Global Ovarian Cancer Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

5.86 Billion

USD

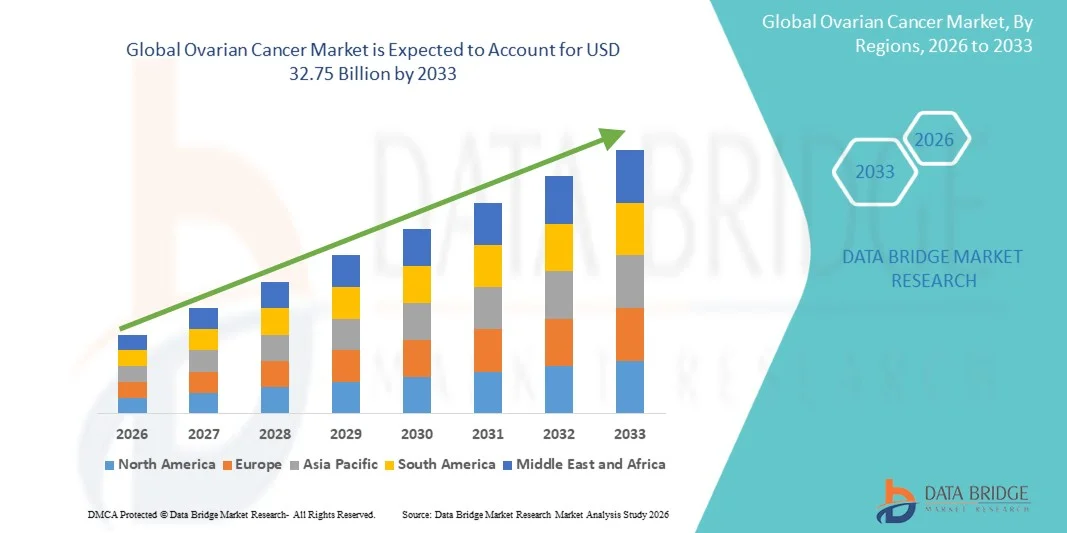

32.75 Billion

2025

2033

USD

5.86 Billion

USD

32.75 Billion

2025

2033

| 2026 –2033 | |

| USD 5.86 Billion | |

| USD 32.75 Billion | |

| % | |

|

Global Ovarian Cancer Market Segmentation, Treatment Type (Chemotherapy, Targeted Therapy, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Speciality Centres, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy) - Industry Trends and Forecast to 2033

Ovarian Cancer Market Size

- The global ovarian cancer market size was valued at USD 5.86 billion in 2025 and is expected to reach USD 32.75 billion by 2033, at a CAGR of 24.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of ovarian cancer worldwide, along with growing awareness regarding early diagnosis and advancements in screening and diagnostic technologies. Continuous progress in targeted therapies, immunotherapy, and personalized medicine is further contributing to improved treatment outcomes and market expansion

- Furthermore, rising demand for effective, safe, and patient-specific treatment options is establishing ovarian cancer therapies as a critical component of modern oncology care. These converging factors are accelerating the uptake of ovarian cancer solutions, thereby significantly boosting growth in the global ovarian cancer market

Ovarian Cancer Market Analysis

- Ovarian cancer therapeutics and diagnostics, including chemotherapy, targeted therapy, immunotherapy, and advanced diagnostic tools, are increasingly vital in modern oncology due to the rising global burden of ovarian cancer and the need for early detection and effective disease management. Continuous advancements in precision medicine and biomarker-based therapies are further enhancing treatment outcomes

- The escalating demand for ovarian cancer solutions is primarily fueled by increasing awareness of early screening, rising healthcare expenditure, and growing adoption of targeted and personalized treatment approaches. These factors are significantly driving the uptake of advanced ovarian cancer therapies across healthcare systems

- North America dominated the ovarian cancer market, accounting for approximately 41% of global revenue in 2025, supported by strong healthcare infrastructure, high adoption of advanced therapies, and significant R&D investments by leading pharmaceutical companies. The U.S. holds the largest share within the region

