Global Phosphodiesterase (PDE) Inhibitors Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

3.66 Billion

USD

5.83 Billion

2025

2033

USD

3.66 Billion

USD

5.83 Billion

2025

2033

| 2026 –2033 | |

| USD 3.66 Billion | |

| USD 5.83 Billion | |

| % | |

|

Global Phosphodiesterase (PDE) Inhibitors Market Segmentation, By Type (Specific, Non-Specific, and Others), Indication (Congestive Heart Failure, Erectile Dysfunction, Inflammatory Airways Disease, and Others), Route of Administration (Oral, Parenteral, and Others), End-Users (Hospitals, Homecare, Specialty Clinics, and Others), Distribution Channel (Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy)- Industry Trends and Forecast to 2033

Phosphodiesterase (PDE) Inhibitors Market Size

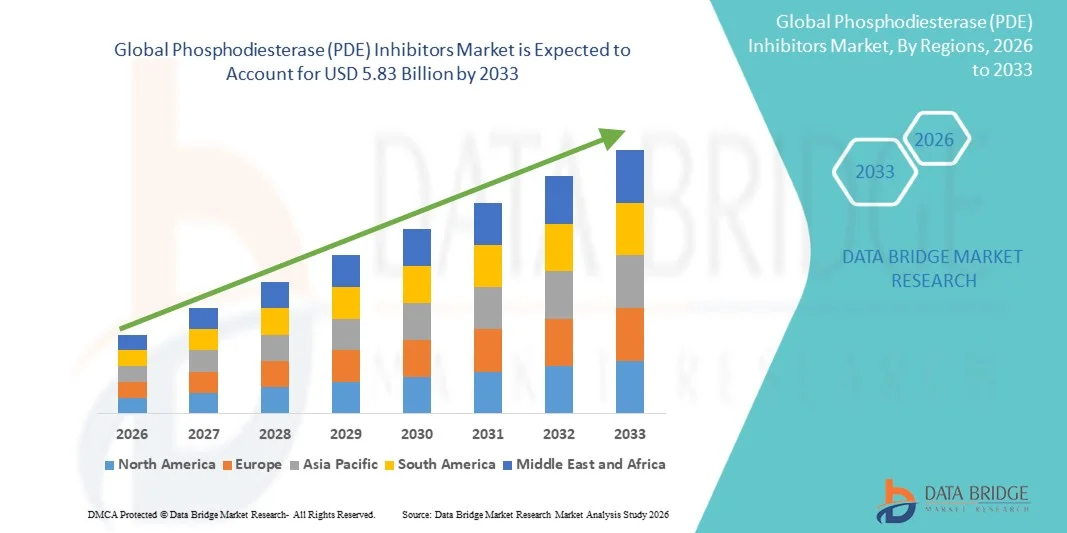

- The global Phosphodiesterase (PDE) inhibitors market size was valued at USD 3.66 billion in 2025 and is expected to reach USD 5.83 billion by 2033, at a CAGR of 6.00% during the forecast period

- The market growth is largely driven by the rising prevalence of chronic conditions such as cardiovascular diseases, respiratory disorders, erectile dysfunction, and neurological conditions, where PDE inhibitors play a critical therapeutic role through targeted enzyme modulation

- Furthermore, increasing R&D investments, ongoing drug development activities, and expanding clinical applications of PDE inhibitors across multiple therapeutic areas are supporting market expansion, alongside growing awareness and adoption of advanced pharmacological treatments in both developed and emerging healthcare systems, thereby significantly boosting the industry's growth

Phosphodiesterase (PDE) Inhibitors Market Analysis

- Phosphodiesterase (PDE) inhibitors, a class of drugs that block specific PDE enzymes to regulate intracellular signaling pathways such as cyclic AMP and cyclic GMP, are widely used in the treatment of cardiovascular diseases, respiratory disorders, erectile dysfunction, and inflammatory conditions due to their targeted mechanism of action and established therapeutic benefits

- The growing burden of chronic diseases, increasing geriatric population, and rising demand for effective long-term pharmacological therapies are key factors driving the adoption of PDE inhibitors, alongside continuous advancements in drug development and expanding clinical research across multiple indications

- North America dominated the PDE inhibitors market with the largest revenue share of 42.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis and treatment rates, strong presence of leading pharmaceutical companies, and widespread utilization of PDE inhibitors across approved indications, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the PDE inhibitors market during the forecast period due to improving healthcare infrastructure, rising healthcare expenditure, growing patient awareness, and increasing prevalence of chronic diseases across emerging economies

