India Sbs Polymer Market

Taille du marché en milliards USD

TCAC :

%

USD

342.62 Million

USD

523.04 Million

2025

2033

USD

342.62 Million

USD

523.04 Million

2025

2033

| 2026 –2033 | |

| USD 342.62 Million | |

| USD 523.04 Million | |

| % | |

|

Inde SBS segmentation du marché des polymères, par produit (SBS linéaire et SBS radial/SBS étoilé [R-SBS]), par type (SBS non-huile étendue et SBS à huile élargie), teneur en styrène (SBS bas styrène, SBS styrène moyen et SBS styrène élevé), application (modification de l'asphalte, mastics routiers, semelles de chaussures et composants de chaussures, bitumen modifié par des polymères, adhésifs et scellants, produits chimiques de la construction, membrane de toiture, etc.), utilisateur final (industrie de la chaussure, construction de routes et infrastructures, adhésifs et scellants, industrie automobile, construction, industrie de l'emballage, etc.), canal de distribution (direct et indirect) - tendances et prévisions de l'industrie jusqu'en 2033

Taille du marché des polymères SBS en Inde

- La taille du marché indien des polymères SBS a été évaluée à523,04 millions de dollars en 2033de342,62 millions de dollars en 2026, croissance avec unTCAC de 5,6%pendant la période de prévision

- Le marché indien des polymères SBS connaît une croissance régulière, en raison de la demande croissante des industries d'utilisation finale comme la construction, l'automobile, les chaussures, les adhésifs et les produits d'étanchéité, et de la modification des polymères, soutenue par l'urbanisation rapide et le développement des infrastructures.

- Les investissements croissants dans la construction de routes, la toiture et les applications d'imperméabilisation, ainsi que la croissance des emballages souples et des biens de consommation, contribuent de façon significative à l'augmentation de la consommation de polymères SBS dans tout le pays.

- Les progrès réalisés dans les technologies de transformation des polymères, l'expansion des capacités de fabrication nationales et les initiatives gouvernementales de soutien dans le cadre des programmes d'infrastructure et de fabrication améliorent l'efficacité de la production et soutiennent l'évolutivité à long terme du marché.

Inde SBS Analyse du marché des polymères

- Le marché indien des polymères SBS connaît une croissance constante, en raison de l'augmentation de la demande liée à la construction, à l'automobile, à la chaussure, à l'adhésif et aux produits d'étanchéité ainsi qu'aux applications de modification des polymères, soutenues par le développement des infrastructures, l'urbanisation et l'utilisation croissante de matériaux de haute performance et flexibles dans toutes les industries.

- En 2026, le segment du SBS linéaire domine le marché, détenant une part de 64,31 %, en raison de son élasticité supérieure, de sa résistance à la traction élevée, de sa facilité de traitement et de son adoption généralisée dans les applications de modification de l'asphalte, d'adhésifs et d'étanchéité et de chaussures, où la performance et la durabilité sont essentielles.

- La prédominance du segment SBS linéaire est soutenue par son rapport coût-efficacité et une meilleure compatibilité avec une large gamme de polymères et de bitume, ce qui en fait le choix préféré pour les grandes infrastructures et les applications industrielles.

Portée du rapport et segmentation du marché indien des polymères SBS

| Attributs | Inde Protection Emballage Principales perspectives du marché |

| Segments couverts |

|

| Pays couverts |

|

| Principaux acteurs du marché |

|

| Possibilités de marché |

|

| Infos sur la valeur ajoutée | En plus des renseignements sur les scénarios du marché tels que la valeur marchande, le taux de croissance, la segmentation, la couverture géographique et les principaux intervenants, les rapports de marché établis par Data Bridge Market Research comprennent aussi l'analyse des exportations d'importations, l'aperçu des capacités de production, l'analyse de la consommation de production, l'analyse des tendances des prix, le scénario du changement climatique, l'analyse de la chaîne d'approvisionnement, l'analyse de la chaîne de valeur, l'aperçu des matières premières et des consommables, les critères de sélection des fournisseurs, l'analyse PESTLE, l'analyse Porter et le cadre réglementaire. |

Tendances du marché des polymères SBS en Inde

(en milliers de dollars)Adoption croissante de technologies avancées de modification et de traitement des polymères(en milliers de dollars)

- On adopte de plus en plus de techniques avancées de modification des polymères pour améliorer l'élasticité, la durabilité et la résistance thermique des polymères SBS, en soutenant leur utilisation dans des applications de haute performance telles que la modification de l'asphalte, la toiture et l'étanchéité.

- L'amélioration des techniques de composition et de mélange permet une meilleure compatibilité des polymères SBS avec le bitume et d'autres polymères, ce qui améliore la performance du produit et prolonge la durée de vie.

- L'automatisation et le contrôle de précision des systèmes de fabrication SBS améliorent l'efficacité, la cohérence et la qualité de la production tout en réduisant le gaspillage des matériaux et les coûts opérationnels.

- Le développement de qualités SBS personnalisées adaptées à certaines industries d'utilisation finale, y compris la construction, les adhésifs et les chaussures, gagne en traction pour répondre aux exigences de performance changeantes.

- L'intégration des systèmes numériques de surveillance et de contrôle de la qualité dans les installations de production favorise l'optimisation axée sur les données, la fiabilité des processus et l'évolutivité, renforçant ainsi la compétitivité globale du marché indien des polymères SBS.

Inde SBS Dynamique du marché des polymères

Chauffeur

Croissance élevée dans les principales industries d'utilisation finale

- L'expansion rapide des activités de construction et d'infrastructure dans toute l'Inde augmente considérablement la consommation de polymères SBS, en particulier dans les bitumes modifiés utilisés pour le revêtement des routes, les autoroutes, les ponts et les applications de toiture.

- Les investissements gouvernementaux à grande échelle dans les infrastructures de transport, le développement urbain et les projets de villes intelligentes ont conduit à une plus grande adoption du bitume modifié par les polymères, où le SBS est préféré pour sa capacité à améliorer l'élasticité, la résistance à la température et la durabilité à long terme.

