アジア太平洋地域ヘルスケア情報技術(IT)市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

81.19 Billion

USD

264.34 Billion

2025

2033

USD

81.19 Billion

USD

264.34 Billion

2025

2033

| 2026 –2033 | |

| USD 81.19 Billion | |

| USD 264.34 Billion | |

| % | |

|

アジア太平洋地域のヘルスケア情報技術(IT)市場のセグメンテーション:ソリューションとサービス別(ソリューション、HCITアウトソーシングサービス、その他)、コンポーネントタイプ別(ソフトウェア、ハードウェア)、提供モード別(オンプレミス、クラウドベース)、エンドユーザー別(プロバイダー、ペイラー) - 業界動向と2033年までの予測

アジア太平洋地域のヘルスケア情報技術(IT)市場規模

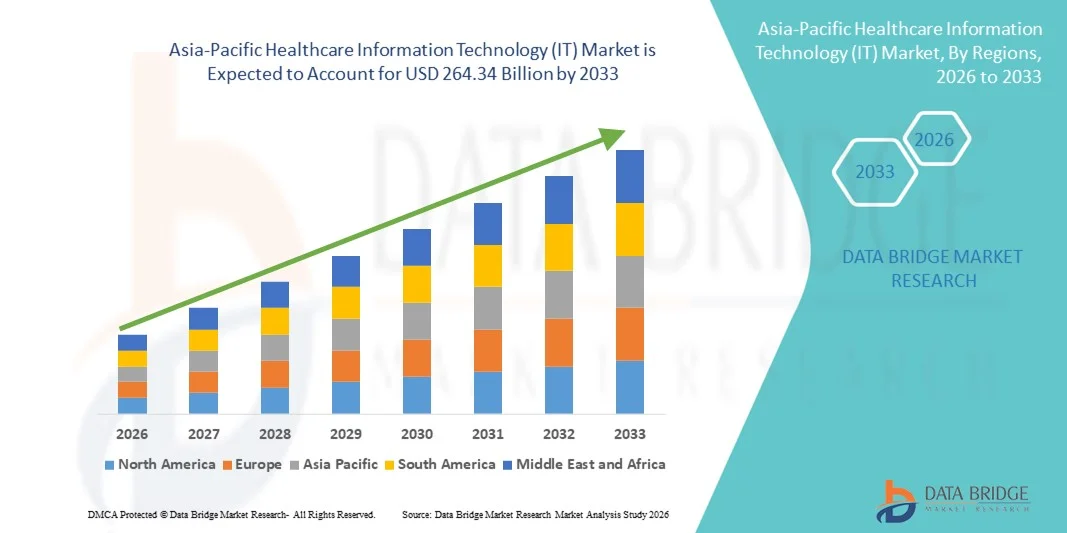

- アジア太平洋地域のヘルスケア情報技術(IT)市場規模は、2025年には811億9,000万米ドルと評価され、予測期間中の年平均成長率(CAGR)15.90%で、2033年には2,643億4,000万米ドル に達すると予測されています。

- 市場の成長は、デジタルヘルスシステム、電子カルテ(EHR)、遠隔医療プラットフォーム、クラウドベースのヘルスケアソリューションの普及拡大によって大きく促進されており、病院、診療所、その他の医療施設におけるデジタル変革の強化につながっています。データ分析、人工知能、相互運用性ソリューションにおける継続的な技術進歩は、医療インフラの近代化をさらに加速させています。

- さらに、効率的な患者データ管理、臨床転帰の改善、規制遵守、コスト最適化に対する需要の高まりにより、医療情報技術(IT)ソリューションは現代の医療提供において不可欠な要素となっています。これらの要因が複合的に作用することで、医療ITシステムの普及が加速し、業界の成長を大きく促進しています。

アジア太平洋地域のヘルスケア情報技術(IT)市場分析

- 電子カルテ(EHR)、病院情報システム(HIS)、遠隔医療プラットフォーム、医療データ分析などを含む医療情報技術(IT)ソリューションは、業務効率の向上、患者の転帰の改善、データに基づいた意思決定の実現を可能にする能力から、公立および私立の医療機関における現代の医療提供においてますます不可欠なものになりつつあります。

