欧州インターベンショナル神経学機器市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.35 Billion

USD

2.54 Billion

2025

2033

USD

1.35 Billion

USD

2.54 Billion

2025

2033

| 2026 –2033 | |

| USD 1.35 Billion | |

| USD 2.54 Billion | |

| % | |

|

欧州インターベンショナル神経学デバイス市場のセグメンテーション:製品タイプ別(動脈瘤コイル塞栓デバイス、脳バルーン血管形成術およびステントシステム、サポートデバイス、神経血栓除去デバイス)、疾患病理別(虚血性脳卒中、脳動脈瘤、動静脈奇形および瘻孔、その他)、処置別(塞栓術、血管形成術、神経血栓除去術、その他)、エンドユーザー別(病院、神経科クリニック、外来診療センター、その他)- 業界動向と2033年までの予測

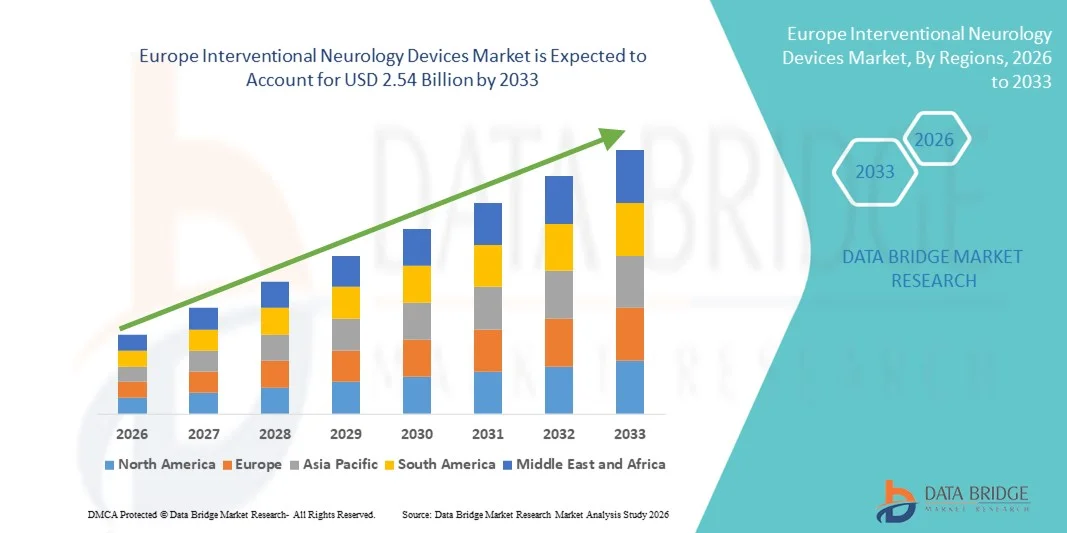

欧州におけるインターベンショナル神経学機器市場規模

- 欧州の神経内科用医療機器市場規模は、2025年には13億5,000万米ドルと評価され 、 予測期間中の年平均成長率(CAGR)8.25%で、2033年には25億4,000万米ドルに達すると予測されている。

- 市場の成長は、脳卒中、動脈瘤、頭蓋内血管疾患などの神経疾患の罹患率の上昇と、病院および専門神経センターにおける低侵襲性および画像誘導型インターベンション手技の普及拡大によって大きく促進されている。

- さらに、より安全で正確かつ迅速な回復を求める患者の嗜好の高まりと、ステント、塞栓コイル、カテーテル、血栓除去システムなどの神経血管デバイスにおける継続的な技術進歩により、インターベンショナル神経デバイスは現代の神経血管治療において不可欠なツールとしての地位を確立しつつあります。これらの要因が複合的に作用することで、インターベンショナル神経デバイスソリューションの普及が加速し、市場全体の成長を大きく促進しています。

欧州におけるインターベンショナル神経学機器市場の分析

- 神経血管ステント、塞栓コイル、血栓除去装置、マイクロカテーテルなどの神経血管インターベンション機器は、脳卒中、動脈瘤、その他の脳血管疾患を低侵襲で正確かつ効果的に治療できるため、病院や専門神経センターにおける現代の神経医療においてますます重要な構成要素となっている。

- 神経血管インターベンション機器の需要増加は、主に脳血管疾患の罹患率の上昇、画像誘導下および低侵襲手術の普及拡大、患者の意識向上、そして安全性、手術成功率、回復時間を改善する神経血管機器の継続的な技術進歩によって促進されている。

- 英国は、高度な医療インフラ、低侵襲神経血管手術の高い普及率、強力な償還政策、そして機器利用を促進する主要病院や神経血管インターベンションセンターの存在を特徴として、2025年には欧州の神経血管インターベンション機器市場で最大の収益シェア28.5%を獲得し、市場を牽引した。