- Dans le même temps, l'augmentation de la production de chaussures, soutenue par une consommation intérieure croissante et une fabrication axée sur l'exportation, stimule la demande de SBS dans les semelles et les composants de chaussures qui exigent flexibilité, résistance à l'abrasion et confort.

Par exemple:

- En mars 2022, selon l'article publié par la Scaff's India Trading Pvt. Ltd., les bardeaux et les membranes de toiture bitume modifiés par SBS offrent une flexibilité, une résistance aux chocs et une durabilité supérieures dans des conditions météorologiques extrêmes, ce qui les rend adaptés aux bâtiments et aux infrastructures modernes. L'adoption généralisée de solutions de toiture à base de SBS augmente directement la consommation de polymères, agissant ainsi comme un moteur clé de la croissance du marché indien des polymères SBS

- En novembre 2024, conformément à la recherche publiée par MDPI, Research mettant en évidence l'utilisation de bitume modifié par SBS à forte teneur pour améliorer la résistance à la rouille, la durée de vie de la fatigue, les performances de fissuration et la recyclabilité des chaussées souligne l'adoption croissante de matériaux avancés dans le développement des infrastructures. Alors que les initiatives de construction routière et de réduction du carbone axées sur la durabilité gagnent en traction, la demande d'asphalte à haute performance modifié par le SBS augmente, alimentant directement la croissance de la consommation et agissant comme un moteur clé pour le marché indien des polymères SBS.

- L'expansion de la fabrication automobile renforce encore l'utilisation du SBS dans des applications telles que les composants intérieurs, les joints et les mélanges de polymères, où les performances et la résilience sont essentielles. Parallèlement, la croissance régulière du secteur des adhésifs et des scellants, alimentée par la construction, l'emballage et l'assemblage industriel, augmente l'utilisation du SBS en raison de sa résistance supérieure au collage et de sa récupération élastique.

- Ensemble, la demande soutenue de ces industries d'utilisation finale à forte croissance entraîne directement une augmentation des volumes de consommation, une meilleure utilisation des capacités et une expansion continue du marché des polymères SBS en Inde.

Restriction/Défi

Pressions réglementaires et conformité environnementale

- Des réglementations de plus en plus strictes sur la production de polymères, les émissions et l'impact environnemental du cycle de vie posent des défis importants à la fabrication traditionnelle de SBS en Inde.

- Le respect de ces règles exige des fabricants qu'ils adoptent des technologies de pointe de réduction des émissions, optimisent la consommation d'énergie et assurent une manipulation et une élimination adéquates des produits chimiques intermédiaires. De plus, les vérifications environnementales, les exigences en matière de rapports et les pénalités pour non-conformité ajoutent à la complexité opérationnelle et augmentent les coûts de production.

Par exemple:

- En décembre 2024, selon l'article publié par Outlook Publishing India Pvt Ltd., au cours de négociations mondiales sur un traité juridiquement contraignant pour lutter contre la pollution plastique, l'Inde s'est opposée à la réglementation de la production de polymères plastiques primaires, citant des impacts potentiels sur les droits de développement et le commerce. Les pressions réglementaires internationales actuelles et l'incertitude entourant les futures limites de production de polymères accroissent les défis de conformité pour les fabricants de SBS, accroissant la complexité opérationnelle et agissant comme un frein clé à la croissance du marché indien des polymères SBS.

- En juin 2025, conformément à l'article publié par l'Institut d'économie de l'énergie et d'analyse financière, l'ONU négocie depuis 2022 un instrument international juridiquement contraignant (ILBI) pour réglementer la pollution plastique tout au long de son cycle de vie, y compris la production et le commerce de polymères. La résistance de pays comme l'Inde met en évidence le potentiel de restrictions futures sur les matières premières pétrochimiques et le commerce des polymères. L'évolution de la réglementation mondiale accroît la complexité de la conformité et l'incertitude opérationnelle, ce qui freine considérablement la croissance du marché indien des polymères SBS

- Les fabricants doivent également envisager la réduction de l'empreinte carbone et l'établissement de rapports sur la durabilité, qui nécessitent souvent des investissements dans des technologies plus propres ou d'autres matières premières.

- Ces pressions réglementaires limitent la flexibilité opérationnelle, augmentent les dépenses en capital et les dépenses opérationnelles et limitent l'augmentation rapide de la production de SBS, ce qui constitue un frein majeur à la croissance du marché indien des polymères SBS.

Possibilités

Demande croissante de l'industrie des véhicules électriques (EV)

- La croissance rapide du secteur des véhicules électriques (EV) en Inde entraîne une forte demande de matériaux légers et performants qui améliorent l'efficacité énergétique, la sécurité et la durabilité.

- Les polymères SBS, avec leur combinaison unique d'élasticité, de flexibilité et de stabilité thermique, sont de plus en plus utilisés dans les composants EV tels que l'isolation du câblage, l'encapsulation de la batterie, les joints, les joints et les pièces intérieures.

Par exemple:

- En octobre 2023, selon l'article publié par Science Direct, la demande croissante de matériaux légers, durables et ignifuges dans les véhicules électriques conduit à l'adoption de composites polymères haute performance. Les polymères SBS, avec élasticité, stabilité thermique et durabilité, sont idéaux pour développer des composants EV qui réduisent le poids, améliorent la sécurité et soutiennent des initiatives d'économie circulaire. Cette tendance crée d'importantes possibilités de croissance pour le marché indien des polymères SBS.

- En octobre 2025, tel que publié par India Brand Equity Foundation, l'Inde connaît une croissance rapide de l'écosystème des véhicules électriques, avec une augmentation de la demande intérieure et des investissements importants dans les véhicules électriques, les batteries et les composants automobiles, conduit à l'expansion de la fabrication locale. Des acteurs internationaux comme VinFast sont en train d'établir des pôles de production, stimulant la production de composants. Cette poussée de la production d'EV augmente le besoin de polymères légers et durables comme SBS, créant directement des opportunités de croissance pour le marché indien des polymères SBS

- Leur capacité à réduire le poids sans compromettre les performances mécaniques contribue à améliorer la portée du véhicule et l'efficacité énergétique, ce qui est crucial dans les applications d'EV. Alors que les constructeurs automobiles adoptent des polymères avancés pour les conceptions d'EV de nouvelle génération, les polymères SBS gagnent en pertinence industrielle, créant un potentiel de croissance important.

