North America Infusion Pump Market

Taille du marché en milliards USD

TCAC :

%

USD

19.32 Billion

USD

41.41 Billion

2025

2033

USD

19.32 Billion

USD

41.41 Billion

2025

2033

| 2026 –2033 | |

| USD 19.32 Billion | |

| USD 41.41 Billion | |

| % | |

|

North America Infusion Pumps Market Segmentation, By Type (Ambulatory Pumps, Volumetric Pumps, and Syringe Pumps and Accessories), Application (Diabetes, Chemotherapy, Gastrointestinal Diseases and Pediatrics), End User (Hospitals & Clinics, Ambulatory Surgical Centers and Homecare) - Industry Trends and Forecast to 2033

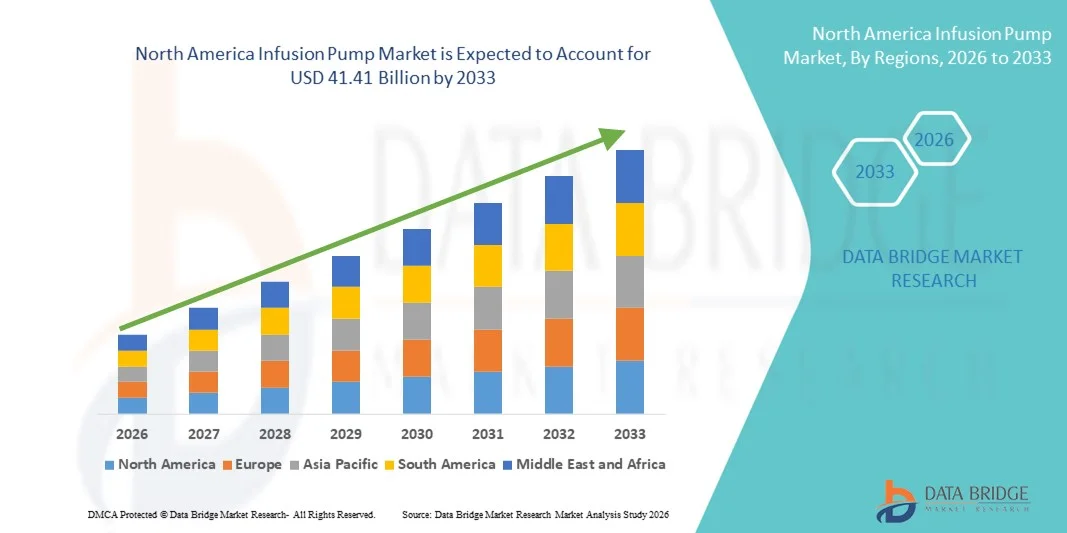

North America Infusion Pump Market Size

- The North America infusion pump market size was valued at USD 19.32 billion in 2025 and is expected to reach USD 41.41 billion by 2033, at a CAGR of 10.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, rising demand for accurate and controlled drug delivery systems, and continuous technological advancements in programmable and smart infusion pumps, leading to improved patient safety and treatment outcomes across hospitals and home healthcare settings

- Furthermore, growing adoption of ambulatory and wearable infusion pumps, expanding home-based care services, and integration of advanced safety features such as dose error reduction systems are establishing infusion pumps as essential components of modern healthcare delivery. These converging factors are accelerating the uptake of Infusion Pump solutions, thereby significantly boosting the industry's growth

North America Infusion Pump Market Analysis

- Infusion pumps, offering precise and controlled delivery of fluids, medications, and nutrients, are increasingly vital components of modern healthcare systems across hospitals, ambulatory care centers, and home healthcare settings due to their enhanced dosing accuracy, safety features, and ability to support complex treatment regimens

- The escalating demand for infusion pumps is primarily fueled by the rising prevalence of chronic diseases such as diabetes and cancer, growing geriatric population, increasing need for long-term intravenous therapies, and expanding adoption of ambulatory and wearable infusion systems

