世界の圧電材料市場規模、株式・動向分析レポート

Market Size in USD Billion

CAGR :

%

USD

1.47 Billion

USD

2.16 Billion

2025

2033

USD

1.47 Billion

USD

2.16 Billion

2025

2033

| 2026 –2033 | |

| USD 1.47 Billion | |

| USD 2.16 Billion | |

| % | |

|

グローバル圧電材料市場セグメンテーション、製品(セラミックス、ポリマー、コンポジット、その他)、アプリケーション(アクチュエータ、センサー、モーター、音響デバイス、ジェネレータ、SONAR、トランスデューサなど)、エンドユース(自動車、ヘルスケア、情報&テレコム、消費者財、航空宇宙&防衛など) - 業界動向と予測 2033

グローバル圧電材料市場規模と成長率は?

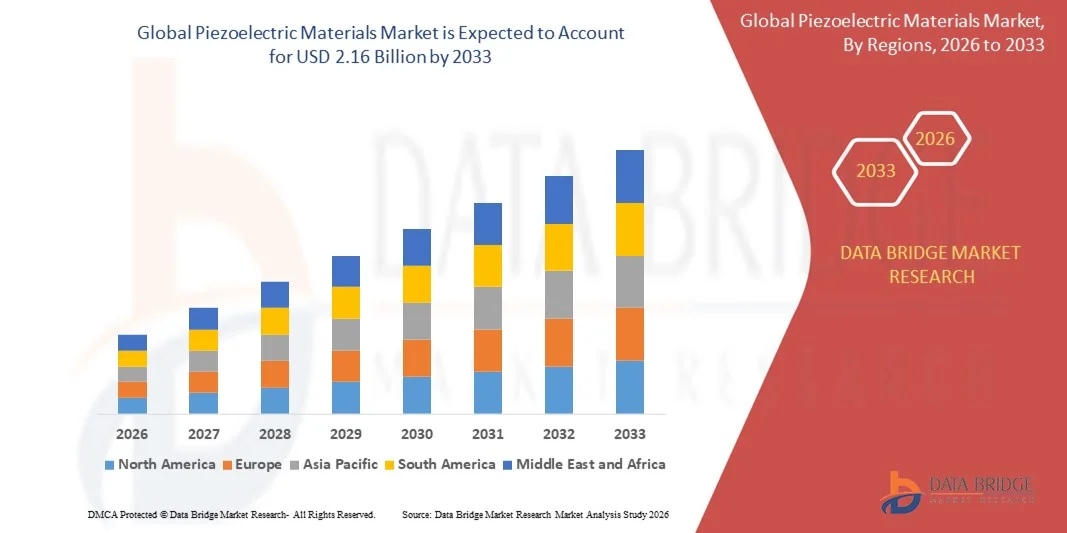

- 世界の圧電気材料の市場規模はで評価されました2025年のUSD 1.47億そして到達する予定2033年までのUSD 2.16億, お問い合わせCAGRの6.88%予報期間中

- 自動車センサー、アクチュエータ、医療用画像機器、産業オートメーション、家電製品、IoT対応機器、スマート材料の継続的な進歩、および小型電子システムにおけるエネルギー効率と高性能電子コンポーネントのライジング要求は、市場成長を牽引する重要な要因の一つです

圧電材料市場の主要なテイクアウトは何ですか?

- 電気自動車、先進医療機器、精密センサー、スマートコンシューマーエレクトロニクスの需要拡大、材料科学の研究開発活動の拡大に伴い、圧電材料市場への大きな成長機会を創出

- しかし、高材料コスト、複雑な製造プロセス、鉛ベースのセラミックスに関する環境問題、高度な材料統合のための熟練した専門知識の限られた可用性は、予測期間にわたって市場成長を抑制する可能性がある重要な課題です

- アジア・パシフィックは、自動車、家電、テレコム、および中国、日本、韓国、インドの産業オートメーション部門の強力な電子機器製造拠点、急速な産業化、そして高い需要によって運転される2025年に35.53%の最大の収益分配と圧電材料市場を支配しました

