Global Satellite Manufacturing and Launch Market Size, Share, and Trends Analysis Report

Market Size in USD Billion

CAGR :

%

USD

23.58 Billion

USD

29.87 Billion

2025

2033

USD

23.58 Billion

USD

29.87 Billion

2025

2033

| 2026 –2033 | |

| USD 23.58 Billion | |

| USD 29.87 Billion | |

| % | |

|

Global Satellite Manufacturing and Launch Market Segmentation, By Satellite Type (LEO (Lower Earth Orbit) Satellites, MEO (Medium Earth Orbit) Satellites, and GEO (Geosynchronous Equatorial Orbit) Satellites Beyond GEO Satellites), Application (Commercial Communications, Government Communications, Earth Observation Services, Research and Development, Navigation, and Military Surveillance Scientific Applications), End user (Military and Government, and Commercial)- Industry Trends and Forecast to 2033

Satellite Manufacturing and Launch Market Size

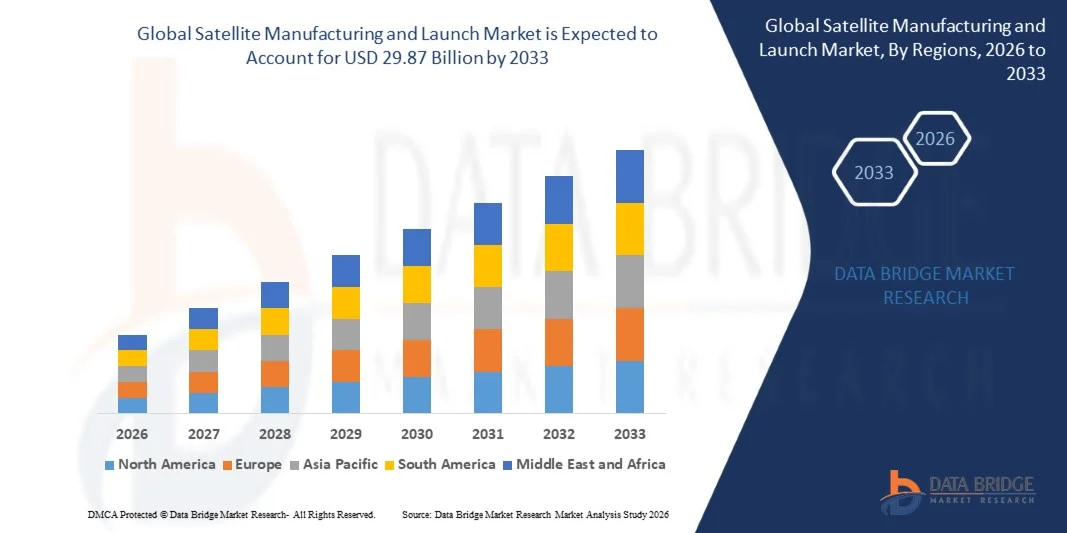

- The global satellite manufacturing and launch market size was valued at USD 23.58 billion in 2025 and is expected to reach USD 29.87 billion by 2033, at a CAGR of 3.00% during the forecast period

- The market growth is largely fuelled by the increasing demand for satellite-based communication, Earth observation, and navigation services across commercial, government, and defense sectors

- Rising investments in space exploration programs and the rapid expansion of low Earth orbit (LEO) satellite constellations for broadband connectivity are further accelerating market development

Satellite Manufacturing and Launch Market Analysis

- The market is experiencing steady growth due to increasing deployment of satellites for telecommunications, remote sensing, climate monitoring, and global navigation applications

- Expanding collaborations between government space agencies and private aerospace companies, along with advancements in miniaturized satellite technologies and cost-efficient launch systems, are expected to strengthen the global satellite manufacturing and launch market during the forecast period

- North America dominated the satellite manufacturing and launch market with the largest revenue share of 40.02% in 2025, driven by strong investments in space exploration, satellite communication infrastructure, and advanced launch technologies

- Asia-Pacific region is expected to witness the highest growth rate in the global satellite manufacturing and launch market, driven by rising investments in national space programs, increasing demand for satellite communication services, and technological advancements across countries such as China, Japan, and India

- The LEO (Lower Earth Orbit) satellites segment held the largest market revenue share in 2025 driven by the rapid expansion of large satellite constellations for broadband connectivity, earth observation, and data communication services. LEO satellites are widely adopted due to their lower latency, reduced launch costs, and suitability for high-speed global internet coverage, particularly in remote and underserved regions

Report Scope and Satellite Manufacturing and Launch Market Segmentation

|

Attributes |

Satellite Manufacturing and Launch Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Airbus S.A.S. (France) |

|

Market Opportunities |

• Expansion Of Low Earth Orbit Satellite Constellations |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Satellite Manufacturing and Launch Market Trends