- The U.S. dominated the infusion pump market with the largest revenue share of 36.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of smart infusion systems with dose error reduction software, strong reimbursement framework, and the presence of leading medical device manufacturers driving continuous technological innovation

- Canada is expected to be the fastest-growing country in the infusion pump market during the forecast period, expanding at a CAGR of 8.4% from 2026 to 2033, driven by rising investments in hospital modernization, increasing demand for home-based infusion therapy, growing prevalence of chronic conditions, and supportive government healthcare initiatives

- The volumetric pumps segment dominated the largest market revenue share of 41.8% in 2025, driven by their widespread use in hospitals for continuous and precise fluid administration

Report Scope and Infusion Pump Market Segmentation

|

Attributes |

Infusion Pump Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

North America Infusion Pump Market Trends

Advancements in Smart and Connected Infusion Technologies

- A significant and accelerating trend in the infusion pump market is the growing adoption of smart infusion systems equipped with advanced software, dose error reduction systems (DERS), and wireless connectivity. These technologically enhanced devices are improving medication safety, reducing human errors, and enabling real-time monitoring of infusion therapy across hospital and homecare settings

- For instance, modern smart infusion pumps integrated with drug libraries and automated safety alerts help clinicians prevent incorrect dosage administration and adverse drug events. Many hospitals are increasingly implementing interoperable infusion systems that can seamlessly communicate with electronic health records (EHRs), ensuring accurate documentation and enhanced clinical workflow efficiency

- The rising demand for ambulatory and wearable infusion pumps is also reshaping treatment delivery, particularly for chronic conditions such as diabetes, cancer, and pain management. Portable insulin pumps and elastomeric pumps allow patients to receive continuous medication therapy outside hospital settings, improving convenience and quality of life

- Furthermore, advancements in syringe and volumetric infusion pumps are enhancing precision in critical care units, neonatal care, and oncology departments. Enhanced battery life, user-friendly interfaces, and compact designs are contributing to broader adoption across healthcare facilities

- The increasing emphasis on patient safety, medication accuracy, and integration of infusion systems within digital healthcare infrastructure is driving continuous innovation. As healthcare providers focus on minimizing infusion-related complications, smart and connected infusion technologies are becoming standard practice in modern clinical environments

- Overall, the transition toward safer, automated, and interoperable infusion pump systems is significantly transforming medication delivery processes and strengthening clinical outcomes

North America Infusion Pump Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Increasing Surgical Procedures

- The growing global burden of chronic diseases such as diabetes, cancer, cardiovascular disorders, and gastrointestinal conditions is a primary driver fueling demand in the Infusion Pump market. These conditions often require long-term and precise drug administration, increasing reliance on advanced infusion technologies

- For instance, the rising number of diabetic patients worldwide has significantly increased demand for insulin infusion pumps that provide continuous and controlled insulin delivery. Similarly, oncology treatments frequently require programmable infusion pumps for chemotherapy administration, ensuring accurate dosage and minimized complications

- The increasing volume of surgical procedures and hospital admissions is also contributing to market expansion. Infusion pumps play a critical role in perioperative care, delivering anesthetics, analgesics, antibiotics, and fluids during and after surgical interventions

- In addition, the expanding geriatric population is more susceptible to chronic illnesses requiring continuous intravenous therapies, thereby increasing hospital-based infusion pump utilization. Aging demographics are creating sustained demand for safe and efficient drug delivery systems

- The growth of home healthcare services and ambulatory care centers is further supporting adoption. Patients increasingly prefer receiving long-term treatments in home settings, boosting demand for portable and user-friendly infusion devices

- Collectively, the rising incidence of chronic diseases, increasing surgical volumes, and expanding homecare services are strongly propelling the Infusion Pump market forward

