Global Agriculture Drone Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

3.88 Billion

USD

16.79 Billion

2025

2033

USD

3.88 Billion

USD

16.79 Billion

2025

2033

| 2026 –2033 | |

| USD 3.88 Billion | |

| USD 16.79 Billion | |

| % | |

|

Global Agriculture Drone Market Segmentation, By Type (Fixed-Wing Drones, Multi-Rotor Drones, and Hybrid Drones), Product (Software and Hardware), Battery Life ( 100 Minutes), Components (Flight Controllers, Propulsion Systems, Camera System, Batteries, and Global Positioning System), Mode of Operation (Fully-Autonomous, Semi-Autonomous, and Remotely Operated), Range (Extended Visual Line of Sight, Beyond Line of Sight, and Visual Line of Sight), Technology (GNSS, Obstacle Detection and Collision Avoidance Technology, Drone Analytics, and Others), Application (Spraying, Field Mapping, Scouting, Soil and Field Analysis, Crop Monitoring, Health Assessment, Irrigation, Crop Spraying, Aerial Planting, Precision Agriculture, Livestock Monitoring, Agricultural Photography, Precision Fish Farming, and Others) - Industry Trends and Forecast to 2033

Agriculture Drone Market Size

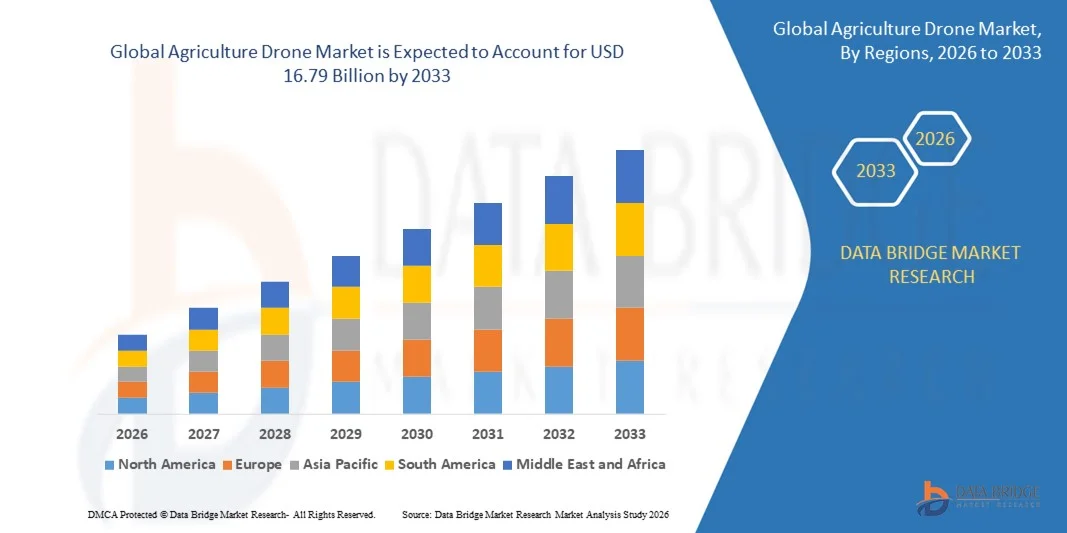

- The global agriculture drone market size was valued at USD 3.88 billion in 2025 and is expected to reach USD 16.79 billion by 2033, at a CAGR of 20.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of precision agriculture practices and the rapid integration of advanced technologies such as AI, GNSS, and data analytics into farming operations, leading to enhanced digitalization across agricultural activities

- Furthermore, rising demand for higher crop yields, efficient pesticide application, and labor cost reduction is establishing agriculture drones as essential tools for modern farm management. These converging factors are accelerating the deployment of drone-based solutions, thereby significantly boosting the overall growth of the agriculture drone market

Agriculture Drone Market Analysis

- Agriculture drones, equipped with advanced imaging sensors, spraying systems, and real-time data transmission capabilities, are becoming critical components of smart farming ecosystems across small, medium, and large-scale agricultural operations due to their ability to improve operational efficiency, monitor crop health, and optimize resource utilization

