Asia

Market Size in USD Billion

CAGR :

%

USD

186.36 Billion

USD

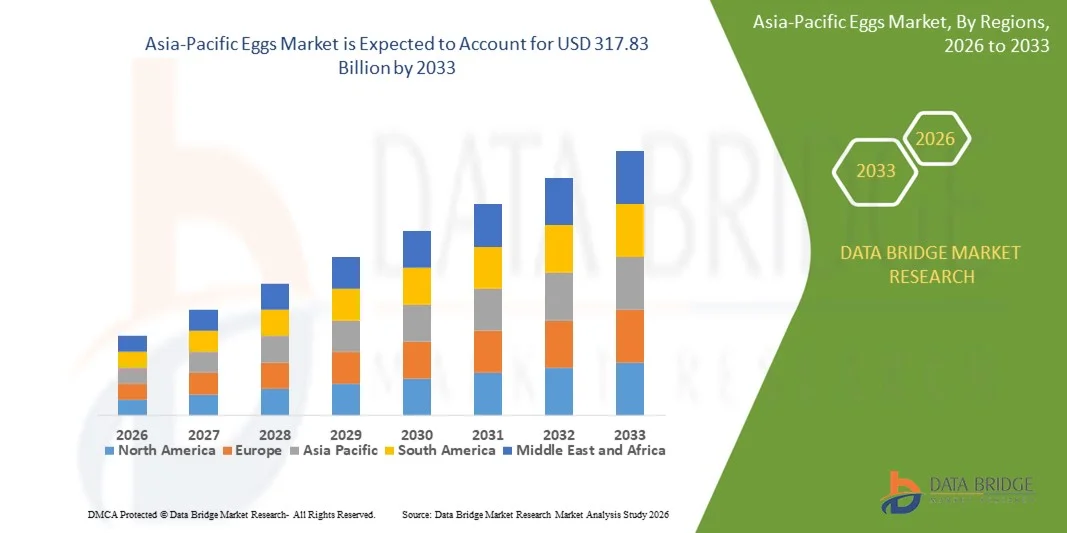

317.83 Billion

2025

2033

USD

186.36 Billion

USD

317.83 Billion

2025

2033

| 2026 –2033 | |

| USD 186.36 Billion | |

| USD 317.83 Billion | |

| % | |

|

Asia-Pacific Eggs Market Segmentation, By Product Type (Shell Egg and Processed Eggs), Source (Plant Based Egg and Animal Based Egg), Category (Conventional and Organic), Packaging Type (Trays, Boxes & Carton, Cans, Bottles, Pouches, and Others), Specialty (Gluten Free, Low Cholesterol, High Protein, and Others), End User (Retail/Household and Food Service Sector), Distribution Channel (Store Based Retailer and Non-Store Based Retailer)- Industry Trends and Forecast to 2033

Asia-Pacific Eggs Market Size

- The Asia-Pacific eggs market size was valued at USD 186.36 billion in 2025 and is expected to reach USD 317.83 billion by 2033, at a CAGR of 6.90% during the forecast period

- The market growth is largely fuelled by the rising consumer demand for protein-rich and nutritious food products, increasing awareness of health and wellness, and the growing adoption of eggs in processed and convenience food segments

- Expansion of the foodservice industry, including restaurants, bakeries, and quick-service outlets, is also contributing to market growth

Asia-Pacific Eggs Market Analysis

- Eggs are widely consumed as a staple protein source across households and foodservice channels, with growing popularity in processed foods, bakery products, and ready-to-eat meals

- Increasing focus on health, nutrition, and functional foods is driving the adoption of eggs globally, while advances in farming practices and supply chain efficiencies are enhancing production and distribution

- China dominated the eggs market in Asia-Pacific with the largest revenue share in 2025, supported by its vast poultry farming base, high production capacity, and strong domestic consumption across both urban and rural populations

- Japan is expected to witness the highest compound annual growth rate (CAGR) in the Asia-Pacific eggs market due to increasing demand for premium and value-added egg products, rising health consciousness, and growing preference for safe, high-quality, and protein-rich food options

