Global Wholesale And Distribution Automotive After Market

Taille du marché en milliards USD

TCAC :

%

USD

221.32 Billion

USD

339.66 Billion

2025

2033

USD

221.32 Billion

USD

339.66 Billion

2025

2033

| 2026 –2033 | |

| USD 221.32 Billion | |

| USD 339.66 Billion | |

| % | |

|

Segmentation du marché mondial de la vente en gros et de la distribution automobile, par type de pièce de rechange (pneus, batteries, pièces de freinage, filtres, pièces de carrosserie, composants d'éclairage et électroniques, roues, composants d'échappement et autres), certification (pièces d'origine, pièces certifiées et pièces non certifiées), canal de distribution (détaillants, grossistes et distributeurs), canal de service (bricolage, réparation par un professionnel et équipementiers) - Tendances du secteur et prévisions jusqu'en 2033

Taille du marché de gros et de distribution automobile

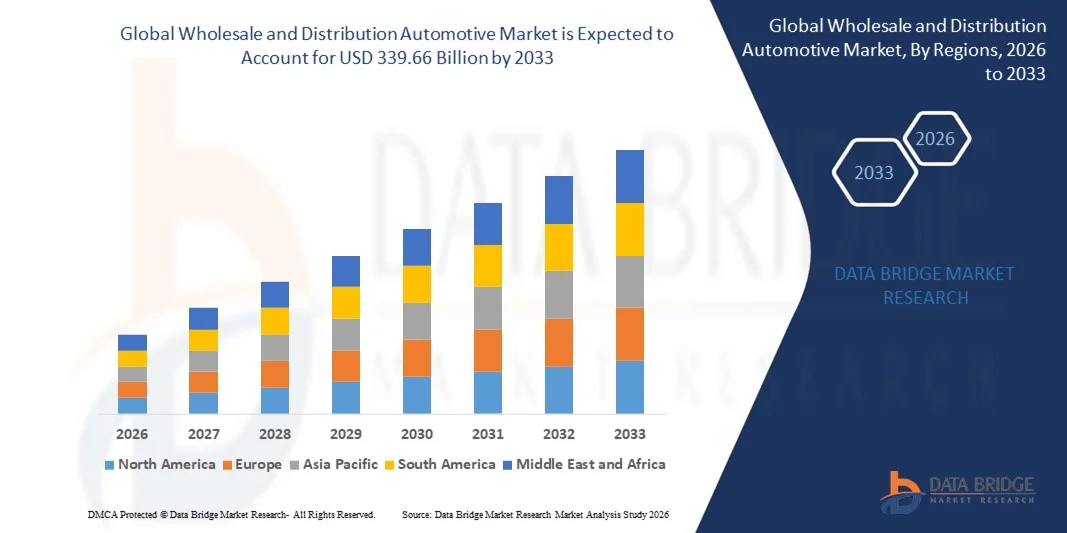

- Le marché mondial de la vente en gros et de la distribution automobile était évalué à 221,32 milliards de dollars en 2025 et devrait atteindre 339,66 milliards de dollars d'ici 2033 , avec un TCAC de 5,50 % au cours de la période de prévision.

- La croissance du marché est largement alimentée par la demande croissante de pièces automobiles de rechange, l'expansion des plateformes de commerce électronique pour la distribution automobile et la croissance du parc automobile dans les économies émergentes.

- De plus, l'adoption croissante des véhicules électriques et le besoin en composants et pièces spécialisés stimulent davantage la croissance du marché.

Analyse du marché automobile de gros et de distribution

- Le marché connaît une transformation grâce à l'intégration des canaux de distribution numériques, à l'optimisation de la chaîne d'approvisionnement et aux solutions avancées de gestion des stocks.

- Le renforcement des collaborations entre fabricants, distributeurs et détaillants améliore la disponibilité et l'efficacité de la livraison des pièces automobiles, consolidant ainsi l'ensemble du marché.

- L'Amérique du Nord a dominé le marché de la distribution automobile en gros avec la plus grande part de revenus (25,3 %) en 2025, grâce à une industrie automobile bien établie, une forte demande sur le marché de l'après-vente et une adoption généralisée des canaux de distribution numériques.

- La région Asie-Pacifique devrait connaître le taux de croissance le plus élevé sur le marché mondial de la vente en gros et de la distribution automobile , grâce à l'augmentation du parc automobile, la hausse des revenus disponibles, l'adoption croissante des services après-vente et l'expansion de réseaux logistiques et de distribution efficaces dans les économies émergentes.

- Le segment des pneumatiques a représenté la plus grande part de chiffre d'affaires du marché en 2025, grâce à une fréquence de remplacement élevée, à l'utilisation généralisée des véhicules et à une demande croissante de pneumatiques durables et performants. Les pneumatiques sont essentiels à la sécurité et à l'efficacité des véhicules, ce qui en fait un enjeu majeur pour les distributeurs et les détaillants.