- 北米は、2026年から2033年までの9.36%の最速のCAGRを登録すると予想され、強力な研究開発活動、先進医療技術の急速な採用、航空宇宙および防衛イノベーション、EV、再生可能エネルギーシステム、および産業オートメーションにおける圧電材料の普及が急速に進んでいます。

- セラミックスセグメントは、2025年の約48%のシェアで市場を支配し、その優れた圧電係数、高い機械的強度、熱安定性、センサー、アクチュエータ、トランスデューサー、および医療超音波装置にわたる幅広い適用性を支持

報告書 スコープおよび圧電材料 市場区分

| アトリビュート | 圧電材料のキー マーケットの洞察 |

| カバーされる区分 |

|

| カバーされた国 | 北アメリカ

ヨーロッパ

アジアパシフィック

中東・アフリカ

南米

|

| 主要市場プレイヤー |

|

| マーケットチャンス |

|

| 付加価値データインフォセットを追加 | 市場価値、成長率、セグメンテーション、地理的カバレッジ、主要なプレーヤーなどの市場シナリオに関する洞察に加えて、Data Bridge Market Researchがキュレーションする市場レポートには、詳細なエキスパート分析、価格設定分析、ブランドシェア分析、消費者調査、デモグラフィ分析、サプライチェーン分析、バリューチェーン分析、原材料/消耗品の概要、ベンダー選定基準、PESTLE分析、ポーター分析、規制フレームワークが含まれます。 |

圧電材料市場の重要な傾向は何ですか。

微細化・高機能化・用途別圧電材へのシフト強化

- 圧電材料市場は、高度なセンサー、アクチュエータ、医療機器、精密電子機器向けに設計されたコンパクト、軽量、高感度材料の採用を目撃しています。

- メーカーは、鉛フリーセラミックス、単結晶、ポリマーベースの圧電気材料にますます焦点を合わせ、持続可能性規制と性能要件を満たす

- 微細な電子部品、MEMS機器、およびウェアラブル技術に対する成長要求は、薄膜とフレキシブルな圧電材料のイノベーションを推進しています。

- たとえば、TDK、CeramTec、PI セラミックス、Solvay、Arkema などの企業は、高効率、アプリケーションに最適化された圧電セラミックス、ポリマーのポートフォリオを拡大しています。

- エネルギー収穫、超音波画像処理、精密運動制御、音響センシングにおける圧電材料の普及が加速する

- 電子システムが小さくなり、よりスマートになり、よりエネルギー効率が向上するにつれて、圧電材料は精密制御、センシング精度、多機能デバイス統合に不可欠です。

圧電材料市場の主要な運転者は何ですか。

- 自動車、ヘルスケア、産業オートメーション、家電分野における高性能センサー、アクチュエータ、トランスデューサーの需要の上昇

- 例えば、2024年~2025年にかけて、EVシステム、先進運転支援システム(ADAS)、医療用画像機器を支える複数のメーカーが圧電材料製剤を強化

- IoTデバイス、ロボティクス、スマート製造システム、精密機器の採用をグローバルに加速

- 材料科学、水晶成長の技術およびポリマー合成物の進歩は感受性、耐久性および温度の安定性を改善しました

- 超音波ベースの診断、最小限の侵襲的な医療機器および宇宙空間センシングシステムの導入の増加は、ボリューム需要を駆動しています

- エレクトロニクス研究開発、医療技術、先端製造に強い投資で支えられた圧電材料市場は、持続的な長期成長を経験することが期待されています

圧電材料市場の成長を望む要因は?