- Cette demande croissante de SBS dans les matériaux d'EV constitue une opportunité majeure d'expansion sur le marché indien des polymères SBS

Étendue du marché des polymères SBS en Inde

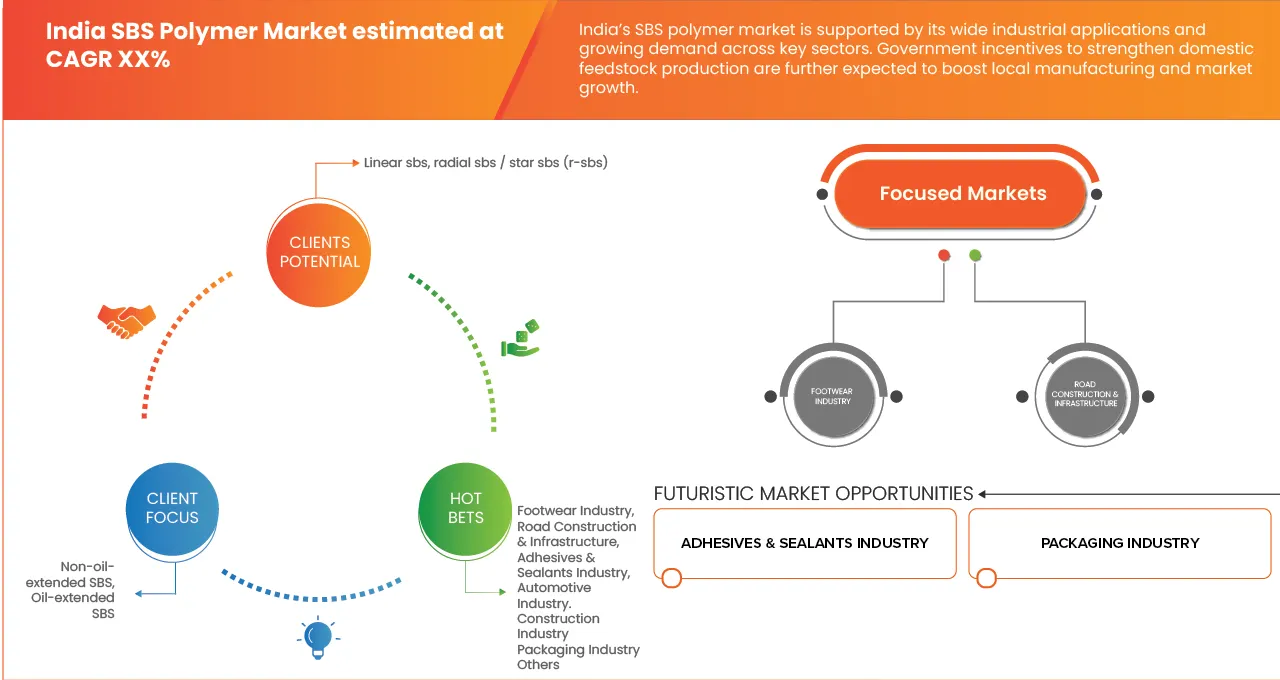

Le marché indien des polymères SBS est segmenté en six segments notables basés sur le produit, le type, le contenu styrène, l'application, l'utilisateur final et le canal de distribution.

- Par type de produit

Le segment du SBS linéaire domine le marché indien des polymères SBS et devrait représenter 64,31% de la part de marché totale en 2026. Sa domination est principalement attribuée à la disponibilité généralisée, à la rentabilité, à la structure moléculaire plus simple et à la facilité de traitement, ce qui rend le SBS linéaire très adapté aux applications à grande échelle et à grand volume telles que les composants de chaussures, les adhésifs à usage général et les matériaux de construction.

En plus de sa position dominante, le segment du SSE linéaire est également le segment qui connaît la croissance la plus rapide, et devrait croître à un TCAC de 5,4 % au cours de la période de prévision. Cette croissance rapide est soutenue par l'augmentation de la demande des industries de la construction et de la chaussure, l'utilisation croissante des adhésifs et des produits d'étanchéité, et par la préférence des fabricants pour les matériaux qui offrent un rendement de transformation et des avantages sur le plan des coûts.

- Par type

Le segment des SBS hors huile domine le marché indien des polymères SBS et devrait représenter 61,02% de la part de marché totale en 2026. Sa dominance est motivée par une résistance mécanique supérieure, une meilleure résistance à la déformation et une performance à long terme constante, ce qui la rend très adaptée aux projets de construction de routes et d'infrastructures où la durabilité et la fiabilité sont des exigences essentielles.

En plus de sa position dominante, le segment des SSE hors huile est également le segment qui connaît la croissance la plus rapide, et devrait croître à un TCAC de 5,8 % au cours de la période de prévision. La croissance est soutenue par l'augmentation des investissements dans le développement de l'autoroute, l'expansion des infrastructures urbaines et l'augmentation de la demande de bitume modifié par des polymères à haute performance, ce qui renforce encore son adoption dans les applications de construction à grande échelle.

- Par contenu styrène

Le segment du SBS à styrène moyen domine le marché des polymères du SBS en Inde et devrait représenter 69,93 % de la part de marché totale en 2026. Sa prédominance est attribuée à sa combinaison équilibrée de flexibilité et de rigidité, qui permet une large adoption dans de multiples applications, y compris les chaussures, les adhésifs, les matériaux de construction et la modification de l'asphalte.

En plus de sa position dominante, le segment SBS de Styrène moyen est également le segment qui connaît la croissance la plus rapide, et devrait croître à un TCAC de 5,7 % au cours de la période de prévision. Cette croissance est due à l'augmentation de la demande de grades SBS polyvalents, à l'expansion des activités d'infrastructure et de construction et à l'augmentation de l'utilisation dans la fabrication d'adhésifs et de chaussures, ce qui renforce les perspectives du marché.

