Uae Specialty Fats Market

Taille du marché en milliards USD

TCAC :

%

USD

116.36 Million

USD

67.58 Million

2024

2032

USD

116.36 Million

USD

67.58 Million

2024

2032

| 2025 –2032 | |

| USD 116.36 Million | |

| USD 67.58 Million | |

| % | |

|

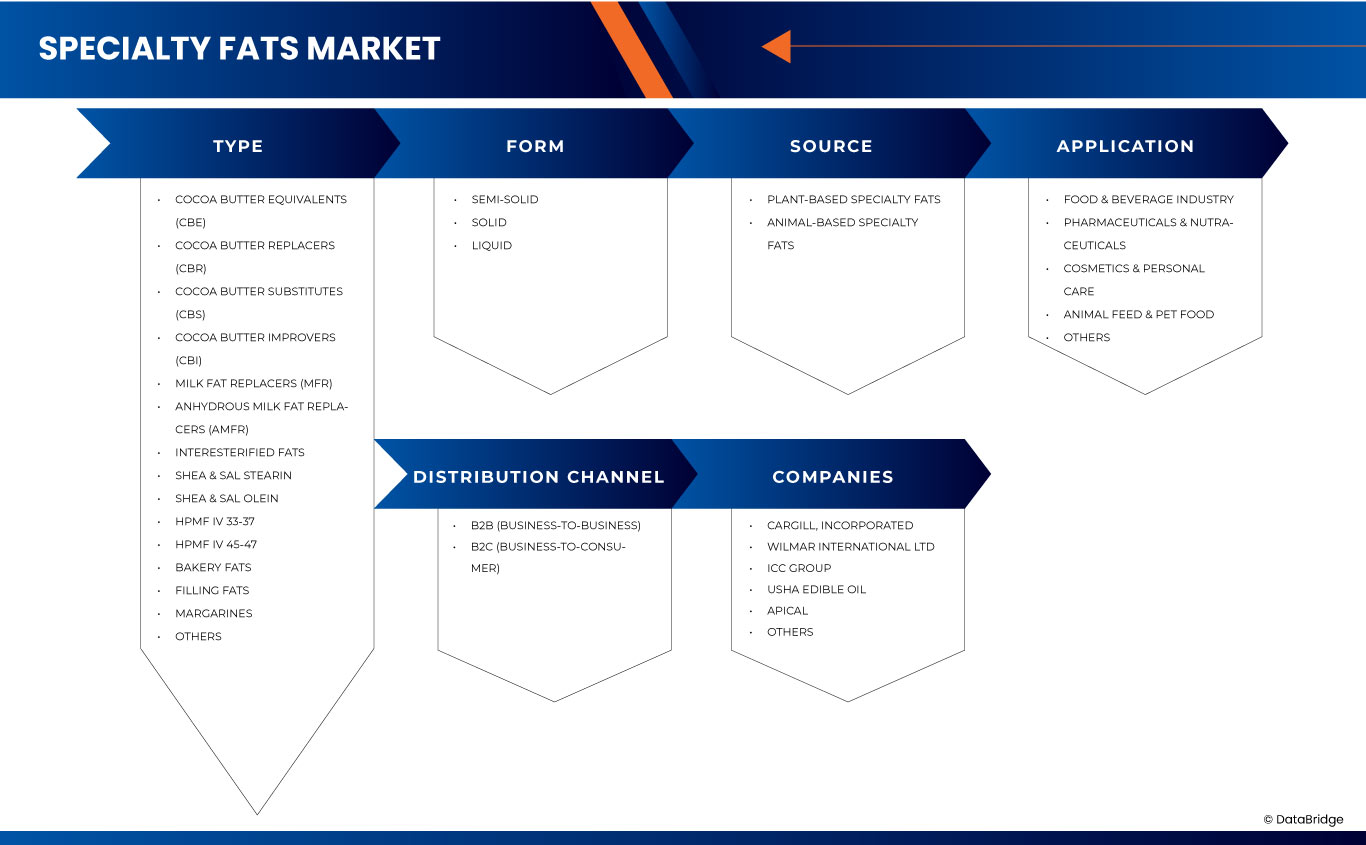

U.A.E Specialty Fats Market Segmentation, By Type (Cocoa Butter Equivalents (CBE), Cocoa Butter Replacers (CBR), Cocoa Butter Substitutes (CBS), Cocoa Butter Improvers (CBI), Milk Fat Replacers (MFR), Anhydrous Milk Fat Replacers (AMFR), Interesterified Fats, Shea & Sal Stearin, Shea & Sal Olein, HPMF IV 33-37, HPMF IV 45-47, Bakery Fats, Filling Fats, Margarines, and Others), Form (Semi-Solid, Solid, and Liquid), Source (Plant-Based Specialty Fats and Animal-Based Specialty Fats), Application (Food & Beverage Industry, Pharmaceuticals & Nutraceuticals, Cosmetics & Personal Care, Animal Feed & Pet Food, and Others), Distribution Channel (B2B (Business-To-Business) and B2C (Business-To-Consumer)) - Industry Trends and Forecast to 2032

Specialty Fats Market Size

- The U.A.E specialty fats market size was valued at USD 116.36 million in 2024 and is expected to reach USD 67.58 million by 2032, at a CAGR of 7.0% during the forecast period

- This growth is driven by factors such as the growing demand from bakery and confectionery industry and rising consumer awareness regarding health and nutrition

Specialty Fats Market Analysis

- The U.A.E specialty fats market is expanding steadily, driven by increasing demand in bakery, confectionery, and processed foods. The market benefits from the country's strong food service sector and rising consumer preference for premium, healthier products.

