Global Virtual Infrastructure Manager Market

Taille du marché en milliards USD

TCAC :

%

USD

3.40 Billion

USD

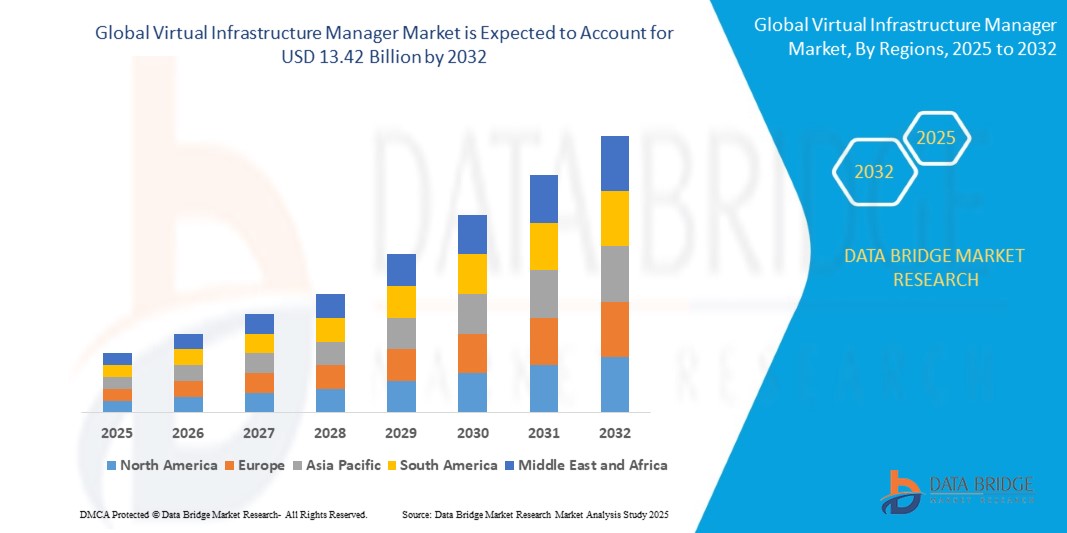

13.42 Billion

2023

2030

USD

3.40 Billion

USD

13.42 Billion

2023

2030

| 2024 –2030 | |

| USD 3.40 Billion | |

| USD 13.42 Billion | |

| % | |

|

Сегментация глобального рынка управления виртуальной инфраструктурой по предложению (решения и услуги), разработке (IaaS и локальные решения), конечному пользователю (ИТ и телекоммуникации, бизнес-финансирование, здравоохранение, производство, розничная торговля и другие) — отраслевые тенденции и прогноз до 2032 года

Размер рынка менеджеров виртуальной инфраструктуры

- Объем мирового рынка управления виртуальной инфраструктурой в 2024 году оценивался в 3,40 млрд долларов США, а к 2032 году , как ожидается, он достигнет 13,42 млрд долларов США при среднегодовом темпе роста 18,70% в течение прогнозируемого периода.

- Рост рынка во многом обусловлен растущим внедрением облачной инфраструктуры, растущим спросом на централизованное и автоматизированное управление виртуальной средой, а также растущим переходом к виртуализации сетевых функций (NFV) и программно-определяемым центрам обработки данных (SDDC) на предприятиях.

- Расширение инициатив цифровой трансформации и растущее внимание к оптимизации ИТ-нагрузок и сокращению капитальных затрат (CapEx) еще больше ускоряют внедрение менеджеров виртуальной инфраструктуры в различных отраслях.

Анализ рынка менеджеров виртуальной инфраструктуры

- Спрос на менеджеров виртуальной инфраструктуры растет, поскольку организации отдают приоритет гибкости, масштабируемости и экономической эффективности ИТ-систем при работе со сложными гибридными и многооблачными средами.

- Растущее внедрение инфраструктуры 5G и технологий периферийных вычислений повышает потребность в динамической координации виртуальных ресурсов в режиме реального времени, где менеджеры виртуальной инфраструктуры играют решающую роль.

- Северная Америка доминировала на рынке управления виртуальной инфраструктурой с наибольшей долей выручки в 37,82% в 2024 году, что обусловлено высоким уровнем внедрения облачных сервисов, широкой цифровой трансформацией в различных отраслях и присутствием ключевых поставщиков технологий.