- Par demande

Le segment des mastics routiers domine le marché indien des polymères SBS et devrait représenter 32,09 % de la part de marché totale en 2026. Sa domination est principalement motivée par la capacité des polymères SBS d'améliorer significativement la durabilité de la chaussée, la résistance à la fatigue et la durée de vie globale, faisant des mastics routiers une solution préférée pour les applications de construction et d'entretien routières à haute performance.

En plus de sa position dominante, le segment des mastics routiers est également le segment qui connaît la croissance la plus rapide, et devrait croître à un TCAC de 5,7 % au cours de la période de prévision. La croissance est soutenue par l'augmentation des investissements dans les infrastructures routières, les projets de modernisation des routes et la demande croissante de matériaux de chaussée durables, ce qui renforce encore l'adoption de polymères SBS dans les applications de mastics routiers.

- Par Utilisateur final

Le segment Construction de routes et infrastructures domine le marché indien des polymères SBS et devrait représenter 32,09 % de la part de marché totale en 2026. Sa prédominance est attribuable à la poursuite des investissements dans l'agrandissement des routes, la modernisation des routes urbaines et l'adoption croissante de matériaux modifiés par les polymères dans les projets d'infrastructure publique, où la durabilité et la longévité sont essentielles.

En plus de sa position dominante, le segment Construction de routes et infrastructures est également le segment qui connaît la croissance la plus rapide et qui devrait croître à un TCAC de 5,8 % au cours de la période de prévision. Cette croissance est soutenue par des initiatives gouvernementales de développement des infrastructures, l'accent étant mis de plus en plus sur la qualité des routes et la demande croissante d'asphalte et de matériaux de construction modifiés par le SBS, renforçant ainsi les perspectives du marché.

- Par canal de distribution

Le canal de distribution directe domine le marché indien des polymères SBS et devrait représenter 78,83 % de la part de marché totale en 2026. Sa domination repose sur l'acquisition directe par de grands entrepreneurs et fabricants, ce qui permet un meilleur contrôle des prix, une offre cohérente et une collaboration technique plus étroite avec les producteurs de polymères SBS.

En plus de sa position dominante, le canal de distribution directe est également le segment qui connaît la croissance la plus rapide et qui devrait croître à un TCAC de 5,6 % au cours de la période de prévision. La croissance est soutenue par une préférence croissante pour les accords d'approvisionnement à long terme, une augmentation de la demande découlant de projets d'infrastructure et d'industrie à grande échelle et la nécessité de solutions matérielles personnalisées, renforçant l'importance des circuits de vente directs sur le marché.

Inde SBS Part du marché des polymères

L'industrie SBS Polymer est principalement dirigée par des entreprises bien établies, notamment :

- DYCON CHIMIQUES (Inde)

- Kumho Petrochemical Co., Ltd. (Corée du Sud)

- DL Chemical (DL Holdings Co., Ltd.) (Corée du Sud)

- SBS POLYCHEM PVT. LTD. (Inde)

- Entec Polymers (États-Unis)

- LG Chem Ltd. (Corée du Sud)

- Reliance Industries Limited (Inde)

- Sinopec (Chine)

- LCY Chemical Corp. (Taiwan)

- Maxwell (États-Unis)

- Amaz Chemicals LLP (Inde)

- KK Kompounding Tech Giant Limited (Inde)

- Versalis S.p.A. (Italie)

- Moras Chemicals India Pvt Ltd (Inde)

- Société TSRC (Taiwan)

Derniers développements en Inde SBS Polymer Market

- En novembre 2025, Sinopec a signé des accords d'achat d'une valeur de 40,9 milliards de dollars américains avec 34 partenaires de 17 pays à travers le pétrole brut, les produits chimiques, les matériaux et l'équipement à la 8e China International Import Expo (CIIE 2025) - mettant l'accent sur la coopération internationale élargie, l'innovation numérique et les initiatives de résilience de la chaîne d'approvisionnement.

- En octobre 2024, LG Chem développe Automotive Adhesive Business Séoul – LG Chem a annoncé son intention d'étendre son activité d'adhésif automobile en une unité de plusieurs millions de dollars d'ici 2030, ciblant les constructeurs nord-américains avec des adhésifs thermoconducteurs pour batteries. La société étend également son portefeuille aux adhésifs pour composants électroniques, y compris les groupes motopropulseurs, les capteurs de caméras et les projecteurs.

- En septembre 2025, une nouvelle ligne de production SSBR (Solution-SBR) a été organisée à Shenhua Chemical, marquant le début de la construction d'une capacité de fabrication d'élastomère élargie en réponse à la demande mondiale croissante de matériaux de caoutchouc performants utilisés dans les pneus et les applications industrielles à haute performance.

- En mai 2025, Arlanxeo et TSRC Corporation ont annoncé conjointement l'inauguration de leur nouvelle usine de NBR (nitrile butadiène caoutchouté) à Nantong, en Chine, représentant une expansion stratégique de la capacité de production de NBR pour répondre à la demande croissante d'élastomères résistants au pétrole sur les marchés de l'automobile, de l'industrie et de la consommation.

- En janvier 2026, Eni a signé un accord avec SOCAR (Statut Oil Company of Azerbaijan Republic) pour l'acquisition d'une participation de 10 % dans le développement des champs pétrolifères et gaziers de Baleine au large de la Côte d'Ivoire, augmentant l'empreinte en Afrique de l'Ouest et renforçant la collaboration en matière de production.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIFS DE L'ÉTUDE

