉTAT MOLTEN DANS LES TANCS 3.2.4 DÉGRADATION FRÉQUENTE DES MATÉRIAUX INSULATIFS DANS L'INDUSTRIE CHIMIQUE

3.3 OPPORTUNITÉS

3.3.1 ÉLEVÉE DE LA DEMANDE POUR LES PÉTROCHÉMIQUES EN CHINE ET EN INDE 3.3.2 ÉLEVÉE DE LA DEMANDE DE MATÉRIAUX INSULATIFS DANS LES PÉTROCHES D'EAU POUR LES BÂTIMENTS MULTI-STOIRES RESIDENTIELS ET COMMERCIAUX 3.3.3 ÉVOLUTION DE L'INDUSTRIE DANS LES ÉCONOMIES ÉMERGÉES

3.4 DÉFIS

3.4.1 FEU ET EXPLOSION DUS À LA RÉACTION CHIMIQUE AVEC DES MATÉRIAUX INSULATIFS DANS LE TANQUE 3.4.2 DANGER SANTÉ DES MÉDIAS INSULATIFS

4 RÉSUMÉ 5 PRIMAIRES 6 INDICATIONS DE L'INDUSTRIE 7 MARCHÉ GLOBAL DE L'INSULATION DES TANQUES, PAR TYPE

7.1 Aperçu 7.2 STOCKAGE 7.3 TRANSPORT

8 MARCHÉ GLOBAL DE L'INSULATION DES TANQUES, PAR TYPE DE MATÉRIEL

8.1 APERÇU 8.2 POLYSTYRENE EXPANDÉ (EPS) 8.3 ROCKWOOL 8.4 GLASSE CELLULAIRE 8.5 FIBERGLASS 8.6 POAM ELASTOMÉRIQUE 8,7 POLYURETHANE (PU) 8,8 AUTRES

9 MARCHÉ MONDIAL DE L'INSULATION PAR TEMPÉRATURE

9.1 APERÇU GÉNÉRAL 9.2 INSULATION DU HOT 9.3 INSULATION DU POUVOIR

10 MARCHÉ GLOBAL DE L'INSULATION DES TANQUES, PAR TYPE DE TANQUE

10.1 APERÇU 10.2 TANQUE VERTIQUE 10.3 TANQUE HORIZONTALE 10.4 TANQUE FIXÉE 10.5 TANQUE MONTÉE

11 MARCHÉ GLOBAL DE L'INSULATION DES TANQUES, PAR TANQUES

11.1 APERÇU 11.2 POISSONS PARABOLIQUES 11.3 FLAT

12 MARCHÉ MONDIAL DE L'INSULATION DE TANQUES, PAR UTILISATEUR

12.1 APERÇU 12.2 OIL ET GAZ

12.2.1 OIL

12.2.1.1 OIL CRUDE 12.2.1.2 PÉTROCHÉMIQUE 12.2.1.3 AUTRES DÉRIVÉS D'HUILE CRUDE

12.2.2 GAZ

12.2.2.1 GAZ NATUREL 12.2.2.2 GAZ SYNTHÉTIQUE

12.3 ÉNERGIE ET POUVOIR 12.4 PRODUITS CHIMIQUES 12.5 ALIMENTS ET BOISSONS

12.5.1 ALIMENTS 12.5.2 BOISSONS

12.5.2.1 BOISSONS ALCOOLIQUES 12.5.2.2 POISSONS DIRECTÉES 12.5.2.3 POISSONS AÉRÉES 12.5.2.4 JUSTES ET EAU INFLAVÉE 12.5.2.5 AUTRES