- Urbanization, tourism growth, and the popularity of Western-style diets are fueling the demand for specialty fats like cocoa butter alternatives, dairy fat replacers, and frying fats.

- The Cocoa Butter Equivalents (CBE) in type segment is expected to dominate the market due to its excellent compatibility with natural cocoa butter, cost-effectiveness, and ability to maintain the desired texture, gloss, and mouthfeel in chocolate and confectionery products.

- The semi-solid in form segment is expected to dominate the market due to its versatility, ease of handling, and widespread use in bakery, confectionery, and dairy applications. Semi-solid fats offer optimal plasticity and spreadability, making them ideal for use in margarine, spreads, and cream fillings.

Report Scope and Specialty Fats Market Segmentation

|

Attributes |

Specialty Fats Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

U.A.E. |

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Specialty Fats Market Trends

“Shift Towards Sustainably Sourced Fats”

- U.A.E. consumers are increasingly seeking healthier alternatives, driving demand for specialty fats rich in omega-3s, antioxidants, and low in trans fats. Oils like avocado, flaxseed, and coconut are gaining popularity due to their perceived health benefits

- In May 2019, as per TechTarget, Inc. leading food companies such as Nestlé, PepsiCo, and Mondelēz International have committed to eliminating industrially produced trans fats from their products by 2023, aligning with the World Health Organization’s (WHO) REPLACE initiative. This move is a direct response to increasing consumer awareness and demand for healthier food options

- There's a growing preference for products with simple, natural ingredients. Consumers favor specialty fats and oils that are non-GMO, organic, and free from artificial additives, reflecting a broader clean-label movement

- Environmental concerns are prompting a shift towards sustainably sourced fats. The demand for products certified by organizations like the Roundtable on Sustainable Palm Oil (RSPO) is on the rise, emphasizing eco-friendly production practices.

- The U.A.E.'s multicultural population and vibrant food scene are fueling demand for diverse specialty fats. High-quality oils such as truffle, walnut, and clarified butter are increasingly used in gourmet cooking, catering to sophisticated palates.

Specialty Fats Market Dynamics

Driver

“Growing Demand From Bakery and Confectionery Industry”

- As consumers increasingly seek out premium, indulgent, and innovative food options, manufacturers are responding by incorporating specialty fats into their formulations to enhance taste, texture, and visual appeal. These fats—such as cocoa butter alternatives, filling fats, and emulsified shortenings—play a crucial role in delivering the softness, creaminess, and shelf stability required in high-quality baked goods and confections

- The U.A.E.’s position as a regional hub for tourism, luxury dining, and food innovation is fueling a steady rise in demand for diverse bakery and dessert offerings. Local production is ramping up to meet both domestic consumption and the growing demand from hospitality and retail channels

- Specialty fats are increasingly being used to create differentiated products that align with regional flavor profiles and performance expectations in high-temperature environments. In addition, the shift towards clean-label, trans-fat-free, and plant-based alternatives is prompting manufacturers to seek customized fat solutions that meet both health and functionality standards

- Specialty fats offer the versatility to reformulate recipes without compromising on quality, making them indispensable in the creation of modern bakery and confectionery products.

For instance,

- In July 2024, William Reed Ltd published an article which states that Cargill has invested USD 50 million to expand its plant in Port Klang, Malaysia, aiming to supply finished specialty fats to consumers throughout Asia-Pacific and semi-finished products to its edible oils facilities in Europe, South America, and North America

- This expansion reflects the company's commitment to meeting the rising demand for specialty fats in regions like the Middle East, where heat resistance is crucial for chocolate products

- According to the New Zealand Institute of Oils and Fats, fats play a crucial role in baking by enhancing the texture, flavor, and shelf-life of baked products. In bread-making, for instance, fats coat the gluten structure, making the dough more extensible and yielding a softer crumb

- This functional importance is driving increased demand for fats, fueled by the rapid growth of the global bakery and confectionery industry