- The escalating demand for agriculture drones is primarily driven by increasing global food demand, shrinking arable land, rising labor shortages in rural areas, and the growing shift toward data-driven and automated farming practices aimed at improving productivity and sustainability

- North America dominated the agriculture drone market with a share of 34% in 2025, due to the rapid adoption of precision agriculture technologies and strong presence of advanced farming infrastructure

- Asia-Pacific is expected to be the fastest growing region in the agriculture drone market during the forecast period due to rapid urbanization, expanding agricultural activities, and increasing government initiatives supporting digital farming in countries such as China, Japan, and India

- Multi-rotor drones segment dominated the market with a market share of 62.9% in 2025, due to their superior maneuverability, vertical take-off and landing capability, and suitability for small to medium-sized farms. Farmers widely prefer multi-rotor drones for precision spraying, crop monitoring, and field scouting due to their ability to hover steadily over specific areas

Report Scope and Agriculture Drone Market Segmentation

|

Attributes |

Agriculture Drone Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Agriculture Drone Market Trends

Rising Adoption of AI-Enabled Precision Agriculture Drones

- A significant trend in the agriculture drone market is the increasing deployment of AI-enabled drones equipped with multispectral sensors and advanced analytics to enhance crop monitoring and farm decision-making. This integration is strengthening the role of drones as essential tools within precision agriculture systems aimed at maximizing yield and optimizing resource utilization

- For instance, DJI has introduced advanced agricultural drones such as the Agras series integrated with smart flight planning and real-time data analytics to improve spraying accuracy and operational efficiency. These systems enable farmers to automate large-scale spraying tasks while minimizing chemical wastage and improving coverage consistency

- The adoption of AI-powered imaging solutions is expanding as farmers increasingly rely on vegetation indices and predictive analytics to detect crop stress, pest infestations, and nutrient deficiencies at early stages. This is positioning agriculture drones as proactive farm management tools rather than only surveillance equipment

- Large agribusinesses are incorporating drone data into integrated farm management platforms where aerial insights support irrigation planning, soil analysis, and yield forecasting. This growing reliance on data-driven cultivation is reinforcing the transformation of conventional farming into technology-enabled precision agriculture

- Governments across key agricultural economies are promoting digital farming initiatives that encourage drone adoption to address labor shortages and improve productivity. This policy support is contributing to stronger market penetration and structured deployment across commercial farms

- The market is witnessing accelerated innovation in autonomous navigation, obstacle avoidance, and cloud-based analytics that enhance operational reliability and scalability. This rising integration of AI and automation is reinforcing the broader transition toward smart, efficient, and sustainable agricultural ecosystems

Agriculture Drone Market Dynamics

Driver

Increasing Demand for Enhanced Crop Yield and Operational Efficiency

- The increasing global demand for higher agricultural productivity is driving the adoption of drones capable of precise spraying, crop monitoring, and real-time field mapping. These technologies enable farmers to optimize fertilizer and pesticide application while reducing manual labor and operational inefficiencies

- For instance, Yamaha Motor Co., Ltd. has deployed its RMAX unmanned helicopter systems for agricultural spraying across Japan and other countries to enhance large-scale crop management efficiency. These UAV platforms support uniform application and reduce time-intensive manual processes on extensive farmland

- Farmers are increasingly utilizing drones to monitor crop health through high-resolution aerial imagery, enabling early identification of stress factors and reducing potential yield losses. This proactive capability directly contributes to improved harvest outcomes and better resource allocation

- The rising pressure to feed a growing global population while managing limited arable land is encouraging investments in precision agriculture technologies. Drones provide scalable solutions that help maximize productivity without significantly expanding land usage

- The continuous emphasis on productivity enhancement and operational optimization is reinforcing this driver across both developed and emerging agricultural markets. The need for efficient, data-backed, and automated farming practices continues to accelerate agriculture drone market expansion

