Global Opaque Polymers Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

3.86 Billion

USD

8.59 Billion

2025

2033

USD

3.86 Billion

USD

8.59 Billion

2025

2033

| 2026 –2033 | |

| USD 3.86 Billion | |

| USD 8.59 Billion | |

| % | |

|

Global Opaque Polymers Market Segmentation, By Type (Solid Content 30% and Solid Content 40%), Application (Paints and Coatings, Personal Care, and Detergents)- Industry Trends and Forecast to 2033

Opaque Polymers Market Size

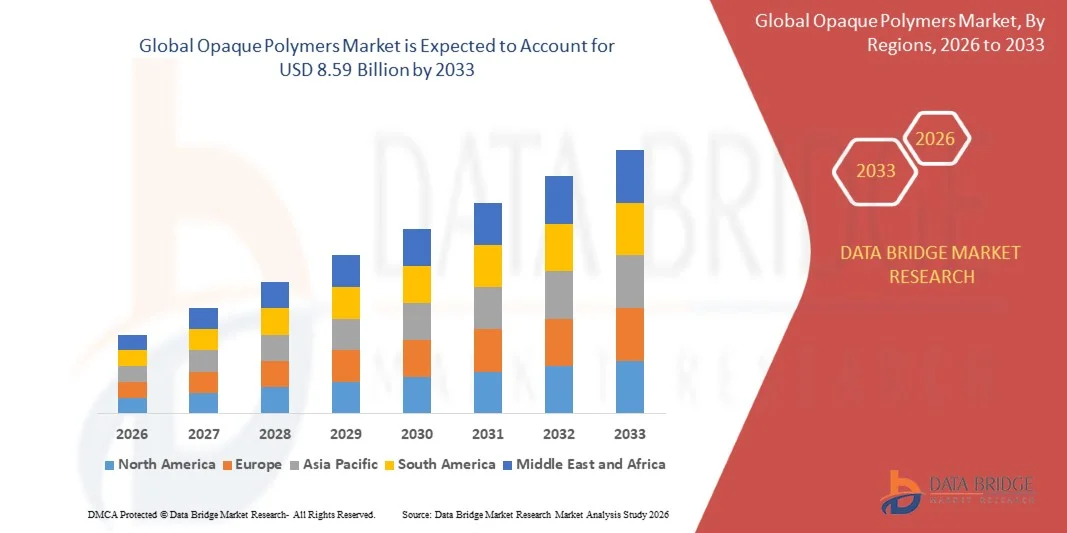

- The global opaque polymers market size was valued at USD 3.86 billion in 2025 and is expected to reach USD 8.59 billion by 2033, at a CAGR of 10.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for lightweight, high-strength, and durable materials across packaging, construction, automotive, and consumer goods industries, which are driving the adoption of opaque polymers

- Rising preference for aesthetic finishes, UV protection, and chemical resistance in products is further supporting the market expansion, encouraging manufacturers to develop innovative formulations and blends

Opaque Polymers Market Analysis

- Increasing adoption of sustainable and recyclable polymer solutions is shaping product development and market trends, as companies strive to meet environmental regulations and consumer demand for eco-friendly materials

- Rapid urbanization, industrialization, and the rising disposable income in emerging economies are contributing to higher demand for opaque polymers in packaging, automotive, and construction applications, reinforcing market growth

- North America dominated the opaque polymers market with the largest revenue share in 2025, driven by increasing demand for high-performance, durable, and aesthetically appealing polymer solutions across paints, coatings, automotive, and packaging industries

- Asia-Pacific region is expected to witness the highest growth rate in the global opaque polymers market, driven by expanding manufacturing industries, rising construction activities, and increasing adoption of advanced polymer applications in paints, coatings, and consumer goods

- The Solid Content 40% segment held the largest market revenue share in 2025, driven by its superior mechanical strength, chemical resistance, and suitability for high-performance applications in paints, coatings, and industrial products. Polymers with higher solid content provide better durability, improved coverage, and enhanced aesthetic finishes, making them a preferred choice for manufacturers seeking long-lasting and visually appealing solutions

Report Scope and Opaque Polymers Market Segmentation

|

Attributes |

Opaque Polymers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Ashland (U.S.) |

|

Market Opportunities |

• Growing Demand For Sustainable And Recyclable Opaque Polymers |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Opaque Polymers Market Trends

“Rising Demand for Durable and Aesthetically Appealing Materials”

• The growing focus on lightweight, high-strength, and durable materials is significantly shaping the opaque polymers market, as manufacturers increasingly prefer polymers that offer superior mechanical properties, chemical resistance, and aesthetic finishes. Opaque polymers are gaining traction due to their ability to enhance product performance without compromising visual appeal, strengthening adoption across packaging, construction, automotive, and consumer goods industries