12.6 PURIFICATION DE L'EAU

12.6.1 ÉTABLISSEMENTS COMMERCIAUX 12.6.2 MUNICIPALITÉ 12.6.3 ÉTABLISSEMENTS RÉSIDENTIELS

12.7 PURIFICATION DES DÉCHETS

12.7.1 ÉTABLISSEMENTS COMMERCIAUX 12.7.2 MUNICIPALITÉ 12.7.3 ÉTABLISSEMENTS RÉSIDENTIELS

12.8 AUTRES

13 MARCHÉ MONDIAL DE L'INSULATION DE TANQUES, PAR GÉOGRAPHIE

13.1 APERÇU 13.2 AMÉRIQUE DU NORD

13.2.1 États-Unis 13.2.2 CANADA 13.2.3 MEXIQUE

13.3 EUROPE

13.3.1 ALLEMAGNE 13.3.2 Royaume-Uni 13.3.3 ITALIE 13.3.4 FRANCE 13.3.5 ESPAGNE 13.3.6 SUISSE 13.3.7 RUSSIE 13.3.8 TURQUIE 13.3.9 BELGIQUE 13.3.10 PAYS-BAS 13.3.11 RESTE D'EUROPE

13.4 ASIE-PACIFIQUE

13.4.1 CHINE 13.4.2 INDE 13.4.3 CORÉE DU SUD 13.4.4 JAPON 13.4.5 AUSTRALIE 13.4.6 SINGAPORE 13.4.7 THAÏLANDE 13.4.8 INDONÉSIE 13.4.9 MALAIS 13.4.10 PHILIPPINES 13.4.11 EST D'ASIE-PACIFIQUE

13.5 AMÉRIQUE DU SUD

13.5.1 BRÉSIL 13.5.2 ARGENTINE 13.5.3 RESTE D'AMÉRIQUE DU SUD

13.6 MOYEN-ORIENT ET AFRIQUE

13.6.1 Émirats arabes unis 13.6.2 ARABIE SAOUDIQUE 13.6.3 ISRAEL 13.6.4 AFRIQUE DU SUD 13.6.5 ÉGYPTE 13.6.6 EST DU MOYEN-ORIENT ET AFRIQUE

14 MARCHÉ MONDIAL DE L'INSULATION DES TANQUES, PAYSAGE DES ENTREPRISES

14.1 ANALYSE DU PARTAGE DES ENTREPRISES: MONDE 14.2 ANALYSE DU PARTAGE DES ENTREPRISES: AMÉRIQUE DU NORD 14.3 ANALYSE DU PARTAGE DES ENTREPRISES: EUROPE 14.4 ANALYSE DU PARTAGE DES ENTREPRISES: ASIE-PACIFIQUE 14.5 MOYENS ET ACQUISITIONS 14.6 DÉVELOPPEMENT ET HOMOLOGATIONS DES NOUVEAUX PRODUITS 14.7 EXPANSIONS 14.8 PARTENARIAT ET AUTRES ÉVOLUTIONS STRATÉGIQUES

15 PROFILS D'ENTREPRISE

15.1 BASE SE

15.1.1 COMPAGNIE SNAPSHOT 15.1.2 ANALYSE DE LA SUITE 15.1.3 ANALYSE DES RECETTES 15.1.4 ANALYSE DES PARTAGES DES ENTREPRISES 15.1.5 PRESENCE GÉOGRAPHIQUE 15.1.6 PORTEFEUILLE DES PRODUITS 15.1.7 FAITS NOUVEAUX 15.1.8 ANALYSE DE LA RECHERCHE SUR LE MARCHÉ DE LA Bride DE DONNÉES

15.2 LA SOCIÉTÉ CHIMIQUE DOW

15.2.1 COMPAGNIE SNAPSHOT 15.2.2 ANALYSE DE LA SUITE 15.2.3 ANALYSE DES REVENUS 15.2.4 ANALYSE DES PARTAGES DES ENTREPRISES 15.2.5 PRESENCE GÉOGRAPHIQUE 15.2.6 PORTEFEUILLE DES PRODUITS 15.2.7 FAITS NOUVEAUX 15.2.8 ANALYSE DE LA RECHERCHE SUR LE MARCHÉ DES BROUGES DE DONNÉES

15.3 SAINT-GOBAINE

15.3.1 COMPAGNIE SNAPSHOT 15.3.2 ANALYSE DU SWOT 15.3.3 ANALYSE DU REVENU 15.3.4 ANALYSE DU PARTAGE DES ENTREPRISES 15.3.5 PRESENCE GÉOGRAPHIQUE 15.3.6 PORTEFEUILLE DES PRODUITS 15.3.7 ÉVOLUTION RÉCENTE 15.3.8 ANALYSE DE LA RECHERCHE SUR LE MARCHÉ DU BRID DE DONNÉES