- Ожидается, что Азиатско-Тихоокеанский регион станет свидетелем самых высоких темпов роста мирового рынка управления виртуальной инфраструктурой, что обусловлено ростом проникновения Интернета, быстрым ростом электронной коммерции и телекоммуникационных секторов, а также государственными инициативами, поддерживающими цифровую трансформацию и развитие умных городов в таких странах, как Китай, Индия и Япония.

- Сегмент решений доминировал на рынке, обеспечив наибольшую долю выручки в 61,4% в 2024 году. Это обусловлено растущим спросом на централизованное управление инфраструктурой и автоматизацию в облачных и виртуальных средах. Организации активно инвестируют в масштабируемые и интеллектуальные платформы управления для поддержки сложных гибридных ИТ-архитектур. Быстрое внедрение виртуализации в центрах обработки данных дополнительно повысило спрос на надежные решения, обеспечивающие мониторинг в режиме реального времени, оркестровку и оптимизацию производительности.

Область применения отчета и сегментация рынка менеджеров виртуальной инфраструктуры

|

Атрибуты |

Ключевые аналитики рынка Virtual Infrastructure Manager |

|

Охваченные сегменты |

|

|

Охваченные страны |

Северная Америка

Европа

Азиатско-Тихоокеанский регион

Ближний Восток и Африка

Южная Америка

|

|

Ключевые игроки рынка |

|

|

Рыночные возможности |

|

|

Информационные наборы данных с добавленной стоимостью |

Помимо информации о рыночных сценариях, таких как рыночная стоимость, темпы роста, сегментация, географический охват и основные игроки, рыночные отчеты, подготовленные Data Bridge Market Research, также включают в себя углубленный экспертный анализ, географически представленные данные о производстве и мощностях компаний, схемы сетей дистрибьюторов и партнеров, подробный и обновленный анализ ценовых тенденций и анализ дефицита цепочки поставок и спроса. |

Тенденции рынка виртуальных инфраструктурных менеджеров

«Расширение интеграции искусственного интеллекта (ИИ) и машинного обучения (МО) в управлении инфраструктурой»

- Искусственный интеллект и машинное обучение (ИИ) всё чаще внедряются в платформы управления виртуальной инфраструктурой для автоматизации рутинных задач, управления рабочими нагрузками и снижения зависимости от человека в масштабных средах. Эти технологии помогают оптимизировать сложные процессы, сократить время отклика и обеспечить единообразие управления производительностью в крупных цифровых инфраструктурах.

- Эти технологии повышают надежность системы благодаря аналитике в реальном времени, автоматизированной диагностике и обнаружению аномалий. Такие возможности помогают организациям выявлять и устранять проблемы заблаговременно, значительно сокращая время простоя инфраструктуры и улучшая непрерывность обслуживания конечных пользователей.

- AI-driven workload balancing enables dynamic allocation of compute, storage, and network resources based on changing demand across cloud ecosystems. This ensures cost efficiency, prevents resource underutilization or overload, and improves system responsiveness for critical applications

- Predictive maintenance powered by ML algorithms is helping enterprises identify performance bottlenecks, hardware degradation, and failure trends before they impact operations. This proactive approach improves infrastructure stability, reduces emergency repairs, and enhances long-term business continuity planning

- For instance, IBM’s Turbonomic platform uses AI to analyze application performance in real time and automatically manage infrastructure resources. It helps enterprises ensure that applications always receive the compute and memory they need, without manual intervention or over-provisioning

Virtual Infrastructure Manager Market Dynamics

Driver

“Surging Demand for Network Function Virtualization (NFV) and Cloud-native Applications”

- The rise of NFV is enabling telecom and enterprise networks to shift from hardware-based functions to virtualized solutions for improved flexibility. By virtualizing network services such as routing, switching, and security, organizations are reducing operational costs and enhancing service agility

- Cloud-native applications built on microservices and containers require dynamic orchestration and scaling across cloud platforms. Virtual infrastructure managers play a critical role by automating container placement, managing storage demands, and balancing resource consumption

