Global Battlefield Management Systems Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

3.18 Billion

USD

4.57 Billion

2025

2033

USD

3.18 Billion

USD

4.57 Billion

2025

2033

| 2026 –2033 | |

| USD 3.18 Billion | |

| USD 4.57 Billion | |

| % | |

|

Global Battlefield Management Systems Market Segmentation, By Component (Communication Devices, Imaging Devices, Display Devices, Tracking Devices, Computer Hardware Devices, Data Distribution Unit, Night Vision Devices, Software, and Others), Solution (Hardware and Software), Platform (Armored Vehicle, Headquarter and Command Centers, and Soldier Systems), Installation Type (New Installation and Upgradation), System (Computing, Communication & Networking, Command & Control, Navigation, Imaging, and Mapping), End User (Army and Air Force)- Industry Trends and Forecast to 2033

Battlefield Management Systems Market Size

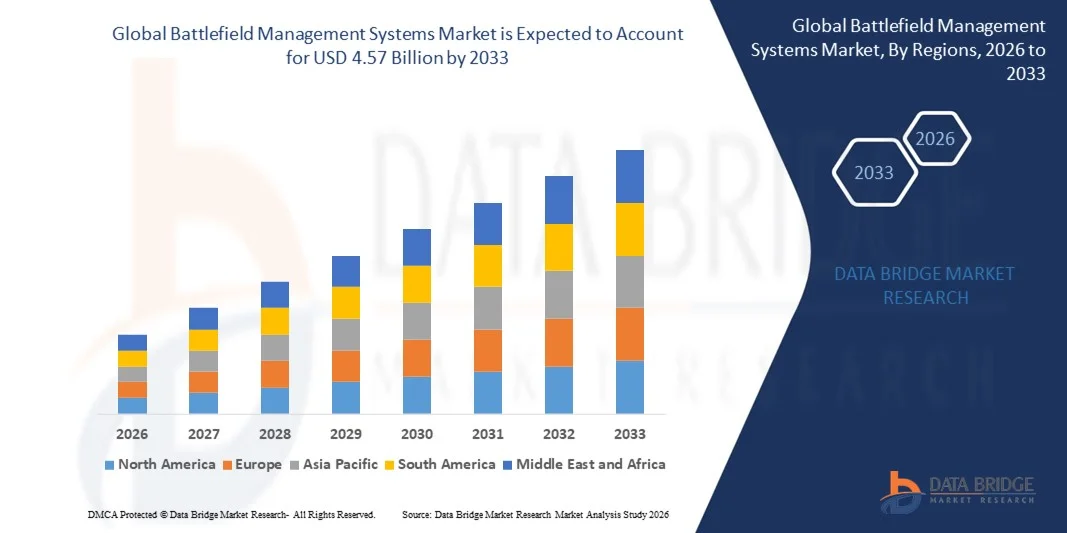

- The global battlefield management systems market size was valued at USD 3.18 billion in 2025 and is expected to reach USD 4.57 billion by 2033, at a CAGR of 4.62% during the forecast period

- The market growth is largely fuelled by the increasing demand for real-time situational awareness and enhanced communication across modern military operations

- Rising defense modernization programs and growing investments in advanced command and control technologies are further supporting market expansion

Battlefield Management Systems Market Analysis

- The market is witnessing steady growth due to the rising need for coordinated operations, improved decision-making, and efficient resource management across land, air, and naval forces

- Technological advancements such as artificial intelligence, cloud-based military networks, and integrated sensor systems are improving the operational efficiency and reliability of battlefield management solutions

- North America dominated the battlefield management systems market with the largest revenue share of 39.56% in 2025, driven by substantial defense budgets, ongoing military modernization programs, and strong emphasis on network-centric warfare capabilities

- Asia-Pacific region is expected to witness the highest growth rate in the global battlefield management systems market, driven by rising geopolitical tensions, expanding defense budgets, and rapid adoption of advanced surveillance and communication systems. Countries such as China, India, Japan, and South Korea are heavily investing in next-generation battlefield management capabilities to enhance operational efficiency and situational awareness