1.2 DÉFINITION DU MARCHÉ

1.3 APERÇU DU MARCHÉ POLYMÉR DE L'INDE

1.4 MONNAIE ET PRÊT

1.5 LIMITATIONS

1.6 MARCHÉS COUVERTS

2 SEGMENTATION DU MARCHÉ

2.1 MARCHÉS COUVERTS

2.2 CHAMP D'APPLICATION GÉOGRAPHIQUE

2.3 ANS CONSIDÉRÉS POUR L'ÉTUDE

2.4 MODÈLE DE VALIDATION DES DONNÉES DU TRIPOD DBMR

2.5 INTERVIEWS PRIMAIRES AVEC LES PRINCIPAUX LEADERS D'AVIS

2.6 GRID DE POSITION DU MARCHÉ DBMR

2.7 ANALYSE DU PARTAGE DES VENDEURS

2.8 MODÈLE MULTIVARIAT

2.9 COURS D'ORIENTATION

2.1 COUVERTURE DE LA DEMANDE DE MARCHÉ

2.11 SOURCES SECONDAIRES

2.12 OBSERVATIONS

3 RÉSUMÉ

4 PRIMAIRES

4.1 CINQ FORCES PORTÉES

4.2 CRITÈRES DE SÉLECTION DU VENDEUR

4.2.1 CERTIFICATION ET CONFORMITÉ RÉGLEMENTAIRE

4.2.2 QUALITÉ ET CONSISTANCE DES PRODUITS

4.2.3 PRATIQUES DURABLES

4.2.4 RESPONSABILITÉ EN MATIÈRE DE DOUANISATION

4.2.5 RESPONSABILITÉ LOGISTIQUE ET ASSURANCE DE L'APPROVISIONNEMENT

4.2.6 FLEXIBILITÉ DE COLLABORATION, D'INNOVATION ET DE PROGRAMME

4.3 CHANGEMENT CLIMATIQUE SCÉNARIO

4.3.1 QUESTIONS ENVIRONNEMENTALES

4.3.2 RÉPONSES DE L'INDUSTRIE

4.3.3 RÔLE DU GOUVERNEMENT

4.3.4 RECOMMANDATIONS D'ANALYSE

4.4 ANALYSE DES COÛTS

4.4.1 COÛTS SUR LES MATÉRIAUX

4.4.1.1 COMPOSITION DES MATÉRIAUX ET IMPLICATIONS DE COÛT

4.4.1.2 VOLATILITÉ DES PRIX DES MATÉRIAUX RÉVISÉS

4.4.2 FRAIS DIRECTS DE TRAVAIL ET DE FABRICATION

4.4.2.1 EXAMEN DES COÛTS DE TRAVAIL

4.4.2.2 TECHNIQUES DE PRODUCTION ET EFFICACITÉ DES COÛTS

4.4.3 COÛTS D'EXPLOITATION ET FRAIS INDIRECTS

4.4.3.1 SURFAIT DE FABRICATION

4.4.3.2 COÛTS DE CONTRÔLE DE LA QUALITÉ ET DE CONFORMITÉ

4.4.4 FRAIS DE CHAINE ET DE LOGISTIQUE

4.4.4.1 LOGISTIQUE ET SOURCE DE L'INNOVATION

4.4.4.2 ÉTABLISSEMENT ET DISTRIBUTION

4.4.5 COÛTS DE DIFFÉRENCE DE LA DOUANE ET DU PRODUIT

4.4.6 COÛTS RÉGLEMENTAIRES ET DURABLES

4.4.7 PRATIQUES STRATÉGIQUES DE GESTION DES COÛTS

4.4.8 CONCLUSION

4.5 ANALYSE DE L'ÉCOSYSTÈME INDUSTRIEL

4.5.1 ENTREPRISES PROMINENTES

4.5.2 Petites et moyennes entreprises

4.5.3 UTILISATEURS DE FIN

4.6 COUVERTURE DU MATÉRIEL RAW

4.6.1 STYRENE

4.6.2 BUTADIÈNE

4.6.3 INITIATEURS ET CATALYSTES DE POLYMÉRISATION

4.6.4 SOLVENTIONS ET MÉDIAS DE RÉACTION

4.6.5 AGENTS DE COUPLAGE ET DE FONCTIONNEMENT

4.6.6 DÉACTEURS ET AGENTS DE TERMINATION

4.6.7 STABILISATEURS ET ADDITIFS DU RENDEMENT

4.7 ANALYSE DE LA CHAINE D'APPROVISIONNEMENT

4.7.1 Aperçu général

4.7.2 SCÉNARIO DES COUTS LOGISTIQUES

4.7.3 IMPORTANCE DES SERVICES LOGISTIQUES

4.8 AVANTAGES TECHNOLOGIQUES

4.8.1 AVANCEMENTS EN MATIÈRE DE TECHNIQUES DE POLITIQUE

4.8.2 INNOVATIONS EN MATIÈRE DE DOUANISATION

4.8.3 AUTOMATION DES PROCESSUS ET INTÉGRATION NUMÉRIQUE

4.8.4 MISES À JOUR TECHNOLOGIQUES DURABLES

4.8.5 APPLICATION DES ESSAIS AVANCÉS ET DE L'ASSURANCE DE QUALITÉ

4.9 ANALYSE DE LA CHAINE DE VALEUR

4.9.1 UPSTREAM RAW MATERIAUX SOURCING ET FOURNITURES

4.9.2 POLYMÉRISATION DES SBS ET FABRICATION PRIMAIRE

4.9.3 COMPOSITION ET FORMULATION

4.9.4 DISTRIBUTION, LOGISTIQUE ET GESTION DU CHANEAU

4.9.5 INTÉGRATION DE L'INDUSTRIE DE LA FIN ET UTILISATION DE LA DEMANDE

4.9.6 RECYCLAGE, FIN DE VIE ET INTÉGRATION CIRCULAIRE

5 COUVERTURE DU RÈGLEMENT

5.1 CODES DES PRODUITS

5.2 NORMES CERTIFIÉES

5.3 NORMES DE SÉCURITÉ

5.4 MATÉRIEL ET STOCKAGE

5.5 TRANSPORT ET PRÉCAUTIONS

5.6 IDENTIFICATION DU DANGER

6 APERÇU DU MARCHÉ

6.1 RÉSEAU

6.1.1 GRANDE CROISSANCE DANS LES INDUSTRIES CLÉS

6.1.2 APPLICATIONS INDUSTRIELLES DE DIVERSES POLYMÈRES

6.1.3 REVENUS DU GOUVERNEMENT RENFORCEMENT DES FRAIS DOMESTIQUES

6.2 RÉSULTATS

6.2.1 VOLATILITÉ DES PRIX DES MATÉRIAUX RÉVISÉS

6.2.2 PRESSIONS RÉGLEMENTAIRES ET CONFORMITÉ ENVIRONNEMENTALE