- NFV allows decoupling of hardware from software, accelerating service rollout and simplifying network updates without physical reconfigurations. This transformation is helping telecom operators respond faster to customer demands while minimizing capital expenditure on legacy hardware

- Virtual infrastructure managers help reduce operational complexity in hybrid and multi-tenant environments by automating resource provisioning and monitoring. They provide centralized control over infrastructure layers, improving visibility and performance management across distributed systems

- For instance, Red Hat’s OpenStack Platform enables NFV infrastructure by using virtual infrastructure managers for high availability and efficient orchestration. This supports telecom operators in delivering scalable, automated services with better uptime and resource optimization

Restraint/Challenge

“Complexity in Integration with Legacy Infrastructure”

- Many legacy systems lack the APIs, software support, or compatibility needed to work with modern virtual infrastructure managers. This leads to prolonged integration timelines, higher costs, and greater risks during the migration from traditional to cloud-based environments

- Transitioning from hardware-centric data centers to software-defined infrastructure requires a major investment in tools and training. The disruption during migration may temporarily impact critical business operations and reduce productivity during the adjustment period

- A key challenge is the shortage of professionals skilled in both legacy technologies and modern virtualization platforms. This talent gap increases the burden on IT departments and slows down successful adoption of virtual infrastructure management tools

- Legacy systems often operate on outdated protocols, file formats, and incompatible security configurations. Integrating them with AI-optimized cloud systems can expose vulnerabilities, increase complexity, and require custom integration efforts

- For instance, hospitals operating legacy EMR systems find it difficult to align with modern infrastructure platforms due to data incompatibility and compliance issues. These limitations delay digital upgrades, hinder cloud adoption, and slow innovation in mission-critical healthcare environments

Virtual Infrastructure Manager Market Scope

The market is segmented on the basis of offering, development, and end-user.

• By Offering

On the basis of offering, the virtual infrastructure manager market is segmented into solution and services. The solution segment dominated the market with the largest revenue share of 61.4% in 2024, driven by the increasing demand for centralized infrastructure management and automation across cloud and virtual environments. Organizations are investing heavily in scalable and intelligent management platforms to support complex, hybrid IT architectures. The rapid adoption of virtualization in data centers has further boosted demand for robust solutions that offer real-time monitoring, orchestration, and performance optimization.

The services segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by growing reliance on managed services and system integration. As businesses navigate digital transformation, the need for consulting, deployment, and support services continues to rise, especially among small and medium enterprises lacking internal IT expertise.

• By Development

On the basis of development, the market is segmented into Infrastructure as a Service (IaaS) and on-premises. The IaaS segment held the largest market revenue share in 2024, driven by the surge in cloud computing and increasing need for scalable infrastructure solutions. IaaS offers flexibility, reduced hardware dependency, and cost-effective deployment models, which are essential for enterprises operating in dynamic digital ecosystems.

Ожидается, что сегмент локальных решений будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, чему будет способствовать спрос со стороны таких строго регулируемых отраслей, как банковское дело и здравоохранение. Эти секторы предпочитают локальное развертывание, чтобы сохранить контроль над конфиденциальными данными и соответствовать строгим стандартам управления, особенно в регионах со строгими законами о резидентстве данных.

• Конечным пользователем

По типу конечного пользователя рынок сегментируется на следующие сферы: ИТ и телекоммуникации, банковское дело, финансовые услуги и страхование (BFSI), здравоохранение, производство, розничная торговля и другие. Сегмент ИТ и телекоммуникаций доминировал на рынке в 2024 году, во многом благодаря росту инвестиций в облачные технологии и виртуализацию для управления сетевыми функциями. Зависимость этого сектора от постоянной доступности и высокопроизводительной инфраструктуры ускорила внедрение систем управления виртуальной инфраструктурой.

Ожидается, что сектор здравоохранения будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, что обусловлено цифровизацией медицинских карт пациентов, развитием телемедицины и потребностью в безопасной и гибкой инфраструктуре. Менеджеры виртуальной инфраструктуры помогают оптимизировать операции, обеспечивать соблюдение требований конфиденциальности данных и поддерживать масштабируемые решения для хранения и обработки медицинских данных.