- The Communication Devices segment held the largest market revenue share in 2025 driven by the critical need for secure, real-time voice and data exchange across military units operating in dynamic environments. These devices ensure encrypted communication between command centers, vehicles, and soldiers, enabling coordinated mission execution. Increasing investments in advanced radio systems, satellite communication modules, and tactical data links further support segment dominance. In addition, interoperability requirements across multi-domain operations are reinforcing the demand for reliable communication infrastructure

Report Scope and Battlefield Management Systems Market Segmentation

|

Attributes |

Battlefield Management Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Battlefield Management Systems Market Trends

Rising Integration Of AI And Network-Centric Warfare Technologies

- The growing focus on real-time situational awareness and digital battlefield connectivity is significantly shaping the global battlefield management systems market, as defense forces increasingly prioritize secure communication, data integration, and coordinated mission execution. Battlefield management systems are gaining traction due to their ability to provide commanders with comprehensive operational visibility without compromising speed or accuracy of decision-making. This trend strengthens adoption across land, air, and naval forces, encouraging defense contractors to innovate with advanced, interoperable solutions that address evolving combat requirements

- Increasing investments in military modernization and digital transformation programs have accelerated the demand for integrated battlefield management platforms. Defense agencies are actively seeking systems that combine satellite communication, GPS tracking, sensor integration, and encrypted data exchange to enhance mission effectiveness. This has also led to collaborations between defense technology providers and government bodies to improve interoperability and operational resilience

- Digital warfare and cybersecurity priorities are influencing procurement decisions, with defense organizations emphasizing secure data transmission, cloud-enabled command centers, and AI-driven analytics. These factors are helping armed forces enhance threat detection, optimize troop deployment, and reduce response times in complex operational environments. Companies are increasingly highlighting these advanced capabilities to strengthen competitive positioning and secure long-term defense contracts

- For instance, in 2024, Lockheed Martin in the U.S. and Thales Group in France expanded their battlefield management and command systems by integrating AI-enabled analytics and secure communication modules. These developments were introduced in response to rising demand for real-time intelligence and network-centric operations, with deployment across multiple defense programs. The systems were also positioned as scalable and cyber-resilient solutions, enhancing operational reliability and mission efficiency

- While demand for advanced battlefield management systems is rising, sustained market expansion depends on continuous R&D, cybersecurity reinforcement, and cost-effective system integration. Defense contractors are also focusing on improving scalability, interoperability, and compatibility with legacy systems to support broader adoption across diverse military infrastructures

Battlefield Management Systems Market Dynamics

Driver

Growing Defense Modernization And Demand For Real-Time Situational Awareness

- Rising defense budgets and modernization initiatives are major drivers for the global battlefield management systems market. Governments are increasingly investing in advanced command and control infrastructure to improve operational coordination and strengthen national security. This trend is also pushing innovation in integrated communication networks and intelligent data processing technologies, supporting system diversification

- Expanding applications across land vehicles, unmanned systems, and command centers are influencing market growth. Battlefield management systems help enhance mission planning, troop coordination, and threat monitoring while maintaining secure communication channels, enabling armed forces to meet complex operational objectives. The increasing emphasis on multi-domain operations globally further reinforces this trend

- Defense organizations are actively promoting the adoption of digital command platforms through procurement programs, joint military exercises, and strategic partnerships. These efforts are supported by the growing need for efficient resource utilization and improved combat readiness, and they also encourage collaboration between system integrators and technology developers to enhance system performance and reduce operational risks

- For instance, in 2023, BAE Systems in the U.K. and Northrop Grumman in the U.S. reported expanded deployment of battlefield management solutions within armored vehicle and command center programs. This expansion followed increased demand for network-enabled warfare capabilities and secure data integration, driving improved mission coordination and response efficiency. Both companies also emphasized system interoperability and cybersecurity features to strengthen defense capabilities and operational trust

- Although modernization programs support growth, wider adoption depends on budget allocation, integration complexity, and long-term maintenance planning. Investment in scalable architectures, advanced encryption, and robust testing frameworks will be critical for meeting evolving defense requirements and maintaining strategic advantage