“Rising Demand for Satellite-Based Communication and Data Services”

• The growing reliance on satellite communication for broadcasting, broadband connectivity, navigation, and remote sensing is significantly shaping the satellite manufacturing and launch market, as governments and private organizations increasingly depend on space-based infrastructure for reliable data transmission. Satellites play a critical role in enabling global communication networks, disaster management, and climate monitoring, encouraging investment in advanced satellite manufacturing technologies and frequent launch missions

• Increasing demand for high-speed internet connectivity in remote and underserved regions has accelerated the deployment of communication satellites, particularly low earth orbit (LEO) constellations. Governments and private space companies are expanding satellite networks to improve global connectivity, support digital transformation, and enable emerging technologies such as Internet of Things (IoT) and 5G integration. This trend is encouraging collaborations between satellite manufacturers, launch service providers, and telecom operators

• Rapid advancements in satellite miniaturization and reusable launch technologies are influencing market development, with manufacturers focusing on producing smaller, cost-efficient satellites capable of delivering high-performance capabilities. Innovations in propulsion systems, payload optimization, and launch vehicle reusability are helping reduce operational costs and increase the frequency of satellite deployments. These advancements are enabling commercial players to participate more actively in the space industry

• For instance, in 2024, SpaceX in the U.S. and OneWeb in the U.K. expanded their satellite constellation deployments to enhance global broadband connectivity. These initiatives involved multiple launch missions and the production of large volumes of small satellites to support high-speed communication networks. The satellites were designed to provide coverage across remote areas, maritime regions, and aviation sectors, strengthening connectivity infrastructure and digital accessibility worldwide

• While the demand for satellite services is rising, sustained market expansion depends on technological innovation, regulatory support, and cost-effective launch solutions. Industry participants are also focusing on improving launch reliability, enhancing payload capabilities, and strengthening supply chain partnerships to ensure efficient satellite manufacturing and deployment at scale

Satellite Manufacturing and Launch Market Dynamics

Driver

“Increasing Demand for Satellite Communication and Earth Observation Services”

• Growing demand for satellite-based communication, navigation, and earth observation services is a major driver for the satellite manufacturing and launch market. Governments, defense agencies, and commercial organizations rely on satellites for applications such as weather forecasting, environmental monitoring, and secure communication. This expanding range of applications is encouraging investments in advanced satellite technologies and new launch capabilities

• Expanding satellite constellations for broadband connectivity, remote sensing, and data analytics are influencing market growth. Satellite systems enable real-time data collection and global communication coverage, supporting industries such as agriculture, maritime, aviation, and disaster management. Increasing digitalization and reliance on satellite-enabled services further strengthen the need for continuous satellite deployment

• Space agencies and private companies are actively promoting satellite programs through strategic partnerships, technology development, and funding initiatives. These efforts are supported by growing government investments in space exploration and national security infrastructure, which also encourage collaboration between satellite manufacturers, launch providers, and research institutions to improve mission efficiency and performance

• For instance, in 2023, Airbus in France and Lockheed Martin in the U.S. reported expanded satellite manufacturing programs for communication and defense missions. The initiatives focused on developing advanced payload systems and improving launch readiness to support national and commercial space projects. Both companies emphasized innovation and reliability in satellite design to strengthen their position in the global space industry

• Although increasing demand for satellite services supports market growth, long-term expansion depends on technological advancements, cost optimization, and streamlined regulatory frameworks. Continued investment in launch infrastructure, satellite production capabilities, and mission planning will be essential to meet the rising demand for space-based services worldwide

Restraint/Challenge

“High Development Costs And Regulatory Complexities In Space Programs”

• The high cost associated with satellite manufacturing, testing, and launch operations remains a major challenge for the market, particularly for smaller companies and emerging space startups. Satellite development involves advanced engineering, specialized materials, and complex integration processes that significantly increase project costs. In addition, launch vehicle expenses and insurance requirements further add to the overall financial burden of space missions

• Regulatory frameworks and licensing requirements also create barriers for satellite deployment, as space activities must comply with national and international regulations governing spectrum allocation, orbital slots, and safety standards. These regulatory complexities can delay project timelines and increase administrative costs for satellite operators and launch providers

• Technical risks related to launch failures, satellite malfunctions, and orbital debris management also impact market growth. Companies must invest heavily in testing, quality assurance, and risk mitigation strategies to ensure mission success. Managing space debris and maintaining satellite longevity in crowded orbital environments have become critical challenges for industry participants

• For instance, in 2024, satellite launch service providers operating in Japan and South Korea reported delays in satellite deployment projects due to licensing approvals, compliance requirements, and rising launch costs. These challenges affected smaller satellite operators aiming to enter the commercial space market and limited the pace of new satellite constellation deployments in the region

• Addressing these challenges will require improved regulatory coordination, cost-efficient manufacturing processes, and innovations in reusable launch technologies. Strengthening international collaboration, enhancing launch reliability, and investing in sustainable space operations will also be essential to support the long-term growth of the global satellite manufacturing and launch market

Satellite Manufacturing and Launch Market Scope

The market is segmented on the basis of satellite type, application, and end user.