- ドイツは、脳卒中や動脈瘤の発生率の上昇、神経血管内治療技術への投資の増加、革新的な血栓除去システムやコイルシステムの採用、低侵襲治療に重点を置いた医療費の拡大などを背景に、予測期間中、欧州の神経血管内治療機器市場において最も急速に成長する国になると予想されている。

- 虚血性脳卒中セグメントは、高齢者における脳卒中の高い罹患率と高度な画像診断による検出率の向上により、2025年には52.1%と最大の収益シェアを占めた。

レポートの範囲と介入神経学機器市場のセグメンテーション

|

属性 |

神経内科介入機器の主要市場動向 |

|

対象分野 |

|

|

対象国 |

ヨーロッパ

|

|

主要市場プレーヤー |

|

|

市場機会 |

|

|

付加価値データ情報セット |

Data Bridge Market Researchが作成する市場レポートには、市場価値、成長率、セグメンテーション、地理的範囲、主要企業といった市場シナリオに関する洞察に加え、専門家による詳細な分析、患者疫学、パイプライン分析、価格分析、規制枠組みなども含まれています。 |

欧州におけるインターベンショナル神経学機器市場の動向

低侵襲手術および画像誘導手術の普及拡大

- 欧州の神経内科医療機器市場における主要かつ加速的なトレンドは、低侵襲性の画像誘導型神経血管インターベンションの普及である。

- 血管内血栓除去術、動脈瘤コイル塞栓術、神経ステント留置術などのこれらの処置は、従来の開腹手術と比較して、外科的侵襲の軽減、入院期間の短縮、患者転帰の改善をもたらします。病院が効率性と患者満足度の最適化を目指す中で、これらの先進的な技術はますます好まれるようになっています。

- For instance, Germany’s leading neurovascular centers are implementing high-precision image-guided navigation systems that allow physicians to accurately position microcatheters during aneurysm repair, reducing the risk of complications. Early clinical data indicates that patients treated with these advanced interventional techniques experience faster recovery and fewer post-procedure neurological deficits, boosting confidence in these devices

- In addition, integration of hybrid operating rooms equipped with real-time fluoroscopy, 3D angiography, and navigation imaging systems is creating new opportunities for the adoption of sophisticated interventional devices. Hospitals in France and the Netherlands are increasingly investing in these hybrid setups to perform complex neurointerventions more safely and efficiently

- The trend is also supported by increasing demand for outpatient-based neurointerventions, where minimally invasive approaches allow faster turnover and reduce costs for healthcare systems

Europe Interventional Neurology Devices Market Dynamics

Driver

Growing Prevalence of Neurological Disorders and Stroke Incidence

- The primary driver of the market is the rising prevalence of neurological disorders, especially ischemic and hemorrhagic strokes, aneurysms, and arteriovenous malformations. With the aging population in Europe, the burden of cerebrovascular diseases continues to increase, necessitating advanced interventional solutions

- For instance, a 2024 European Stroke Organisation report highlighted over 1.2 million stroke cases in Germany and the U.K., with increasing survival rates leading to higher demand for follow-up interventional procedures to prevent recurrence

- Healthcare initiatives aimed at early detection and management of stroke and neurovascular disorders are also promoting market growth. Public awareness campaigns and widespread adoption of neuroimaging screening programs have resulted in higher referral rates for interventional procedures

- Favorable reimbursement frameworks in key countries, including the U.K. and Germany, are facilitating hospital adoption of high-cost interventional devices such as flow-diverter stents, embolization coils, and thrombectomy systems. These policies reduce financial barriers and encourage hospitals to invest in cutting-edge technologies

- Technological advancements in devices are another significant driver. Improvements in catheter design, microcatheter flexibility, low-profile delivery systems, and enhanced visibility under imaging are increasing procedural success rates and safety, thereby accelerating market adoption

- The integration of AI-assisted imaging and robotic-assisted navigation platforms is further enhancing the precision and efficiency of neurointerventions, creating a positive cycle of device adoption and clinical validation

Restraint/Challenge

High Device Costs, Regulatory Hurdles, and Skilled Workforce Shortages

- Despite the market potential, several challenges hinder rapid growth. The high cost of advanced interventional neurology devices, such as MRI-compatible stents, neurovascular flow-diverters, and AI-enabled navigation systems, limits adoption in smaller hospitals or budget-constrained regions

- Stringent European regulatory requirements, including CE marking and compliance with the Medical Device Regulation (MDR), can delay product approvals and increase development and clinical trial costs

- For instance, in 2023, a leading manufacturer of flow-diverter stents experienced a 12-month delay in CE approval due to In addition clinical evidence requirements, postponing market entry in several EU countries. These factors sometimes restrict the timely introduction of innovative devices to the market