- The specific segment dominated the PDE inhibitors market with a significant market share of 58.3% in 2025, owing to their targeted mechanism of action, higher clinical efficacy, and broad usage in key indications such as erectile dysfunction, congestive heart failure, and inflammatory airway diseases, supported by strong prescription rates and established therapeutic profiles

Report Scope and Phosphodiesterase (PDE) Inhibitors Market Segmentation

|

Attributes |

Phosphodiesterase (PDE) Inhibitors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Phosphodiesterase (PDE) Inhibitors Market Trends

“Expanding Therapeutic Applications Beyond Traditional Indications”

- A significant and accelerating trend in the global Phosphodiesterase (PDE) inhibitors market is the expanding exploration of these drugs across emerging therapeutic areas such as pulmonary hypertension, neurological disorders, and inflammatory conditions, enhancing their clinical utility beyond conventional uses such as erectile dysfunction and respiratory diseases

- For instance, PDE5 inhibitors such as sildenafil are increasingly being studied and utilized in pulmonary arterial hypertension management, demonstrating improved vascular relaxation and hemodynamic outcomes in affected patients

- Ongoing research into PDE4 and PDE7 inhibitors is further highlighting their potential in treating inflammatory airway diseases and autoimmune disorders, with clinical trials evaluating their efficacy in modulating immune responses and reducing inflammation. Furthermore, advancements in drug formulations and combination therapies are enabling improved patient outcomes and broader applicability across indications

- The integration of precision medicine approaches and biomarker-driven therapies is facilitating more targeted use of PDE inhibitors, allowing healthcare providers to optimize treatment strategies based on patient-specific conditions. Through continued innovation and pipeline developments, pharmaceutical companies are focusing on next-generation PDE inhibitors with improved selectivity, reduced side effects, and enhanced therapeutic performance, thereby shaping the evolution of the market

- Another emerging trend is the increasing development of novel PDE isoform-specific inhibitors aimed at minimizing off-target effects while improving efficacy, supported by advancements in molecular biology and drug discovery technologies

Phosphodiesterase (PDE) Inhibitors Market Dynamics

Driver

“Growing Demand Driven by Rising Prevalence of Chronic Diseases and Aging Population”

- The increasing prevalence of chronic diseases such as cardiovascular disorders, respiratory illnesses, and erectile dysfunction, coupled with a rapidly aging global population, is a significant driver for the heightened demand for PDE inhibitors

- For instance, in April 2025, several pharmaceutical companies advanced clinical-stage PDE inhibitor candidates targeting inflammatory and cardiopulmonary conditions, reflecting growing investment in expanding therapeutic applications and improving treatment outcomes

- As patients and healthcare providers seek effective long-term pharmacological solutions, PDE inhibitors offer proven efficacy in modulating intracellular signaling pathways, making them a preferred option in multiple indications

- Furthermore, rising awareness of treatment options, improved diagnostic rates, and increasing healthcare access in emerging economies are supporting wider adoption of PDE inhibitors across both developed and developing regions. The growing focus on outpatient care and chronic disease management is further propelling market growth through consistent prescription demand and long-term therapy usage

- Another key driver is the increasing investment in pharmaceutical R&D and clinical trials focused on next-generation PDE inhibitors, which is accelerating innovation and expanding the pipeline of advanced and more selective therapeutic options

Restraint/Challenge

“Side Effects and Regulatory Scrutiny Limiting Market Penetration”

- Concerns related to adverse effects and stringent regulatory requirements pose a significant challenge to broader adoption of PDE inhibitors across certain patient populations. As these drugs act on systemic signaling pathways, they may cause side effects such as headaches, hypotension, and gastrointestinal disturbances, which can impact patient compliance

- For instance, regulatory agencies impose strict approval processes and post-marketing surveillance requirements to ensure safety and efficacy, which can delay product launches and increase development costs for pharmaceutical companies

- Addressing these safety concerns through improved drug selectivity, optimized dosing regimens, and continuous pharmacovigilance is essential for maintaining therapeutic reliability and patient trust. In addition, the availability of alternative treatment options and the presence of generic versions can intensify market competition, potentially limiting revenue growth for branded PDE inhibitor products

- While advancements in drug design and clinical research are gradually mitigating some of these challenges, the need for rigorous safety evaluations and compliance with evolving regulatory standards continues to act as a restraint on rapid market expansion

- Another challenge is the variability in patient response and drug interactions, which can limit the uniform effectiveness of PDE inhibitors and necessitate careful patient monitoring and personalized treatment approaches