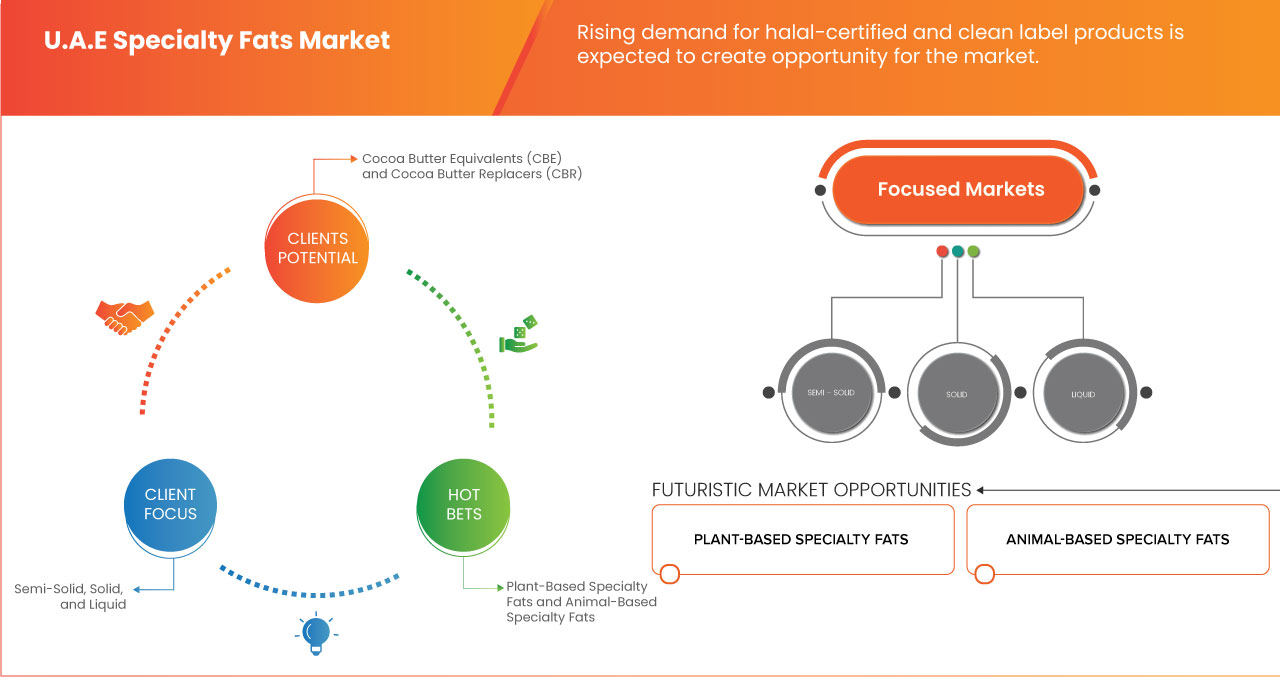

Opportunity

“Expansion in Plant-Based and Vegan Products”

- The specialty fats sector is seeing growing interest in plant-based and vegan products. This opportunity comes from changes in consumer preferences, with more people looking for healthier and more sustainable food options. Plant-based diets are gaining popularity among both locals and expatriates, especially among younger consumers who are more health-conscious and aware of global food trends.

- Food producers and manufacturers are introducing a wider range of plant-based alternatives, including those made with specialty fats that mimic the taste and texture of traditional animal-based products. These specialty fats are used in bakery items, confectionery, and dairy alternatives to improve quality and performance.

- For instance,

- In February 2025, a ResearchGate publication titled "Are Emirati consumers in United Arab Emirates open to alternative proteins" revealed that many Emirati consumers show positive attitudes toward alternative proteins and are willing to replace animal-based sources, driven by health, sustainability, and ethical concerns, highlighting growing openness to plant-based diets

- In September 2024, the Middle East Vegan Society reported a surge in plant-based food adoption across the Middle East, driven by health, sustainability, and ethical concerns. Local innovations and startups are meeting this demand, with increasing availability of vegan products in supermarkets, restaurants, and food delivery platforms throughout the region

Restraint/Challenge

“High Costs of Specialty Fats”

- Despite rising demand across food processing and confectionery segments, the high cost of specialty fats remains a significant barrier to widespread market penetration in the U.A.E. These fats—such as cocoa butter equivalents, structured lipids, and trans-fat alternatives—undergo complex processing and formulation techniques, resulting in elevated production costs compared to conventional fats and oils.

- Moreover, sourcing premium raw materials such as sustainable palm oil, shea butter, and exotic plant-based ingredients often involves import duties, fluctuating exchange rates, and supply chain constraints, further inflating prices for manufacturers and end-users alike.

- This cost burden particularly impacts small and medium-sized food producers and bakeries, who often operate with thinner margins and limited capacity to absorb high ingredient costs. As a result, these businesses may either avoid incorporating specialty fats into their products or opt for cheaper, lower-quality substitutes, ultimately slowing market adoption.

- Additionally, consumers in price-sensitive segments of the U.A.E. population may find products formulated with specialty fats less accessible, especially when faced with premium pricing on health-positioned items.

For instance,

- In September 2024, ICE cocoa futures prices reached USD 9,821 per tonne, more than doubling from USD 3,430 per tonne a year earlier. This significant increase in cocoa prices has led confectionery manufacturers to seek alternatives to cocoa butter, such as specialty fats, to manage costs. However, these alternatives also come with their own cost implications, affecting product pricing and profitability

Specialty Fats Market Scope

The U.A.E. specialty fats market is segmented into five notable segments based on type, form, source, application, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Form |

|

|

By Source |

|

|

By Application

|

|

|

By Distribution Channel

|

|

In 2025, the Cocoa Butter Equivalents (CBE) segment is projected to dominate the market with a largest share in type segment

The Cocoa Butter Equivalents (CBE) segment is expected to dominate the market with a market share of 26.16% due to its excellent compatibility with natural cocoa butter, cost-effectiveness, and ability to maintain the desired texture, gloss, and mouthfeel in chocolate and confectionery products.

In 2025, the semi-solid segment is expected to account for the largest share during the forecast period in form segment

The semi-solid segment is expected to dominate the market with a market share of 51.95% due to its versatility, ease of handling, and widespread use in bakery, confectionery, and dairy applications. Semi-solid fats offer optimal plasticity and spreadability, making them ideal for use in margarine, spreads, and cream fillings.

Specialty Fats Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, regional presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Cargill, Incorporated (U.S.)

- Wilmar International Ltd (Singapore)

- ICC Group (Indonesia)

- Usha Edible Oil (U.A.E)

- Apical (Singapore)

- Al Tawun Solyman Services (FZE) (U.A.E)

- Dulzer (U.A.E)

- Saha Edible Oil Trading (U.A.E)

- Shahraan Group (U.A.E)

- United Foods Company (U.A.E)

Latest Developments in U.A.E Specialty Fats Market

- In February 2025, ICC Group participated in Gulfood 2025 at the Dubai World Trade Centre, showcasing its premium palm oil products, including cooking oils, specialty fats, and bakery ingredients. The event provided an opportunity to strengthen global partnerships and highlight the company’s commitment to sustainability and innovation. ICC Group remains dedicated to expanding its global footprint and meeting evolving industry needs.

