Global Influenza Testing Market Size, Share and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

2.89 Billion

USD

5.50 Billion

2025

2033

USD

2.89 Billion

USD

5.50 Billion

2025

2033

| 2026 –2033 | |

| USD 2.89 Billion | |

| USD 5.50 Billion | |

| % | |

|

Global Influenza Testing Market Segmentation, By Test Type (Traditional Diagnostic Tests and Molecular Diagnostic Tests), Product (Point-Of-Care Testing, Immunodiagnostics, and Molecular Diagnostics), Type-of-Flu (Type A Flu, Type B Flu, and Type C Flu), End User (Hospitals/Clinical Laboratories, Reference Laboratories, and Other End Users) - Industry Trends and Forecast to 2033

Influenza Testing Market Size

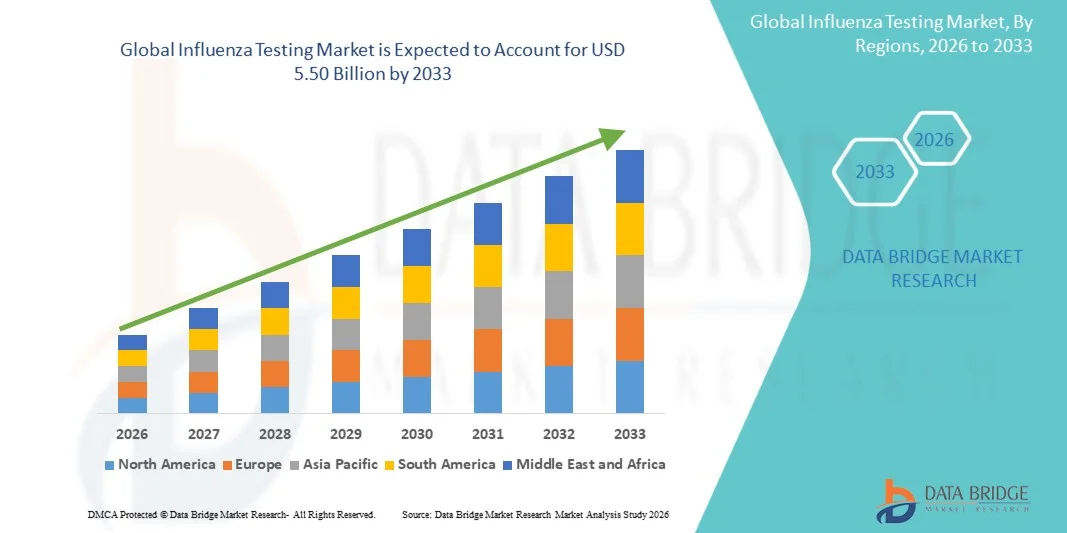

- The global influenza testing market size was valued at USD 2.89 billion in 2025 and is expected to reach USD 5.50 billion by 2033, at a CAGR of 8.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of seasonal influenza and respiratory infections worldwide, driving the need for rapid and accurate influenza testing solutions in hospitals, clinics, and diagnostic laboratories

- Furthermore, rising demand for early diagnosis and timely treatment of influenza, along with growing awareness among healthcare providers and patients, is establishing influenza testing solutions as essential tools for disease management, thereby significantly boosting the market’s growth

Influenza Testing Market Analysis

- Influenza testing, which includes rapid diagnostic tests, molecular assays, and point-of-care solutions, is increasingly becoming essential in both clinical and public health settings due to the need for early and accurate detection of influenza viruses to manage outbreaks and guide treatment decisions

- The escalating demand for influenza testing is primarily driven by the growing prevalence of seasonal influenza, increasing awareness about early diagnosis, and the need for timely antiviral treatment, particularly in hospitals, clinics, and diagnostic laboratories

- North America dominated the influenza testing market with the largest revenue share of 39.5% in 2025, supported by advanced healthcare infrastructure, high adoption of molecular and point-of-care diagnostic solutions, and a strong presence of key industry players in the U.S., which is witnessing substantial growth in influenza testing, especially in hospitals and diagnostic centers

- Asia-Pacific is expected to be the fastest growing region in the influenza testing market during the forecast period, owing to rising healthcare awareness, increasing urbanization, and growing investments in diagnostic infrastructure in countries such as China, India, and Japan

- The Type A Flu segment dominated the largest market revenue share of 62.3% in 2025, due to its higher prevalence, frequent outbreaks, and ability to cause seasonal epidemics

Report Scope and Influenza Testing Market Segmentation

|

Attributes |

Influenza Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Abbott (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Influenza Testing Market Trends

“Enhanced Convenience Through Rapid and Accurate Influenza Testing”