- 高度な圧電気セラミックス、単結晶材料、精密製造プロセスに関連したコストは、コスト感度の高いアプリケーションでの採用を制限します。

- 例えば、2024-2025年の間に、原材料価格の変動とエネルギーコストは、複数のグローバル圧電気材料サプライヤーの生産費に影響

- 高周波、高温、および小型化された適用の複雑さおよび物質的な統合の挑戦の設計は専門にされた専門知識を要求します

- 鉛ベースの圧電気材料に対する環境の懸念と規制上の制限は、コンプライアンスコストと研究開発の負担を増加させます

- 光学や電磁センサーなどの代替センシング技術から競争し、特定のアプリケーションで価格設定圧力を作成します。

- これらの課題を克服するために、企業は鉛フリー素材、スケーラブルな製造、およびアプリケーション固有のカスタマイズに投資し、圧電気材料の幅広い市場採用をサポート

圧電材料市場はどのように区分されますか?

市場は、に基づいてセグメント化されます製品の種類、アプリケーション、エンド使用.

- 製品情報

製品のベースでは、圧電材料の市場は、セラミックス、ポリマー、複合材料、その他に分けられます。 セラミックスセグメントは、2025年の約48%のシェアで市場を支配し、その優れた圧電係数、高い機械的強度、熱安定性、センサー、アクチュエータ、トランスデューサー、および医療超音波装置にわたる幅広い適用性を支持しています。 PZTなどの圧電セラミックスは、自動車システム、産業オートメーション、航空宇宙部品、および消費電子機器で大量生産における信頼性とコスト効率性のために幅広く使用されています。

ポリマーセグメントは、軽量、柔軟性、およびウェアラブルエレクトロニクスの需要を増加させ、2026年から2033年まで最速のCAGRを登録することが期待されます。 医療機器、エネルギー収穫システム、フレキシブルセンサー、IoTアプリケーションにおけるポリマー系圧電材料の普及が加速 素材工学の進歩と鉛フリーの代替品の優先度が高まり、長期的拡張をサポートします。

- 用途別

アプリケーションに基づいて、市場はアクチュエータ、センサー、モーター、音響デバイス、発電機、SONAR、トランスデューサー、その他に分けられます。 センサーセグメントは、自動車安全システム、産業監視、ヘルスケア診断、および消費者電子機器の広範な使用量で、約38~40%の2025の最大の市場シェアを保持しました。 圧・振動・加速・音響センシング用途に理想的な、高感度・高速応答・耐久性を実現。

アクチュエータセグメントは、2026~2033年の間に最速のCAGRで成長し、ロボティクス、半導体製造、航空宇宙システム、医療機器の精度制御の需要が高まっています。 マイクロポジショニングシステム、アダプティブオプティクス、ナノポジショニング技術を採用し、高度なエンジニアリングアプリケーションにおける圧電気アクチュエータの使用を大幅に向上させます。

- エンド使用

エンドユースに基づいて、圧電気材料の市場は自動車、ヘルスケア、情報及び電気通信、消費財、大気および防衛および他に分けられます。 自動車分野は、燃料噴射システム、エンジン管理、ADAS、振動センシング、EVパワートレインコンポーネントの圧電材料の上昇の統合によって駆動され、2025年に約34〜36%のシェアで市場を支配しました。 車両の電動化と厳格な安全基準を増加させ、採用を強化し続けます。

ヘルスケアセグメントは、超音波イメージング、医療センサー、医薬品配信システム、および最小侵襲デバイスにおける圧電気材料の普及により、2026年から2033年までの最速成長を目撃する見込みです。 ヘルスケア投資の拡大、高齢化、技術の進歩は、このセグメントにおける市場成長を加速しています。

圧電材料市場最大のシェアはどの地域ですか?

- アジア・パシフィックは、自動車、家電、テレコム、および中国、日本、韓国、インドを横断する産業オートメーション部門から、強力な電子機器製造拠点、急速な産業化、高需要によって運転され、2025年に35.53%の最大の収益シェアで、圧電材料市場を支配しました。 センサ、アクチュエータ、トランスデューサー、音響部品の製造から、圧電セラミックやポリマーを幅広く使用

- 半導体製造、EV製造、ロボティクス、スマートデバイスへの投資を促進し、5GインフラとIoT導入の拡大に伴い、量産・高機能用途における圧電気材料の燃料供給を継続