- Asia-Pacific is expected to be the fastest-growing region in the ovarian cancer market during the forecast period, with a projected CAGR driven by increasing cancer incidence, improving access to healthcare, and rising awareness regarding early diagnosis and treatment

- The parenteral segment dominated the largest market revenue share of 46.3% in 2025, driven by its extensive use in chemotherapy and biologic treatments administered intravenously in hospital settings

Report Scope and Ovarian Cancer Market Segmentation

|

Attributes |

Ovarian Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ovarian Cancer Market Trends

“Advancements in Targeted Therapies and Personalized Medicine”

- A significant and accelerating trend in the global ovarian cancer market is the growing focus on targeted therapies and personalized treatment approaches, which are transforming the way the disease is managed and treated across different patient populations

- For instance, the increasing adoption of PARP inhibitors such as olaparib and niraparib has demonstrated improved progression-free survival in patients with BRCA-mutated ovarian cancer, highlighting the shift toward biomarker-driven therapies

- The integration of genomic profiling and molecular diagnostics is enabling clinicians to identify specific mutations and tailor treatment strategies accordingly, thereby improving treatment efficacy and reducing unnecessary side effects

- Furthermore, the development of combination therapies involving targeted drugs, chemotherapy, and immunotherapy is enhancing overall patient outcomes and expanding treatment options for advanced-stage ovarian cancer

- The rising emphasis on precision medicine is also encouraging pharmaceutical companies to invest in research and development of novel therapeutics that address unmet clinical needs and rare genetic variation

- This trend is reshaping the treatment landscape by moving away from one-size-fits-all approaches toward more individualized and effective care strategies, ultimately improving survival rates and quality of life for patients

Ovarian Cancer Market Dynamics

Driver

“Increasing Incidence and Growing Demand for Early Diagnosis and Treatment”

- The rising global incidence of ovarian cancer, particularly among aging female populations, is a major driver for the market, increasing the demand for effective diagnostic and therapeutic solutions

- For instance, according to global cancer statistics, ovarian cancer remains one of the leading causes of cancer-related deaths among women, prompting governments and healthcare organizations to strengthen screening programs and awareness campaigns

- Advancements in diagnostic technologies, including imaging techniques and biomarker-based tests such as CA-125 and HE4, are enabling earlier detection of the disease, which is critical for improving survival rates

- In addition, increasing awareness among women regarding symptoms and risk factors is encouraging timely medical consultation and diagnosis, thereby boosting treatment adoption

- The expansion of healthcare infrastructure and improved access to oncology care in developing regions are further supporting market growth by ensuring availability of treatment options

- Moreover, ongoing clinical trials and drug approvals are continuously expanding the therapeutic landscape, providing patients with more effective and innovative treatment choices

Restraint/Challenge

“High Treatment Costs and Limited Early Detection in Low-Resource Settings”

- The high cost associated with ovarian cancer treatment, including surgery, chemotherapy, and targeted therapies, remains a significant barrier to market growth, particularly in low- and middle-income countries

- For instance, advanced targeted therapies such as PARP inhibitors and biologics can be expensive and are not always covered under insurance schemes in developing regions, limiting patient access to these life-extending treatments

- Limited availability of effective early screening methods often leads to late-stage diagnosis, reducing the success rate of treatment and increasing the overall burden on healthcare systems

- Disparities in healthcare infrastructure and access to specialized oncology care further restrict timely diagnosis and treatment, especially in rural and underserved areas

- Side effects associated with chemotherapy and targeted treatments can also impact patient adherence and overall treatment outcomes, posing additional challenges

- Addressing these issues through cost reduction strategies, improved screening programs, and expansion of healthcare access will be crucial for ensuring sustainable growth of the ovarian cancer market