Restraint/Challenge

High Development Costs And Cybersecurity Risks

- The relatively high cost of developing and deploying advanced battlefield management systems remains a key challenge, limiting adoption in budget-constrained defense environments. Complex hardware integration, software customization, and extensive testing procedures contribute to elevated costs. In addition, continuous upgrades and maintenance requirements can further affect long-term expenditure and procurement planning

- Awareness and technical readiness vary across regions, particularly in developing nations where digital defense infrastructure is still evolving. Limited expertise in integrating multi-platform communication systems may restrict rapid implementation. This also leads to slower deployment cycles in regions where advanced training and technological resources are limited

- Cybersecurity and data protection challenges also impact market growth, as battlefield management systems rely heavily on secure communication networks and real-time data exchange. Vulnerabilities in network architecture can pose risks to mission-critical operations. Defense agencies must invest in advanced encryption, threat monitoring, and secure communication protocols to maintain system integrity

- For instance, in 2024, defense integrators in Southeast Asia working with regional armed forces reported slower procurement cycles due to high system costs and concerns regarding cyber resilience. Budget limitations and interoperability challenges with legacy systems were additional barriers. These factors also prompted phased implementation strategies, affecting short-term deployment rates

- Overcoming these challenges will require cost-efficient development strategies, strengthen cybersecurity frameworks, and expanded technical training programs. Collaboration between defense agencies, technology providers, and cybersecurity experts can help unlock the long-term growth potential of the global battlefield management systems market. Furthermore, developing modular and upgradeable platforms while reinforcing digital security standards will be essential for widespread adoption

Battlefield Management Systems Market Scope

The market is segmented on the basis of component, solution, platform, installation type, system, and end user.

- By Component

On the basis of component, the global battlefield management systems market is segmented into Communication Devices, Imaging Devices, Display Devices, Tracking Devices, Computer Hardware Devices, Data Distribution Unit, Night Vision Devices, Software, and Others. The Communication Devices segment held the largest market revenue share in 2025 driven by the critical need for secure, real-time voice and data exchange across military units operating in dynamic environments. These devices ensure encrypted communication between command centers, vehicles, and soldiers, enabling coordinated mission execution. Increasing investments in advanced radio systems, satellite communication modules, and tactical data links further support segment dominance. In addition, interoperability requirements across multi-domain operations are reinforcing the demand for reliable communication infrastructure.

The Software segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing integration of artificial intelligence, data analytics, and cloud-enabled command platforms. Software solutions enable real-time data visualization, predictive threat analysis, and automated decision support, improving battlefield efficiency. Growing focus on cyber-secure architectures and network-centric warfare strategies is accelerating adoption. Continuous upgrades and modular software frameworks are also enhancing scalability and long-term operational adaptability.

- By Solution

On the basis of solution, the market is segmented into Hardware and Software. The Hardware segment accounted for the largest market revenue share in 2025 due to high procurement of ruggedized computing units, advanced sensors, communication terminals, and display systems. Hardware components form the structural backbone of battlefield management systems, ensuring durability and performance under harsh operational conditions. Defense modernization initiatives across major economies are significantly contributing to hardware demand. In addition, replacement of legacy equipment with technologically advanced devices supports consistent revenue generation.

The Software segment is expected to witness the fastest growth rate from 2026 to 2033, supported by rising demand for integrated command dashboards, cybersecurity layers, and AI-driven mission planning tools. Software platforms enhance coordination between multiple defense assets while ensuring real-time situational awareness. Increasing reliance on digital simulations and data-driven operational strategies is further driving growth.

- By Platform

On the basis of platform, the market is segmented into Armored Vehicle, Headquarter and Command Centers, and Soldier Systems. The Armored Vehicle segment held the largest market revenue share in 2025 driven by extensive deployment of communication, navigation, and tracking systems within combat and tactical vehicles. These integrations enhance mobility, coordination, and mission accuracy in complex terrains. Governments are increasingly upgrading armored fleets with digital battlefield solutions to strengthen operational superiority. In addition, integration with unmanned ground vehicles is expanding application scope.