Restraint/Challenge

High Device Costs and Risk of Medication Errors

- The high cost associated with advanced infusion pump systems remains a significant challenge, particularly for healthcare facilities in low- and middle-income regions. Procurement, maintenance, and software upgrades require considerable financial investment, which may limit accessibility in resource-constrained settings

- For instance, smart infusion pumps equipped with dose error reduction systems and integrated software platforms involve substantial upfront costs, making large-scale adoption challenging for smaller hospitals and clinics

- Despite technological safeguards, infusion-related medication errors and device malfunctions continue to pose concerns. Programming complexities, user errors, and technical glitches can potentially lead to incorrect drug delivery, impacting patient safety

- Regulatory scrutiny and product recalls related to infusion pump malfunctions have also created compliance challenges for manufacturers, increasing operational costs and delaying product launches

- Furthermore, the need for continuous staff training and competency development to operate advanced infusion systems adds to healthcare providers’ operational burden. Without proper training, the risk of improper usage may increase

- Addressing these challenges through cost optimization strategies, enhanced device reliability, improved user interfaces, and comprehensive training programs will be essential to ensure sustained growth and safe adoption within the infusion pump market

North America Infusion Pump Market Scope

The market is segmented on the basis of type, application, and end user.

- By Type

On the basis of type, the Infusion Pumps market is segmented into ambulatory pumps, volumetric pumps, and syringe pumps and accessories. The volumetric pumps segment dominated the largest market revenue share of 41.8% in 2025, driven by their widespread use in hospitals for continuous and precise fluid administration. Volumetric pumps are extensively utilized for intravenous delivery of medications, nutrients, and fluids in critical care settings. Increasing number of hospital admissions globally supports sustained demand. Rising prevalence of chronic diseases requiring long-term infusion therapy accelerates adoption. Technological advancements improving accuracy and safety features enhance utilization. Integration of smart pump technology with dose error reduction systems strengthens segment growth. Growing geriatric population requiring hospitalization further boosts installations. Expansion of intensive care units in emerging economies supports procurement. Strong regulatory approvals and compliance with safety standards promote market penetration. High reliability and versatility across multiple therapeutic areas sustain preference. Increasing healthcare infrastructure investments further consolidate dominance. Continuous product upgrades with wireless connectivity enhance operational efficiency.

The ambulatory pumps segment is anticipated to witness the fastest CAGR of 9.6% from 2026 to 2033, fueled by rising demand for portable and home-based infusion therapies. Growing shift toward outpatient and homecare settings significantly supports growth. Increasing prevalence of diabetes and cancer requiring long-term therapy accelerates adoption. Compact and lightweight designs improve patient mobility and convenience. Technological advancements enabling remote monitoring enhance safety and compliance. Rising healthcare cost containment initiatives promote ambulatory care solutions. Expansion of home healthcare services globally strengthens demand. Increasing awareness about patient-centric treatment approaches drives uptake. Integration with digital health platforms improves therapy management. Favorable reimbursement policies in developed regions encourage adoption. Growing demand for wearable infusion devices further boosts growth. Continuous innovation in battery life and dosing accuracy sustains strong CAGR momentum.

- By Application

On the basis of application, the Infusion Pumps market is segmented into diabetes, chemotherapy, gastrointestinal diseases, and pediatrics. The diabetes segment held the largest market revenue share of 36.5% in 2025, driven by the rapidly increasing global prevalence of diabetes. Rising adoption of insulin infusion pumps supports significant revenue generation. Growing awareness regarding continuous glucose management enhances demand. Technological advancements in insulin pump integration with CGM systems improve outcomes. Increasing patient preference for automated insulin delivery systems accelerates growth. Expanding diabetic population in emerging economies strengthens market penetration. Government initiatives promoting diabetes management further stimulate adoption. Rising healthcare expenditure on chronic disease management supports segment dominance. Availability of portable and user-friendly insulin pumps enhances patient adherence. Growing geriatric population with type 2 diabetes contributes to sustained demand. Continuous product innovation improves dosing precision and safety. Strong presence of leading manufacturers further consolidates market leadership.