• By Satellite Type

On the basis of satellite type, the satellite manufacturing and launch market is segmented into LEO (Lower Earth Orbit) Satellites, MEO (Medium Earth Orbit) Satellites, GEO (Geosynchronous Equatorial Orbit) Satellites, and Beyond GEO Satellites. The LEO (Lower Earth Orbit) satellites segment held the largest market revenue share in 2025 driven by the rapid expansion of large satellite constellations for broadband connectivity, earth observation, and data communication services. LEO satellites are widely adopted due to their lower latency, reduced launch costs, and suitability for high-speed global internet coverage, particularly in remote and underserved regions.

The GEO (Geosynchronous Equatorial Orbit) satellites segment is expected to witness steady growth from 2026 to 2033, supported by their capability to provide continuous coverage over a fixed geographic region. These satellites are commonly used for broadcasting, weather monitoring, and long-distance communication services. Their high orbital altitude allows operators to maintain stable communication links, making them suitable for television broadcasting, defense communication systems, and large-scale data transmission.

• By Application

On the basis of application, the satellite manufacturing and launch market is segmented into Commercial Communications, Government Communications, Earth Observation Services, Research and Development, Navigation, Military Surveillance, and Scientific Applications. The Commercial Communications segment held the largest market revenue share in 2025 driven by the increasing demand for satellite-based broadband services, television broadcasting, and global connectivity solutions. Telecommunications companies and private satellite operators are expanding satellite constellations to enhance network coverage and support high-speed data services across multiple regions.

The Earth Observation Services segment is expected to witness significant growth from 2026 to 2033 due to the increasing use of satellite imagery and data analytics for environmental monitoring, agriculture, disaster management, and urban planning. Satellites equipped with advanced sensors enable real-time monitoring of weather patterns, climate change, and natural resources, supporting government agencies and research organizations in making informed decisions.

• By End User

On the basis of end user, the satellite manufacturing and launch market is segmented into Military and Government, and Commercial. The Military and Government segment held the largest market revenue share in 2025 driven by increasing investments in defense communication systems, surveillance satellites, and national security infrastructure. Governments worldwide are deploying advanced satellites to strengthen intelligence gathering, secure communication networks, and border monitoring capabilities.

The Commercial segment is expected to witness the fastest growth rate from 2026 to 2033 driven by the rapid expansion of private space companies and satellite service providers. Commercial organizations are investing in satellite technologies to deliver broadband internet, earth observation data, and navigation services to various industries, supporting the growth of satellite-based applications in telecommunications, logistics, agriculture, and environmental monitoring.

Satellite Manufacturing and Launch Market Regional Analysis

• North America dominated the satellite manufacturing and launch market with the largest revenue share of 40.02% in 2025, driven by strong investments in space exploration, satellite communication infrastructure, and advanced launch technologies

• Governments and private space companies in the region emphasize innovation, reliable launch capabilities, and the development of satellite constellations for broadband connectivity, earth observation, and defense communication systems

• The presence of leading satellite manufacturers, established launch service providers, and supportive government initiatives further strengthens the regional market. Continuous advancements in reusable launch vehicles, satellite miniaturization, and increasing commercial participation are reinforcing North America’s leadership in the global satellite manufacturing and launch industry.

U.S. Satellite Manufacturing and Launch Market Insight

The U.S. satellite manufacturing and launch market captured the largest revenue share in 2025 within North America, fueled by the rapid expansion of commercial satellite constellations and strong government investment in space programs. The country hosts numerous private space companies and advanced research institutions actively engaged in satellite design, launch services, and space exploration missions. Increasing demand for satellite-based broadband, earth observation data, and defense communication systems continues to support market growth. Moreover, the integration of advanced propulsion systems, reusable launch vehicles, and next-generation satellite technologies is significantly strengthening the country’s position in the global space industry.

Europe Satellite Manufacturing and Launch Market Insight

The Europe satellite manufacturing and launch market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing government investments in space programs and the expanding demand for satellite-based communication and earth observation services. European countries are focusing on strengthening their independent launch capabilities and enhancing satellite manufacturing technologies. The growing emphasis on climate monitoring, navigation services, and secure communication infrastructure is encouraging the development of advanced satellite missions across the region.

U.K. Satellite Manufacturing and Launch Market Insight

The U.K. satellite manufacturing and launch market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in commercial space activities and satellite technology development. The country has been strengthening its space ecosystem through research programs, partnerships with private companies, and the development of spaceports for satellite launches. The growing demand for satellite data services, particularly in telecommunications, earth observation, and environmental monitoring, is further supporting market expansion.