- コスト効率の高い製造業、熟練工の可用性、エレクトロニクスおよび先進材料の強力な政府サポートにより、アジア太平洋のグローバル市場におけるリーダーシップを強化

中国圧電材料市場インサイト

中国は、アジア・パシフィックで最大のコントリビューターであり、その優れたエレクトロニクス製造エコシステム、大型自動車生産拠点、スマート製造および再生可能エネルギー技術の積極的な投資によって支持されています。 センサー、超音波装置、エネルギー収穫システムおよび産業オートメーションの圧電気材料の成長の使用は支持された市場成長を運転します。

日本圧電材料市場インサイト

高精度な電子機器、自動車のイノベーション、ロボット、医療機器などへの強い注力により、日本は着実な成長を発揮します。 高度なセラミックスと鉛フリーの圧電材料の継続的な研究開発は、プレミアムアプリケーション全体で長期的な採用をサポートしています。

インドの圧電材料市場の洞察

インドは、エレクトロニクス製造を拡大し、EV導入、ヘルスケア機器製造、政府が支持する「インドでMake in India」イニシアチブを主導し、成長を続ける市場として誕生しています。 センサー、アクチュエータ、医療用超音波機器の需要の増加により、市場浸透を加速します。

北アメリカの圧電気材料の市場

北米は、2026年から2033年までの9.36%の最速のCAGRを登録すると予想され、強力な研究開発活動、先進医療技術の急速な採用、航空宇宙および防衛イノベーション、EV、再生可能エネルギーシステム、および産業オートメーションにおける圧電材料の普及が急速に進んでいます。

米国圧電材料市場インサイト

米国は、強力な半導体研究、医療機器のイノベーション、航空宇宙アプリケーションによる地域成長をリードしています。 精密センサー、アクチュエータ、超音波技術の需要を上げることで、市場拡大が大幅に向上します。

カナダ圧電材料市場インサイト

カナダは、医療診断、産業センシング、クリーンエネルギーアプリケーション、および政府の有益イノベーションプログラムおよび熟練したエンジニアリングの才能によって支えられた学術研究における圧電材料の採用を成長させることによって、着実に、運転しました。

圧電材料市場でトップ企業は?

圧電気材料の企業は主に下記のものを含んでいます:

- PI セラミックス GmbH(ドイツ)

- APCインターナショナル株式会社(米国)

- L3ハリステクノロジーズ株式会社(米国)

- CeramTec(ドイツ)

- アーケマ(フランス)

- ソルベイ(ベルギー)

- スパークラーセラミックス(インド)

- Piezomechanik GmbH(ドイツ)

- 株式会社TDK(日本)

- 香港ピエゾ株式会社(中国)

- ミドテクノロジー(米国)

- Meggitt PLC (米国)

- ホルビガー・モーション・コントロール・ GmbH(ドイツ)

- 株式会社ピエゾキネティックス(米国)

- TRSテクノロジーズ株式会社(米国)

グローバル圧電材料市場における最近の発展とは?

- 2025年2月、CeramTecは、新しいビスマスナトリウムのチタン酸塩-バリウムチタン酸塩(BNT-BT)を基調とした鉛フリーのpiezoceramicを開発し、医療用途に強い可能性を秘め、次世代医療技術のためのサステナブルで高性能な材料に注力

- 2024年12月、PI Ceramicは、多層技術のための完全自動化生産ラインを導入し、約USD 1.08百万を投資し、小シリーズの生産と試作開発を加速し、より高速なサンプルのターンアラウンドと増加した顧客需要を満たすためにより大きな製造の柔軟性を可能にしました

- 2022年10月、PI Ceramicは、ドイツのLederhoseに新しい施設を建設するために約16.24万ドルを投資し、高品質のPiezoコンポーネントの生産能力を50%近く増加させ、グローバル需要を成長させる長期供給能力を強化する動き

- 当社は、2020年4月、自動車用水晶共振器用途向けに設計した4つの新しいクリスタルファミリーを発売し、自動車用電子機器市場での地位を向上し、性能と信頼性を向上しました。

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。