6.3 POSSIBILITÉ

6.3.1 DEMANDE DE RISQUE DE VÉHICULES ÉLECTRIQUES (EV)

6.3.2 INNOVATION TECHNOLOGIQUE DANS LE COMPOSANT DES SBS

6.3.3 GRADES DE SBS BIOBASÉS ET RECYCLABLES

6.4 DÉFIS

6.4.1 TECHNOLOGIE ET GAZ DE COMPÉTENCE DANS L'INDUSTRIE CHIMIQUE INDIENNE

6.4.2 IMPACT DES IMPORTATIONS INFÉRIEURES SUR LES SBS DOMESTIQUES

7 PAR PRODUITS

7.1 Aperçu général

7.2 SBS LINEAIRES

7.3 SBS RADIAL / SBS STAR (R-SBS)

7.4 MARCHÉ DES POLYMÈRES DE L'INDE, PAR PRODUIT, 2018-2033 (TONS)

7.4.1 SBS LINEAR

7.4.2 SBS RADIAL / SBS STAR (R-SBS)

7.5 SBS LINEAR DE L'INDE SUR LE MARCHÉ DES POLYMÈRES SBS, PAR FORMULAIRE , 2018-2033

7.5.1 SOLIDE

7.5.2 GRANUL

7.5.3 LIQUIDE

7.6 SBS LINEAR DE L'INDE SUR LE MARCHÉ DES POLYMÈRES SBS, PAR UTILISATEUR DE FIN , 2018-2033 (MILLIERS USD)

7.6.1 CONSTRUCTION ET INFRASTRUCTURE ROUTIÈRES

7.6.2 INDUSTRIE INTÉRIEURE

7.6.3 ADHÉSIFS ET SECTEURS

7.6.4 INDUSTRIE AUTOMOBILE

7.6.5 INDUSTRIE DE LA CONSTRUCTION

7.6.6 INDUSTRIE DE L' EMBALLAGE

7.6.7 AUTRES

7.7 SBS RADIALES DE L'INDE / SBS STAR (R-SBS) SUR LE MARCHÉ DES POLYMÈRES DE L'INDE, PAR FORMULAIRE , 2018-2033 (MILLIERS DE USD)

7.7.1 SOLIDE

7.7.2 GRANUL

7.7.3 LIQUIDE

7.8 SBS RADIALES DE L'INDE / SBS STAR (R-SBS) SUR LE MARCHÉ DES POLYMÈRES DE SBS, PAR UTILISATEUR FINAL , 2018-2033 (MILLIERS DE USD)

7.8.1 CONSTRUCTION ET INFRASTRUCTURE ROUTIÈRES

7.8.2 INDUSTRIE DES ADHÉSIFS ET DES SALAIRES

7.8.3 INDUSTRIE INTÉRIEURE

7.8.4 INDUSTRIE AUTOMOBILE

7.8.5 INDUSTRIE DE LA CONSTRUCTION

7.8.6 INDUSTRIE DE L' EMBALLAGE

7.8.7 AUTRES

8 MARCHÉ DES POLYMÈRES DE L'INDE, PAR TYPE

8.1 Aperçu général

8.2 SBS NON EXTENDUES

8.3 SBS EXTENDUES DE L'HUILE

8.4 MARCHÉ DES POLYMÈRES DE L'INDE, PAR TYPE, 2018-2033 (TONS)

8.4.1 SBS NON ÉLÉMENTAIRES

8.4.2 SBS EXTENDUES PAR L'HUILE

9 LE MARCHÉ DES POLYMÈRES DE L'INDE, PAR CONTENU DE STYRENE

9.1 Aperçu général

9.2 SBS DE STYRENE MOYENNE

9.3 SBS DE STYRENE INFÉRIEUR

9.4 SBS DE HAUT STYRENE

9.5 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CONTENU DE STYRENE, 2018-2033 (TONS)

9.5.1 SBS DE STYRENE MOYEN

9.5.2 SBS DE STYRENE INFÉRIEUR

9.5.3 SBS HAUT STYRENE

10 MARCHÉ DES POLYMÈRES DE L'INDE, PAR DEMANDE

10.1 Aperçu général

10.2 MASTIQUES ROUTIÈRES

10.3 ADHÉSIFS ET SEALANTS

10.4 SOLES ET COMPOSANTES FOOTWEAR

10.5 BITUMINE MODIFIÉE PAR POLYMER

10.6 PRODUITS CHIMIQUES DE CONSTRUCTION

10.7 MODIFICATION D ' ASPHALT

10.8 MEMRANE ROUTIÈRE

10.9 AUTRES

10.1 MARCHÉ DES POLYMÈRES DE L'INDE, PAR DEMANDE, 2018-2033 (TONS)

10.10.1 MASTIQUES ROUTIÈRES

10.10.2 ADHÉSIVES ET SEALANTS

10.10.3 SOLES ET COMPOSANTES DE CHAUSSURES

10.10.4 BITUMEN MODIFIÉ PAR POLYMER

10.10.5 PRODUITS CHIMIQUES DE CONSTRUCTION

10.10.6 MODIFICATION D'ASPHALT

10.10.7 MEMRANE ROUTIÈRE

10.10.8 AUTRES

11 LE MARCHÉ DES POLYMERS DE L'INDE, PAR UTILISATEUR DE FIN

11.1 Aperçu général

11.2 CONSTRUCTION ROUTIÈRE ET INFRASTRUCTURE

11.3 INDUSTRIE INTÉRIEURE

11.4 ADHÉSIF ET SECTEURS

11.5 INDUSTRIE AUTOMOBILE

11.6 INDUSTRIE DE LA CONSTRUCTION

11.7 INDUSTRIE DE L' EMBALLAGE

11.8 AUTRES

11.9 MARCHÉ DES POLYMERS DE L'INDE, PAR UTILISATEUR FINAL , 2018-2033 (TONS)

11.9.1 INDUSTRIE INTÉRIEURE

11.9.2 CONSTRUCTION ET INFRASTRUCTURE ROUTIÈRES

11.9.3 ADHÉSIFS ET SALAIRES

11.9.4 INDUSTRIE AUTOMOBILE

11.9.5 INDUSTRIE DE LA CONSTRUCTION

11.9.6 INDUSTRIE DE L' EMBALLAGE

11.9.7 AUTRES

12 LE MARCHÉ DES POLYMÈRES DE L'INDE, PAR CHANEAU DE DISTRIBUTION

12.1 Aperçu général

12.2 DIRECT

12.3 INDIRECT

12.4 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CHANEAU DE DISTRIBUTION , 2018-2033 (TONS)