Ovarian Cancer Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

• By Type

On the basis of type, the Ovarian Cancer market is segmented into chemotherapy, targeted therapy, and others. The chemotherapy segment dominated the largest market revenue share of 41.9% in 2025, driven by its widespread use as a first-line treatment for ovarian cancer across all stages. Hospitals and specialty centres heavily rely on chemotherapy due to its proven clinical efficacy and established treatment protocols. Oncologists prefer chemotherapy for its ability to reduce tumor size and manage disease progression. Availability of combination regimens enhances treatment outcomes. Strong clinical guidelines and physician familiarity support continued adoption. High patient inflow in oncology centres contributes to segment growth. Insurance coverage for chemotherapy treatments improves accessibility. Continuous advancements in drug formulations enhance tolerability. Integration with surgical interventions strengthens effectiveness. Government cancer programs support chemotherapy usage. Awareness initiatives promote early treatment adoption.

The targeted therapy segment is expected to witness the fastest CAGR of 11.6% from 2026 to 2033, fueled by increasing adoption of precision medicine and therapies such as PARP inhibitors that specifically target cancer cells. Hospitals and specialty centres are rapidly integrating targeted therapies into treatment protocols. Growing awareness among oncologists drives adoption. Advancements in molecular diagnostics enable personalized treatment approaches. Clinical trials demonstrating improved survival rates support growth. Pharmaceutical innovations enhance drug efficacy and safety. Rising investment in oncology research accelerates development. Patient preference for less toxic therapies boosts demand. Emerging markets are witnessing increased access to targeted drugs. Regulatory approvals for new therapies strengthen market expansion. Integration with combination therapies further enhances outcomes.

• By Route of Administration

On the basis of route of administration, the Ovarian Cancer market is segmented into oral, parenteral, and others. The parenteral segment dominated the largest market revenue share of 46.3% in 2025, driven by its extensive use in chemotherapy and biologic treatments administered intravenously in hospital settings. Hospitals and specialty oncology centres prefer parenteral administration for precise dosing and rapid drug delivery. Clinical protocols strongly support IV-based therapies. High effectiveness in advanced-stage cancer reinforces dominance. Integration with supportive care enhances patient outcomes. Physician preference and regulatory approvals support adoption. Monitoring systems in hospitals ensure safety. Increasing number of oncology centres strengthens usage. Patient trust in hospital-administered treatments drives demand.

The oral segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, fueled by increasing availability of oral targeted therapies and growing preference for outpatient treatment. Patients prefer oral medications due to convenience and ease of administration. Homecare and specialty clinics support oral therapy adoption. Pharmaceutical advancements improve bioavailability and effectiveness. Telemedicine facilitates monitoring and prescription. Patient adherence is higher with oral regimens. Awareness programs encourage early and continuous treatment. Emerging markets show strong uptake. Reduced hospital visits further support growth. Cost-effectiveness enhances accessibility.

• By End-Users

On the basis of end-users, the Ovarian Cancer market is segmented into hospitals, homecare, specialty centres, and others. The hospitals segment dominated the largest market revenue share of 48.7% in 2025, driven by availability of advanced oncology infrastructure, skilled professionals, and comprehensive treatment options. Hospitals manage diagnosis, surgery, chemotherapy, and follow-up care under one setting. High patient inflow supports segment dominance. Access to advanced imaging and laboratory diagnostics enhances accuracy. Multidisciplinary oncology teams improve outcomes. Insurance coverage supports hospital-based treatments. Government cancer care programs strengthen hospital infrastructure. Continuous research and clinical trials reinforce adoption. Patient trust and safety drive preference.

The specialty centres segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, fueled by increasing focus on dedicated oncology care and personalized treatment approaches. Specialty centres provide targeted therapies and advanced diagnostics. Rising awareness among patients drives preference for specialized care. Technological advancements support precision medicine. Collaboration with pharmaceutical companies enhances treatment options. Emerging markets show growing number of oncology centres. Patient-centric care models improve outcomes. Shorter waiting times and focused expertise attract patients. Integration with research initiatives accelerates growth.