Restraint/Challenge

High Initial Investment and Regulatory Compliance Barriers

- The agriculture drone market faces challenges related to the high upfront cost associated with advanced drone systems, sensors, and data analytics platforms. Small and medium-scale farmers often encounter financial constraints that limit large-scale adoption despite operational benefits

- For instance, the Federal Aviation Administration imposes strict operational and certification requirements for agricultural drone usage in the U.S., which increases compliance complexity for commercial farm operators. These regulatory procedures can extend deployment timelines and add administrative burdens to drone implementation strategies

- The requirement for licensed pilots, operational training, and adherence to airspace restrictions further increases operational costs and limits accessibility in certain regions. Compliance with evolving aviation regulations remains a critical barrier for new market entrants

- Advanced agriculture drones equipped with AI analytics and multispectral sensors involve higher procurement and maintenance expenses, impacting affordability in price-sensitive markets. This cost factor restricts widespread penetration among smallholder farmers in developing economies

- Inconsistent regulatory frameworks across countries create uncertainty for manufacturers and service providers seeking global expansion. These regulatory and financial challenges collectively restrain faster market adoption despite strong technological advancements and productivity advantages

Agriculture Drone Market Scope

The market is segmented on the basis of type, product, battery life, components, mode of operation, range, technology, and application.

- By Type

On the basis of type, the agriculture drone market is segmented into fixed-wing drones, multi-rotor drones, and hybrid drones. The multi-rotor drones segment dominated the market with the largest revenue share of 62.9% in 2025, driven by their superior maneuverability, vertical take-off and landing capability, and suitability for small to medium-sized farms. Farmers widely prefer multi-rotor drones for precision spraying, crop monitoring, and field scouting due to their ability to hover steadily over specific areas. Their lower operational complexity and comparatively affordable pricing further strengthen adoption among individual farmers and agribusinesses. The segment continues to benefit from ongoing improvements in payload capacity and sensor integration enhancing operational efficiency.

The hybrid drones segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the growing need for longer flight endurance combined with vertical take-off capability. Hybrid models integrate the advantages of fixed-wing endurance and multi-rotor flexibility, making them suitable for large-scale farms requiring extensive field coverage. Increasing investments in advanced agricultural technologies and demand for high-efficiency aerial mapping solutions are accelerating adoption. Their ability to cover vast acreage with reduced energy consumption makes them increasingly attractive for commercial farming operations.

- By Product

On the basis of product, the agriculture drone market is segmented into software and hardware. The hardware segment dominated the market with the largest revenue share in 2025, driven by strong demand for drone platforms, sensors, cameras, propulsion systems, and batteries. Rising adoption of high-resolution imaging systems and advanced spraying mechanisms significantly contributes to hardware sales. Farmers and service providers invest heavily in durable drone structures and precision components to enhance field productivity. Continuous technological advancements in lightweight materials and improved battery systems further support hardware dominance.

The software segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by increasing reliance on data analytics, AI-based crop monitoring, and cloud-based farm management platforms. Advanced software solutions enable real-time field mapping, crop health assessment, and yield prediction improving decision-making accuracy. Integration of drone analytics with farm management systems enhances operational transparency and resource optimization. Growing awareness of precision agriculture practices is accelerating demand for subscription-based and data-driven software platforms.

- By Battery Life

On the basis of battery life, the agriculture drone market is segmented into < 30 minutes, 30–60 minutes, 60–100 minutes, and > 100 minutes. The 30–60 minutes segment dominated the market with the largest revenue share in 2025, driven by its balanced combination of operational endurance and cost efficiency. Most commercial agriculture drones are designed within this flight duration range to support spraying and mapping tasks efficiently. The segment meets the requirements of medium-sized farms while maintaining manageable battery weight and charging time. Manufacturers continue to optimize lithium-based battery systems to enhance reliability within this range.

The > 100 minutes segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for large-scale field surveillance and extended mapping operations. Long-endurance drones reduce the need for frequent battery replacements, improving productivity in expansive agricultural lands. Technological progress in high-density battery chemistries and hybrid power solutions supports this segment’s expansion. Commercial agribusinesses are increasingly investing in extended-flight drones to maximize operational efficiency.