The Soldier Systems segment is expected to witness rapid growth from 2026 to 2033, supported by modernization programs focused on equipping soldiers with wearable communication devices, GPS trackers, and digital display units. These systems improve individual situational awareness and connectivity with command units. Rising emphasis on troop safety and operational efficiency is reinforcing adoption across defense forces.

- By Installation Type

On the basis of installation type, the market is segmented into New Installation and Upgradation. The New Installation segment dominated the market in 2025 due to ongoing procurement of next-generation military platforms and integrated battlefield networks. Countries investing in new defense infrastructure are deploying advanced systems at the initial stage to ensure seamless digital integration. Large-scale modernization programs in developed economies are further strengthening this segment.

The Upgradation segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing need to retrofit existing platforms with advanced communication and command modules. Budget optimization strategies are encouraging phased upgrades rather than complete replacements. This approach enables armed forces to maintain technological relevance while controlling expenditure.

- By System

On the basis of system, the market is segmented into Computing, Communication & Networking, Command & Control, Navigation, Imaging, and Mapping. The Command & Control segment accounted for the largest market revenue share in 2025 as it serves as the central framework for strategic planning, operational monitoring, and coordinated response. Advanced command systems enable data consolidation from multiple sources, improving real-time decision-making. Growing adoption of AI-assisted command centers is strengthening operational precision.

The Communication & Networking segment is expected to witness strong growth from 2026 to 2033, driven by increasing reliance on secure digital communication channels and integrated battlefield networks. Enhanced bandwidth capacity, encrypted data transmission, and satellite-based connectivity are supporting multi-domain operations.

- By End User

On the basis of end user, the market is segmented into Army and Air Force. The Army segment held the largest market revenue share in 2025 driven by extensive deployment of battlefield management systems across ground operations, armored units, and infantry divisions. Land-based missions require robust coordination and communication frameworks, contributing to higher system adoption. Continuous training exercises and modernization initiatives further strengthen this segment.

The Air Force segment is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing integration of advanced navigation, surveillance, and communication systems within aerial operations. Digital command integration between air and ground units is enhancing mission effectiveness. Growing investments in advanced defense aircraft and unmanned aerial systems are further driving adoption within this segment

Battlefield Management Systems Market Regional Analysis

- North America dominated the battlefield management systems market with the largest revenue share of 39.56% in 2025, driven by substantial defense budgets, ongoing military modernization programs, and strong emphasis on network-centric warfare capabilities

- Defense agencies in the region highly prioritize real-time situational awareness, secure communication networks, and integrated command platforms to enhance operational coordination across land, air, and naval forces

- This widespread adoption is further supported by advanced technological infrastructure, presence of leading defense contractors, and continuous investments in AI-enabled and cyber-secure military systems, establishing battlefield management systems as critical assets for modern armed forces

U.S. Battlefield Management Systems Market Insight

The U.S. battlefield management systems market captured the largest revenue share in 2025 within North America, fueled by high defense expenditure and rapid integration of advanced digital command technologies. Military forces are increasingly focusing on strengthening joint operations through secure data exchange, satellite communication, and AI-driven analytics. The growing deployment of integrated systems across armored vehicles, command centers, and soldier platforms further propels market growth. Moreover, continuous research and development initiatives and collaboration with major defense contractors are significantly contributing to the expansion of battlefield management capabilities.

Europe Battlefield Management Systems Market Insight

The Europe battlefield management systems market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by rising geopolitical tensions and increasing defense collaboration among regional nations. The emphasis on strengthening border security and enhancing coordinated multi-domain operations is accelerating adoption. European defense forces are investing in interoperable communication and command platforms to improve mission effectiveness. The region is experiencing steady growth across land and air defense applications, with battlefield management solutions being integrated into both new procurements and modernization projects.

U.K. Battlefield Management Systems Market Insight

The U.K. battlefield management systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by ongoing defense modernization initiatives and the increasing need for secure and efficient command structures. Rising focus on digital transformation within the armed forces is encouraging adoption of integrated communication and control systems. In addition, the U.K.’s commitment to strengthening joint force operations and cybersecurity resilience is expected to continue stimulating market expansion.