- A significant and accelerating trend in the global Influenza Testing market is the increasing adoption of rapid diagnostic and point-of-care testing technologies, which allow healthcare providers to deliver timely results and make prompt treatment decisions

- For instance, Abbott’s BinaxNOW Influenza A & B Card provides results in just 15 minutes, enabling hospitals and clinics to quickly identify influenza infections and implement necessary interventions

- Multiplex testing panels are also gaining traction, allowing simultaneous detection of multiple respiratory pathogens such as influenza A, influenza B, RSV, and SARS-CoV-2. This trend improves diagnostic efficiency in hospitals, diagnostic laboratories, and research institutions

- The growing preference for molecular diagnostic methods, including RT-PCR and isothermal amplification, reflects the need for high-sensitivity testing, particularly during early-stage infections. For example, Cepheid’s Xpert Xpress Flu/RSV assay enables rapid molecular detection of influenza strains, supporting timely antiviral therapy and infection control measures

- This shift towards faster, more accurate, and multiplexed influenza testing is reshaping healthcare delivery by enabling clinicians to respond more effectively to seasonal flu outbreaks and potential epidemics

- Consequently, demand is rising for influenza diagnostic platforms that combine speed, accuracy, and usability across hospitals, clinical laboratories, and research centers

Influenza Testing Market Dynamics

Driver

“Rising Prevalence of Seasonal Influenza and Respiratory Infections”

- The increasing incidence of seasonal influenza and other respiratory infections is driving demand for reliable and rapid diagnostic tests across hospitals, clinics, and research institutions

- For instance, in the 2022–2023 flu season, the CDC reported over 35 million influenza cases in the U.S., highlighting the need for widespread testing and timely intervention

- Early and accurate detection of influenza enables healthcare providers to initiate antiviral treatments, minimize complications, and reduce the spread of infection, particularly among high-risk populations such as children, elderly, and immunocompromised patients

- The heightened awareness among healthcare providers and patients about the importance of timely influenza detection is further supporting market growth

Restraint/Challenge

“High Costs, Infrastructure Limitations, and Regulatory Hurdles”

- The relatively high cost of advanced influenza testing platforms, especially molecular assays and multiplex panels, remains a significant barrier for adoption in small clinics, rural healthcare centers, and budget-constrained regions

- For instance, Cepheid GeneXpert or BioFire FilmArray systems require substantial investment for both the instrument and consumables, limiting access in emerging markets

- Maintenance, calibration, and supply chain challenges for reagents and consumables add to operational costs and may affect uninterrupted service in diagnostic laboratories

- Regulatory approvals and compliance requirements can slow the introduction of new testing technologies. Ensuring FDA, CE, or WHO certifications for diagnostic assays is necessary but often time-consuming

- Shortage of skilled personnel trained in molecular techniques or multiplex testing can restrict adoption, especially in regions with underdeveloped healthcare infrastructure

- Competition from low-cost rapid antigen tests in emerging markets can limit the adoption of advanced diagnostic assays, even though molecular methods offer higher accuracy and sensitivity

- Seasonal fluctuations in influenza prevalence create variable demand, affecting laboratory resource planning, test utilization, and revenue predictability

- Overcoming these challenges will require cost-effective testing platforms, simplified operational protocols, scalable automation, staff training programs, and streamlined regulatory processes to ensure broader access to accurate and timely influenza diagnostics

Influenza Testing Market Scope

The Influenza Testing market is segmented on the basis of test type, product, type-of-flu, and end user.

• By Test Type

On the basis of test type, the Influenza Testing market is segmented into traditional diagnostic tests and molecular diagnostic tests. The traditional diagnostic tests segment dominated the largest market revenue share of 55.4% in 2025, driven by their long-standing adoption in hospitals and clinical laboratories for rapid influenza detection. These tests, including rapid antigen detection tests (RADTs), are widely used due to low cost, ease of use, and minimal infrastructure requirements. Traditional tests remain popular in primary care and point-of-care settings where immediate diagnosis is critical for timely treatment. The segment benefits from the continued prevalence of influenza outbreaks and seasonal demand. Moreover, their rapid turnaround time and compatibility with existing laboratory workflows enhance adoption globally. Public health programs and government influenza surveillance initiatives also support strong usage of traditional testing methods.

The molecular diagnostic tests segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, fueled by increasing demand for high-sensitivity and high-specificity testing. Molecular methods, such as RT-PCR, detect influenza viral RNA with high accuracy, reducing false-negative results. Hospitals and reference laboratories prefer molecular tests for critically ill patients and immunocompromised populations where precise diagnosis is essential. The rising awareness of rapid and accurate influenza diagnostics, especially following the COVID-19 pandemic, is driving growth. Technological innovations, automation, and multiplexing capabilities that allow detection of multiple viral strains simultaneously are also boosting adoption. Expansion of molecular testing infrastructure in emerging markets supports this high growth trajectory.