Portée du rapport et segmentation du marché automobile de gros et de distribution

|

Attributs |

Aperçus clés du marché de la vente en gros et de la distribution automobile |

|

Segments couverts |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Wholesale and Distribution Automotive Market Trends

Rising Demand for E-Commerce and Efficient Distribution Channels

- The growing focus on digital sales platforms and streamlined supply chains is significantly shaping the wholesale and distribution automotive market, as businesses increasingly prefer channels that offer faster delivery, wider product selection, and reliable inventory management. Online and omnichannel distribution solutions are gaining traction due to their ability to reduce operational costs, improve service efficiency, and enhance customer satisfaction, encouraging distributors to adopt innovative logistics and digital tools

- Increasing awareness around vehicle maintenance, aftermarket parts availability, and convenient ordering options has accelerated the adoption of wholesale and distribution automotive services in passenger vehicles, commercial vehicles, and specialty segments. Consumers and fleet operators are actively seeking faster, more accessible channels for spare parts and accessories, prompting companies to strengthen partnerships with distributors and e-commerce platforms

- Technological advancements, such as AI-based inventory management, predictive analytics, and automated warehousing, are influencing purchasing decisions, with distributors emphasizing faster turnaround times, transparent supply chains, and real-time tracking. These factors help automotive companies differentiate themselves in a competitive market while improving operational efficiency and customer satisfaction

- For instance, in 2024, AutoZone in the U.S. and LKQ Corporation expanded their digital distribution networks and integrated e-commerce platforms for spare parts and accessories. These initiatives were introduced in response to rising demand for faster, more convenient parts delivery and wider product availability, with distribution across retail stores, online marketplaces, and fleet servicing channels

- While demand for efficient wholesale and distribution channels is growing, sustained market expansion depends on continuous investment in logistics infrastructure, digital platforms, and supply chain reliability. Companies are also focusing on optimizing inventory management, delivery networks, and order fulfillment to balance cost, speed, and service quality for broader adoption

Wholesale and Distribution Automotive Market Dynamics

Driver

Growing Adoption of E-Commerce And Omnichannel Distribution

- Rising demand for faster, more convenient ordering and delivery solutions is a major driver for the wholesale and distribution automotive market. Distributors are increasingly integrating online platforms with traditional retail networks to meet consumer expectations, improve product availability, and expand market reach

- Expanding automotive aftermarket, fleet management, and replacement parts segments are influencing market growth. Efficient distribution channels help ensure timely delivery, reduce downtime, and maintain vehicle performance, meeting the increasing demand for high-quality parts and services

- Automotive manufacturers and distributors are actively promoting digital sales and streamlined supply chains through partnerships, technology adoption, and improved logistics. These efforts are supported by growing vehicle ownership, urbanization, and the shift toward connected and electric vehicles, which require specialized distribution solutions

- For instance, in 2023, Advance Auto Parts in the U.S. and Brembo in Italy reported enhanced distribution efficiency by integrating digital order tracking and warehouse automation. This expansion followed higher demand for timely delivery of automotive parts and accessories, strengthening customer satisfaction and loyalty

- Although rising e-commerce and omnichannel adoption support growth, wider market penetration depends on logistics optimization, cost management, and technological investments. Investment in warehouse automation, AI-enabled inventory tracking, and robust delivery networks will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

High Operational Costs And Complex Supply Chain Management

- The relatively high operational cost of maintaining extensive distribution networks, warehousing, and last-mile delivery remains a key challenge, limiting profitability for some distributors. Rising fuel costs, labor expenses, and technology investments contribute to elevated operating costs

- Market awareness and digital adoption remain uneven, particularly in emerging economies where online and omnichannel distribution is still developing. Limited understanding of e-commerce and logistics efficiency restricts market growth in certain regions

- Supply chain complexities also impact market expansion, as automotive parts distribution requires coordination among manufacturers, wholesalers, retailers, and service providers. Delays, inventory mismanagement, and logistical inefficiencies can affect service quality and customer satisfaction

- For instance, in 2024, distributors in India and Southeast Asia supplying aftermarket parts to automotive service providers reported slower growth due to high operational costs and limited digital adoption. Infrastructure limitations and fragmented supply networks were additional barriers, affecting timely delivery and market reach

- Overcoming these challenges will require investment in cost-efficient logistics, digital supply chain platforms, and education for distributors and retailers. Collaboration with manufacturers, e-commerce platforms, and fleet operators can help unlock the long-term growth potential of the global wholesale and distribution automotive market. Furthermore, optimizing delivery networks and inventory management will be essential for widespread adoption

Wholesale and Distribution Automotive Market Scope

The market is segmented on the basis of replacement part, certification, distribution channel, and service channel.