SKU-

Accédez en ligne au rapport sur le premier cloud mondial de veille économique

- Tableau de bord d'analyse de données interactif

- Tableau de bord d'analyse d'entreprise pour les opportunités à fort potentiel de croissance

- Accès d'analyste de recherche pour la personnalisation et les requêtes

- Analyse de la concurrence avec tableau de bord interactif

- Dernières actualités, mises à jour et analyse des tendances

- Exploitez la puissance de l'analyse comparative pour un suivi complet de la concurrence

Table des matières

1 INTRODUCTION

1.1 OBJECTIFS DE L'ÉTUDE

1.2 DÉFINITION DU MARCHÉ

1.3 APERÇU

1.4 LIMITATIONS

1,5 MARCHÉS COUVERTS

2 SEGMENTATION DU MARCHÉ

2.1 MARCHÉS COUVERTS

2,2 ANS CONSIDÉRÉS POUR L'ÉTUDE

2.3 MONNAIE ET TARIFS

2.4 MODÈLE DE VALIDATION DES DONNÉES DU TRÉPIED DBMR

2.5 MODÉLISATION MULTIVARIÉE

2.6 ENTRETIENS PRIMAIRES AVEC DES LEADERS D'OPINION CLÉS

2.7 GRILLE DE POSITIONNEMENT DU MARCHÉ DBMR

2.8 ANALYSE DE LA PART DES FOURNISSEURS DBMR

2.9 GRILLE DE COUVERTURE DES APPLICATIONS DU MARCHÉ

2.1 SOURCES SECONDAIRES

2.11 HYPOTHÈSES

3 RÉSUMÉ EXÉCUTIF

4 INFORMATIONS PREMIUM

4.1 LES CINQ FORCES DE PORTER

4.1.1 MENACE DE NOUVEAUX ENTRANTS

4.1.2 POUVOIR DE NÉGOCIATION DES FOURNISSEURS

4.1.3 POUVOIR DE NÉGOCIATION DES ACHETEURS

4.1.4 MENACE DE SUBSTITUTS

4.1.5 CONCURRENCE INTERNE

4.2 SCÉNARIO D'IMPORTATION-EXPORTATION

4.3 ANALYSE DES PRIX

4.4 ANALYSE DE LA CHAÎNE DE VALEUR : MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS

4.4.1 APPROVISIONNEMENT :

4.4.2 FABRICATION :

4.4.3 COMMERCIALISATION ET DISTRIBUTION :

4.5 PERSPECTIVES DE LA MARQUE

4.5.1 ANALYSE COMPARATIVE DES MARQUES

4.5.2 APERÇU PRODUIT VS MARQUE

4.6 AVANTAGE CONCURRENTIEL DE L'IMPLANTATION D'UNE USINE DE MATIÈRES GRASSES SPÉCIALES AUX EAU

4.6.1 EMPLACEMENT STRATÉGIQUE ET LOGISTIQUE : PORTE D'ENTRÉE VERS LE CCG ET LA RÉGION MENA

4.6.2 STABILITÉ ÉCONOMIQUE ET POLITIQUES FAVORABLES AUX INVESTISSEURS

4.6.3 DEMANDE INTÉRIEURE CROISSANTE ET SOPHISTICATION DES CONSOMMATEURS

4.6.4 INNOVATION DANS LE SECTEUR DE LA RESTAURATION ET DES BOISSONS AXÉE SUR LE TOURISME

4.6.5 INTÉGRATION AUX OBJECTIFS NATIONAUX DE SÉCURITÉ ALIMENTAIRE ET D'INNOVATION

4.6.6 ENGAGEMENTS EN MATIÈRE D'ÉCOSYSTÈME TECHNOLOGIQUE ET DE DURABILITÉ

4.6.7 ACCÈS AU MARCHÉ : ATTEINDRE LE MARCHÉ DU CCG DE 65 MILLIARDS DE DOLLARS

4.6.8 ACCORDS COMMERCIAUX GLOBAUX

4.6.9 DÉTAIL ET ÉLECTRONIQUE

4.6.9.1 EXPANSION COMMERCIALE

4.6.10 CONCLUSION

4.7 TENDANCES ÉMERGENTES ET PERSPECTIVES D'AVENIR

4.7.1 AXE SUR LA SANTÉ ET LE BIEN-ÊTRE

4.7.2 DIVERSITÉ CULINAIRE ET PREMIUMISATION

4.7.3 DURABILITÉ ET APPROVISIONNEMENT ÉTHIQUE

4.7.4 INNOVATION DANS L'OFFRE DE PRODUITS

4.7.5 PERSPECTIVES D'AVENIR

4.8 FACTEURS INFLUENÇANT LA DÉCISION D'ACHAT DES UTILISATEURS FINAUX

4.8.1 SENSIBILITÉ AUX COÛTS ET AUX PRIX

4.8.2 PERFORMANCES ET FONCTIONNALITÉS

4.8.3 TENDANCES EN MATIÈRE DE SANTÉ ET DE NUTRITION

4.8.4 CERTIFICATION HALAL ET CONFORMITÉ RÉGLEMENTAIRE

4.8.5 ÉTIQUETTE PROPRE ET TRANSPARENCE DES INGRÉDIENTS

4.8.6 RÉPUTATION DE LA MARQUE ET FIABILITÉ DES FOURNISSEURS

4.8.7 DURABILITÉ ET APPROVISIONNEMENT ÉTHIQUE

4.8.8 INNOVATION ET PERSONNALISATION DES PRODUITS

4.8.9 CONCLUSION

4.9 STRATÉGIES DE CROISSANCE ADOPTÉES PAR LES PRINCIPAUX ACTEURS DU MARCHÉ

4.9.1 CARGILL, INCORPORÉE

4.9.2 WILMAR INTERNATIONAL LTD

4.9.3 GROUPE ICC

4.9.4 HUILE COMESTIBLE USHA

4.9.5 APICAL

4.9.6 UNITED FOODS COMPANY

4.1 IMPACT DU RALENTISSEMENT ÉCONOMIQUE

4.10.1 IMPACT DU PRIX

4.10.2 IMPACT SUR LA CHAÎNE D'APPROVISIONNEMENT

4.10.3 L'AUGMENTATION DES COÛTS DES INTRANTS MET À FOND LES MARGES BÉNÉFICIAIRES

4.10.4 IMPACT SUR LES DÉCISIONS STRATÉGIQUES DE L'ENTREPRISE

4.10.5 CONCLUSION

4.11 TENDANCES DE L'INDUSTRIE ET PERSPECTIVES D'AVENIR

4.11.1 AXE SUR LA SANTÉ ET LE BIEN-ÊTRE

4.11.2 CONFORMITÉ RÉGLEMENTAIRE ET CERTIFICATION HALAL

4.11.3 CONCURRENCE ET INNOVATION

4.11.4 DURABILITÉ ET APPROVISIONNEMENT ÉTHIQUE

4.11.5 PROGRÈS TECHNOLOGIQUES

4.11.6 PERSPECTIVES D'AVENIR

4.11.7 CONCLUSION

4.12 ANALYSE DES INVESTISSEMENTS ET DES COÛTS POUR LA MISE EN PLACE D'UNE USINE DE FABRICATION DE MATIÈRES GRASSES SPÉCIALES AUX EAU