Germany Satellite Manufacturing and Launch Market Insight

The Germany satellite manufacturing and launch market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong engineering expertise and emphasis on advanced aerospace technologies. Germany plays a significant role in satellite manufacturing, particularly in the development of high-precision components and research-driven space missions. Increasing collaboration between aerospace companies, research institutions, and government agencies is accelerating innovation in satellite design, propulsion systems, and space exploration technologies.

Asia-Pacific Satellite Manufacturing and Launch Market Insight

The Asia-Pacific satellite manufacturing and launch market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising investments in national space programs, increasing demand for satellite communication services, and rapid technological advancements in countries such as China, Japan, and India. Governments across the region are prioritizing the expansion of satellite networks to support navigation, disaster management, and digital connectivity initiatives. The growing participation of private space companies and the development of domestic launch capabilities are also strengthening the regional market.

Japan Satellite Manufacturing and Launch Market Insight

The Japan satellite manufacturing and launch market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s strong technological capabilities and continuous investments in space research and development. Japan’s space industry focuses on developing advanced earth observation satellites, navigation systems, and scientific missions. The integration of satellite technologies with disaster monitoring, environmental research, and communication infrastructure is contributing to sustained market growth.

China Satellite Manufacturing and Launch Market Insight

The China satellite manufacturing and launch market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s extensive investments in space infrastructure, satellite manufacturing, and launch vehicle development. China has been actively deploying large satellite constellations to support communication, navigation, and earth observation services. Strong government support, expanding domestic aerospace capabilities, and continuous satellite launch missions are key factors driving the growth of the satellite manufacturing and launch market in China.

Satellite Manufacturing and Launch Market Share

The Satellite Manufacturing and Launch industry is primarily led by well-established companies, including:

• Airbus S.A.S. (France)

• Arianespace (France)

• Blue Origin LLC (U.S.)

• Boeing (U.S.)

• GeoOptics Inc. (U.S.)

• ISISPACE Group (Netherlands)

• Lockheed Martin Corporation (U.S.)

• Northrop Grumman Corporation (U.S.)

• Raytheon Technologies Corporation (U.S.)

• SpaceX (U.S.)

• Thales Group (France)

• Viasat Inc. (U.S.)

SKU-

世界初のマーケットインテリジェンスクラウドに関するレポートにオンラインでアクセスする

- インタラクティブなデータ分析ダッシュボード

- 成長の可能性が高い機会のための企業分析ダッシュボード

- カスタマイズとクエリのためのリサーチアナリストアクセス

- インタラクティブなダッシュボードによる競合分析

- 最新ニュース、更新情報、トレンド分析

- 包括的な競合追跡のためのベンチマーク分析のパワーを活用

調査方法

データ収集と基準年分析は、大規模なサンプル サイズのデータ収集モジュールを使用して行われます。この段階では、さまざまなソースと戦略を通じて市場情報または関連データを取得します。過去に取得したすべてのデータを事前に調査および計画することも含まれます。また、さまざまな情報ソース間で見られる情報の不一致の調査も含まれます。市場データは、市場統計モデルと一貫性モデルを使用して分析および推定されます。また、市場シェア分析と主要トレンド分析は、市場レポートの主要な成功要因です。詳細については、アナリストへの電話をリクエストするか、お問い合わせをドロップダウンしてください。

DBMR 調査チームが使用する主要な調査方法は、データ マイニング、データ変数が市場に与える影響の分析、および一次 (業界の専門家) 検証を含むデータ三角測量です。データ モデルには、ベンダー ポジショニング グリッド、市場タイムライン分析、市場概要とガイド、企業ポジショニング グリッド、特許分析、価格分析、企業市場シェア分析、測定基準、グローバルと地域、ベンダー シェア分析が含まれます。調査方法について詳しくは、お問い合わせフォームから当社の業界専門家にご相談ください。

カスタマイズ可能

Data Bridge Market Research は、高度な形成的調査のリーダーです。当社は、既存および新規のお客様に、お客様の目標に合致し、それに適したデータと分析を提供することに誇りを持っています。レポートは、対象ブランドの価格動向分析、追加国の市場理解 (国のリストをお問い合わせください)、臨床試験結果データ、文献レビュー、リファービッシュ市場および製品ベース分析を含めるようにカスタマイズできます。対象競合他社の市場分析は、技術ベースの分析から市場ポートフォリオ戦略まで分析できます。必要な競合他社のデータを、必要な形式とデータ スタイルでいくつでも追加できます。当社のアナリスト チームは、粗い生の Excel ファイル ピボット テーブル (ファクト ブック) でデータを提供したり、レポートで利用可能なデータ セットからプレゼンテーションを作成するお手伝いをしたりすることもできます。