- By Components

On the basis of components, the agriculture drone market is segmented into flight controllers, propulsion systems, camera system, batteries, and global positioning system. The camera system segment dominated the market with the largest revenue share in 2025, driven by increasing demand for multispectral and thermal imaging to assess crop health and soil conditions. High-resolution imaging systems enable farmers to detect pest infestations, nutrient deficiencies, and irrigation issues at early stages. Continuous innovation in sensor accuracy and imaging capabilities significantly boosts adoption. The rising importance of data-driven farming practices further strengthens the dominance of camera systems.

The flight controllers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in autonomous navigation and precision flight stabilization technologies. Modern flight controllers integrate AI algorithms and real-time data processing to improve route planning and obstacle avoidance. Growing emphasis on automation in agriculture increases demand for intelligent control systems. Enhanced compatibility with GNSS and analytics platforms further accelerates segment expansion.

- By Mode of Operation

On the basis of mode of operation, the agriculture drone market is segmented into fully-autonomous, semi-autonomous, and remotely operated. The fully-autonomous segment dominated the market with the largest revenue share in 2025, driven by increasing adoption of automated flight planning and minimal human intervention systems. Farmers prefer fully-autonomous drones for consistent spraying patterns and efficient field mapping reducing labor dependency. Integration with AI-powered analytics enhances operational precision and productivity. Expanding digital transformation across agriculture further supports segment leadership.

The semi-autonomous segment is projected to witness the fastest growth rate from 2026 to 2033, fueled by the need for flexible control combined with automation. Semi-autonomous drones allow operators to intervene when necessary while benefiting from automated navigation systems. This operational balance makes them suitable for farms transitioning toward advanced automation. Increasing training programs and user-friendly interfaces are accelerating adoption across developing agricultural economies.

- By Range

On the basis of range, the agriculture drone market is segmented into extended visual line of sight, beyond line of sight, and visual line of sight. The visual line of sight segment dominated the market with the largest revenue share in 2025, driven by regulatory compliance requirements in several countries and ease of operational approval. Most small and medium-scale farmers operate drones within visible range to ensure safety and control. Lower technical complexity and reduced regulatory barriers further strengthen adoption. The segment remains widely preferred for localized crop monitoring and spraying activities.

The beyond line of sight segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by regulatory advancements and increasing demand for large-area coverage. BVLOS operations enable efficient monitoring of expansive agricultural fields reducing operational time. Technological improvements in communication systems and collision avoidance enhance safety and reliability. Growing commercial farming activities are driving investment in long-range drone capabilities.

- By Technology

On the basis of technology, the agriculture drone market is segmented into GNSS, obstacle detection and collision avoidance technology, drone analytics, and others. The GNSS segment dominated the market with the largest revenue share in 2025, driven by its critical role in ensuring accurate positioning and navigation during spraying and mapping operations. Precision agriculture heavily depends on satellite-based guidance systems to optimize input application. Reliable GNSS integration enhances flight stability and field coverage accuracy. Increasing deployment of high-precision GPS modules strengthens segment dominance.

ドローン分析分野は、航空データから得られる実用的な農業情報への需要の高まりを背景に、2026年から2033年にかけて最も急速な成長を遂げると予測されています。高度な分析プラットフォームは、ドローンから得られた生画像を作物の健康状態指標や収量予測に変換し、戦略的な農場経営を支援します。AIや機械学習技術との統合により、予測能力が向上します。データ中心の農業モデルの普及拡大が、この分野の成長を加速させています。

- 申請により

用途に基づいて、農業用ドローン市場は、散布、圃場マッピング、偵察、土壌および圃場分析、作物モニタリング、健康状態評価、灌漑、作物散布、空中播種、精密農業、家畜モニタリング、農業写真撮影、精密養殖、その他に分類されます。2025年には、効率的な農薬および肥料散布と無駄の最小化に対するニーズの高まりにより、作物散布セグメントが最大の収益シェアを獲得し、市場を牽引しました。ドローンは均一な化学物質散布を可能にし、労働コストと環境への影響を削減します。精密投入管理への注目の高まりは、このセグメントでの採用を大幅に促進します。ペイロードシステムの継続的な改善は、運用効率をさらに向上させます。