4.12.1 RÉPARTITION DES INVESTISSEMENTS EN CAPITAL

4.12.1.1 TERRAIN ET INFRASTRUCTURES

4.12.1.2 MACHINES ET ÉQUIPEMENTS

4.12.1.3 APPROVISIONNEMENT EN MATIÈRES PREMIÈRES

4.12.1.4 R&D et développement de produits

4.12.1.5 COÛTS DE MAIN-D'ŒUVRE ET D'EXPLOITATION

4.12.1.6 EMBALLAGE ET LOGISTIQUE

4.12.1.7 CONFORMITÉ ET CERTIFICATIONS

4.12.1.8 AUTRES

4.13 APERÇU DES INNOVATIONS TECHNOLOGIQUES

4.13.1 TECHNOLOGIES AVANCÉES DE MODIFICATION DES MATIÈRES GRASSES

4.13.2 UPCYCLING ET RÉDUCTION DES DÉCHETS

4.13.3 ÉTIQUETTE PROPRE ET TRANSPARENCE

4.13.4 APPROVISIONNEMENT DURABLE ET PRATIQUES ÉCOLOGIQUES

4.13.5 DÉVELOPPEMENT DE PRODUITS RESPECTUEUX DE LA SANTÉ

4.13.6 PERSONNALISATION ET MÉLANGES FONCTIONNELS

4.13.7 INTÉGRATION TECHNOLOGIQUE DANS LES INSTALLATIONS DE PRODUCTION

4.13.8 INITIATIVES DE RECHERCHE ET DÉVELOPPEMENT

4.13.9 CONCLUSION

4.14 APERÇU DE LA CAPACITÉ DE PRODUCTION

4.14.1 APERÇU

4.14.2 RÉPARTITION DES CAPACITÉS RÉGIONALES

4.14.3 ACTEURS CLÉS ET EMPREINTE DES INSTALLATIONS

4.14.4 DÉFIS ET PERSPECTIVES D'AVENIR

4.14.4.1 DÉFIS

4.14.4.2 PERSPECTIVES

4.15 ANALYSE DE L'APPROVISIONNEMENT EN MATIÈRES PREMIÈRES

4.15.1 HUILE DE PALME

4.15.2 HUILE DE PALMISTE (PKO)

4.15.3 BEURRE DE KARITÉ

4.15.4 BEURRE DE CACAO ET ÉQUIVALENTS DE BEURRE DE CACAO (CBES)

4.15.5 HUILE DE COCO

4.15.6 MATIÈRES GRASSES EXOTIQUES

4.16 ANALYSE DE LA CHAÎNE D'APPROVISIONNEMENT

4.16.1 APPROVISIONNEMENT EN MATIÈRES PREMIÈRES

4.16.2 TRANSFORMATION ET FABRICATION

4.16.3 ASSURANCE QUALITÉ ET CONFORMITÉ RÉGLEMENTAIRE

4.16.4 DISTRIBUTION ET LOGISTIQUE

4.16.5 INDUSTRIES D'UTILISATION FINALE

4.16.6 TENDANCES DE LA VENTE AU DÉTAIL ET DE LA CONSOMMATION

4.16.7 DÉFIS ET OPPORTUNITÉS

4.16.8 DÉFIS :

4.16.9 OPPORTUNITÉS :

4.16.10 CONCLUSION

4.17 LES TARIFS ET LEUR IMPACT SUR LE MARCHÉ

4.17.1 TAUX TARIFAIRES ACTUELS SUR LES 5 PRINCIPAUX MARCHÉS NATIONAUX

4.17.2 PERSPECTIVES : PRODUCTION LOCALE VS DÉPENDANCE AUX IMPORTATIONS

4.17.3 DYNAMIQUE DES CRITÈRES DE SÉLECTION DES FOURNISSEURS

4.17.4 IMPACT SUR LA CHAÎNE D'APPROVISIONNEMENT

4.17.4.1 APPROVISIONNEMENT EN MATIÈRES PREMIÈRES

4.17.4.2 FABRICATION ET PRODUCTION

4.17.4.3 LOGISTIQUE ET DISTRIBUTION

4.17.4.4 PRIX ET POSITIONNEMENT DU MARCHÉ

4.17.5 PARTICIPANTS DE L'INDUSTRIE : ACTIONS PROACTIVES

4.17.5.1 OPTIMISATION DE LA CHAÎNE D'APPROVISIONNEMENT

4.17.5.2 ÉTABLISSEMENTS DE COENTREPRISES

4.17.6 IMPACT SUR LES PRIX

4.17.7 INCLINAISON RÉGLEMENTAIRE

4.17.7.1 ALIGNEMENT COMMERCIAL ET ZLE DU CCG

4.17.7.2 ZONES SPÉCIALES ET MODÈLES DE RÉEXPORTATION