12.4.1 DIRECT

12.4.2 INDIRECT

12.5 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CHANEAU DE DISTRIBUTION , 2018-2033 (en MILLE USD)

12.5.1 DISTRIBUTEURS

12.5.2 AGENTS ET DÉLAIS

12.5.3 AUTRES

13 INDE SBS POLYMER MARKET: SOCIÉTÉ PAYSAGE

13.1 ANALYSE DE PARTAGE DES COMPAGNIES FABRICANTES: INDE

14 ANALYSE SWOT

15 FABRICANT PROFIL

15.1 SOCIÉTÉ PÉTROCHE DE LA CHINE (SINOPEC)

15.1.1 COMPAGNIE

15.1.2 ANALYSE DES RECETTES

15.1.3 PORTEFEUILLE DE PRODUITS

15.1.4 DÉVELOPPEMENT RÉCENT

15.2 LG CHEM LTD.

15.2.1 COMPAGNIE SNAPSHOT

15.2.2 ANALYSE DES RECETTES

15.2.3 PORTEFEUILLE DE PRODUITS

15.2.4 DÉVELOPPEMENT RÉCENT

15.3 PRODUITS CHIMIQUES DL

15.3.1 COMPAGNIE SNAPSHOT

15.3.2 PORTEFEUILLE DE PRODUITS

15.3.3 DÉVELOPPEMENT RÉCENT

15.4 SOCIÉTÉ DU CRTS

15.4.1 COMPAGNIE SNAPSHOT

15.4.2 ANALYSE DES RECETTES

15.4.3 PORTEFEUILLE DE PRODUITS

15.4.4 DÉVELOPPEMENT RÉCENT

15.5 ENI S.P.A. (SOCIÉTÉ PARTENAIRE DE VERSALIS S.P.A.)

15.5.1 COMPAGNIE SNAPSHOT

15.5.2 ANALYSE DES RECETTES

15.5.3 PORTEFEUILLE DE PRODUITS

15.5.4 DÉVELOPPEMENT RÉCENT

15.6 AMAZ CHEMICALS LLP

15.6.1 COMPAGNIE SNAPSHOT

15.6.2 PORTEFEUILLE DE PRODUITS

15.6.3 DÉVELOPPEMENT RÉCENT

15.7 PRODUITS CHIMIQUES DYCON

15.7.1 COMPAGNIE SNAPSHOT

15.7.2 PORTEFEUILLE DE PRODUITS

15.7.3 DÉVELOPPEMENT RÉCENT

15.8 POLITIQUES DE L'ENTITÉ

15.8.1 COMPAGNIE SNAPSHOT

15.8.2 PORTEFEUILLE DE PRODUITS

15.8.3 DÉVELOPPEMENT RÉCENT

15.9 KK KOMPOUNDING TECH GIANT LIMITED

15.9.1 COMPAGNIE SNAPSHOT

15.9.2 PORTEFEUILLE DE PRODUITS

15.9.3 DÉVELOPPEMENT RÉCENT

15.1 KUMHO PETROCHEMICAL CO LTD

15.10.1 COMPAGNIE SNAPSHOT

15.10.2 ANALYSE DES RECETTES

15.10.3 PORTEFEUILLE DE PRODUITS

15.10.4 DÉVELOPPEMENT RÉCENT

15.11 LCY

15.11.1 COMPAGNIE SNAPSHOT

15.11.2 PORTEFEUILLE DE PRODUITS

15.11.3 DÉVELOPPEMENT RÉCENT

15.12 MAXWELL.

15.12.1 COMPAGNIE SNAPSHOT

15.12.2 PORTEFEUILLE DE PRODUITS

15.12.3 DÉVELOPPEMENT RÉCENT

15.13 MORAS CHIMIQUES INDIA PVT LTD

15.13.1 COMPAGNIE SNAPSHOT

15.13.2 PORTEFEUILLE DE PRODUITS

15.13.3 DÉVELOPPEMENT RÉCENT

15.14 INDUSTRIES DE RELIANCE LIMITÉES.

15.14.1 COMPAGNIE SNAPSHOT

15.14.2 ANALYSE DES RECETTES

15.14.3 PORTEFEUILLE DE PRODUITS

15.14.4 DÉVELOPPEMENT RÉCENT

15.15 SBS POLYCHEM PVT. Tél.

15.15.1 COMPAGNIE SNAPSHOT

15.15.2 PORTEFEUILLE DE PRODUITS

15.15.3 DÉVELOPPEMENT RÉCENT

16 ACHETEUR DE PROFIL DE L'ENTREPRISE

16.1 ASIAN PAINTS LTD.

16.1.1 COMPAGNIE

16.1.2 ANALYSE DES RECETTES

16.1.3 PORTEFEUILLE DE PRODUITS

16.1.4 DÉVELOPPEMENT RÉCENT

16.2 BOSTIK

16.2.1 COMPAGNIE SNAPSHOT

16.2.2 PORTEFEUILLE DE PRODUITS

16.2.3 DÉVELOPPEMENT RÉCENT

16.3 PIDILITE INDUSTRIES LTD.

16.3.1 COMPAGNIE SNAPSHOT

16.3.2 ANALYSE DES RECETTES

16.3.3 PORTEFEUILLE DE PRODUITS

16.3.4 DÉVELOPPEMENT RÉCENT

16.4 LIMITÉES DE LIMITÉES DE LALAXO

16.4.1 COMPAGNIE SNAPSHOT

16.4.2 ANALYSE DES RECETTES

16.4.3 PORTEFEUILLE DE PRODUITS

16.4.4 DÉVELOPPEMENT RÉCENT

16.5 PRODUITS TAR SVIHAM

16.5.1 COMPAGNIE SNAPSHOT

16.5.2 PORTEFEUILLE DE PRODUITS

16.5.3 DÉVELOPPEMENT RÉCENT

17 QUESTIONNAIRE

18 RAPPORTS CONNEXES

Liste des tableaux

TABLEAU 1 MARCHÉ DES POLYMÈRES DE L'INDE, PAR PRODUITS, 2018-2033 (MILLIERS USD)

