グローバル航空宇宙プラスチック市場規模、シェア、トレンド分析レポート

Market Size in USD Billion

CAGR :

%

USD

0.85 Billion

USD

1.41 Billion

2024

2032

USD

0.85 Billion

USD

1.41 Billion

2024

2032

| 2025 –2032 | |

| USD 0.85 Billion | |

| USD 1.41 Billion | |

| % | |

|

Global Aerospace Plastics Market Segmentation, By Type (Polyetheretherketone (PEEK), Polycarbonate, Polymethyl Methacrylate (PMMA), Polyamide, Polyphenylene Sulfide (PPS), and Others), Application (Aerostructure, Cabin Interiors, Propulsion System, Equipment, and Others), By End Use (Commercial Aviation, Military Aviation, General Aviation) – Industry Trends and Forecast to 2032

Aerospace Plastics Market Size

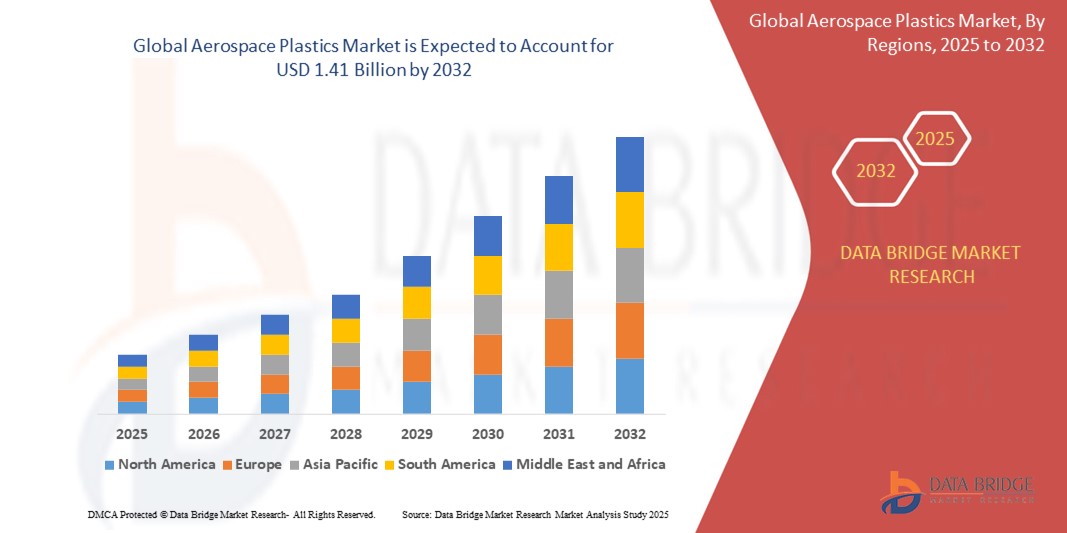

- The global aerospace plastics market size was valued at USD 0.85 billion in 2024 and is expected to reach USD 1.41 billion by 2032, growing at a CAGR of 6.50% during the forecast period.

- The growth is primarily driven by the rising demand for lightweight materials to enhance fuel efficiency, increasing aircraft production, and expanding defense budgets globally.

Aerospace Plastics Market Analysis

- Aerospace plastics are high-performance polymeric materials used in the aerospace sector for applications where strength-to-weight ratio, durability, and chemical resistance are critical. These materials are widely applied in interior components, fuselage parts, and engine components, helping reduce aircraft weight and improve fuel economy.

- The market is experiencing stable and consistent growth, supported by increasing commercial air traffic, rising preference for fuel-efficient aircraft, and growing investments in military aviation modernization programs.

- North America is expected to dominate the aerospace plastics market with a market share of 38.27%, attributed to the presence of major aircraft OEMs such as Boeing and Lockheed Martin, along with ongoing upgrades in commercial and defense aviation fleets.

- Asia-Pacific is anticipated to be the fastest growing region during the forecast period, supported by rapid expansion in air travel, increasing aircraft procurement by regional carriers, and government initiatives for indigenous aircraft manufacturing in countries like India and China.

- Among types, the polyetheretherketone (PEEK) segment is expected to lead the market with a share of 29.64%, owing to its exceptional thermal stability, chemical resistance, and mechanical strength, making it ideal for demanding applications such as engine parts and structural components in both commercial and military aircraft.