4.17.7.3 SUBVENTIONS LOCALES ET RÉPONSE POLITIQUE

4.17.7.4 COURS DE CORRECTION NATIONAL

5 COUVERTURE RÉGLEMENTAIRE

5.1 LICENCES INDUSTRIELLES ET COMMERCIALES

5.2 ENREGISTREMENT DE LA CHAMBRE DE COMMERCE ET DE LA MUNICIPALITÉ

5.3 SÉCURITÉ ALIMENTAIRE ET CONFORMITÉ AUX NORMES

5.4 CERTIFICATION HALAL

5.5 PERMIS ENVIRONNEMENTAUX ET DE DURABILITÉ

5.6 CERTIFICATIONS DE QUALITÉ ET DE PROCESSUS

6 APERÇU DU MARCHÉ

6.1 PILOTES

6.1.1 DEMANDE CROISSANTE DE L'INDUSTRIE DE LA BOULANGERIE ET DE LA CONFISERIE

6.1.2 SENSIBILISATION ACCRUE DES CONSOMMATEURS À LA SANTÉ ET À LA NUTRITION

6.1.3 AUGMENTATION DE LA POPULATION EXPATRIE ET INFLUENCE OCCIDENTALE

6.1.4 L'INDUSTRIE ALIMENTAIRE BIOLOGIQUE EN CROISSANCE RAPIDE

6.2 RESTRICTIONS

6.2.1 COÛTS ÉLEVÉS DES MATIÈRES GRASSES SPÉCIALES

6.3 OPPORTUNITÉS

6.3.1 EXPANSION DES PRODUITS À BASE DE PLANTES ET VÉGANS

6.3.2 PROGRÈS TECHNOLOGIQUES DANS LA MODIFICATION DES MATIÈRES GRASSES

6.3.3 DEMANDE CROISSANTE DE PRODUITS CERTIFIÉS HALAL ET CLEAN LABEL

6.4 DÉFIS

6.4.1 UNE CONCURRENCE FORTE DES HUILES ET DU BEURRE STANDARDS

6.4.2 LIMITES CLIMATIQUES POUR LA PRODUCTION LOCALE

7 MARCHÉS DES MATIÈRES GRASSES SPÉCIALES AUX EAU, PAR TYPE

7.1 APERÇU

7.2 ÉQUIVALENTS BEURRE DE CACAO (CBE)

7.3 SUBSTITUTS DE BEURRE DE CACAO (CBR)

7.4 SUBSTITUTS DU BEURRE DE CACAO (CBS)

7,5 AMÉLIORANTS DU BEURRE DE CACAO (CBI)

7.6 SUBSTITUTS DE MATIÈRES GRASSES DU LAIT (MFR)

7.7 SUBSTITUTS DE MATIÈRES GRASSES DU LAIT ANHYDRES (AMFR)

7.8 MATIÈRES GRASSES INTERESTÉRIFIÉES

7.9 STÉARIN DE KARITÉ ET DE SEL

7.1 OLÉINE DE KARITÉ ET DE SEL

7.11 HPMF IV 33-37

7.12 HPMF IV 45-47

7.13 MATIÈRES GRASSES DE BOULANGERIE

7.14 MATIÈRES GRASSES DE REMPLISSAGE

7.15 MARGARINES

7.16 AUTRES

8 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX EAU, PAR FORME

8.1 APERÇU

8.2 SEMI-SOLIDE

8.3 SOLIDE

8.4 LIQUIDE

9 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS, PAR SOURCE

9.1 APERÇU

9.2 MATIÈRES GRASSES SPÉCIALES D'ORIGINE VÉGÉTALE

9.3 MATIÈRES GRASSES SPÉCIALES D'ORIGINE ANIMALE

10 MARCHÉS DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION

10.1 APERÇU

10.2 INDUSTRIE ALIMENTAIRE ET DES BOISSONS

10.3 PRODUITS PHARMACEUTIQUES ET NUTRACEUTIQUES

10.4 COSMÉTIQUES ET SOINS PERSONNELS

10.5 ALIMENTS POUR ANIMAUX ET ALIMENTS POUR ANIMAUX DE COMPAGNIE

10.6 AUTRES

11 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR CANAL DE DISTRIBUTION

11.1 APERÇU

11.2 B2B (BUSINESS-TO-BUSINESS)

11.3 B2C (BUSINESS TO CONSUMER)

12 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : PAYSAGE DES ENTREPRISES