The chemotherapy segment is projected to grow at the fastest CAGR of 10.4% from 2026 to 2033, driven by increasing global cancer incidence. Rising adoption of infusion pumps for controlled drug delivery enhances treatment effectiveness. Technological advancements improving programmable dosing accuracy support growth. Growing number of oncology centers globally boosts equipment demand. Expansion of ambulatory chemotherapy services accelerates segment expansion. Increasing investment in cancer care infrastructure strengthens adoption. Rising preference for outpatient chemotherapy promotes portable pump usage. Integration of smart safety features reduces medication errors. Government funding for cancer treatment programs supports market penetration. Growing research in targeted oncology therapies further increases infusion pump usage. Improved patient survival rates lead to longer treatment durations, driving demand. Continuous innovation in compact and precise infusion systems sustains strong CAGR growth.

- By End User

On the basis of end user, the Infusion Pumps market is segmented into hospitals & clinics, ambulatory surgical centers, and homecare. The hospitals & clinics segment accounted for the largest market revenue share of 58.9% in 2025, supported by high inpatient volumes and advanced healthcare infrastructure. Hospitals require multiple infusion systems for critical and routine care procedures. Increasing ICU admissions significantly boost demand. Availability of skilled healthcare professionals enhances device utilization. Integration of smart infusion pumps with hospital information systems improves workflow. Rising surgical procedures globally further strengthen demand. Government and private investments in hospital modernization support growth. Strong regulatory standards encourage adoption of advanced pump systems. Growing prevalence of chronic and acute conditions sustains high usage rates. Expansion of multi-specialty hospitals in emerging economies drives procurement. Continuous upgrades to advanced safety-enabled pumps consolidate dominance.

The homecare segment is anticipated to register the fastest CAGR of 11.2% from 2026 to 2033, driven by increasing preference for home-based treatment solutions. Rising healthcare cost pressures encourage shift from inpatient to homecare settings. Growing elderly population requiring long-term infusion therapy supports demand. Technological advancements enabling portable and easy-to-use pumps accelerate adoption. Increasing patient awareness regarding self-administration enhances growth. Expansion of telehealth services supports remote monitoring of infusion therapy. Favorable reimbursement policies in developed markets further boost uptake. Rising prevalence of chronic diseases requiring continuous medication strengthens segment expansion. Improved patient comfort and reduced hospital visits enhance preference. Integration of wireless monitoring systems improves safety and compliance. Growing investment in home healthcare infrastructure supports procurement. Continuous innovation in lightweight and wearable pumps sustains strong segment CAGR throughout the forecast period.

North America Infusion Pump Market Regional Analysis

- North America dominated the infusion pump market with the largest revenue share in 2025, driven by its highly advanced healthcare infrastructure, strong clinical adoption of technologically sophisticated infusion systems, and growing prevalence of chronic diseases requiring continuous drug administration. The region benefits from widespread implementation of smart infusion pumps equipped with dose error reduction systems, integration with electronic health records, and stringent patient safety standards across hospitals and ambulatory care centers. Additionally, the increasing number of surgical procedures, rising geriatric population, and expanding home healthcare services have significantly contributed to the steady demand for infusion pumps across various care settings

- The region’s leadership is further supported by substantial healthcare expenditure, well-established reimbursement frameworks, and the presence of major medical device manufacturers investing heavily in research and product innovation. Hospitals across North America are increasingly focusing on minimizing medication errors and improving infusion safety, which is accelerating the transition from conventional pumps to advanced programmable systems. Moreover, the growing adoption of ambulatory and portable infusion pumps for chemotherapy, insulin therapy, and pain management continues to strengthen market growth