• By Distribution Channel

On the basis of distribution channel, the Ovarian Cancer market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 44.8% in 2025, driven by direct linkage with hospital treatment protocols and availability of critical oncology drugs. Hospitals ensure immediate access to chemotherapy and targeted therapies. Physician prescriptions are primarily fulfilled through hospital pharmacies. Regulatory compliance ensures drug quality and safety. Strong supply chain management supports availability. Insurance coverage facilitates patient access. High patient trust reinforces dominance. Integration with hospital systems improves efficiency.

The online pharmacy segment is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by growing digital healthcare adoption, convenience, and availability of oncology medications. Increasing smartphone penetration supports online purchases. Patients prefer doorstep delivery for long-term treatment. Telemedicine integration enhances prescription access. Competitive pricing and discounts attract consumers. Awareness of online platforms is increasing. Emerging markets show rapid adoption. Accessibility and convenience sustain growth. Expansion of digital health ecosystems further accelerates demand.

Ovarian Cancer Market Regional Analysis

- North America dominated the ovarian cancer market, accounting for approximately 41% of global revenue in 2025, supported by strong healthcare infrastructure, high adoption of advanced therapies, and significant R&D investments by leading pharmaceutical companies. The region benefits from early diagnosis capabilities, widespread availability of advanced imaging technologies, and strong presence of specialized oncology centers, enabling timely and effective treatment interventions

- For instance, the extensive use of targeted therapies such as PARP inhibitors and combination treatment regimens across the United States has significantly improved patient survival outcomes and accelerated treatment adoption. Favorable reimbursement policies and insurance coverage across the U.S. and Canada further enhance patient access to high-cost therapies, encouraging consistent treatment uptake

- The increasing prevalence of ovarian cancer, particularly among aging populations, along with rising awareness regarding early screening and genetic testing, is further driving demand in the region. In addition, ongoing clinical trials, strong pharmaceutical pipeline, and continuous innovation in precision medicine are reinforcing North America’s leading position in the global market

U.S. Ovarian Cancer Market Insight

The U.S. ovarian cancer market holds the largest share within North America, driven by advanced healthcare infrastructure, high healthcare spending, and rapid adoption of innovative treatment options. The country has a strong presence of leading pharmaceutical companies actively engaged in developing targeted therapies and immunotherapies for ovarian cancer. Increasing use of genetic testing, such as BRCA mutation analysis, is enabling personalized treatment approaches, improving clinical outcomes. In addition, strong awareness programs, early screening initiatives, and favorable reimbursement frameworks are supporting early diagnosis and treatment. The availability of specialized oncology centers and ongoing clinical research further accelerates the growth of the ovarian cancer market in the U.S.

Europe Ovarian Cancer Market Insight

The Europe ovarian cancer market is expected to expand at a substantial CAGR during the forecast period, driven by well-established healthcare systems and increasing focus on cancer research and early diagnosis. Rising incidence of ovarian cancer and growing awareness regarding women’s health are contributing to higher screening and diagnosis rates. Countries such as Germany, the U.K., and France benefit from strong government support, reimbursement policies, and access to advanced treatment options. In addition, increasing adoption of targeted therapies and participation in clinical trials are enhancing treatment outcomes and supporting market growth across the region.

U.K. Ovarian Cancer Market Insight

The U.K. ovarian cancer market is anticipated to grow steadily, supported by the National Health Service (NHS) and ongoing initiatives to improve early cancer detection. Rising awareness campaigns and screening programs are encouraging early diagnosis, which is critical for improving survival rates. The country is also witnessing increased adoption of advanced therapies and personalized medicine approaches. Furthermore, strong research activities and collaborations between academic institutions and pharmaceutical companies are contributing to the development of innovative treatment solutions.