15.4 HUNTSMAN INTERNATIONAL LLC

15.4.1 COMPAGNIE SNAPSHOT 15.4.2 ANALYSE DU SWOT 15.4.3 ANALYSE DU REVENU 15.4.4 ANALYSE DU PARTAGE DES ENTREPRISES 15.4.5 PRESENCE GÉOGRAPHIQUE 15.4.6 PORTEFEUILLE DES PRODUITS 15.4.7 FAITS NOUVEAUX 15.4.8 ANALYSE DU MARCHÉ DES DONNÉES

15.5 GROUPE KINGSPAN

15.5.1 COMPAGNIE SNAPSHOT 15.5.2 ANALYSE DE LA SUITE 15.5.3 ANALYSE DES RECETTES 15.5.4 ANALYSE DES PARTAGES DES ENTREPRISES 15.5.5 PRESENCE GÉOGRAPHIQUE 15.5.6 PORTFOLIO DES PRODUITS 15.5.7 FAITS NOUVEAUX 15.5.8 ANALYSE DE LA RECHERCHE SUR LE MARCHÉ DES BROUGES DE DONNÉES

15.6 ARMACELL LLC

15.6.1 COMPAGNIE SNAPSHOT 15.6.2 ANALYSE DES RECETTES 15.6.3 PRESENCE GÉOGRAPHIQUE 15.6.4 PORTEFEUILLE DE PRODUITS 15.6.5 FAITS NOUVEAUX

15.7 SOCIÉTÉ CABOT

15.7.1 COMPAGNIE SNAPSHOT 15.7.2 ANALYSE DES RECETTES 15.7.3 PRESENCE GÉOGRAPHIQUE 15.7.4 PORTEFEUILLE DE PRODUITS 15.7.5 FAITS NOUVEAUX

15.8 SOLUTIONS THERMALES COMMERCIALES, INC.

15.8.3 DÉVELOPPEMENT RÉCENT

15.9 TECHNOLOGIES RÉSISTANTES DE LA CORROSION, INC.

15.9.1 COMPAGNIE SNAPSHOT 15.9.2 PORTEFEUILLE DE PRODUITS 15.9.3 DÉVELOPPEMENT RÉCENT

15.10 DUNMORE

15.10.1 COMPAGNIE SNAPSHOT 15.10.2 PRESENCE GÉOGRAPHIQUE 15.10.3 PORTEFEUILLE DES PRODUITS 15.10.4 FAITS NOUVEAUX

15.11 GILSULATE INTERNATIONAL, INC.

15.11.1 COMPAGNIE SNAPSHOT 15.11.2 PORTEFEUILLE DE PRODUITS 15.11.3 FAITS NOUVEAUX

15.12 GULF COOL THERM FACTORY LTD

15.12.1 COMPAGNIE SNAPSHOT 15.12.2 PORTEFEUILLE DE PRODUITS 15.12.3 DÉVELOPPEMENT RÉCENT

15.13 SYSTÈMES D ' INSULATION

15.13.1 COMPAGNIE SNAPSHOT 15.13.2 PRESENCE GÉOGRAPHIQUE 15.13.3 PORTEFEUILLE DES PRODUITS 15.13.4 FAITS NOUVEAUX

15.14 MOYENS D'EMPLOI

15.14.1 COMPAGNIE SNAPSHOT 15.14.2 PRESENCE GÉOGRAPHIQUE 15.14.3 PORTEFEUILLE DES PRODUITS 15.14.4 FAITS NOUVEAUX

15.15 J.H. ZIEGLER GMBH

15.15.1 COMPAGNIE SNAPSHOT 15.15.2 PRESENCE GÉOGRAPHIQUE 15.15.3 PORTEFEUILLE DE PRODUITS 15.15.4 DÉVELOPPEMENT RÉCENT

15.16 INSULATION DU KNAUF

15.16.1 COMPAGNIE SNAPSHOT 15.16.2 PRESENCE GÉOGRAPHIQUE 15.16.3 PORTEFEUILLE DE PRODUITS 15.16.4 FAITS NOUVEAUX

15.17 MAYES COATINGS & INSULATION, INC.

15.17.1 COMPAGNIE SNAPSHOT 15.17.2 PORTEFEUILLE DE PRODUITS 15.17.3 FAITS NOUVEAUX

15.18 PERSONNES D'ENTREPRISE

15.18.1 COMPAGNIE SNAPSHOT 15.18.2 ANALYSE DES RECETTES 15.18.3 PRESENCE GÉOGRAPHIQUE 15.18.4 PORTEFEUILLE DES PRODUITS 15.18.5 FAITS NOUVEAUX