- The expansion of outpatient care facilities and rising preference for home-based treatment solutions are also reinforcing demand for user-friendly, compact infusion devices. Continuous technological advancements and strong regulatory oversight aimed at enhancing patient safety further solidify North America’s dominant position in the global infusion pump market

U.S. Infusion Pump Market Insight

The U.S. infusion pump market dominated the infusion pump market with the largest revenue share of 36.9% in 2025, characterized by advanced healthcare infrastructure, high adoption of smart infusion systems with dose error reduction software, strong reimbursement framework, and the presence of leading medical device manufacturers driving continuous technological innovation. Hospitals and specialty clinics across the country have widely implemented programmable infusion pumps integrated with electronic medical records to enhance medication accuracy and patient safety. The increasing burden of chronic diseases such as diabetes, cancer, and cardiovascular disorders continues to drive demand for insulin pumps, ambulatory infusion systems, and chemotherapy infusion devices. Furthermore, growing investments in hospital digitization and patient safety initiatives are accelerating the deployment of next-generation infusion technologies nationwide.

Canada Infusion Pump Market Insight

Canada infusion pump market is expected to be the fastest-growing country in the infusion pump market during the forecast period, expanding at a CAGR of 8.4% from 2026 to 2033. Growth in the country is driven by rising investments in hospital modernization, increasing demand for home-based infusion therapy, and the growing prevalence of chronic conditions requiring long-term medication administration. Supportive government healthcare initiatives and improvements in healthcare accessibility across provinces are encouraging the adoption of advanced infusion technologies. Additionally, the expanding focus on outpatient and community-based care models is anticipated to significantly contribute to sustained market expansion in Canada throughout the forecast period.

North America Infusion Pump Market Share

The Infusion Pump industry is primarily led by well-established companies, including:

- Baxter International Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- B. Braun S.E. (Germany)

- ICU Medical, Inc. (U.S.)

- Medtronic plc (Ireland)

- Fresenius Kabi AG (Germany)

- Terumo Corporation (Japan)

- Smiths Medical (U.S.)

- Moog Inc. (U.S.)

- Mindray Medical International Limited (China)

- Nipro Corporation (Japan)

- Ypsomed Holding AG (Switzerland)

- Roche Diabetes Care (Switzerland)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care, Inc. (U.S.)

- Micrel Medical Devices SA (Greece)

- Zyno Medical (U.S.)

- Arcomed AG (Switzerland)

- CME Medical (U.K.)

- Hospira (U.S.)

Latest Developments in North America Infusion Pump Market

- In February 2023, Mindray launched its BeneFusion i Series and u Series infusion systems, offering high-precision infusion pumps with adaptive customization designed to enhance medication safety across diverse clinical settings

- In August 2023, ICU Medical received U.S. FDA 510(k) clearance for its Plum Duo infusion pump with LifeShield Infusion Safety Software, aimed at improving the safety, accuracy, and efficiency of IV medication delivery in acute care environments; the device became available in early 2024

- In April 2024, Baxter International Inc. received U.S. FDA 510(k) clearance for its Novum IQ large volume infusion pump (LVP) with Dose IQ Safety Software — part of the Novum IQ Infusion Platform designed to integrate large-volume and syringe infusion modalities with advanced safety and connectivity features

- In February 2024, ICU Medical’s Plum 360™ smart infusion pump was named “Best in KLAS” for smart pumps, recognizing its excellence in electronic medical record (EMR) integration, safety features, and reliability in clinical use

- In April 2025, ICU Medical Inc. announced FDA 510(k) clearance for the Plum Solo™ precision IV pump — a single-channel infusion device designed to complement the Plum Duo and bolster the ICU Medical IV Performance Platform with enhanced accuracy, safety alerts, and wireless clinical connectivity

- In April 2025, ICU Medical also received clearance for updated versions of its Plum Duo infusion pump and LifeShield infusion safety software, reinforcing its portfolio of precision IV therapy systems that support connected care and real-time data integration

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.