• By Product

On the basis of product, the Influenza Testing market is segmented into point-of-care testing, immunodiagnostics, and molecular diagnostics. The point-of-care testing segment dominated the largest market revenue share of 48.9% in 2025, owing to its rapid results, minimal equipment requirements, and suitability for outpatient and emergency settings. POC tests allow clinicians to quickly diagnose influenza and initiate antiviral treatments, improving patient outcomes and reducing transmission. These tests are widely used in hospitals, clinics, and community healthcare settings. Increasing adoption of portable and easy-to-use devices is driving the segment’s dominance. Moreover, the growing prevalence of seasonal influenza and government-supported vaccination programs enhance the need for immediate testing at the point of care.

The molecular diagnostics segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, due to the demand for highly accurate, nucleic acid-based testing solutions. Molecular diagnostics are preferred for complex cases and influenza surveillance programs as they offer high sensitivity and specificity. Hospitals, reference laboratories, and specialized diagnostic centers increasingly rely on molecular tests for precise strain identification. Technological advancements such as real-time PCR, high-throughput platforms, and automated sample processing drive the growth of this segment. The segment is further supported by increased government funding and pandemic preparedness initiatives across the globe.

• By Type-of-Flu

On the basis of type-of-flu, the market is segmented into Type A Flu, Type B Flu, and Type C Flu. The Type A Flu segment dominated the largest market revenue share of 62.3% in 2025, due to its higher prevalence, frequent outbreaks, and ability to cause seasonal epidemics. Type A influenza viruses are associated with significant morbidity and hospitalization, driving continuous demand for diagnostic testing. Hospitals and public health agencies rely heavily on accurate testing for Type A to manage outbreaks effectively. Vaccination programs and antiviral treatment strategies are also primarily targeted toward Type A, further supporting testing adoption. Continuous monitoring for emerging strains and mutations sustains high demand for both traditional and molecular diagnostics.

The Type B Flu segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by increased awareness of its clinical impact, especially in children and older adults. Type B influenza can cause severe illness and hospitalizations, necessitating accurate diagnostics for timely treatment. Rising surveillance efforts, school-based testing programs, and integration with multiplex testing platforms contribute to segment growth. Technological improvements enabling rapid differentiation between Type A and Type B flu are also fueling adoption.

• By End User

On the basis of end user, the Influenza Testing market is segmented into hospitals/clinical laboratories, reference laboratories, and other end users. The hospitals/clinical laboratories segment dominated the largest market revenue share of 51.7% in 2025, driven by high patient volumes and the need for immediate influenza diagnosis. Hospitals rely on both rapid tests and molecular diagnostics to manage seasonal outbreaks and critically ill patients. Access to skilled healthcare professionals and laboratory infrastructure makes hospitals the primary choice for influenza testing. The segment also benefits from insurance coverage for diagnostic procedures and government-supported influenza surveillance programs.

The reference laboratories segment is expected to witness the fastest CAGR of 18.9% from 2026 to 2033, fueled by rising demand for confirmatory and high-complexity testing services. Reference laboratories offer advanced molecular diagnostics, multiplex assays, and strain typing services that hospitals and clinics often outsource. The growth of specialized diagnostic services, pandemic preparedness initiatives, and expansion of laboratory networks in urban and semi-urban regions drive adoption in this segment. Technological advancements and automation in reference labs also improve turnaround time and testing accuracy, supporting strong growth over the forecast period.

Influenza Testing Market Regional Analysis

- North America dominated the influenza testing market with the largest revenue share of 39.5% in 2025, supported by advanced healthcare infrastructure, high adoption of molecular and point-of-care diagnostic solutions, and a strong presence of key industry players in the U.S., which is witnessing substantial growth in influenza testing, especially in hospitals and diagnostic centers

- The widespread availability of advanced laboratory facilities and well-established public health networks is accelerating the adoption of rapid and accurate influenza diagnostics across the region

- Growing awareness about seasonal influenza outbreaks, coupled with robust government-led influenza surveillance programs, is driving the use of molecular and point-of-care testing in clinical settings, including hospitals, diagnostic laboratories, and research institutions

U.S. Influenza Testing Market Insight

The U.S. influenza testing market captured the largest revenue share within North America in 2025, driven by the adoption of molecular diagnostic assays and rapid point-of-care tests in hospitals, clinics, and diagnostic laboratories. The presence of leading diagnostic companies and continuous technological innovations in high-throughput testing platforms is significantly contributing to market expansion.