- The shell egg segment held the largest market revenue share in 2025 driven by its widespread use in households and foodservice applications. Shell eggs are preferred for their versatility in cooking, baking, and direct consumption, making them a staple in daily diets. Moreover, their natural form and minimal processing appeal to consumers seeking fresh and wholesome products. The segment continues to benefit from consistent production standards and established distribution networks

Report Scope and Asia-Pacific Eggs Market Segmentation

|

Attributes |

Asia-Pacific Eggs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Asia-Pacific Eggs Market Trends

Rising Demand For Protein-Rich And Nutrient-Dense Foods

- The growing focus on health, nutrition, and functional diets is significantly shaping the eggs market, as consumers increasingly prefer protein-rich, nutrient-dense, and versatile food sources. Eggs are gaining traction due to their affordability, high nutritional value, and functional properties in cooking and baking. This trend strengthens their adoption across households, foodservice, and processed food industries, encouraging manufacturers to innovate with new formulations that cater to evolving consumer preferences

- Increasing awareness around wellness, balanced diets, and convenience foods has accelerated the demand for eggs in bakery, confectionery, ready-to-eat meals, and packaged food products. Health-conscious consumers are actively seeking products formulated with eggs for their protein, vitamins, and minerals, prompting brands to prioritize sustainable sourcing and quality standards

- Clean-label and functional food trends are influencing purchasing decisions, with manufacturers emphasizing transparent sourcing, animal welfare, and certification labels. These factors are helping brands differentiate products in a competitive market and build consumer trust, while also driving the adoption of organic, free-range, and fortified eggs

- For instance, in 2024, Michael Foods expanded its egg-based product portfolio by launching liquid and powdered egg products designed for convenience and bakery applications, addressing the growing demand for ready-to-use protein sources

- While demand for eggs is growing, sustained market expansion depends on continuous innovation in product formats, supply chain efficiency, and cost-effective production. Manufacturers are also focusing on improving egg-based value-added products, maintaining quality standards, and developing convenient and fortified egg offerings for broader adoption

Asia-Pacific Eggs Market Dynamics

Driver

Growing Preference For Protein-Rich And Nutrient-Dense Foods

- Rising consumer demand for protein-rich, nutrient-dense, and versatile foods is a major driver for the eggs market. Manufacturers are increasingly incorporating eggs into a wide range of products to meet dietary preferences, improve product appeal, and comply with health-oriented trends. This trend is also pushing research into enriched, organic, and specialty eggs, supporting product diversification

- Expanding applications in bakery, confectionery, dairy alternatives, spreads, and ready-to-eat products are influencing market growth. Eggs help enhance texture, stability, and nutritional profile while maintaining natural positioning of products, enabling manufacturers to meet consumer expectations for high-quality, functional offerings

- Foodservice and processed food manufacturers are actively promoting egg-based formulations through product innovation, marketing campaigns, and industry certifications. These efforts are supported by the growing consumer preference for health-oriented and convenient products, and they also encourage partnerships between egg producers and brands to improve product quality and reduce operational inefficiencies

- For instance, in 2023, Cal-Maine Foods introduced fortified and omega-3 enriched eggs for retail and foodservice channels, catering to health-conscious consumers and boosting repeat purchases. The launch included liquid, powdered, and shell eggs, providing versatile options for bakery, ready-to-eat, and protein-fortified food applications. This initiative helped strengthen the company’s presence in the functional foods segment and encouraged other producers to innovate with nutritionally enhanced egg products

- Although rising health, wellness, and protein-rich diet trends support growth, wider adoption depends on cost optimization, ingredient availability, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced processing technology will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

Higher Cost And Supply Variability Compared To Conventional Protein Sources

- The relatively higher cost of specialty, organic, or free-range eggs compared to conventional eggs remains a key challenge, limiting adoption among price-sensitive consumers and manufacturers. Higher feed, labor, and certification costs contribute to elevated pricing, while fluctuating supply can affect availability and market penetration