- 医療ITシステムに対する需要の高まりは、主に政府主導のデジタルヘルス構想、患者数の増加、正確な医療記録の必要性の高まり、そして病院や診断センターにおけるクラウドベースおよびAI対応の医療ソリューションの普及拡大によって促進されている。

- 中国は、病院における急速なデジタル変革、電子カルテ(EHR)、遠隔医療プラットフォーム、AIベースの医療ソリューションの普及拡大、そしてスマート病院インフラを推進する強力な政府イニシアチブに牽引され、2025年には医療情報技術(IT)市場で37.1%という最大の収益シェアを獲得し、市場を席巻した。

- インドは、医療情報技術(IT)市場において予測期間中に最も急速に成長する地域になると予想されており、2026年から2033年にかけて年平均成長率(CAGR)13.4%で拡大すると見込まれています。これは、医療のデジタル化の進展、ヘルステック系スタートアップへの投資増加、デジタルヘルスエコシステムを推進する政府プログラム、クラウドベースの病院管理および遠隔医療ソリューションへの需要の高まりによって支えられています。

- オンプレミス型セグメントは、2025年には市場収益の55.3%を占め、最大のシェアを獲得した。これは主に、大規模病院におけるデータセキュリティへの懸念と、確立されたITインフラによるものである。

レポートの範囲とヘルスケア情報技術(IT)市場のセグメンテーション

|

属性 |

医療情報技術(IT)の主要市場インサイト |

|

対象分野 |

|

|

対象国 |

アジア太平洋

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成する市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業といった市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みなども含まれています。 |

アジア太平洋地域のヘルスケア情報技術(IT)市場動向

医療システムにおけるデジタル変革と相互運用性の加速

- インドの医療情報技術(IT)市場における重要かつ加速的なトレンドは、電子カルテ(EHR)、病院情報システム(HIS)、遠隔医療プラットフォーム、医療データ相互運用性フレームワークの導入など、医療インフラの急速なデジタル変革です。この変革は、業務効率の向上、患者ケアの連携強化、そして病院や診療所全体におけるデータに基づいた臨床意思決定の実現を可能にしています。

- For instance, the Government of India’s Ayushman Bharat Digital Mission (ABDM) is actively promoting the creation of digital health IDs and integrated health records, enabling seamless data exchange across healthcare providers and strengthening nationwide healthcare connectivity

- The increasing integration of cloud-based healthcare IT solutions is enabling hospitals and diagnostic centers to store, access, and analyze patient information securely and efficiently. Healthcare providers are leveraging advanced analytics tools to improve disease surveillance, optimize hospital workflows, and reduce administrative burdens

- The shift toward paperless healthcare environments is also improving transparency, reducing medical errors, and enhancing patient engagement through digital appointment scheduling, e-prescriptions, and remote consultations

- Private hospitals and diagnostic chains are investing heavily in integrated IT platforms to streamline billing, claims management, laboratory information systems, and radiology information systems. This integration supports improved turnaround times and better financial management

- The growing demand for data standardization, interoperability, and centralized healthcare information exchange is reshaping the healthcare delivery landscape in India, positioning Healthcare IT as a critical backbone of modern medical infrastructure

Asia-Pacific Healthcare Information Technology (IT) Market Dynamics

Driver

Increasing Healthcare Digitization and Government Initiatives

- The rising emphasis on healthcare digitization, supported by strong government initiatives and regulatory driver propelling the growth of the India Healthcare Information Technology (IT) market

- Programs focused on universal health coverage and digital health ecosystems are encouraging hospitals and clinics to modernize their IT infrastructure

- For instance, initiatives under the National Digital Health Blueprint and Ayushman Bharat Digital Mission are facilitating the integration of digital health records, telemedicine services, and centralized health data repositories, significantly accelerating Healthcare IT adoption across public and private sectors

- The growing burden of chronic diseases, increasing patient volumes, and demand for efficient healthcare delivery systems are compelling providers to adopt automated workflow management, digital documentation, and advanced analytics tools

- Furthermore, the rapid expansion of private healthcare facilities and multispecialty hospitals in tier II and tier III cities is driving the need for scalable and cost-effective IT solutions to manage clinical and administrative operations efficiently

- The increasing penetration of smartphones and internet connectivity in rural and semi-urban regions is also supporting telehealth expansion, remote monitoring solutions, and digital consultation services, further contributing to market growth. reforms, is a major