15.19 INSULATION DE LA POLARCLANDE

15.19.1 COMPAGNIE SNAPSHOT 15.19.2 PORTEFEUILLE DE PRODUITS 15.19.3 DÉVELOPPEMENT RÉCENT

15.20 GROUPE DE RÖCHLING

15.20.1 COMPAGNIE SNAPSHOT 15.20.2 PRESENCE GÉOGRAPHIQUE 15.20.3 PORTEFEUILLE DE PRODUITS 15.20.4 FAITS NOUVEAUX

15.21 ROCKWOOL INTERNATIONAL A/S

15.21.1 COMPAGNIE SNAPSHOT 15.21.2 ANALYSE DES RECETTES 15.21.3 PRESENCE GÉOGRAPHIQUE 15.21.4 PORTEFEUILLE DES PRODUITS 15.21.5 FAITS NOUVEAUX

15.22 SOLUTIONS DE TRANSFORMATEUR SPX INC.

15.22.1 COMPAGNIE SNAPSHOT 15.22.2 PORTEFEUILLE DE PRODUITS 15.22.3 FAITS NOUVEAUX

15.23 SYNAVAX

15.23.1 COMPAGNIE SNAPSHOT 15.23.2 PORTEFEUILLE DE SOLUTION 15.23.3 FAITS NOUVEAUX

15.24 THERMACON

15.24.1 COMPAGNIE SNAPSHOT 15.24.2 PORTEFEUILLE DE PRODUITS 15.24.3 DÉVELOPPEMENT RÉCENT

15.25 GROUPE T.F.WARREN

15.25.1 COMPAGNIE SNAPSHOT 15.25.2 PRESENCE GÉOGRAPHIQUE 15.25.3 PORTEFEUILLE DES PRODUITS 15.25.4 FAITS NOUVEAUX

16 QUESTIONNAIRE 17 CONCLUSION 18 RAPPORTS CONNEXES

Liste des tableaux

LISTE DES TABLEAUX MARCHÉ MONDIAL DE L'INSULATION

TABLEAU 1 DONNÉES D'IMPORTATION DE RÉSERVES, DE TANQUES, DE VAT ET DE CONTENEURS SIMILAIRES, D'ENTREPRISE OU D'ACIER, POUR TOUTE MATÉRIEL "AUTE QUE LE GAZ COMPRIMÉ OU LIQUÉFIÉ", D'UNE CAPACITÉ DE > 300 L, NON ACCOMPLIS AVEC UN MÉCANIQUE OU UN ÉQUIPEMENT THERMIQUE, LORSQU'IL N'EST PAS LINÉ OU INSULÉ À LA CHAUFFAGE (EXCLUANT LES CONTENEURS SPÉCIFIQUEMENT CONSTRUITS OU EQUIPÉS POUR UN OU plusieurs TYPES DE TRANSPORT); CODE SH 7309 (MILLIONS USD) TABLEAU 2 DONNÉES SUR L'EXPORTATION DES CONTENEURS, TANQUES, VAT ET CONTENEURS SIMILAIRES, D'IRON OU D'ACIER, POUR TOUT MATÉRIEL "AUT QUE LE GAZ COMPRIMÉ OU LIQUÉ", D'UNE CAPACITÉ DE > 1er janvier 2017

Liste des figures

LISTE DES CHIFFRES MARCHÉ DE L'INSULATION MONDIALE

FIGURE 1 TANQUE GLOBALE MARCHANDISES : SEGLEMENT 13 TANQUES MANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT 13 TANQUES : SEGLEMENT

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.