Phosphodiesterase (PDE) Inhibitors Market Scope

The market is segmented on the basis of type, indication, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the PDE inhibitors market is segmented into specific, non-specific, and others. The specific segment dominated the market with the largest market revenue share of 58.3% in 2025, driven by its targeted mechanism of action that allows selective inhibition of particular PDE enzymes, leading to improved therapeutic efficacy and reduced off-target effects. Specific PDE inhibitors such as PDE5 inhibitors are widely used in the treatment of erectile dysfunction, pulmonary hypertension, and certain cardiovascular conditions, contributing significantly to their high adoption. The growing preference for precision medicine and targeted therapies further supports the dominance of this segment, as clinicians prioritize drugs with predictable pharmacological profiles and better safety margins. In addition, strong clinical evidence, widespread availability, and established regulatory approvals across multiple indications reinforce the sustained demand for specific PDE inhibitors in both developed and emerging healthcare markets.

The non-specific segment is anticipated to witness the fastest growth rate of 6.8% from 2026 to 2033, driven by their broader mechanism of action that inhibits multiple PDE enzymes simultaneously, making them useful in complex or multifactorial conditions. These inhibitors are increasingly being explored in inflammatory and respiratory disorders where multi-pathway modulation is beneficial. Growing research into combination therapies and the potential for broader therapeutic applications is further accelerating interest in non-specific PDE inhibitors. Moreover, ongoing drug development efforts aimed at improving efficacy and reducing side effects are expected to expand their clinical utility, particularly in cases where selective inhibition alone may not be sufficient.

- By Indication

On the basis of indication, the PDE inhibitors market is segmented into congestive heart failure, erectile dysfunction, inflammatory airways disease, and others. The erectile dysfunction segment dominated the market with the largest revenue share of 46.5% in 2025, primarily due to the high global prevalence of the condition, strong patient awareness, and the widespread use of PDE5 inhibitors such as sildenafil and tadalafil as first-line treatments. The availability of oral formulations, ease of administration, and proven clinical efficacy have made PDE inhibitors the standard of care for erectile dysfunction. In addition, increasing social acceptance and growing healthcare access have contributed to higher diagnosis and treatment rates, particularly in developed economies. The presence of both branded and generic versions has also improved affordability and accessibility, further supporting the dominance of this segment.

The inflammatory airways disease segment is expected to witness the fastest growth rate of 7.2% from 2026 to 2033, driven by the rising prevalence of respiratory conditions such as asthma and chronic obstructive pulmonary disease (COPD). PDE inhibitors, particularly PDE4 inhibitors, are increasingly being utilized for their anti-inflammatory properties in managing airway inflammation. Growing clinical research, regulatory approvals, and expanding use of these drugs in combination therapies are contributing to segment growth. Furthermore, increasing environmental pollution, smoking rates in certain regions, and improved diagnosis of respiratory diseases are fueling demand for advanced treatment options, thereby accelerating the adoption of PDE inhibitors in this segment.

- By Route of Administration

On the basis of route of administration, the PDE inhibitors market is segmented into oral, parenteral, and others. The oral segment dominated the market with the largest revenue share of 72.4% in 2025, driven by the convenience, patient compliance, and non-invasive nature of oral drug delivery. Most widely used PDE inhibitors, including those for erectile dysfunction and cardiovascular conditions, are available in oral formulations, making them the preferred choice for both patients and healthcare providers. The ease of self-administration and widespread availability of oral medications across retail and hospital pharmacies further contribute to the dominance of this segment. In addition, advancements in drug formulation technologies have improved the bioavailability and effectiveness of oral PDE inhibitors, reinforcing their strong market position.

The parenteral segment is expected to witness the fastest growth rate of 6.5% from 2026 to 2033, driven by the increasing use of injectable PDE inhibitors in critical care and hospital settings where rapid therapeutic action is required. Parenteral administration allows for direct delivery into the bloodstream, ensuring faster onset of action, which is particularly beneficial in acute or severe conditions such as pulmonary hypertension and congestive heart failure. Growing adoption of hospital-based treatments, advancements in injectable formulations, and increasing use in emergency and intensive care units are contributing to the growth of this segment.

- By End-Users

On the basis of end-users, the PDE inhibitors market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share of 49.1% in 2025, driven by the high volume of prescriptions, availability of advanced diagnostic facilities, and presence of specialized healthcare professionals. Hospitals are the primary point of care for patients with severe or chronic conditions requiring PDE inhibitor therapy, particularly in cardiovascular and respiratory diseases. The availability of both oral and parenteral administration options in hospital settings further supports the dominance of this segment. In addition, hospitals play a key role in initiating treatment regimens and monitoring patient responses, contributing to consistent demand for PDE inhibitors.