Report Scope and Aerospace Plastics Market Segmentation

|

Attributes |

Aerospace Plastics Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Aerospace Plastics Market Trends

“Growing Adoption of Lightweight, Fuel-Efficient Aircraft Components”

- A key trend in the global aerospace plastics market is the growing adoption of lightweight plastic components to enhance fuel efficiency, reduce carbon emissions, and optimize aircraft performance.

- This trend is strongly influenced by stringent environmental regulations, rising jet fuel costs, and the aerospace industry's push toward sustainable aviation and operational efficiency.

- For instance, leading aerospace manufacturers such as Boeing and Airbus are increasingly integrating high-performance thermoplastics like PEEK, PMMA, and polycarbonate into aircraft interiors, structural parts, and propulsion systems to replace traditional metal components and reduce aircraft weight.

- Lightweight aerospace plastics enable lower fuel consumption, increased payload capacity, and improved range, making them ideal for new-generation aircraft platforms.

- As the industry transitions toward hybrid and electric aircraft, the demand for advanced plastics that combine electrical insulation, thermal resistance, and structural integrity is expected to surge further.

- With ongoing innovation in flame-retardant, recyclable, and high-temperature-resistant plastics, the trend toward lightweighting is set to remain a major driver of technological advancement in aerospace manufacturing.

Aerospace Plastics Market Dynamics

Driver

“Rising Aircraft Production and Fleet Modernization”

- One of the major growth drivers in the aerospace plastics market is the rising production of commercial and military aircraft, coupled with increasing efforts to modernize existing fleets with lighter, more efficient components.

- The push for next-generation aircraft with better performance, lower emissions, and improved passenger comfort is accelerating the use of advanced plastics in both primary and secondary aircraft structures.

- Aerospace plastics offer excellent strength-to-weight ratio, corrosion resistance, and design flexibility, making them ideal substitutes for metals in critical aircraft systems.

- As airlines look to improve fuel efficiency and meet environmental targets, manufacturers are scaling up the use of plastics in areas such as aerostructures, cabin interiors, and propulsion systems.

For instance,

- Hexcel Corporation and Solvay S.A. are developing aerospace-grade thermoplastics and thermoset composites that meet stringent FAA requirements while reducing aircraft weight and enhancing fuel efficiency.

- Toray Industries is also investing in the production of carbon-fiber-reinforced plastic (CFRP) systems using polymer matrices for aerostructures.

- The combined effect of growing air travel, fleet renewal programs, and regulatory mandates for efficiency is expected to drive sustained demand for high-performance aerospace plastics through 2032.

Restraint/Challenge

“High Processing Costs and Regulatory Barriers”

- A significant restraint in the aerospace plastics market is the high processing cost and stringent regulatory approval process associated with aerospace-grade plastic materials.

- Advanced thermoplastics like PEEK, PPS, and PEI require sophisticated production techniques, precise quality control, and long certification timelines to meet aviation safety and performance standards.

- These complexities increase initial investment and time-to-market, deterring small and medium suppliers from entering the market and raising costs for aircraft OEMs.

- For instance, plastics used in aerospace applications must pass rigorous flammability, smoke, and toxicity (FST) tests and meet international regulatory certifications such as FAR 25.853, making material qualification both costly and time-consuming.

- Additionally, the limited recyclability and end-of-life management of high-performance plastics present further sustainability challenges for manufacturers and operators.

- While the benefits of aerospace plastics are significant, their higher cost compared to metals or commodity plastics, along with certification constraints, may slow adoption, especially in cost-sensitive defense and regional aviation markets.

Aerospace Plastics Market Scope

The market is segmented on the basis of type, application, and end-use.

- By Type

On the basis of type, the Aerospace Plastics Market is segmented into Polyetheretherketone (PEEK), Polycarbonate, Polymethyl Methacrylate (PMMA), Polyamide, Polyphenylene Sulfide (PPS), and Others. The Polyetheretherketone (PEEK) segment dominates the largest market revenue share of 31.5% in 2025, owing to its exceptional strength-to-weight ratio, high-temperature resistance, and flame retardancy, making it ideal for critical aerospace components including engine parts and structural assemblies.

However, the Polycarbonate segment is projected to grow at the highest CAGR of 6.82% during the forecast period of 2025–2032, driven by its extensive use in aircraft interiors and windows due to impact resistance, transparency, and lightweight properties, which align with industry efforts toward enhancing fuel efficiency and passenger comfort.