Restraint/Challenge

Data Privacy Concerns and High Implementation Costs

- Concerns regarding data privacy, cybersecurity risks, and regulatory compliance pose significant challenges to the widespread adoption of Healthcare Information Technology solutions in Asia Pacific. As healthcare institutions digitize sensitive patient information, risks related to data breaches and unauthorized access remain critical concerns

- For instance, reported incidents of hospital data breaches and ransomware attacks in the healthcare sector have heightened awareness around the need for stronger cybersecurity frameworks, making some smaller healthcare providers cautious about rapid digital adoption

- Ensuring compliance with data protection regulations, implementing robust encryption systems, and maintaining secure cloud environments require substantial investment, which can be challenging for small and mid-sized healthcare facilities. In addition, the high initial cost of implementing comprehensive hospital information systems, including hardware infrastructure, software licensing, and staff training, may limit adoption in resource-constrained settings

- Resistance to change among healthcare professionals and lack of technical expertise in certain regions further slowdown implementation and optimal utilization of Healthcare IT systems

- Overcoming these challenges through improved cybersecurity standards, government incentives, training programs, and the development of affordable, scalable Healthcare IT platforms will be essential to ensure sustained and inclusive market growth across India

Asia-Pacific Healthcare Information Technology (IT) Market Scope

The market is segmented on the basis of product and services, components, delivery mode, and end-users.

- By Product and Services

On the basis of product and services, the Healthcare Information Technology (IT) market is segmented into Healthcare Provider Solutions, Healthcare Payer Solutions, and HCIT Outsourcing Services. The Healthcare Provider Solutions segment dominated the largest market revenue share of 46.8% in 2025, driven by the widespread adoption of electronic health records (EHRs), clinical decision support systems, and hospital information systems. Hospitals and physician practices are increasingly investing in digital platforms to enhance patient care, streamline workflows, and improve clinical outcomes. Regulatory mandates promoting EHR adoption further strengthen segment dominance. Integration of telehealth, e-prescribing, and population health management tools supports comprehensive care delivery. Growing patient volumes and the need for data-driven decision-making accelerate solution deployment. Interoperability requirements encourage healthcare facilities to upgrade IT infrastructure. Rising focus on value-based care models further fuels demand. Provider solutions also enable real-time analytics and reporting capabilities. Strong government funding initiatives support digital transformation in hospitals. Continuous innovation in AI-powered diagnostics enhances provider efficiency. Overall, healthcare provider solutions maintain leadership due to high adoption across hospitals and clinics and continuous regulatory support.

The HCIT Outsourcing Services segment is anticipated to witness the fastest CAGR of 13.4% from 2026 to 2033, fueled by the increasing need to reduce operational costs and improve IT efficiency. Healthcare organizations are outsourcing IT management, revenue cycle management, and infrastructure services to specialized vendors. Growing complexity of regulatory compliance drives demand for third-party expertise. Cloud migration initiatives further boost outsourcing partnerships. Smaller hospitals and clinics prefer outsourcing to avoid high capital expenditure. Demand for cybersecurity and data protection services accelerates segment growth. Expansion of telehealth platforms increases reliance on managed IT services. Outsourcing also enhances scalability and flexibility for healthcare providers. Globalization of healthcare services supports offshore IT support models. Continuous technological upgrades necessitate expert external support. Rising adoption of subscription-based service models further strengthens demand. Overall, HCIT outsourcing services represent the fastest-growing segment due to cost-efficiency, scalability, and rising digital complexity.

- By Components

On the basis of components, the Healthcare Information Technology (IT) market is segmented into Services, Software, and Hardware. The Services segment dominated the largest market revenue share of 41.9% in 2025, driven by the growing demand for implementation, maintenance, consulting, and training services. Healthcare institutions require continuous support for system integration and upgrades. Increasing cybersecurity threats necessitate ongoing monitoring and risk assessment services. Regulatory compliance requirements push hospitals to seek professional IT advisory services. Expansion of digital health platforms demands technical support and customization. Interoperability challenges further strengthen reliance on service providers. Healthcare facilities prioritize workflow optimization and data analytics services. Managed services contracts ensure long-term revenue streams. Growing complexity of IT ecosystems increases service dependency. Rising telemedicine adoption requires continuous system support. Overall, the services component leads the market due to sustained demand for technical expertise and system management.