Региональный анализ рынка менеджеров виртуальной инфраструктуры

- Северная Америка доминировала на рынке управления виртуальной инфраструктурой с наибольшей долей выручки в 37,82% в 2024 году, что обусловлено высоким уровнем внедрения облачных сервисов, широкой цифровой трансформацией в различных отраслях и присутствием ключевых поставщиков технологий.

- Предприятия региона уделяют первостепенное внимание масштабируемости инфраструктуры и бесперебойности ИТ-операций, делая менеджеров виртуальной инфраструктуры неотъемлемой частью повышения эффективности, снижения эксплуатационных расходов и усиления безопасности данных.

- Сильная технологическая экосистема в сочетании с ранним внедрением моделей «инфраструктура как услуга» (IaaS) поддерживает рост рынка в таких секторах, как банковское дело, здравоохранение и телекоммуникации.

Обзор рынка менеджеров виртуальной инфраструктуры в США

Рынок систем управления виртуальной инфраструктурой США в 2024 году занял наибольшую долю выручки в Северной Америке – 79%, в первую очередь благодаря быстрому развитию облачных приложений и платформ виртуализации. Растущий спрос на централизованный контроль, автоматизацию и эффективное управление ресурсами стимулирует внедрение решений как в частном, так и в государственном секторе. Кроме того, растущая потребность в гибридной облачной инфраструктуре и модернизации центров обработки данных побуждает организации интегрировать передовые системы управления виртуальной инфраструктурой. Крупнейшие поставщики облачных услуг со штаб-квартирой в США также вносят свой вклад в инновации и доступность решений на рынке.

Обзор рынка менеджеров виртуальной инфраструктуры в Европе

Ожидается, что европейский рынок управления виртуальной инфраструктурой будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, что обусловлено стремительным ростом цифровизации предприятий и ужесточением законодательства о защите данных. Общий регламент по защите данных (GDPR) повысил спрос на безопасные и соответствующие требованиям решения для управления инфраструктурой. Такие страны, как Германия, Франция и Нидерланды, инвестируют в передовые технологии виртуализации для оптимизации ИТ-инфраструктуры. Регион также получает выгоду от мощной государственной поддержки внедрения облачных технологий и устойчивых ИТ-стратегий.

Анализ рынка менеджеров виртуальной инфраструктуры в Великобритании

Ожидается, что рынок управления виртуальной инфраструктурой в Великобритании будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, чему будет способствовать развитие цифровой экономики и увеличение инвестиций в ИТ в банковском и финансовом секторах, розничной торговле и здравоохранении. Спрос на гибкие, масштабируемые платформы виртуальной инфраструктуры обусловлен необходимостью оптимизации операций и поддержки удалённой работы. Присутствие ведущих поставщиков облачных решений и динамичной экосистемы технологических стартапов дополнительно стимулирует рост рынка в стране.

Обзор рынка менеджеров виртуальной инфраструктуры в Германии

Ожидается, что рынок управления виртуальной инфраструктурой в Германии будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год благодаря развитому промышленному сектору и мощной ИТ-инфраструктуре. Приверженность страны концепциям Индустрии 4.0 и цифрового производства стимулирует внедрение виртуализированной инфраструктуры в обрабатывающей промышленности и машиностроении. Немецкие предприятия также инвестируют в локальные и гибридные облачные модели, что требует эффективных инструментов управления инфраструктурой, поддерживающих масштабируемость, целостность данных и автоматизацию операций.

Обзор рынка менеджеров виртуальной инфраструктуры в Азиатско-Тихоокеанском регионе

Ожидается, что рынок систем управления виртуальной инфраструктурой в Азиатско-Тихоокеанском регионе будет демонстрировать самые высокие темпы роста в период с 2025 по 2032 год, чему будет способствовать цифровой бум в развивающихся странах, таких как Индия, Китай и страны Юго-Восточной Азии. Основными драйверами роста являются более широкое внедрение облачных вычислений, распространение центров обработки данных и государственные инициативы, поддерживающие цифровую трансформацию. По мере того, как всё больше малых и средних предприятий (МСП) переходят на облачную инфраструктуру, растёт спрос на гибкие и экономичные системы управления виртуальной инфраструктурой.