Germany Battlefield Management Systems Market Insight

The Germany battlefield management systems market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising investments in advanced defense technologies and emphasis on operational efficiency. Germany’s strong industrial base and focus on innovation promote adoption of secure, interoperable battlefield management platforms across military divisions. Integration of digital command systems within armored and aerial platforms is becoming increasingly prevalent, aligning with national objectives for technological advancement and defense readiness.

Asia-Pacific Battlefield Management Systems Market Insight

The Asia-Pacific battlefield management systems market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing defense budgets, regional security concerns, and rapid modernization of armed forces in countries such as China, Japan, and India. Growing emphasis on enhancing cross-border surveillance and joint operations is accelerating adoption of advanced command and communication systems. Furthermore, expansion of domestic defense manufacturing capabilities is improving accessibility and deployment of battlefield management solutions across the region.

Japan Battlefield Management Systems Market Insight

The Japan battlefield management systems market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s focus on strengthening national security and advancing digital defense infrastructure. The adoption of integrated communication, navigation, and surveillance systems is increasing across defense platforms. Growing investments in technology-driven military solutions and emphasis on interoperability with allied forces are fueling steady market growth in Japan.

China Battlefield Management Systems Market Insight

The China battlefield management systems market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid military modernization, strong government support for defense innovation, and expanding digital warfare capabilities. China is significantly investing in integrated command networks and advanced communication platforms to enhance operational coordination. The push toward intelligentized warfare and development of indigenous defense technologies are key factors propelling the battlefield management systems market in the country.

Battlefield Management Systems Market Share

The Battlefield Management Systems industry is primarily led by well-established companies, including:

- Rolta India Limited (India)

- Cobham Limited (U.K.)

- Collins Aerospace (U.S.)

- Atos SE (France)

- Rheinmetall AG (Germany)

- KONGSBERG (Norway)

- Systematic (Denmark)

- General Dynamics Corporation (U.S.)

- Airbus S.A.S. (Netherlands)

- Rafael Advanced Defense Systems (Israel)

- BAE Systems (U.K.)

- Indra Sistemas (Spain)

- Saab (Sweden)

- Elbit Systems Ltd. (Israel)

- IAI (Israel)

- Leonardo S.p.A. (Italy)

- Lockheed Martin Corporation (U.S.)

- Thales Group (France)

- ASELSAN A.S. (Turkey)

- L3Harris Technologies, Inc. (U.S.)

- Northrop Grumman (U.S.)

Latest Developments in Global Battlefield Management Systems Market

- In March 2024, RTX Corporation, product testing, successfully conducted live-fire exercises for its Lower Tier Air and Missile Defense Sensor (LTAMDS) under the U.S. Army test program. The trials validated radar performance and seamless integration with the Integrated Battle Command System. This development enhances next-generation air and missile defense capabilities and strengthens the company’s position in the battlefield management and integrated air defense market.

- In March 2024, Northrop Grumman, partnership agreement, signed a Memorandum of Understanding with Diehl Defence to support Germany’s layered air and missile defense architecture. The collaboration combines advanced Integrated Air and Missile Defense command capabilities with ground-based defense systems. This move expands international cooperation and reinforces market competitiveness in Europe’s evolving defense landscape.

- In January 2024, BAE Systems, product delivery, delivered the first Amphibious Combat Vehicle Command and Control (ACV-C) variant to the U.S. Marine Corps. The platform functions as a mobile command center, improving operational coordination and situational awareness in combat scenarios. This strengthens modernization initiatives and supports demand for advanced command and control solutions.

- In November 2023, Lockheed Martin Corporation, system integration, integrated the Patriot Advanced Capability-3 (PAC-3) interceptor with the LTAMDS radar to counter air-breathing threats. The solution enhances interoperability with the U.S. Army’s Integrated Battle Command System and improves missile defense precision. This advancement reinforces integrated defense ecosystems and drives innovation within the global battlefield management systems market.

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。