Europe Influenza Testing Market Insight

The Europe influenza testing market is projected to expand at a substantial CAGR during the forecast period, primarily driven by stringent healthcare regulations, growing demand for rapid diagnostic solutions, and the need for efficient outbreak management. Hospitals and clinical laboratories across the region are increasingly adopting multiplex and molecular influenza tests for timely and accurate disease management.

U.K. Influenza Testing Market Insight

The U.K. influenza testing market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by increased awareness of seasonal influenza and the adoption of point-of-care molecular testing solutions. The U.K.’s well-established healthcare system, alongside strong investments in diagnostic laboratories, is expected to continue supporting market growth.

Germany Influenza Testing Market Insight

The Germany influenza testing market is expected to expand at a considerable CAGR during the forecast period, driven by a growing emphasis on precision diagnostics, the adoption of advanced molecular testing platforms, and government initiatives aimed at enhancing disease surveillance. Hospitals and research laboratories are increasingly integrating automated testing solutions for accurate and rapid influenza detection.

Asia-Pacific Influenza Testing Market Insight

The Asia-Pacific influenza testing market is poised to grow at the fastest CAGR during the forecast period, owing to rising healthcare awareness, increasing urbanization, and growing investments in diagnostic infrastructure in countries such as China, India, and Japan. The expansion of hospitals, clinics, and research facilities, along with government initiatives to strengthen infectious disease surveillance, is driving the adoption of rapid and molecular influenza testing solutions.

Japan Influenza Testing Market Insight

The Japan influenza testing market is gaining momentum due to high healthcare standards, a strong focus on preventive care, and the demand for timely and accurate influenza diagnostics. Hospitals and diagnostic laboratories are adopting advanced molecular and multiplex testing methods, facilitating rapid identification of influenza infections and supporting effective patient management.

China Influenza Testing Market Insight

The China influenza testing market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to expanding healthcare infrastructure, rapid urbanization, and rising investments in diagnostic technologies. Hospitals and diagnostic centers are increasingly integrating rapid antigen, molecular, and multiplex testing platforms to meet the growing demand for accurate influenza detection. Government programs aimed at strengthening disease surveillance and improving public health outcomes further drive market growth.

Influenza Testing Market Share

The Influenza Testing industry is primarily led by well-established companies, including:

• Abbott (U.S.)

• Roche Diagnostics (Switzerland)

• Thermo Fisher Scientific Inc. (U.S.)

• BD (Becton, Dickinson and Company) (U.S.)

• Quidel Corporation (U.S.)

• Luminex Corporation (U.S.)

• bioMérieux S.A. (France)

• Hologic, Inc. (U.S.)

• Siemens Healthineers AG (Germany)

• PerkinElmer, Inc. (U.S.)

• Meridian Bioscience, Inc. (U.S.)

• Danaher Corporation (U.S.)

• Fujirebio Inc. (Japan)

• Nova Biomedical Corporation (U.S.)

• Bio-Rad Laboratories, Inc. (U.S.)

• Becton Dickinson Diagnostic Systems (U.S.)

• Alere Inc. (U.S.)

• Roche Molecular Systems (U.S.)

• Seegene Inc. (South Korea)

• DiaSorin S.p.A. (Italy)

Latest Developments in Global Influenza Testing Market

- In February 2023, the U.S. Food and Drug Administration (FDA) granted Emergency Use Authorization for the Lucira COVID‑19 & Flu Home Test, an over‑the‑counter at‑home diagnostic kit capable of detecting influenza A and B viruses rapidly, expanding accessible influenza testing beyond traditional clinical settings

- In September 2024, Roche launched the cobas® Influenza A/B & RSV test on its cobas® Liat System in the United States, providing a rapid molecular diagnostic solution that delivers accurate influenza A and B results at point‑of‑care settings, improving response time during respiratory disease seasons

- In June 2024, BD (Becton, Dickinson and Company) received the CE Mark approval for its BD MAX Influenza A/B Test, enabling broader access to its molecular influenza diagnostic platform across European markets and strengthening the company’s molecular testing portfolio for respiratory infections

- In January 2025, Roche Diagnostics announced a major deployment contract to expand its cobas influenza A/B testing across centralized laboratory networks in the United States, facilitating broader institutional access to high‑throughput influenza diagnostics

- In March 2025, the global Influenza Diagnostics Market was forecasted to exceed USD 2.0 billion by 2031, driven by rising influenza prevalence, technological advancements in rapid and molecular testing, and increasing point‑of‑care demand, highlighting the expanding role of innovative diagnostics in managing seasonal flu outbreaks

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。