- Another key restraint is the shortage of trained neurointerventional specialists. While urban centers have access to skilled neurosurgeons and interventional radiologists, rural and semi-urban regions often lack adequately trained personnel, limiting the reach of advanced devices

- Reliance on continuous training programs for physicians and technicians adds operational costs for hospitals, which can slow the adoption of new technologies

- In addition challenges include procedural risks associated with complex neurointerventions, concerns regarding long-term device durability, and the need for robust post-market clinical evidence to reassure healthcare providers

- Overcoming these challenges requires strategic initiatives such as collaborative physician training programs, cost-effective device development, partnerships with academic and research institutions, and streamlined regulatory pathways for faster approvals. This will be vital for sustained and inclusive growth of the market across Europe

Europe Interventional Neurology Devices Market Scope

The market is segmented on the basis of product type, disease pathology, procedure, and end user.

- By Product Type

On the basis of product type, the Interventional Neurology Devices market is segmented into Aneurysm Coiling and Embolization Devices, Cerebral Balloon Angioplasty and Stenting Systems, Support Devices, and Neurothrombectomy Devices. The Aneurysm Coiling and Embolization Devices segment dominated the largest market revenue share of 47.5% in 2025, driven by its widespread use in treating cerebral aneurysms and preventing ruptures. Hospitals and neurology clinics rely on these devices due to their minimally invasive nature, precision, and ability to reduce patient recovery time. Technological innovations such as detachable coils and improved embolic materials have enhanced procedural safety and outcomes. The growing prevalence of cerebral aneurysms in aging populations, coupled with rising awareness of endovascular procedures, further supports adoption. Government initiatives promoting advanced neurocare devices, reimbursement schemes, and increasing infrastructure of neurointerventional suites also drive demand. Device availability across Europe and North America contributes to market leadership.

The Neurothrombectomy Devices segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, fueled by increasing incidence of ischemic strokes worldwide and growing adoption of rapid clot retrieval procedures. Hospitals and stroke centers increasingly prefer neurothrombectomy devices for their efficacy in restoring blood flow and improving functional outcomes. Rising awareness of stroke treatment guidelines, higher investment in stroke-ready facilities, and adoption of advanced imaging support the growth trajectory. Market expansion is also aided by improvements in device design, including smaller catheters, improved navigation systems, and safety features, making them more suitable for complex neurovascular cases.

- By Disease Pathology

On the basis of disease pathology, the market is segmented into Ischemic Strokes, Cerebral Aneurysms, Arteriovenous Malformations and Fistulas, and Others. The Ischemic Strokes segment held the largest revenue share of 52.1% in 2025, attributed to the high prevalence of stroke among the elderly and increased detection through advanced imaging. Hospitals and specialized stroke centers rely heavily on devices for mechanical thrombectomy and catheter-based reperfusion. Early intervention and minimally invasive procedures reduce disability and hospital stay durations, reinforcing adoption. Rising patient awareness, availability of skilled neurologists, and government health initiatives further enhance growth. Technological integration with imaging and digital monitoring optimizes treatment planning and post-procedural follow-up.

The Arteriovenous Malformations and Fistulas segment is projected to witness the fastest CAGR of 12.5% from 2026 to 2033, driven by increasing awareness and early diagnosis. Minimally invasive embolization techniques for AVMs and fistulas are preferred due to reduced risk and faster recovery compared with open surgery. Investments in neurointerventional infrastructure and specialized clinics, along with innovation in microcatheters and embolic agents, support rapid adoption. Rising incidence of vascular malformations in both pediatric and adult populations also propels market growth.

- By Procedure

On the basis of procedure, the market is segmented into Embolization, Angioplasty, Neurothrombectomy, and Others. The Embolization segment dominated the largest revenue share of 49.8% in 2025, as it is the preferred method for treating cerebral aneurysms, AVMs, and fistulas. Hospitals and neurology clinics prioritize embolization due to its minimally invasive approach, improved patient safety, and reduced recovery time. Growing awareness of cerebrovascular disease treatments, supportive reimbursement frameworks, and availability of advanced embolization devices drive dominance. Adoption of advanced imaging modalities such as 3D angiography and AI-assisted planning enhances procedural accuracy. Regulatory approvals for innovative coils and embolic materials across Europe further reinforce market share.

The Neurothrombectomy segment is expected to witness the fastest CAGR of 13.6% from 2026 to 2033, fueled by increasing ischemic stroke cases and wider clinical adoption of mechanical clot retrieval devices. Hospitals are adopting neurothrombectomy devices due to their proven efficacy in restoring cerebral blood flow and improving survival and functional outcomes. Rising investment in stroke-ready facilities, updated treatment guidelines, and technological improvements such as smaller, navigable catheters accelerate growth. Early intervention campaigns and public awareness programs also contribute to segment expansion, particularly in developed countries with established stroke care networks.