Germany Ovarian Cancer Market Insight

Germany’s ovarian cancer market is expected to expand at a considerable rate due to its advanced healthcare infrastructure and strong emphasis on medical research and innovation. The country has a high number of specialized oncology centers and access to cutting-edge diagnostic and therapeutic technologies. Increasing adoption of targeted therapies and precision medicine approaches is improving patient outcomes. In addition, high healthcare expenditure and supportive government policies are facilitating access to advanced treatments, further driving market growth.

Asia-Pacific Ovarian Cancer Market Insight

The Asia-Pacific ovarian cancer market is projected to be the fastest-growing region during the forecast period, driven by increasing cancer incidence, improving access to healthcare, and rising awareness regarding early diagnosis and treatment. Rapid urbanization, lifestyle changes, and a growing aging population are contributing to the rising burden of ovarian cancer. Governments in countries such as China and India are investing in healthcare infrastructure and expanding cancer care services. In addition, improving availability of diagnostic facilities and cost-effective treatment options is supporting market expansion across the region.

Japan Ovarian Cancer Market Insight

Japan’s ovarian cancer market is witnessing steady growth due to its advanced healthcare system and aging population, which is more susceptible to cancer. The country emphasizes early diagnosis and precision treatment, supported by widespread availability of advanced diagnostic technologies. Increasing adoption of targeted therapies and strong clinical expertise are enhancing treatment outcomes. Government support for cancer research and innovation further contributes to market growth in Japan.

China Ovarian Cancer Market Insight

China ovarian cancer market holds a significant share in the Asia-Pacific Ovarian Cancer market, driven by a large population base, increasing cancer prevalence, and rapid improvements in healthcare infrastructure. The country is experiencing growing adoption of advanced diagnostic technologies and treatment methods, particularly in urban areas. Government initiatives aimed at expanding healthcare coverage and improving cancer care services are further supporting market growth. In addition, rising awareness of early detection and increasing investments in oncology research are strengthening China’s position in the regional market.

Ovarian Cancer Market Share

The Ovarian Cancer industry is primarily led by well-established companies, including:

- Roche (Switzerland)

- AstraZeneca (U.K.)

- Pfizer (U.S.)

- GlaxoSmithKline (U.K.)

- Johnson & Johnson (U.S.)

- Novartis (Switzerland)

- Merck & Co. (U.S.)

- Bristol-Myers Squibb (U.S.)

- AbbVie (U.S.)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Amgen (U.S.)

- Takeda Pharmaceutical (Japan)

- Bayer (Germany)

- Gilead Sciences (U.S.)

- Teva Pharmaceutical (Israel)

- Dr. Reddy’s Laboratories (India)

- Sun Pharma (India)

- Cipla (India)

- Lupin Pharmaceuticals (India)

Latest Developments in Global Ovarian Cancer Market

- In November 2022, the U.S. Food and Drug Administration (FDA) granted accelerated approval to Elahere (mirvetuximab soravtansine), an antibody-drug conjugate (ADC) developed by ImmunoGen (later acquired by AbbVie), for the treatment of folate receptor-alpha (FRα) positive, platinum-resistant ovarian cancer, marking a significant advancement in targeted therapy for difficult-to-treat patients

- In March 2024, the U.S. FDA granted full approval to AbbVie’s Elahere (mirvetuximab soravtansine) for patients with FRα-positive ovarian cancer following positive confirmatory trial results, strengthening the role of antibody-drug conjugates as a key innovation in ovarian cancer treatment

- In March 2024, the FDA approved mirvetuximab soravtansine-gynx (Elahere) based on the Phase 3 MIRASOL trial, demonstrating improved outcomes compared to chemotherapy in platinum-resistant ovarian cancer, further validating targeted ADC therapies in this segment

- In May 2025, the U.S. FDA approved Verastem Oncology’s Avmapki Fakzynja co-pack combination therapy for patients with KRAS-mutated low-grade serous ovarian cancer, representing the first approved treatment for this rare ovarian cancer subtype and addressing a significant unmet clinical need.

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。