Обзор рынка менеджеров виртуальной инфраструктуры в Японии

The Japan virtual infrastructure manager market is expected to witness the fastest growth rate from 2025 to 2032, supported by widespread digital transformation in the healthcare, financial, and manufacturing sectors. Japan’s strong focus on innovation, automation, and resilience in IT operations is fostering the integration of advanced virtualization tools. Enterprises are leveraging virtual infrastructure managers to increase uptime, optimize performance, and ensure security compliance across diverse workloads. The rising popularity of containerization and edge computing is also influencing market dynamics.

China Virtual Infrastructure Manager Market Insight

The China virtual infrastructure manager market accounted for the largest revenue share in Asia-Pacific in 2024, driven by an explosion in data generation, cloud usage, and smart city development. The government's focus on digital infrastructure, along with the presence of domestic cloud giants such as Alibaba Cloud and Tencent Cloud, is accelerating the deployment of virtual infrastructure managers. These tools are being widely adopted across e-commerce, financial services, and telecommunications to enable real-time scalability, automation, and resource efficiency.

Virtual Infrastructure Manager Market Share

The virtual infrastructure manager industry is primarily led by well-established companies, including:

- SolarWinds Worldwide, LLC (U.S.)

- Ciena Corporation (U.S.)

- Ribbon Communications Operating Company, Inc. (U.S.)

- Corsa Technology Inc. (Canada)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Broadcom (U.S.)

- Fujitsu (Japan)

- IBM Corporation (U.S.)

- Nokia (Finland)

- NetApp (U.S.)

- Enterprise Management Associates, Inc. (U.S.)

- Virtual Open Systems SAS (France)

- HashRoot Ltd. (India)

- Netedge Technology (India)

- Datanetiix Solutions Inc. (U.S.)

- Paessler AG (Germany)

- Micropro (India)

- eG Innovations (U.S.)

- Zuci (U.S.)

Latest Developments in Global Virtual Infrastructure Manager Market

- In September 2023, Corsa Technology Inc. partnered with Eventus Security, India's leading Managed Security Services Provider. Eventus expanded its managed security services portfolio through this collaboration by adopting Corsa Security's hosted and managed virtual firewall service. Utilizing the Corsa Security Orchestrator (CSO) and software firewalls from top vendors, Eventus achieved rapid service delivery, providing customers with flexible firewall capacity and tailored security services to meet their specific needs

- In October 2023, Ciena Corporation showcased groundbreaking Open Broadband Solutions and expertise at Network X 2023 during the Broadband Forum (BBF) and CloudCo Proof of Concept. The demonstration highlighted Ciena's virtual Broadband Network Gateway (vBNG) and Secure Service Edge (SSE) capabilities within a Secure Access Service Edge (SASE) framework, delivering edge security for residential and small businesses. Featured use cases included secure high-speed internet as an overlay service with spam filtering and DDoS protection. This benefits the company to expand its product and solution portfolio and thus increase revenue

- In May 2023, Telefonaktiebolaget LM Ericsson achieved the FutureNet World Network Sustainability Award for its Predictive Cell Energy Management (PCEM) solution. Recognized for reducing energy consumption without compromising service quality, PCEM is a key component of Ericsson's Energy Infrastructure Operations offering. This multi-vendor, multi-technology application optimizes energy usage at the cell level, ensuring network quality and customer experience. This benefits the company by boosting its image in the IT industry

- In January 2023, Micropro emerged victorious at the Digital India Awards, a prestigious accolade presented by the Ministry of Electronics and Information Technology, Government of India. The award recognizes excellence in e-governance initiatives and underscores Micropro's outstanding contributions to India's digital transformation. This benefits the company to boost its image in the region

- In August 2022, SolarWinds Worldwide, LLC was acknowledged in GigaOm Radar Reports as a Leader in Network and Cloud Observability for 2022. The company's hybrid and multi-cloud observability solutions earned praise for enhancing enterprise visibility, intelligence, and productivity in today's distributed network environments. GigaOm's recognition positioned SolarWinds as a Leader and Outperformer in Network Observability and a Leader and Fast Mover in Cloud Observability Solutions for 2022. The evaluations were based on technical capabilities, product roadmap, innovation, and execution prowess. This benefits the company by accelerating its digital transformation efforts and adopting a proactive IT posture

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.