TABLEAU 2 MARCHÉ DES POLYMÈRES DE L'INDE, PAR PRODUITS, 2018-2033 (TONS)

TABLEAU 3 SBS LINEAR INDIA SUR LE MARCHÉ DES POLYMÈRES DE SBS, PAR FORMULAIRE , 2018-2033 (MILLIERS USD)

TABLEAU 4 SBS LINEAR INDIA SUR LE MARCHÉ DES POLYMÈRES SBS, PAR UTILISATEUR FINAL , 2018-2033

TABLEAU 5 SBS RADIALES DE L'INDE / SBS STAR (R-SBS) SUR LE MARCHÉ DES POLYMÈRES DE L'INDE, PAR FORMULAIRE , 2018-2033 (MILLIERS USD)

TABLEAU 6 SBS RADIALES DE L'INDE / SBS STAR (R-SBS) SUR LE MARCHÉ DES POLYMÈRES DE SBS, PAR UTILISATEUR DE FIN , 2018-2033 (MILLIERS USD)

TABLEAU 7 MARCHÉ DES POLYMÈRES DE L'INDE, PAR TYPE, 2018-2033

TABLEAU 8 MARCHÉ DES POLYMÈRES DE L'INDE, PAR TYPE, 2018-2033 (TONS)

TABLEAU 9 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CONTENU DE STYRENE, 2018-2033 (en MILLIERS)

TABLEAU 10 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CONTENU DE STYRENE, 2018-2033 (TONS)

TABLEAU 11 MARCHÉ DES POLYMÈRES DE L'INDE, PAR DEMANDE, 2018-2033 (MILLIERS USD)

TABLEAU 12 MARCHÉ DES POLYMÈRES DE L'INDE, PAR DEMANDE, 2018-2033 (TONS)

TABLEAU 13 MARCHÉ DES POLYMÈRES DE L'INDE, PAR UTILISATEUR DE FIN , 2018-2033 (en MILLIERS)

TABLEAU 14 PAR UTILISATEUR , 2018-2033 (TONS)

TABLEAU 15 MARCHÉ DES POLYMÈRES DE L'INDE , PAR CHANEAU DE DISTRIBUTION , 2018-2033 (MILLIERS USD)

TABLEAU 16 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CHANEAU DE DISTRIBUTION , 2018-2033 (TONS)

TABLEAU 17 MARCHÉ DES POLYMÈRES DE L'INDE , PAR CHANEAU DE DISTRIBUTION , 2018-2033 (MILLIERS USD)

Liste des figures

FIGURE 1 SUR LE MARCHÉ POLITIQUE DE L'INDE: SEGMENTATION

FIGURE 2 SUR LE MARCHÉ POLITIQUE DE L'INDE: TRIANGULATION DES DONNÉES

FIGURE 3 SUR LE MARCHÉ POLYMER DE L'INDE: ANALYSE DES DROGUES

FIGURE 4 SBS INDE MARCHÉ POLYMER: ANALYSE MONDIALE DES MARCHÉS RÉGIONAUX

FIGURE 5 MARCHÉ DU POLYMER DE L'INDE: ANALYSE DE RECHERCHE DES ENTREPRISES

GRAPHIQUE 6 SUR LE MARCHÉ POLYMER DE L'INDE: DÉMOGRAPHIQUES INTERVIEW

GRID DE POSITION DU MARCHÉ DE L'INDE

FIGURE 8 SUR LE MARCHÉ POLYMER DE L'INDE: ANALYSE DU PARTAGE DES VENDEURS

GRAPHIQUE 9 MARCHÉ DU POLYMER DE L'INDE: MODÈLE MULTIVARIVÉ

FIGURE 10 SUR LE MARCHÉ POLYMER DE L'INDE: COURS DE CALENDRIER DES PRODUITS

GRID DE COUVERTURE DES DEMANDES

FIGURE 12 SUR LE MARCHÉ POLITIQUE DE L'INDE: SEGMENTATION

FIGURE 13 DEUX SEGMENTS COMPRIS PAR PRODUITS LE MARCHÉ DU POLYMER DE L'INDE (2025)

GRAPHIQUE 14 MARCHÉ DU POLYMER DE L'INDE: RÉSUMÉ

FIGURE 15 DÉCISIONS STRATÉGIQUES

LA GRANDE CROISSANCE DE LA FIGURE 16 DANS LES INDUSTRIES CLÉS EST PRÉVUE À LA CONDUITE DU MARCHÉ POLYMER DE L'INDIA POUR LA PÉRIODE PRÉCÉDENTE DE 2026 À 2033.

FIGURE 17 LE SEGMENT DE PRODUITS EST EXPLOITÉ À COMPTER DE LA PLUS GRANDE PART DU MARCHÉ POLYMER DE L'INDE EN 2026 ET 2033

FIGURE 18 CRITÈRES DE SÉLECTION DES VENDEURS

FIGURE 19 ANALYSE DES DROGUES

GRAPHIQUE 20 PAR PRODUITS, 2025

GRAPHIQUE 21 MARCHÉ DES POLYMÈRES DE L'INDE, PAR TYPE, 2025

FIGURE 22 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CONTENU DE STYRENE, 2025

FIGURE 23 MARCHÉ DES POLYMÈRES DE L'INDE, PAR DEMANDE, 2025

FIGURE 24 MARCHÉ DES POLYMÈRES DE L'INDE, PAR UTILISATEUR DE FIN, 2025

FIGURE 25 MARCHÉ DES POLYMÈRES DE L'INDE, PAR CHANEAU DE DISTRIBUTION, 2025

FIGURE 26 SUR LE MARCHÉ POLYMER DE L'INDE: PARTAGE DE L'ENTREPRISE 2025 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.