• Increasing awareness around sustainability, recyclability, and energy-efficient production has accelerated the demand for opaque polymers in food and beverage packaging, household appliances, electronics, and automotive components. Environmentally conscious consumers and regulatory pressures are prompting manufacturers to prioritize eco-friendly polymer solutions, encouraging collaborations between polymer producers and end-use industries to develop innovative applications

• Design and performance trends are influencing purchasing decisions, with manufacturers emphasizing UV protection, thermal stability, and chemical resistance. These factors help brands differentiate products in competitive markets, improve product longevity, and drive the adoption of high-performance opaque polymers

• For instance, in 2024, BASF in Germany and Clariant in Switzerland expanded their opaque polymer product portfolios by launching advanced polymer blends for packaging and automotive applications. These launches were aimed at meeting increasing consumer and industrial demand for durable, lightweight, and visually appealing materials, with distribution across industrial and retail channels

• While demand for opaque polymers is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining performance comparable to alternative materials. Manufacturers are also focusing on improving scalability, supply chain efficiency, and developing innovative formulations that balance cost, quality, and sustainability for broader adoption

Opaque Polymers Market Dynamics

Driver

“Growing Preference for Lightweight, Durable, and Sustainable Materials”

• Rising industrial and consumer demand for high-performance, lightweight, and durable materials is a major driver for the opaque polymers market. Manufacturers are increasingly replacing metals, glass, or conventional plastics with opaque polymers to improve product functionality, reduce weight, and meet sustainability goals

• Expanding applications in packaging, construction, automotive, electronics, and household appliances are influencing market growth. Opaque polymers enhance product strength, durability, and appearance while providing chemical resistance and UV protection, enabling manufacturers to meet evolving consumer and industrial expectations

• Polymer manufacturers are actively promoting advanced opaque polymer solutions through product innovation, certifications, and collaborations with end-use industries to improve performance, reduce environmental impact, and comply with global regulations

• For instance, in 2023, Dow in the U.S. and LyondellBasell in the Netherlands reported increased incorporation of opaque polymers in packaging and automotive components. This expansion followed higher demand for lightweight, durable, and visually appealing materials, driving product differentiation and brand value

• Although rising industrial and consumer trends support growth, wider adoption depends on cost optimization, raw material availability, and scalable production processes. Investment in supply chain efficiency, sustainable sourcing, and advanced polymerization technology will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“Higher Cost and Limited Awareness Compared to Conventional Materials”

• The relatively higher cost of high-performance opaque polymers compared to conventional plastics or metals remains a key challenge, limiting adoption among price-sensitive manufacturers. Higher raw material costs and complex production processes contribute to elevated pricing, affecting market penetration

• Consumer and manufacturer awareness remains uneven, particularly in developing regions where adoption of advanced polymer solutions is still emerging. Limited understanding of performance benefits restricts uptake across certain applications and slows innovation in emerging economies

• Supply chain and distribution challenges also impact market growth, as opaque polymers require consistent quality, proper handling, and adherence to regulatory standards. Logistical complexities and specific storage requirements increase operational costs, especially for high-performance or specialty polymers

• For instance, in 2024, manufacturers in Southeast Asia supplying packaging and automotive industries reported slower uptake due to higher costs and limited knowledge of the functional advantages of opaque polymers. Infrastructure limitations and certification compliance were additional barriers, affecting visibility and adoption

• Overcoming these challenges will require cost-efficient production processes, expanded distribution networks, and focused educational initiatives for manufacturers and end-users. Collaboration with industrial partners, regulatory bodies, and certification agencies can help unlock long-term growth potential in the global opaque polymers market. Developing cost-competitive formulations while highlighting performance and sustainability benefits will be essential for widespread adoption

Opaque Polymers Market Scope

The market is segmented on the basis of type and application.

• By Type

On the basis of type, the opaque polymers market is segmented into Solid Content 30% and Solid Content 40%. The Solid Content 40% segment held the largest market revenue share in 2025, driven by its superior mechanical strength, chemical resistance, and suitability for high-performance applications in paints, coatings, and industrial products. Polymers with higher solid content provide better durability, improved coverage, and enhanced aesthetic finishes, making them a preferred choice for manufacturers seeking long-lasting and visually appealing solutions.

The Solid Content 30% segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by its easier processability, cost-effectiveness, and suitability for applications requiring moderate durability and flexibility. Polymers with lower solid content are particularly popular in personal care and detergent formulations, offering smooth textures, ease of blending, and consistent performance in diverse end-use products.

• By Application

On the basis of application, the opaque polymers market is segmented into Paints and Coatings, Personal Care, and Detergents. The Paints and Coatings segment held the largest market revenue share in 2025, driven by increasing demand for high-performance, durable, and visually appealing coatings across industrial, automotive, and architectural sectors. Opaque polymers enhance adhesion, chemical resistance, and UV protection, making them essential for premium coating formulations.