The homecare segment is expected to witness the fastest growth rate of 7.0% from 2026 to 2033, driven by the increasing preference for at-home treatment, rising geriatric population, and advancements in telemedicine and remote patient monitoring. Oral PDE inhibitors, in particular, are well-suited for homecare settings due to their ease of administration and minimal need for clinical supervision. Growing awareness of self-management of chronic diseases and the convenience of long-term therapy at home are encouraging patients to opt for homecare-based treatment. Furthermore, cost-effectiveness and reduced hospital visits are additional factors supporting the rapid expansion of this segment.

- By Distribution Channel

On the basis of distribution channel, the PDE inhibitors market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share of 44.7% in 2025, driven by the high volume of inpatient and outpatient prescriptions originating from hospitals. Hospital pharmacies ensure immediate availability of medications for patients undergoing treatment within healthcare facilities, particularly for acute and chronic conditions requiring supervised care. The integration of hospital pharmacies with prescribing physicians and treatment protocols ensures streamlined drug dispensing and adherence to therapy, contributing to their dominant position in the market.

The online pharmacy segment is expected to witness the fastest growth rate of around 8.1% from 2026 to 2033, driven by increasing digitalization of healthcare services, rising internet penetration, and growing consumer preference for convenient medication purchasing options. Online pharmacies offer advantages such as doorstep delivery, competitive pricing, and easy access to a wide range of PDE inhibitors, particularly for patients managing chronic conditions. The expansion of e-commerce platforms, along with regulatory support for digital health services in several regions, is further accelerating the growth of this segment.

Phosphodiesterase (PDE) Inhibitors Market Regional Analysis

- North America dominated the PDE inhibitors market with the largest revenue share of 42.6% in 2025, supported by advanced healthcare infrastructure, high diagnosis and treatment rates, strong presence of leading pharmaceutical companies

- Patients and healthcare providers in the region benefit from widespread availability of advanced therapeutic options, high diagnosis rates, and established treatment protocols for conditions such as erectile dysfunction, pulmonary hypertension, and cardiovascular disorders where PDE inhibitors are extensively used

- This widespread adoption is further supported by high healthcare expenditure, strong R&D investments, and favorable reimbursement frameworks, along with increasing awareness among patients regarding treatment options, establishing PDE inhibitors as a key component of pharmacological therapy across both residential and clinical settings

U.S. Phosphodiesterase (PDE) Inhibitors Market Insight

The United States dominated the Phosphodiesterase (PDE) inhibitors market with the largest revenue share of 42.6% in 2025, driven by the high prevalence of chronic diseases, advanced healthcare infrastructure, and strong presence of leading pharmaceutical companies across the country Patients and healthcare providers in the region benefit from widespread access to advanced treatment options, high diagnosis rates, and well-established clinical practices for conditions such as erectile dysfunction, pulmonary hypertension, and cardiovascular disorders where PDE inhibitors are extensively utilized. This widespread adoption is further supported by high healthcare expenditure, strong research and development activities, favorable reimbursement policies, and increasing awareness among patients regarding effective pharmacological therapies, establishing PDE inhibitors as a key component of modern treatment protocols

Europe Phosphodiesterase (PDE) Inhibitors Market Insight

The Europe PDE inhibitors market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by the rising burden of chronic diseases, supportive healthcare systems, and increasing adoption of innovative therapies. The region benefits from well-established regulatory frameworks and reimbursement structures that facilitate patient access to PDE inhibitor drugs. Growing awareness of advanced treatment options, along with increasing investments in pharmaceutical research and clinical trials, is further supporting market growth. In addition, the presence of a large aging population and strong emphasis on evidence-based medicine are contributing to the steady uptake of PDE inhibitors across key European countries.

U.K. Phosphodiesterase (PDE) Inhibitors Market Insight

The U.K. PDE inhibitors market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing prevalence of cardiovascular and respiratory conditions, along with growing awareness of erectile dysfunction treatments. The country’s well-developed National Health Service (NHS) ensures broad access to prescription medications, supporting consistent demand for PDE inhibitors. In addition, the U.K.’s strong pharmaceutical sector, combined with ongoing clinical research and adoption of advanced therapies, is contributing to market expansion. Rising patient awareness and early diagnosis of chronic conditions are further encouraging the use of PDE inhibitors in both primary and specialized care settings.