精密農業分野は、持続可能な農業と資源最適化に対する世界的な関心の高まりを背景に、2026年から2033年にかけて最も急速な成長を遂げると予測されています。精密農業は、ドローンを用いた分析、GNSSマッピング、自動意思決定を統合することで、収量を最大化し、投入コストを最小限に抑えます。スマート農業技術に対する政府の支援の拡大は、市場拡大を後押ししています。データ駆動型作物管理に対する農家の意識の高まりは、先進国と新興国の両方で、その導入を加速させています。

農業用ドローン市場の地域別分析

- 北米は、精密農業技術の急速な普及と高度な農業インフラの充実により、2025年には34%という最大の収益シェアを獲得し、農業用ドローン市場を牽引した。

- この地域の農家は、収穫効率の向上と運用コストの削減のために、ドローンを用いた作物モニタリング、圃場マッピング、散布ソリューションを高く評価している。

- この普及は、有利な規制枠組み、スマート農業に関する高い意識、そして農業技術革新への強力な投資によってさらに後押しされ、農業用ドローンは現代の農場管理における重要な要素としての地位を確立している。

米国農業用ドローン市場の洞察

2025年には、精密農業ツールの早期導入と大規模農地における農場統合の進展を背景に、米国の農業用ドローン市場が北米で最大の収益シェアを獲得しました。農家は生産性の向上と投入資材の最適化を図るため、データ駆動型の作物管理と自動散布システムをますます重視するようになっています。スマート農業イニシアチブに対する政府の強力な支援に加え、DJIやAeroVironmentといった大手ドローンメーカーが市場に参入していることも、業界の拡大をさらに加速させています。

欧州農業用ドローン市場概況

欧州の農業用ドローン市場は、持続可能な農業への重視の高まりと、農薬使用に関する厳格な環境規制を主な要因として、予測期間を通じて大幅な年平均成長率(CAGR)で拡大すると予測されています。作物の収量を向上させつつ環境への影響を最小限に抑えるための精密農業ツールの需要の高まりが、ドローンの導入を促進しています。この地域では、デジタル農業への変革と高度な農場監視技術への投資が各国で着実に進んでいます。

英国農業用ドローン市場の現状分析

英国の農業用ドローン市場は、農業業務のデジタル化の進展と効率的な作物監視システムへの需要の高まりを背景に、予測期間中に著しい年平均成長率(CAGR)で成長すると予想されています。農家は、土壌評価や作物の健康状態のモニタリングを改善するために、ドローンを用いた分析手法を採用しています。農業支援政策や自律型農業機器への関心の高まりも、英国市場の成長を今後も促進していくと見込まれます。

ドイツ農業用ドローン市場に関する洞察

ドイツの農業用ドローン市場は、技術革新と持続可能な農業慣行への強い注力に支えられ、予測期間中に著しい年平均成長率(CAGR)で拡大すると見込まれています。ドイツの高度な製造能力と精密工学への注力は、作物監視や畜産管理におけるドローンの活用を促進しています。スマート農業ソリューションとデジタルインフラへの投資増加も、市場の発展をさらに後押ししています。

アジア太平洋地域の農業用ドローン市場に関する洞察

アジア太平洋地域の農業用ドローン市場は、急速な都市化、農業活動の拡大、そして中国、日本、インドなどの国々におけるデジタル農業を支援する政府の取り組みの増加を背景に、2026年から2033年の予測期間において最も高い年平均成長率(CAGR)で成長すると見込まれています。食料需要の増加と労働力不足により、農家は効率的な農場管理のために自動化された空中ソリューションの導入を促されています。さらに、同地域がドローン部品の製造拠点としての役割を拡大していることも、新興国におけるドローンの価格と入手性の向上に貢献しています。