The Personal Care segment is expected to witness the fastest growth from 2026 to 2033, driven by rising consumer preference for safe, aesthetic, and functional formulations in cosmetics, skincare, and hair care products. Detergents also show steady growth as opaque polymers improve product stability, suspension, and visual appeal, supporting broader adoption across household and industrial cleaning applications.

Opaque Polymers Market Regional Analysis

• North America dominated the opaque polymers market with the largest revenue share in 2025, driven by increasing demand for high-performance, durable, and aesthetically appealing polymer solutions across paints, coatings, automotive, and packaging industries

• Manufacturers in the region highly value the versatility, chemical resistance, and lightweight properties offered by opaque polymers, which improve product quality, durability, and visual appeal across industrial and consumer applications

• This widespread adoption is further supported by robust industrial infrastructure, advanced manufacturing capabilities, and the growing emphasis on sustainable and recyclable polymer solutions, establishing opaque polymers as a preferred material for multiple end-use sectors

U.S. Opaque Polymers Market Insight

The U.S. opaque polymers market captured the largest revenue share in North America in 2025, fueled by rising industrialization and consumer demand for high-performance coatings, packaging materials, and durable consumer products. Manufacturers are increasingly adopting advanced polymer solutions that enhance strength, chemical resistance, and finish quality. Moreover, integration of sustainable and recyclable polymers, along with innovation in polymer blends, is significantly contributing to market expansion.

Europe Opaque Polymers Market Insight

The Europe opaque polymers market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent environmental regulations, increasing adoption of eco-friendly materials, and rising demand for high-performance coatings and packaging solutions. The region is experiencing growth across automotive, construction, and industrial applications, with opaque polymers being incorporated into innovative formulations that improve durability and reduce environmental impact.

U.K. Opaque Polymers Market Insight

The U.K. opaque polymers market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for sustainable and aesthetically appealing polymer solutions in paints, coatings, and consumer goods. In addition, growing focus on lightweight and durable materials is encouraging manufacturers to adopt opaque polymers that combine performance, visual quality, and environmental compliance.

Germany Opaque Polymers Market Insight

The Germany opaque polymers market is expected to witness the fastest growth rate from 2026 to 2033, supported by strong industrial infrastructure, emphasis on innovation, and high awareness of sustainable materials. Manufacturers are integrating advanced opaque polymers into automotive, construction, and industrial coatings, enhancing product performance while meeting environmental and regulatory requirements.

Asia-Pacific Opaque Polymers Market Insight

The Asia-Pacific opaque polymers market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, urbanization, and growing demand for durable and cost-effective coatings, packaging, and consumer products in countries such as China, India, and Japan. Increasing adoption of eco-friendly and high-performance polymers, supported by government initiatives and expanding manufacturing capabilities, is enhancing market penetration.

Japan Opaque Polymers Market Insight

The Japan opaque polymers market is expected to witness significant growth from 2026 to 2033 due to technological advancements, high industrial standards, and strong demand for durable, lightweight, and visually appealing materials. The market emphasizes sustainable and high-performance polymers for automotive, construction, and consumer applications, with manufacturers integrating these solutions to improve efficiency, aesthetics, and product lifespan.

China Opaque Polymers Market Insight

The China opaque polymers market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid industrial growth, increasing urbanization, and high adoption of polymer-based materials in paints, coatings, packaging, and consumer goods. The push for sustainable manufacturing, coupled with strong domestic polymer production capabilities, is driving demand for high-performance opaque polymers across both industrial and residential applications.

Opaque Polymers Market Share

The Opaque Polymers industry is primarily led by well-established companies, including:

• Ashland (U.S.)

• Croda International Plc (U.K.)

• En-Tech Polymer Co., Ltd (China)

• EC21 Inc. (South Korea)

• GUANGZHOU JUNNENG CHEMICALS CO., LTD. (China)

• Organik Kimya (Turkey)

• Dow (U.S.)

• Visen Industries Limited (China)

• Solvay SA (Belgium)

• BASF SE (Germany)

• Evonik Industries AG (Germany)

• Lubrizol Corporation (U.S.)

• Arkema S.A. (France)

Latest Developments in Global Opaque Polymers Market

- In December 2024, Arkema, Acquisition, Arkema acquired Dow’s flexible packaging laminating adhesives business, strengthening its position in the specialty chemicals sector. This strategic move is expected to enhance Arkema’s footprint in the opaque polymers market, particularly in paints and coatings, boosting product offerings, market share, and competitive advantage while supporting growth in high-demand industrial applications

- In October 2022, Aurora Plastics, LLC, Merger, Aurora Plastics merged with Enviroplas Inc., creating a consolidated entity focused on engineered polymers. This merger aims to expand the combined product portfolio, improve customer service, and strengthen market presence in polymer compounds, enabling the company to better cater to evolving industrial and commercial demands

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。