12.1 ANALYSE DES ACTIONS DE L'ENTREPRISE : EAU

13 ANALYSE SWOT

14 PROFIL DE L'ENTREPRISE

14.1 CARGILL, INCORPORÉE

14.1.1 INSTANTANÉ DE L'ENTREPRISE

14.1.2 PORTEFEUILLE DE PRODUITS

14.1.3 ÉVOLUTION RÉCENTE

14.2 WILMAR INTERNATIONAL LTD

14.2.1 INSTANTANÉ DE L'ENTREPRISE

14.2.2 ANALYSE DES REVENUS

14.2.3 PORTEFEUILLE DE PRODUITS/MARQUES

14.2.4 ÉVOLUTION RÉCENTE

14.3 GROUPE ICC

14.3.1 INSTANTANÉ DE L'ENTREPRISE

14.3.2 PORTEFEUILLE DE PRODUITS

14.3.3 ÉVOLUTION RÉCENTE

14.4 HUILE COMESTIBLE USHA

14.4.1 INSTANTANÉ DE L'ENTREPRISE

14.4.2 PORTEFEUILLE DE PRODUITS

14.4.3 ÉVOLUTION RÉCENTE

14,5 APICAL

14.5.1 INSTANTANÉ DE L'ENTREPRISE

14.5.2 PORTEFEUILLE DE PRODUITS

14.5.3 ÉVOLUTION RÉCENTE

14.6 SERVICES AL TAWUN SOLYMAN (FZE)

14.6.1 INSTANTANÉ DE L'ENTREPRISE

14.6.2 PORTEFEUILLE DE PRODUITS

14.6.3 ÉVOLUTION RÉCENTE

14,7 DULZER

14.7.1 INSTANTANÉ DE L'ENTREPRISE

14.7.2 PORTEFEUILLE DE PRODUITS

14.7.3 ÉVOLUTION RÉCENTE

14.8 COMMERCE D'HUILE COMESTIBLE SAHA

14.8.1 INSTANTANÉ DE L'ENTREPRISE

14.8.2 PORTEFEUILLE DE PRODUITS

14.8.3 ÉVOLUTION RÉCENTE

14.9 GROUPE SHAHRAAN

14.9.1 INSTANTANÉ DE L'ENTREPRISE

14.9.2 PORTEFEUILLE DE PRODUITS

14.9.3 ÉVOLUTION RÉCENTE

14.1 UNITED FOODS COMPANY

14.10.1 INSTANTANÉ DE L'ENTREPRISE

14.10.2 ANALYSE DES REVENUS

14.10.3 PORTEFEUILLE DE PRODUITS

14.10.4 ÉVOLUTION RÉCENTE

15 QUESTIONNAIRE

16 RAPPORTS CONNEXES

Liste des tableaux

TABLE 1 COMPARATIVE BRAND ANALYSIS: KEY PLAYERS

TABLE 2 PRODUCT VS BRAND OVERVIEW

TABLE 3 COMPREHENSIVE ECONOMIC PARTNERSHIP AGREEMENTS

TABLE 4 REGULATORY COVERAGE

TABLE 5 TYPES OF FATS AND THEIR NUTRITIONAL BENEFITS

TABLE 6 U.A.E. SPECIALITY FATS MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 7 U.A.E. COCOA BUTTER EQUIVALENTS (CBE) IN SPECIALTY FATS MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 8 U.A.E. COCOA BUTTER REPLACERS (CBR) IN SPECIALTY FATS MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 9 U.A.E. COCOA BUTTER SUBSTITUTES (CBS) IN SPECIALTY FATS MARKET, BY TYPE, 2018-2032 (USD THOUSAND)

TABLE 10 U.A.E. SPECIALITY FATS MARKET, BY FORM, 2018-2032 (USD THOUSAND)

TABLE 11 U.A.E. SPECIALITY FATS MARKET, BY SOURCE,2018-2032 (USD THOUSAND)

TABLE 12 U.A.E. PLANT-BASED SPECIALTY FATS IN SPECIALTY FATS MARKET, BY SOURCE, 2018-2032 (USD THOUSAND)

TABLEAU 13 MATIÈRES GRASSES SPÉCIALES D'ORIGINE ANIMALE SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES DES ÉMIRATS ARABES UNIS, PAR SOURCE, 2018-2032 (EN MILLIERS USD)

TABLEAU 14 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 15 INDUSTRIE ALIMENTAIRE ET DES BOISSONS DES ÉMIRATS ARABES UNIS SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 16 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES DE LA BOULANGERIE ET DE LA CONFISERIE AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 17 ALTERNATIVES AUX PRODUITS LAITIERS ET ALIMENTS À BASE DE PLANTES SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 18 HUILES DE FRITURE ET DE CUISSON SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 19 NUTRITION INFANTILE SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 20 PRODUITS PHARMACEUTIQUES ET NUTRACEUTIQUES SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 21 COSMÉTIQUES ET SOINS PERSONNELS AUX ÉMIRATS ARABES UNIS SUR LE MARCHÉ DES GRAISSES SPÉCIALISÉES, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 22 ALIMENTS POUR ANIMAUX ET ALIMENTS POUR ANIMAUX DE COMPAGNIE SUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR APPLICATION, 2018-2032 (EN MILLIERS USD)

TABLEAU 23 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS, PAR CANAL DE DISTRIBUTION, 2018-2032 (EN MILLIERS USD)