Germany Phosphodiesterase (PDE) Inhibitors Market Insight

The Germany PDE inhibitors market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure, strong focus on innovation, and high prevalence of chronic diseases. Germany’s emphasis on high-quality medical care and access to cutting-edge therapies supports the adoption of PDE inhibitors across multiple indications. The presence of leading pharmaceutical companies and robust R&D activities further strengthens the market landscape. In addition, increasing awareness of chronic disease management and a growing elderly population are driving demand for effective long-term treatment options, contributing to sustained market growth.

Asia-Pacific Phosphodiesterase (PDE) Inhibitors Market Insight

The Asia-Pacific PDE inhibitors market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare expenditure, increasing prevalence of chronic diseases, and improving access to healthcare services in countries such as China, India, and Japan. Rapid urbanization, growing awareness of treatment options, and expanding pharmaceutical manufacturing capabilities are key factors supporting regional growth. Government initiatives aimed at improving healthcare infrastructure and expanding access to essential medicines are further boosting market penetration. In addition, the availability of cost-effective generic PDE inhibitors is making these therapies more accessible to a broader patient population across the region.

Japan Phosphodiesterase (PDE) Inhibitors Market Insight

The Japan PDE inhibitors market is gaining momentum due to the country’s aging population, advanced healthcare system, and high demand for effective treatments for chronic conditions. The increasing prevalence of cardiovascular and respiratory diseases is driving the adoption of PDE inhibitors in clinical practice. Japan’s strong emphasis on innovation and precision medicine is also supporting the development and use of targeted therapies, including PDE inhibitors. Furthermore, the integration of advanced diagnostics and a well-regulated pharmaceutical environment are contributing to consistent market growth, particularly in hospital and specialty clinic settings.

India Phosphodiesterase (PDE) Inhibitors Market Insight

The India PDE inhibitors market accounted for a significant revenue share in Asia-Pacific in 2025, attributed to the country’s large population base, increasing burden of chronic diseases, and growing healthcare awareness. Rapid urbanization, rising disposable incomes, and improved access to healthcare services are driving demand for PDE inhibitor therapies. The expansion of pharmaceutical manufacturing, along with the availability of affordable generic drugs, is making these treatments more accessible to a wider population. In addition, increasing penetration of healthcare infrastructure and growing focus on chronic disease management are key factors propelling market growth in India.

Phosphodiesterase (PDE) Inhibitors Market Share

The Phosphodiesterase (PDE) Inhibitors industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- AstraZeneca PLC (U.K.)

- Sanofi (France)

- GSK plc (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Ltd. (India)

- Lupin Ltd. (India)

- Hanmi Pharmaceutical Co., Ltd. (South Korea)

- CSL Limited (Australia)

- Takeda Pharmaceutical Company Ltd. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Astellas Pharma Inc. (Japan)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Ono Pharmaceutical Co., Ltd. (Japan)

- Amgen Inc. (U.S.)

What are the Recent Developments in Global Phosphodiesterase (PDE) Inhibitors Market?

- In August 2025, Cardurion Pharmaceuticals completed enrollment in two Phase 2 clinical trials (CYCLE-1-REF and CYCLE-2-PEF) evaluating CRD-750, a novel oral PDE9 inhibitor, in patients with chronic heart failure with reduced and preserved ejection fraction, advancing PDE9 modulation as a potential new cardiovascular therapy

- In June 2024, regulatory review documentation confirmed that ensifentrine, a dual PDE3/PDE4 inhibitor under development for respiratory diseases, continued progressing through clinical and regulatory pathways, highlighting ongoing innovation in multi-target PDE inhibitors for airway conditions

- In June 2024, Verona Pharma announced that the U.S. FDA approved Ohtuvayre (ensifentrine), the first-in-class dual PDE3/PDE4 inhibitor for the maintenance treatment of chronic obstructive pulmonary disease (COPD) in adults, marking a major regulatory milestone for PDE inhibitors in respiratory care and offering a novel mechanism of action after decades without new therapies

- In March 2024, FDA documentation reiterated the clinical significance of PDE5 inhibitors such as tadalafil and sildenafil for pulmonary arterial hypertension (PAH) and erectile dysfunction, reinforcing continued therapeutic relevance and regulatory support for these established PDE inhibitor classes

- In March 2024, a Phase II clinical trial protocol was published for roflumilast (a PDE4 inhibitor) investigating its effects on mild cognitive impairment and mild Alzheimer’s disease dementia, indicating expanding research into neurological applications of PDE inhibitors beyond traditional indications

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。