- By Replacement Part

On the basis of replacement part, the wholesale and distribution automotive market is segmented into tire, battery, brake parts, filters, body parts, lighting and electronic components, wheels, exhaust components, and others. The tire segment held the largest market revenue share in 2025, driven by high replacement frequency, widespread vehicle usage, and increasing demand for durable and performance-oriented tires. Tires are essential for vehicle safety and efficiency, making them a key focus for distributors and retailers.

The battery segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising adoption of electric vehicles and hybrid vehicles, which require frequent replacement and advanced battery technologies. Battery replacement demand is further fueled by consumer preference for longer-lasting, high-capacity batteries and the increasing use of battery management systems in modern vehicles.

- By Certification

On the basis of certification, the market is segmented into genuine parts, certified parts, and uncertified parts. The genuine parts segment held the largest market revenue share in 2025, fueled by consumer preference for original equipment manufacturer (OEM) quality, reliability, and warranty assurance. Genuine parts are widely sought after by vehicle owners and service centers to maintain vehicle performance and safety standards.

The certified parts segment is expected to witness the fastest growth rate from 2026 to 2033, driven by regulatory compliance requirements, rising awareness of safety standards, and the increasing availability of certified aftermarket components. Certified parts offer verified quality and performance while often being more cost-effective than OEM parts.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into retailers, wholesalers, and distributors. The retailers segment held the largest revenue share in 2025, driven by the accessibility of automotive parts to end consumers, the expansion of retail networks, and growing online sales channels. Retailers often combine physical stores and e-commerce platforms to provide convenient purchasing options.

The distributors segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the increasing demand for bulk supply, fleet management services, and partnerships with automotive manufacturers. Distributors provide efficient supply chain solutions and enable wider market penetration for replacement parts.

- By Service Channel

On the basis of service channel, the market is segmented into DIY, DIFM (Do It For Me), and OEM. The DIFM segment held the largest market revenue share in 2025, driven by vehicle owners’ preference for professional installation, convenience, and assurance of proper fitment and performance. DIFM services are commonly offered by service centers, workshops, and dealerships.

The DIY segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing trend of vehicle owners performing minor repairs and replacements themselves, supported by online tutorials, instructional content, and availability of easy-to-install parts.

Wholesale and Distribution Automotive Market Regional Analysis

- North America dominated the wholesale and distribution automotive market with the largest revenue share of 25.3% in 2025, driven by a well-established automotive industry, strong aftermarket demand, and high adoption of digital distribution channels

- Businesses in the region highly value efficient supply chain management, reliable inventory availability, and fast delivery services offered by wholesalers and distributors, ensuring timely access to replacement parts and automotive components

- This widespread adoption is further supported by robust infrastructure, advanced logistics networks, and a strong focus on fleet management and service quality, establishing wholesale and distribution channels as a preferred solution for automotive parts in both commercial and retail segments

U.S. Wholesale and Distribution Automotive Market Insight

The U.S. wholesale and distribution automotive market captured the largest revenue share in 2025 within North America, fueled by increasing vehicle parc, rising demand for aftermarket parts, and the growing trend of online automotive sales. Businesses are prioritizing faster, reliable access to replacement components through integrated distribution networks. The expansion of e-commerce platforms, coupled with advanced inventory management systems and fleet servicing solutions, further propels the market. Moreover, partnerships between distributors, retailers, and manufacturers enhance availability and operational efficiency, significantly contributing to market growth.

Europe Wholesale and Distribution Automotive Market Insight

The Europe wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by regulatory requirements for quality and safety, increasing vehicle ownership, and demand for timely delivery of replacement parts. Urbanization, coupled with the growth of connected vehicle technologies, is fostering the adoption of advanced distribution solutions. European businesses are also investing in digital supply chain platforms to ensure seamless procurement and distribution across retail and commercial segments.

U.K. Wholesale and Distribution Automotive Market Insight

The U.K. wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for aftermarket parts, fleet management services, and e-commerce-based distribution. Concerns over vehicle downtime and the need for prompt maintenance are encouraging businesses and individual consumers to rely on professional distributors and wholesalers. The country’s well-developed logistics and retail infrastructure, alongside increasing online sales penetration, is expected to continue supporting market growth.

Germany Wholesale and Distribution Automotive Market Insight

The Germany wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s large automotive manufacturing base, high-quality standards, and advanced logistics networks. Businesses in Germany are increasingly adopting integrated inventory management, automated warehousing, and digital ordering solutions to enhance distribution efficiency. The emphasis on timely delivery, sustainability in logistics, and operational optimization supports market adoption across commercial and retail segments.