- Consumer and manufacturer awareness of specialty or fortified eggs remains uneven, particularly in emerging markets where protein-rich diets are still developing. Limited understanding of functional and nutritional benefits restricts adoption across certain product categories

- Supply chain and distribution challenges also impact market growth, as eggs require proper handling, cold storage, and adherence to quality standards. Logistical complexities, shorter shelf life, and seasonality can increase operational costs

- For instance, in 2024, Rose Acre Farms faced distribution challenges due to cold storage limitations, which temporarily affected the supply of specialty and organic eggs to retail outlets. To overcome this, the company invested in expanding refrigerated storage and optimized its logistics network, ensuring consistent delivery of high-quality eggs. These measures also highlighted the importance of infrastructure improvements for sustaining growth in the specialty and organic egg segment, encouraging better supply chain management practices across the industry

- Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for manufacturers and consumers. Collaboration with retailers, foodservice operators, and certification bodies can help unlock the long-term growth potential of the global eggs market. Furthermore, developing cost-competitive, fortified, and value-added egg products, while strengthening marketing strategies around health and nutrition benefits, will be essential for widespread adoption

Asia-Pacific Eggs Market Scope

The market is segmented on the basis of product type, source, category, packaging type, specialty, end user, and distribution channel.

- By Product Type

On the basis of product type, the Asia-Pacific eggs market is segmented into shell eggs and processed eggs. The shell egg segment held the largest market revenue share in 2025 driven by its widespread use in households and foodservice applications. Shell eggs are preferred for their versatility in cooking, baking, and direct consumption, making them a staple in daily diets. Moreover, their natural form and minimal processing appeal to consumers seeking fresh and wholesome products. The segment continues to benefit from consistent production standards and established distribution networks.

The processed eggs segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for ready-to-use and convenience egg products in the foodservice industry. Processed eggs offer benefits such as extended shelf life, ease of storage, and standardized quality, making them increasingly popular among commercial kitchens and packaged food manufacturers. Innovation in liquid, powdered, and pre-cooked egg products is also driving adoption, especially in urban areas with fast-paced lifestyles.

- By Source

On the basis of source, the market is segmented into plant-based eggs and animal-based eggs. Animal-based eggs dominated the market in 2025 due to their established consumption patterns and high protein content, which is widely recognized by consumers. They are also preferred for their natural taste, texture, and suitability across various culinary applications. In addition, animal-based eggs benefit from a mature supply chain and strong consumer trust.

Plant-based eggs is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing vegan and vegetarian diets, along with rising awareness about sustainability and animal welfare. These alternatives are gaining popularity in both retail and foodservice sectors as healthier and environmentally friendly options. Continuous product innovation, such as plant-based liquid eggs and egg substitutes for baking, is further expanding their market reach.

- By Category

On the basis of category, the market is segmented into conventional and organic eggs. Conventional eggs held the largest share in 2025 owing to their affordability, availability, and consistent supply across retail channels. They are widely accepted by households for daily consumption and meet the standard regulatory quality requirements. The convenience and cost-effectiveness of conventional eggs continue to support strong demand across Asia-Pacific.

Organic eggs is expected to witness the fastest growth rate from 2026 to 2033 as consumers increasingly prefer chemical-free, pesticide-free, and naturally raised products for better health and nutrition. Rising disposable incomes, health-conscious eating habits, and awareness of animal welfare are major factors driving the adoption of organic eggs. Specialty retailers and supermarkets are also expanding their organic egg offerings, making them more accessible to urban consumers.

- By Packaging Type

On the basis of packaging type, the market is segmented into trays, boxes & cartons, cans, bottles, pouches, and others. Trays dominated the market in 2025 due to their convenience, cost-effectiveness, and ease of transportation and storage. They also help in reducing egg breakage during distribution and offer consumers an easy-to-handle format for household use. The standardization of tray sizes supports bulk buying for both retail and foodservice segments.