日本の農業用ドローン市場に関する洞察

農村部における労働力不足と、高度なロボット技術および自動化技術の普及拡大により、日本の農業用ドローン市場は勢いを増している。日本の農家は、生産性向上と人手作業の削減を目指し、農薬散布や精密モニタリングにドローンを積極的に活用している。ドローンシステムとスマート農業プラットフォーム、IoTベースの農業管理ツールとの統合も、市場成長に大きく貢献している。

中国農業用ドローン市場の洞察

中国の農業用ドローン市場は、農業慣行の急速な近代化と強力な国内製造能力を背景に、2025年にはアジア太平洋地域で最大の市場収益シェアを占める見込みです。中国では、効率性の向上と農薬の無駄の削減を目的として、大規模農場で農薬散布用ドローンが広く導入されています。DJIなどの大手ドローンメーカーの存在と、農業機械化を促進する政府の支援政策が、中国市場の拡大を後押しする重要な要因となっています。

農業用ドローンの市場シェア

農業用ドローン業界は主に、以下のような実績のある企業によって牽引されています。

- エアロバイロメント社(米国)

- AGCOコーポレーション(米国)

- AgEagle Aerial Systems Inc. (米国)

- デレール(フランス)

- DroneDeploy(米国)

- Trimble Inc.(米国)

- Parrot Drone SAS(フランス)

- ヤマハ発動機株式会社(日本)

- オプティム株式会社(日本)

- センテラ(米国)

- Insitu Pacific Pty Ltd(オーストラリア)

- ALTI UAS (PTY) LTD(南アフリカ)

- senseFly(スイス)

- AgEagle Sensor Systems Inc. (米国)

- Pix4D SA(スイス)

- DJI(中国)

世界の農業用ドローン市場における最新動向

- 2025年12月、Jyoti Global Plastは、インド全土の農家向けに、精度、運用安全性、散布効率を向上させる農業用ドローン「AeroCrop UAS」を発表しました。この発表は、同社がプラスチックおよびFRP成形から無人航空システム分野へと戦略的に事業を拡大し、国内製造能力を強化することを示しています。この開発は、労働力不足の解消、化学薬品の無駄の削減、作物生産性の向上により、インドにおける精密農業技術の普及を加速させ、ひいては農業用ドローン市場全体の成長に貢献することが期待されています。

- 2025年12月、米国コネチカット州は、播種、散布、作物調査活動における農業用ドローンの利用拡大を認める公共法25-152号を制定した。この改正された規制枠組みは、連邦航空局(FAA)の基準に沿ってコンプライアンス要件を簡素化し、農場がUAV技術をより効率的に導入できるようにする。この立法措置は、州全体での商用ドローンの導入を促進し、地域農業ドローン市場における投資とイノベーションを奨励することが期待される。

- In August 2025, Terra Drone Corporation entered into a sales partnership with PT. Yanmar Diesel Indonesia, a subsidiary of Yanmar Co., Ltd., to distribute its G20 and E16 agricultural drones to rice and field crop farmers in Indonesia. This collaboration strengthens Terra Drone’s footprint in Southeast Asia by leveraging Yanmar’s established agricultural distribution network. The partnership is expected to expand drone accessibility among local farmers, driving regional adoption and reinforcing market penetration in emerging agricultural economies

- In April 2024, DJI announced the global launch of the Agras T50 and T25 agricultural drones, targeting both large-scale and small-field farming operations. The T50 offers high-efficiency performance for extensive farmland coverage, while the T25 emphasizes portability and operational flexibility. Integration with the SmartFarm application enhances aerial spraying management and data-driven decision-making, strengthening DJI’s competitive position and advancing technological standards within the global agriculture drone market

- In July 2023, Pix4D SA launched PIX4Dfields 2.4 featuring an upgraded workflow designed to streamline precision agriculture applications. The introduction of Targeted Operations enables users to generate customized prescription maps more efficiently, improving resource optimization and crop management accuracy. This innovation enhances software-driven value within drone ecosystems, supporting broader adoption of data-centric farming solutions and reinforcing growth in the agriculture drone analytics segment

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。