The Software segment is expected to witness the fastest CAGR of 12.7% from 2026 to 2033, driven by advancements in AI-based analytics, electronic medical records, and cloud-native healthcare platforms. Demand for patient engagement solutions and remote monitoring software accelerates growth. Software upgrades enable predictive analytics and personalized medicine initiatives. Expansion of digital therapeutics and mobile health applications strengthens adoption. Healthcare providers increasingly invest in integrated platforms for seamless operations. Automation of administrative workflows boosts efficiency and reduces errors. Growth in big data analytics enhances population health management capabilities. Favorable regulatory frameworks encourage digital innovation. Increasing interoperability standards support software expansion. Rising investments in health-tech startups further stimulate development. Overall, software emerges as the fastest-growing component due to innovation, scalability, and expanding digital healthcare ecosystems.

- By Delivery Mode

On the basis of delivery mode, the Healthcare Information Technology (IT) market is segmented into On-Premises and Cloud-Based. The On-Premises segment dominated the largest market revenue share of 55.3% in 2025, primarily due to data security concerns and established IT infrastructure in large hospitals. Healthcare organizations prefer on-premises systems for better control over sensitive patient information. Regulatory compliance requirements support in-house data storage. Large-scale hospitals invest in customized IT environments tailored to operational needs. Integration with legacy systems further sustains demand. High-volume institutions require robust internal servers for data processing. Concerns about cyber threats encourage controlled infrastructure management. Established procurement frameworks favor traditional deployment models. Long-term contracts with IT vendors reinforce adoption. On-premises systems also ensure uninterrupted access in low-connectivity regions. Overall, on-premises deployment leads due to security, control, and infrastructure stability.

The Cloud-Based segment is projected to register the fastest CAGR of 15.1% from 2026 to 2033, driven by scalability, cost-effectiveness, and remote accessibility. Cloud platforms enable real-time data sharing across multiple healthcare facilities. Smaller clinics adopt cloud solutions to reduce upfront investment costs. Growing telehealth adoption accelerates demand for cloud integration. Advanced encryption and security enhancements increase confidence in cloud systems. Subscription-based pricing models support budget flexibility. Interoperability and seamless updates enhance operational efficiency. Rising mobile health applications depend heavily on cloud infrastructure. Disaster recovery and backup capabilities strengthen adoption. Expansion of AI-driven analytics platforms further boosts cloud utilization. Overall, cloud-based delivery is the fastest-growing mode due to flexibility, innovation, and digital transformation initiatives.

- By End-Users

On the basis of end-users, the Healthcare Information Technology (IT) market is segmented into Providers and Payers. The Providers segment accounted for the largest market revenue share of 63.7% in 2025, driven by increasing adoption of EHRs, telemedicine platforms, and clinical workflow management systems. Hospitals and clinics require integrated IT systems for efficient patient management. Growing patient volumes demand streamlined digital solutions. Regulatory mandates for digital record-keeping strengthen provider investments. Providers adopt analytics tools to improve care quality and reduce readmissions. Integration of AI-based diagnostics enhances treatment accuracy. Expansion of outpatient and specialty clinics increases IT spending. Government funding initiatives promote healthcare digitization. Continuous upgrades of hospital information systems sustain revenue generation. Overall, providers dominate due to extensive IT deployment across clinical settings.

The Payers segment is expected to witness the fastest CAGR of 11.8% from 2026 to 2033, driven by the growing need for claims management automation and fraud detection systems. Insurance companies invest in advanced analytics to optimize risk assessment. Digital platforms enhance customer engagement and policy management. Increasing regulatory compliance requirements drive IT adoption among payers. Automation of reimbursement processes improves operational efficiency. Rising healthcare expenditure necessitates cost-containment strategies supported by IT solutions. Integration of AI for predictive modeling strengthens competitiveness. Expansion of value-based reimbursement models accelerates digital transformation. Collaboration between payers and providers enhances data exchange platforms. Overall, the payers segment is growing rapidly due to digital modernization and efficiency-driven strategies.