- By Application

Based on application, the Aerospace Plastics Market is segmented into Aerostructure, Cabin Interiors, Propulsion System, Equipment, and Others. The Cabin Interiors segment held the largest market share of 34.7% in 2025, primarily attributed to the rising demand for durable, lightweight, and aesthetically appealing plastics used in seats, panels, overhead bins, and other interior components. This demand is further supported by airline fleet modernization and growing air passenger traffic.

However, the Aerostructure segment is expected to record the highest CAGR of 7.23% during the forecast period. This growth is driven by the rising adoption of carbon-reinforced and high-performance plastics in fuselage, wings, and other structural components, where reduced weight contributes directly to fuel efficiency and emissions reduction.

- By End-Use

On the basis of end use, the Aerospace Plastics Market is categorized into Commercial Aviation, Military Aviation, and General Aviation. The Commercial Aviation segment accounted for the largest market share of 59.2% in 2025, due to the continued expansion of commercial airline fleets and increasing production of next-generation aircraft, which prioritize lightweight materials for cost and performance advantages.

Meanwhile, the Military Aviation segment is projected to grow at the highest CAGR of 6.95% during 2025–2032, fueled by increased defense budgets, modernization of air fleets, and demand for high-performance materials that offer enhanced durability, heat resistance, and survivability in extreme conditions.

Global Aerospace Plastics Market Regional Analysis

North America Aerospace Plastics Market Insight

North America commands a leading position in the global aerospace plastics market, backed by the presence of major aircraft manufacturers, strong defense budgets, and continuous investments in aviation modernization programs. The region's focus on fuel efficiency and emissions reduction has significantly increased the adoption of lightweight and high-performance plastics in commercial and military aviation.

- U.S. Aerospace Plastics Market Insight

米国の航空宇宙用プラスチック市場は、ボーイングやロッキード・マーティンといったOEMを含む米国の堅調な航空宇宙セクターに牽引され、2025年には北米で最大の収益シェアを占める見込みです。胴体部品、客室内装、推進システムにおける熱可塑性プラスチックや複合材料の広範な使用は、航空機の性能向上と運用コストの削減に寄与しています。難燃性および低煙性プラスチックにおける継続的なイノベーションが、成長をさらに促進しています。

- カナダ航空宇宙プラスチック市場インサイト

カナダの航空宇宙用プラスチック市場は、特にケベック州における活況を呈する航空宇宙製造拠点に支えられ、安定した成長を遂げています。リージョナルジェット機やヘリコプターにおける軽量素材の需要増加は、内装材や構造材におけるポリカーボネート、PEEK、PMMAの使用を促進しています。航空宇宙分野の研究開発と持続可能性への取り組みに対する政府の支援は、リサイクル可能で高強度のプラスチック素材の活用を促進しています。

欧州航空宇宙プラスチック市場インサイト

欧州では、航空機の排出ガス、重量最適化、持続可能性に関する厳格なEU規制の強化を受け、予測期間中、航空宇宙用プラスチック市場が力強い成長を遂げると予想されています。エアバスをはじめとする大手航空機メーカーの存在や、電気自動車およびハイブリッド航空機への投資増加により、航空機構造および客室システムにおける先進的なプラスチック材料の採用が加速しています。

- ドイツ航空宇宙プラスチック市場洞察

ドイツは、精密エンジニアリング能力と強力な航空機部品サプライチェーンを背景に、欧州の航空宇宙用プラスチック市場で大きなシェアを占めています。航空機の外装、ブラケット、エンジン部品における高性能熱可塑性プラスチックの使用は拡大しています。さらに、ドイツのカーボンニュートラルへの取り組みは、OEMやティアサプライヤーにバイオベースおよびリサイクル可能なプラスチック代替品の検討を促しています。

- フランスの航空宇宙用プラスチック市場インサイト

フランスの航空宇宙用プラスチック市場は、世界的な航空宇宙ハブであり、エアバス本社があるという背景から、目覚ましい拡大が見込まれています。低排出ガス航空機の推進と航空機生産率の向上により、航空機構造および内装における軽量ポリマーの需要が高まっています。次世代航空技術に焦点を当てた官民パートナーシップは、航空宇宙グレードのプラスチック配合におけるイノベーションを促進しています。