TABLEAU 24 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES (B2C) AUX EAU, PAR CANAL DE DISTRIBUTION, 2018-2032 (EN MILLIERS USD)

Liste des figures

FIGURE 1 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS

FIGURE 2 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : TRIANGULATION DES DONNÉES

FIGURE 3 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : ANALYSE DROC

FIGURE 4 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : ANALYSE DU MARCHÉ MONDIAL ET RÉGIONAL

FIGURE 5 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : ANALYSE DE LA RECHERCHE DES ENTREPRISES

FIGURE 6 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : MODÉLISATION MULTIVARIÉE

FIGURE 7 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : DONNÉES DÉMOGRAPHIQUES DES ENTRETIENS

FIGURE 8 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : GRILLE DE POSITIONNEMENT DU MARCHÉ DBMR

FIGURE 9 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : ANALYSE DES PARTS DE FOURNISSEURS

FIGURE 10 RÉSUMÉ EXÉCUTIF

FIGURE 11 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : SEGMENTATION

FIGURE 12 QUINZE SEGMENTS COMPOSENT LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES DES ÉMIRATS ARABES UNIS, PAR TYPE (2024)

FIGURE 13 DÉCISIONS STRATÉGIQUES

FIGURE 14 LA DEMANDE CROISSANTE DE L'INDUSTRIE DE LA BOULANGERIE ET DE LA CONFISERIE DEVRAIT STIMULER LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES DES ÉMIRATS ARABES UNIS AU COURS DE LA PÉRIODE DE PRÉVISION (2025-2032)

FIGURE 15 LES ÉQUIVALENTS BEURRE DE CACAO (CBE) DEVRAIENT REPRÉSENTER LA PLUS GRANDE PART DU MARCHÉ DES MATIÈRES GRASSES SPÉCIALES DES ÉMIRATS ARABES UNIS EN 2025 ET 2032

FIGURE 16 LES CINQ FORCES DE PORTER

FIGURE 17 SCÉNARIO D'IMPORTATION-EXPORTATION (EN MILLIERS USD)

FIGURE 18 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS, 2024-2032, PRIX DE VENTE MOYEN (USD/KG)

FIGURE 19 ANALYSE DE LA CHAÎNE DE VALEUR DU MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS

FIGURE 20 MOTEURS, CONTRAINTES, OPPORTUNITÉS ET DÉFIS POUR LE MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS

FIGURE 21 POPULATION D'EXPATRIÉS DE DIFFÉRENTS PAYS AUX ÉMIRATS ARABES UNIS

FIGURE 22 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : PAR TYPE, 2024

FIGURE 23 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : PAR FORME, 2024

FIGURE 24 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : PAR SOURCE, 2024

FIGURE 25 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : PAR APPLICATION, 2024

FIGURE 26 MARCHÉ DES MATIÈRES GRASSES SPÉCIALISÉES AUX ÉMIRATS ARABES UNIS : PAR CANAL DE DISTRIBUTION, 2024

FIGURE 27 MARCHÉ DES MATIÈRES GRASSES SPÉCIALES AUX ÉMIRATS ARABES UNIS : PART DE L'ENTREPRISE EN 2024 (%)

Méthodologie de recherche

La collecte de données et l'analyse de l'année de base sont effectuées à l'aide de modules de collecte de données avec des échantillons de grande taille. L'étape consiste à obtenir des informations sur le marché ou des données connexes via diverses sources et stratégies. Elle comprend l'examen et la planification à l'avance de toutes les données acquises dans le passé. Elle englobe également l'examen des incohérences d'informations observées dans différentes sources d'informations. Les données de marché sont analysées et estimées à l'aide de modèles statistiques et cohérents de marché. De plus, l'analyse des parts de marché et l'analyse des tendances clés sont les principaux facteurs de succès du rapport de marché. Pour en savoir plus, veuillez demander un appel d'analyste ou déposer votre demande.

La méthodologie de recherche clé utilisée par l'équipe de recherche DBMR est la triangulation des données qui implique l'exploration de données, l'analyse de l'impact des variables de données sur le marché et la validation primaire (expert du secteur). Les modèles de données incluent la grille de positionnement des fournisseurs, l'analyse de la chronologie du marché, l'aperçu et le guide du marché, la grille de positionnement des entreprises, l'analyse des brevets, l'analyse des prix, l'analyse des parts de marché des entreprises, les normes de mesure, l'analyse globale par rapport à l'analyse régionale et des parts des fournisseurs. Pour en savoir plus sur la méthodologie de recherche, envoyez une demande pour parler à nos experts du secteur.

Personnalisation disponible

Data Bridge Market Research est un leader de la recherche formative avancée. Nous sommes fiers de fournir à nos clients existants et nouveaux des données et des analyses qui correspondent à leurs objectifs. Le rapport peut être personnalisé pour inclure une analyse des tendances des prix des marques cibles, une compréhension du marché pour d'autres pays (demandez la liste des pays), des données sur les résultats des essais cliniques, une revue de la littérature, une analyse du marché des produits remis à neuf et de la base de produits. L'analyse du marché des concurrents cibles peut être analysée à partir d'une analyse basée sur la technologie jusqu'à des stratégies de portefeuille de marché. Nous pouvons ajouter autant de concurrents que vous le souhaitez, dans le format et le style de données que vous recherchez. Notre équipe d'analystes peut également vous fournir des données sous forme de fichiers Excel bruts, de tableaux croisés dynamiques (Fact book) ou peut vous aider à créer des présentations à partir des ensembles de données disponibles dans le rapport.