Asia-Pacific Healthcare Information Technology (IT) Market Regional Analysis

- The Asia-Pacific healthcare information technology (IT) market is poised to grow at a significant CAGR during the forecast period of 2026 to 2033, driven by rapid healthcare digitalization, increasing government initiatives promoting e-health infrastructure, and rising investments in hospital information systems across countries such as China, Japan, and India

- The region’s strong focus on expanding digital health ecosystems, improving patient data management, and integrating AI-driven healthcare solutions is accelerating the adoption of Healthcare IT platforms

- Furthermore, the expansion of telemedicine services and cloud-based healthcare management systems is contributing substantially to regional market growth

China Healthcare Information Technology (IT) Market Insight

China healthcare information technology (IT) market dominated the Healthcare Information Technology (IT) market with the largest revenue share of 37.1% in 2025, driven by rapid digital transformation across hospitals, expanding adoption of electronic health records (EHRs), telemedicine platforms, and AI-based healthcare solutions, along with strong government initiatives promoting smart hospital infrastructure. Increasing healthcare expenditure, large patient population, and strong domestic technology providers are further strengthening China’s leadership position in the regional market.

India Healthcare Information Technology (IT) Market Insight

India healthcare information technology (IT) market is expected to be the fastest-growing region in the Healthcare Information Technology (IT) market during the forecast period, expanding at a CAGR of 13.4% from 2026 to 2033, supported by increasing healthcare digitalization, rising investments in health-tech startups, government programs promoting digital health ecosystems such as national health ID initiatives, and growing demand for cloud-based hospital management systems and telehealth services.

Asia-Pacific Healthcare Information Technology (IT) Market Share

The Healthcare Information Technology (IT) industry is primarily led by well-established companies, including:

- Epic Systems Corporation (U.S.)

- Allscripts Healthcare Solutions (U.S.)

- McKesson Corporation (U.S.)

- GE HealthCare (U.S.)

- Philips Healthcare (Netherlands)

- Siemens Healthineers (Germany)

- Oracle Health (U.S.)

- Cognizant Technology Solutions (U.S.)

- Wipro (India)

- Tata Consultancy Services (India)

- Infosys (India)

- Optum (U.S.)

- Athenahealth (U.S.)

- eClinicalWorks (U.S.)

- NextGen Healthcare (U.S.)

- IBM Watson Health (U.S.)

- Intersystems (U.S.)

- Change Healthcare (U.S.)

- HCL Technologies (India)

Latest Developments in Asia-Pacific Healthcare Information Technology (IT) Market

- In December 2021, Oracle announced its agreement to acquire Cerner Corporation, one of the largest suppliers of electronic health records (EHR) and healthcare IT solutions worldwide. This strategic acquisition (completed in July 2022) marked one of the largest healthcare IT consolidations, aimed at modernizing EHR systems and expanding cloud-based healthcare IT infrastructure globally

- In January 2025, Veradigm launched its Ambient Scribe platform, an AI-enabled ambient scribing solution designed to automatically transcribe clinical encounters and reduce the documentation burden on healthcare professionals. This launch represents a major step forward in AI-driven automation for clinician workflow in healthcare IT

- 2025年5月、Innovaccerは、クラウドに依存しないデータ統合ソリューションであるヘルスケアインテリジェンスプラットフォーム「Gravity」を発表しました。このプラットフォームは、電子カルテ、請求データ、その他のシステムからのデータを集約し、AIを活用した集団健康管理と相互運用性の取り組みを推進します。このプラットフォームの発表は、ヘルスケアITにおけるAIの導入加速とデータ統合に向けた大きな推進力となります。

- 2025年6月、Relatientは、予約管理、確認、キャンセルを自動化するために患者予約システムに統合された高度な対話型AIエージェントであるDash Voice AIを発表し、医療管理IT機能におけるAI強化の傾向を示した。

- 2025年9月の市場調査では、世界のヘルスケアIT市場の成長は遠隔医療と電子カルテ(EHR)のイノベーションによって牽引されており、2030年まで年平均成長率(CAGR)16%で推移すると予測され、遠隔医療、モバイルヘルス、臨床意思決定支援システムなどのヘルスケアITソリューションの継続的な拡大と医療提供における重要性が強調されました。

- 2025年1月、Healthcare Triangle, Inc.などの医療ITプロバイダーは、AIとEHRの統合サービスを全国規模で拡大するための主要な医療システム契約を獲得し、米国の医療システムにおける統合クラウド、マネージドサービス、および自動化ソリューションに対する商業的需要を強化した。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。