アジア太平洋地域の航空宇宙用プラスチック市場に関する洞察

アジア太平洋地域は、航空旅行の増加、航空機の急速な拡大、そして国内航空機製造プログラムへの多額の投資により、2025年から2032年にかけて航空宇宙用プラスチック市場において最も高いCAGRを記録すると予測されています。中国やインドなどの国々は、航空宇宙インフラの規模拡大を進めており、航空宇宙用プラスチックを含む先端材料の現地生産を促進することで、輸入依存度の低減を目指しています。

- 中国航空宇宙プラスチック市場洞察

中国は、COMAC C919をはじめとする自国製航空機開発プログラムの拡大に支えられ、アジア太平洋地域の航空宇宙用プラスチック市場をリードしています。胴体パネル、客室部品、換気システムにおけるポリマーの使用増加は、軽量化と設計柔軟性というメリットを背景に推進されています。国内航空産業の自立と持続可能な材料利用を重視する政府の姿勢も、市場のさらなる成長を後押ししています。

- インドの航空宇宙用プラスチック市場の洞察

インドの航空宇宙用プラスチック市場は、軍用航空、MRO(整備・修理・オーバーホール)サービス、そして「Make in India」イニシアチブに基づく国産航空機生産への投資増加を背景に、目覚ましい年平均成長率(CAGR)で成長すると予想されています。燃費効率と軽量化に優れた航空機への需要の高まりは、様々な用途における熱可塑性プラスチックと複合材料の活用を促進しています。さらに、世界的な航空宇宙企業との提携により、航空宇宙グレードのプラスチック加工におけるインドの能力が強化されています。

航空宇宙用プラスチックの市場シェア

航空宇宙用プラスチック業界は、主に次のような老舗企業によって牽引されています。

- エボニック インダストリーズ AG(ドイツ)

- SABIC(サウジ基礎産業公社)(サウジアラビア)

- ヘクセルコーポレーション(米国)

- ビクトレックスplc(英国)

- ソルベイSA(ベルギー)

- アルケマSA(フランス)

- ドレイクプラスチックス株式会社(米国)

- エンジンガーGmbH(ドイツ)

- ロシュリンググループ(ドイツ)

- 東レ株式会社(日本)

- 三菱ケミカルグループ株式会社(日本)

- 帝人株式会社(日本)

- ポリワン・コーポレーション(現アビエント・コーポレーション)(米国)

- セラニーズ・コーポレーション(米国)

世界の航空宇宙用プラスチック市場の最新動向

- 2025年3月、ソルベイSA(ベルギー)は、Amodel® PPAポートフォリオの拡充を発表し、難燃性と機械強度を向上させた航空宇宙グレードの新たな配合を導入しました。この開発は、航空機の内装および電気システムにおける軽量で高性能なポリマーの需要の高まりに対応し、厳格な安全基準への適合と航空機全体の軽量化を支援することを目的としています。

- 東レ株式会社(日本)は、2025年2月、航空宇宙用推進システムおよび構造部品向けに特別に設計された高耐熱性PEEK樹脂「TorayPEEK™」を発売しました。この材料は優れた耐熱性と耐薬品性を備えており、次世代航空機設計における先進的な熱可塑性プラスチックの重要なサプライヤーとしての東レの地位をさらに強化します。

- 2024年8月、ヘクセル・コーポレーション(米国)はユタ州ソルトレイクシティに新たな航空宇宙用熱可塑性樹脂研究センターを開設しました。この施設は、民間航空および軍事航空用途向けの先進的な炭素繊維強化熱可塑性複合材料の開発に注力します。この投資は、従来の金属ベース部品に代わる、より軽量で持続可能な代替品を提供するというヘクセルの戦略的取り組みの一環です。

- In May 2024, Victrex plc (UK) unveiled a collaboration with Tri-Mack Plastics to produce aerospace-qualified composite brackets using Victrex AE™ 250 UDT thermoplastic composite. These lightweight, corrosion-resistant components are designed to replace traditional metallic parts, enabling fuel efficiency and compliance with evolving aerospace design requirements.

- In April 2024, BASF SE (Germany) launched Ultrason® E2010, a new high-performance polyethersulfone (PESU) grade targeted for aerospace interior panels and ventilation systems. This product offers excellent flame resistance, dimensional stability, and low smoke density, helping aircraft manufacturers meet strict global safety standards.

- In January 2024, SABIC (Saudi Arabia) introduced a new LEXAN™ polycarbonate film solution tailored for aerospace display panels and cabin window applications. This product enhances optical clarity, durability, and ease of processing, addressing growing demand for lighter, impact-resistant materials in commercial aircraft.

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。