- By End User

On the basis of end user, the market is segmented into Hospitals, Neurology Clinics, Ambulatory Care Centres, and Others. The Hospitals segment held the largest revenue share of 56.3% in 2025, driven by high patient volumes, advanced infrastructure, and availability of interventional suites. Hospitals prefer comprehensive device portfolios covering aneurysm, stroke, and AVM treatments. Government initiatives, reimbursements, and skilled neurologists further reinforce adoption. Large hospitals also benefit from economies of scale and multi-modality imaging integration, supporting continued dominance.

The Ambulatory Care Centres segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, driven by the rising preference for outpatient neurointerventional procedures. Minimally invasive treatments and shorter recovery times are ideal for ambulatory settings. Technological innovations enabling safe and efficient outpatient procedures, along with increased availability of portable imaging and treatment devices, support growth. Adoption by private neurology practices and specialty care centers further accelerates market expansion. Expansion into urban and semi-urban regions with high patient demand also contributes to rapid growth.

Europe Interventional Neurology Devices Market Regional Analysis

- The Europe interventional neurology devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of neurovascular disorders, such as stroke, cerebral aneurysms, and arteriovenous malformations, alongside growing demand for minimally invasive treatment options

- Advancements in device technology, including thrombectomy devices, coil systems, flow diverters, and AI-assisted navigation platforms, are enhancing procedural accuracy and patient outcomes, further fueling market growth. The increasing investments in digital neuro-interventional platforms, coupled with the rising awareness among healthcare providers regarding early intervention and preventive care, are also supporting market expansion

- Moreover, government initiatives promoting stroke care, aging populations, and increasing hospital infrastructure across Europe are contributing to the widespread adoption of these devices in both public and private healthcare settings

U.K. Interventional Neurology Devices Market Insight

The U.K. interventional neurology devices market is anticipated to grow at a noteworthy CAGR during the forecast period, largely driven by advanced healthcare infrastructure, high adoption of minimally invasive neurovascular procedures, and strong reimbursement frameworks. The presence of leading hospitals and specialized neuro-interventional centers ensures consistent utilization of innovative devices, including thrombectomy systems, neurovascular coils, and flow diverters. In addition, growing awareness about early intervention in stroke and aneurysm management, coupled with robust training programs for neuro-interventionalists, supports higher procedural volumes. The U.K.’s proactive healthcare policies, coupled with increasing adoption of AI-assisted imaging and navigation systems, are further expected to accelerate market growth.

Germany Interventional Neurology Devices Market Insight

The Germany interventional neurology devices market is expected to be the fastest growing in Europe during the forecast period, driven by rising incidence of stroke and aneurysms, increasing healthcare expenditure, and substantial investments in advanced neuro-interventional technologies. Hospitals and specialized centers are increasingly adopting innovative devices, including coil embolization systems, stent-assisted thrombectomy devices, and AI-guided navigation platforms, improving procedural efficiency and patient safety. Germany’s focus on minimally invasive treatment approaches, coupled with an aging population and expanding healthcare infrastructure, is fostering widespread adoption of these devices across both urban and semi-urban regions. Moreover, supportive reimbursement policies, ongoing clinical trials, and investments in training programs for neuro-interventional specialists are expected to sustain long-term growth in the country.

Europe Interventional Neurology Devices Market Share

The Interventional Neurology Devices industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- Penumbra, Inc. (U.S.)

- Terumo Corporation (Japan)

- MicroVention, Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Cerenovus (U.S.)

- Balt Extrusion (France)

- Phenox GmbH (Germany)

- Kaneka Corporation (Japan)

- Asahi Intecc Co., Ltd. (Japan)

- NeuroIntervention AG (Switzerland)

- Pulse Medical Devices Ltd. (U.K.)

Latest Developments in Europe Interventional Neurology Devices Market

- In June 2025, InspireMD announced that its CGuard Prime Embolic Prevention System (EPS) received CE Mark approval under the European Medical Device Regulation (MDR) for use in stroke prevention. The CE Mark enables wider adoption of this embolic protection device across European healthcare systems, offering clinicians a new tool to reduce stroke risk during carotid interventions

- In May 2025, Terumo Interventional Systems commercially launched its FDA‑approved ROADSAVER Carotid Stent System in select European markets. Designed for use with the Nanoparasol Embolic Protection System, the ROADSAVER Stent System provides a minimally invasive solution for treating carotid artery stenosis and expanding therapeutic options for patients at high surgical risk

- In March 2025, Boston Scientific launched an updated FilterWire EZ embolic protection system in select European markets. The updated system features a 110‑micron‑pore filter tip designed to capture embolic debris while maintaining blood flow, improving embolic protection performance in neurovascular procedure

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。