Asia-Pacific Wholesale and Distribution Automotive Market Insight

The Asia-Pacific wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, rising vehicle sales, and expansion of automotive aftermarket infrastructure in countries such as China, Japan, and India. Growing urbanization, increasing disposable incomes, and technological advancements in logistics and e-commerce platforms are driving the adoption of efficient distribution solutions. Furthermore, APAC’s emergence as a manufacturing hub for automotive components enhances affordability and accessibility of replacement parts across the region.

Japan Wholesale and Distribution Automotive Market Insight

The Japan wholesale and distribution automotive market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s high vehicle ownership, demand for efficient fleet management, and adoption of digital supply chain solutions. Japanese businesses increasingly rely on distributors and wholesalers for timely access to replacement parts, ensuring minimal downtime and operational efficiency. Integration of automated inventory management, predictive ordering, and e-commerce channels is fueling growth, while aging population trends also boost demand for easy-to-access automotive services.

China Wholesale and Distribution Automotive Market Insight

The China wholesale and distribution automotive market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding automotive industry, rapidly growing vehicle parc, and rising demand for aftermarket services. China is one of the largest markets for replacement parts and automotive components, with wholesalers and distributors playing a critical role in ensuring availability across retail, commercial, and fleet segments. Government initiatives promoting digitalization, expansion of e-commerce channels, and local manufacturing capabilities are key factors propelling market growth.

Wholesale and Distribution Automotive Market Share

The Wholesale and Distribution Automotive industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- DENSO CORPORATION (Japan)

- Tenneco Inc. (U.S.)

- Marelli Holdings Co., Ltd. (Japan)

- Robert Bosch GmbH (Germany)

- The Goodyear Tire and Rubber Company (U.S.)

- ZF Friedrichshafen AG (Germany)

- Cooper Tire and Rubber Company (U.S.)

- LEMANS CORPORATION (U.S.)

- Motorsport Aftermarket Group (U.S.)

- Textron Inc. (U.S.)

- Western Power Sports, Inc. (U.S.)

- Polaris Inc. (U.S.)

- AISIN SEIKI Co., Ltd. (Japan)

- Deere and Company (U.S.)

- BRP (Canada)

Latest Developments in Global Wholesale and Distribution Automotive Market

- En juillet 2023, General Motors Co. a finalisé l'acquisition de la start-up israélienne ALGOLiON Ltd., spécialisée dans les logiciels pour batteries. Cette opération stratégique, pilotée par l'équipe Technologies Acceleration and Commercialization (TAC) de GM, vise à renforcer les capacités de développement de batteries de GM grâce à des solutions logicielles avancées. Cette acquisition consolide la position de GM dans le domaine des technologies pour véhicules électriques et favorise une innovation plus rapide en matière de performance, d'efficacité et de gestion de l'énergie des batteries, contribuant ainsi positivement au marché des véhicules électriques.

- En juin 2023, Continental AG a lancé l'UltraContact NXT, son pneu le plus respectueux de l'environnement à ce jour. Composé jusqu'à 65 % de matériaux recyclés, renouvelables et certifiés conformes aux normes d'équilibre massique, ce pneu offre une sécurité et des performances optimales tout en réduisant l'impact environnemental. Ce lancement renforce la stratégie de développement durable de Continental et répond aux attentes des consommateurs soucieux de l'environnement, consolidant ainsi sa compétitivité sur le marché des solutions de mobilité verte.

- En mai 2023, Stellantis NV s'est associée à Petromin en Arabie saoudite pour lancer la gamme Eurorepar de pièces automobiles et de produits d'entretien. Cette collaboration améliore l'accès à l'entretien des véhicules et soutient les initiatives de sécurité routière. En proposant une gamme de pièces fiables, Stellantis renforce sa présence sur le marché de l'après-vente et étend sa portée commerciale au Moyen-Orient.

- En février 2023, Continental AG a lancé le pneu été CrossContact H/T, conçu pour une utilisation polyvalente sur routes pavées et non pavées. Adapté aux véhicules conventionnels et électriques, ce pneu allie robustesse, confort et sécurité, et bénéficie notamment d'un homologation M+S pour une utilisation hors route modérée. Ce lancement enrichit la gamme de produits Continental et répond à la demande des consommateurs pour des pneus polyvalents et performants.

- En mars 2023, BorgWarner Inc. a lancé des disques de frein bimétalliques plus légers, plus silencieux et plus économes en carburant que les disques traditionnels en fonte. Leur conception en alliage bi-matière permet un gain de poids de 15 %, améliorant ainsi le rendement énergétique et réduisant les émissions, tout en minimisant les vibrations et le bruit pour un confort de conduite accru. Cette innovation optimise les performances et la durabilité des véhicules, renforçant la position concurrentielle de BorgWarner sur le marché des composants de freinage.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.