Cans is expected to witness the fastest growth rate from 2026 to 2033, driven by the expansion of liquid and powdered egg products in commercial and industrial applications. These formats provide extended shelf life and precise portioning, which is particularly attractive for bakeries, hotels, and ready-to-eat food manufacturers. Innovation in packaging for processed egg products is also improving convenience and reducing wastage.

- By Specialty

On the basis of specialty, the market is segmented into gluten free, low cholesterol, high protein, and others. High-protein eggs accounted for the largest share in 2025 due to the growing focus on fitness, bodybuilding, and protein-rich diets. Consumers increasingly prefer eggs as a natural source of protein and essential nutrients, supporting their widespread adoption in health-conscious diets. This segment also benefits from promotional campaigns highlighting the nutritional advantages of eggs.

Low-cholesterol is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing health consciousness and preventive healthcare measures among consumers. Demand for eggs fortified with vitamins, minerals, and functional ingredients is also rising. Specialty eggs are being promoted in retail and foodservice sectors as premium products that cater to specific dietary needs and wellness trends.

- By End User

On the basis of end user, the market is segmented into retail/household and food service sector. The retail/household segment held the largest revenue share in 2025 due to consistent household consumption and easy availability of eggs in supermarkets and grocery stores. Eggs remain a daily staple in Asia-Pacificn diets, and promotional strategies by retailers further encourage repeat purchases. Seasonal demand peaks, such as during holidays, also strengthen retail sales.

The food service sector is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand from restaurants, hotels, and catering services for processed and convenient egg products. The increasing popularity of prepared meals, bakeries, and fast-food chains is creating steady demand for both shell and processed eggs. Moreover, commercial kitchens benefit from time-saving pre-processed egg products that ensure consistency and reduce labor requirements.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into store-based retailers and non-store-based retailers. Store-based retailers dominated the market in 2025, as supermarkets, hypermarkets, and local grocery stores remain the primary source of egg purchases for consumers. These channels provide wide product variety, in-store promotions, and trusted quality assurance, which continue to attract household buyers. Convenience and brand visibility in stores also support strong sales.

Non-store-based retailers is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing online grocery shopping and home delivery services. Consumers are embracing digital ordering for convenience, subscription models, and contactless delivery. This channel is particularly appealing to urban populations seeking hassle-free purchasing and access to specialty egg products not always available in physical stores.

Asia-Pacific Eggs Market Regional Analysis

- China dominated the eggs market in Asia-Pacific with the largest revenue share in 2025, supported by its vast poultry farming base, high production capacity, and strong domestic consumption across both urban and rural populations

- The country benefits from well-established supply chains, increasing modernization of layer farming operations, and growing integration of automated feeding and processing technologies

- Rising demand from food processing industries, bakery applications, and convenience food manufacturers further reinforces China’s leadership position in the regional eggs market

Japan Eggs Market Insight

The Japan eggs market i is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for premium and value-added egg products, strong consumer preference for high-quality and safe food options, and growing consumption of protein-rich diets. Expanding innovation in packaged, processed, and ready-to-eat egg products, along with advanced cold chain infrastructure and retail expansion, is further accelerating market growth

Asia-Pacific Eggs Market Share

The Asia-Pacific eggs industry is primarily led by well-established companies, including:

- ISE Foods Inc. (Japan)

- JA ZEN-NOH Tamago Co., Ltd. (Japan)

- NH Foods Ltd. (Japan)

- Charoen Pokphand Foods PCL (Thailand)

- Betagro Group (Thailand)

- Japfa Ltd. (Singapore)

- Srinivasa Farms Private Limited (India)

- Venky’s (India) Limited (India)

- Hy-Line International (China)

- Beijing DQY Agriculture & Technology Co., Ltd. (China)

- New Hope Liuhe Co., Ltd. (China)

- PT Charoen Pokphand Indonesia Tbk (Indonesia)

- San Miguel Foods, Inc. (Philippines)

- Farm Pride Foods Ltd. (Australia)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。